Receiving a Notice of Incomplete Application often indicates an Incomplete Schedule of Real Estate Owned. This critical document tracks your property assets, mortgages, and rental income for lender evaluation. Accurate disclosure is essential to secure financing and ensure a smooth underwriting process. To help you respond quickly to your lender, below are some ready to use template.

Image cover: Action Required: Completing Your Schedule of Real Estate Owned (Templates Included)

Letter Samples List

- Notice of Incomplete Application Letter Regarding Schedule of Real Estate Owned

- Missing Real Estate Owned Schedule Incomplete Application Letter

- Incomplete Mortgage Application Letter for Omitted Schedule of Real Estate Owned

- Schedule of Real Estate Owned Deficiency Letter for Incomplete Application

- Notice of Incomplete Mortgage Application Letter Missing Real Estate Owned Information

- Incomplete Real Estate Owned Schedule Notice Letter

- Pending Mortgage Application Letter for Incomplete Schedule of Real Estate Owned

- Request for Completed Schedule of Real Estate Owned Letter

- Action Required Letter for Incomplete Schedule of Real Estate Owned

- Incomplete Application Letter Missing Schedule of Real Estate Owned Documentation

- Outstanding Real Estate Owned Schedule Application Notice Letter

- Mortgage File Suspended Letter for Incomplete Schedule of Real Estate Owned

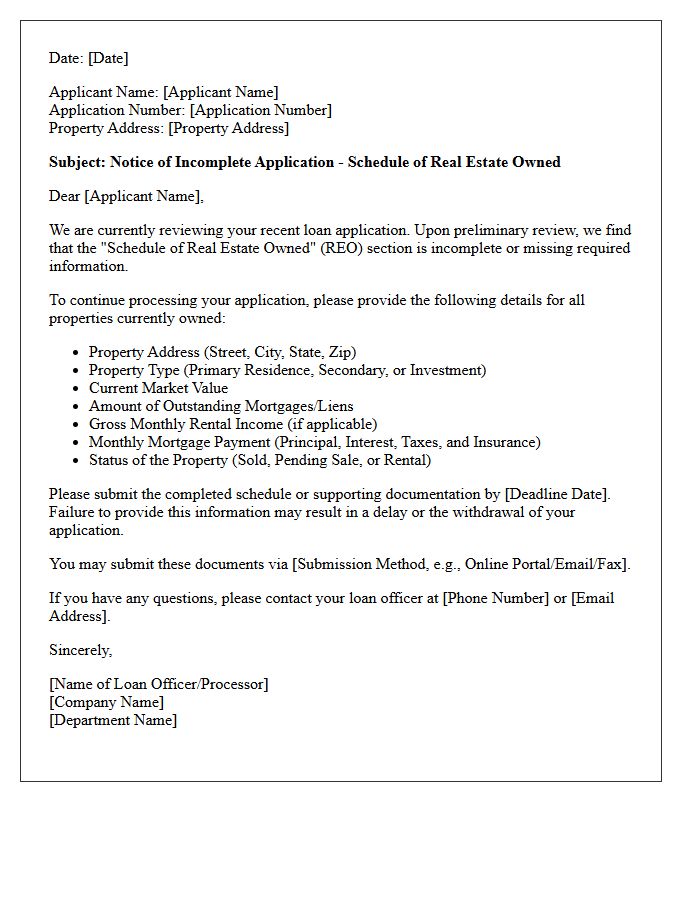

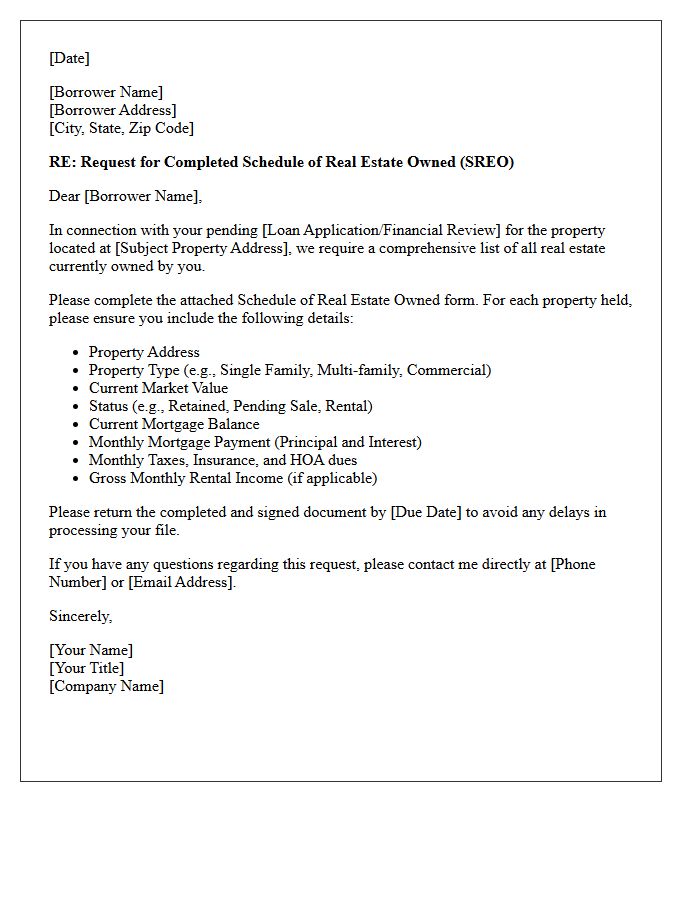

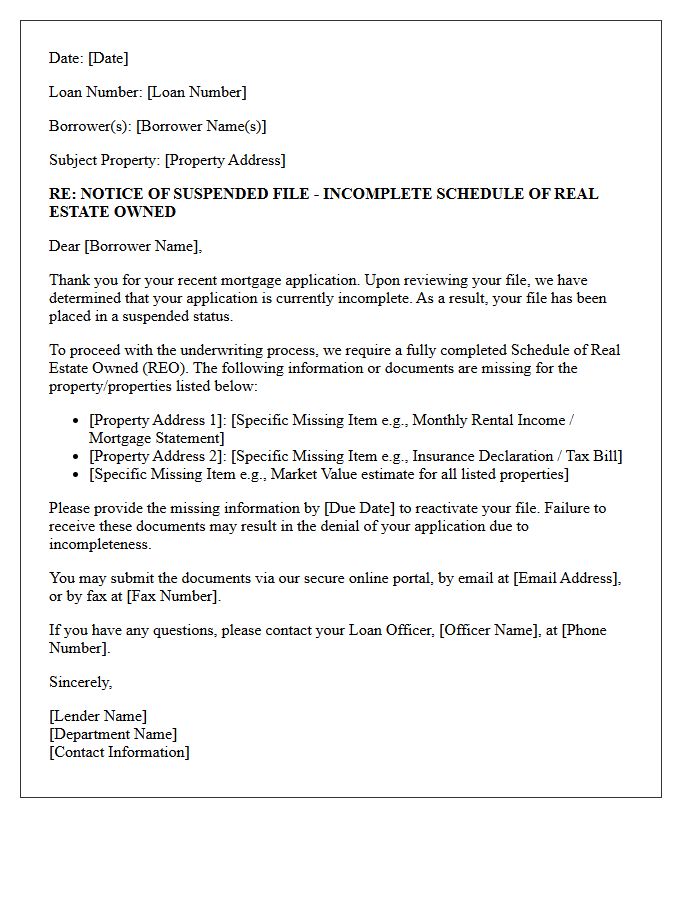

Notice of Incomplete Application Letter Regarding Schedule of Real Estate Owned

Receiving a notice of incomplete application indicates your Schedule of Real Estate Owned (SREO) is missing or contains errors. This essential document lists all properties you currently hold, including their market value, mortgage balances, and rental income. Lenders use this data to calculate your debt-to-income ratio and total liabilities. To avoid processing delays, ensure every field is accurate and matches your supporting financial statements. Promptly providing the corrected schedule is vital for maintaining your mortgage application timeline and securing final loan approval.

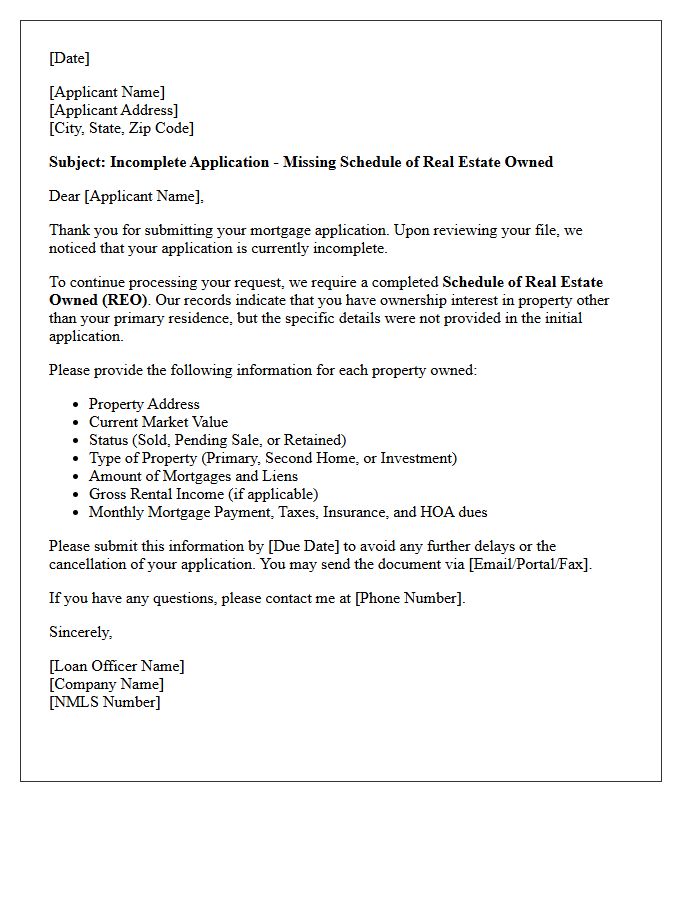

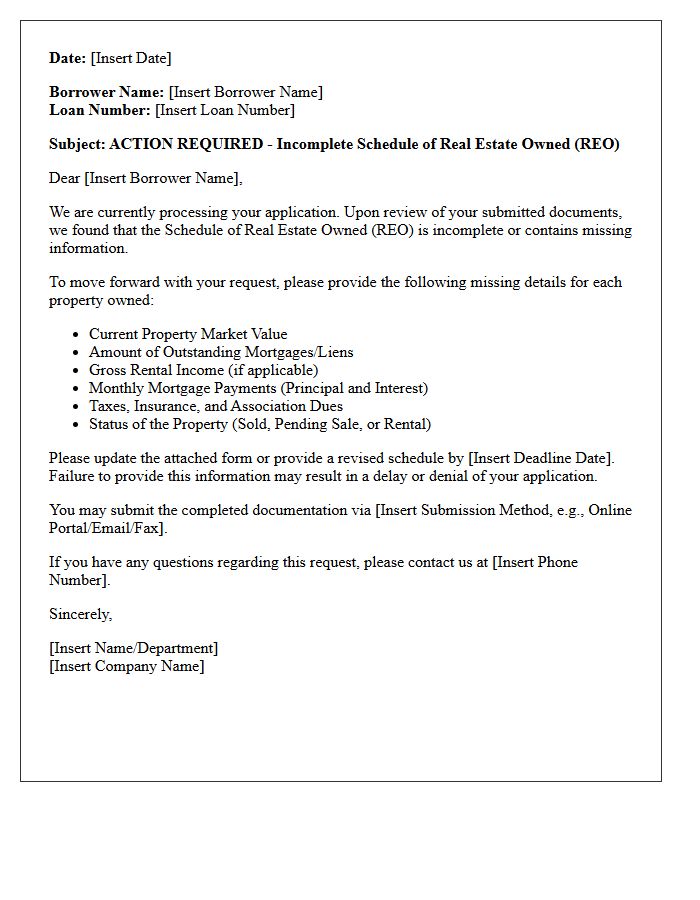

Missing Real Estate Owned Schedule Incomplete Application Letter

A Missing Real Estate Owned (REO) Schedule letter signifies an incomplete mortgage application. Lenders require a detailed list of all currently owned properties to accurately calculate your debt-to-income ratio and assess financial risk. This document must include property values, outstanding mortgage balances, and monthly carrying costs. Failing to provide a comprehensive REO schedule causes significant underwriting delays. To ensure a smooth approval process, submit a complete Schedule of Real Estate Owned immediately to verify your total liabilities and rental income potential.

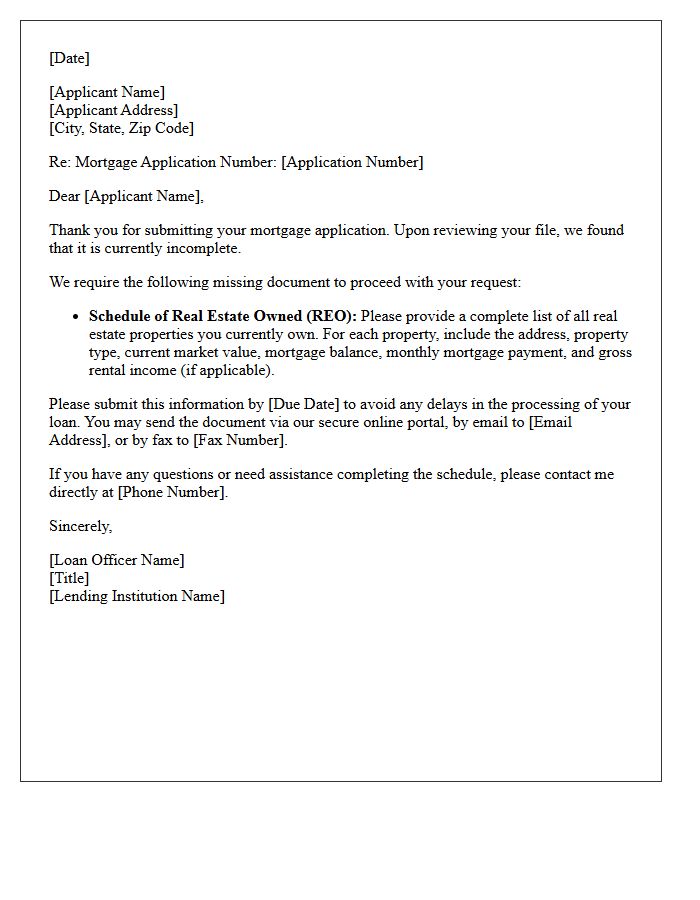

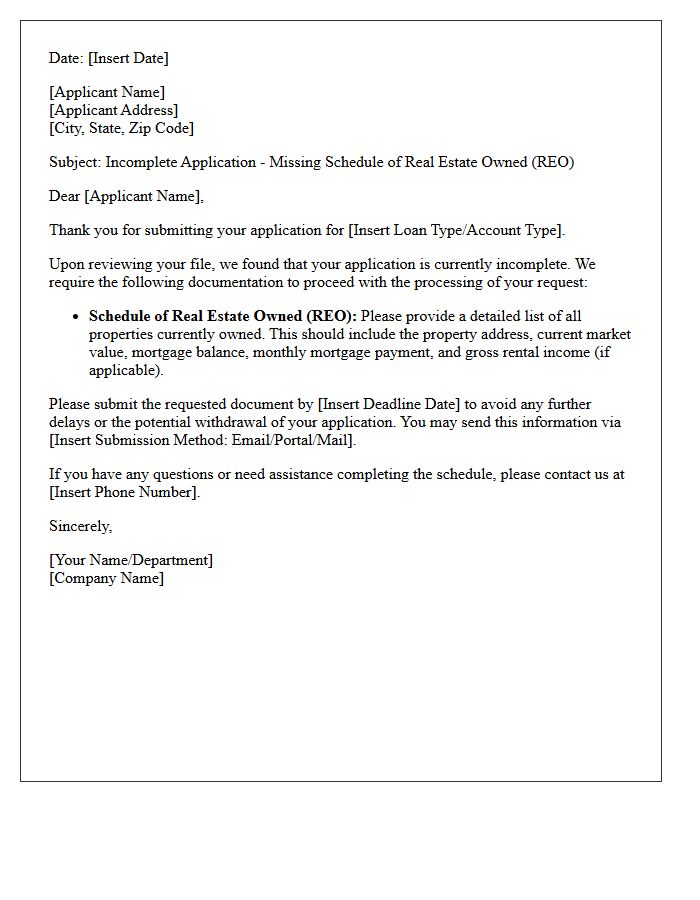

Incomplete Mortgage Application Letter for Omitted Schedule of Real Estate Owned

Receiving an incomplete mortgage application letter often indicates a missing Schedule of Real Estate Owned. This essential document lists all properties you currently own, including their market value, mortgage balances, and rental income. Lenders require this data to calculate your debt-to-income ratio and assess financial risk accurately. To avoid processing delays, you must promptly provide a detailed list of addresses, property types, and associated expenses. Ensuring this schedule is comprehensive allows the underwriter to verify your liquidity and overall creditworthiness, moving your loan toward final approval.

Schedule of Real Estate Owned Deficiency Letter for Incomplete Application

A Schedule of Real Estate Owned (REO) Deficiency Letter signifies that your mortgage application is incomplete due to missing property details. Lenders require comprehensive data for every owned property, including market value, mortgage balances, and rental income. To avoid processing delays, ensure your REO schedule matches your credit report and tax returns exactly. Addressing these documentation gaps promptly is critical for accurate debt-to-income calculations and final loan approval. Failure to provide specific addresses or lien information will halt the underwriting process until the deficiency is resolved.

Notice of Incomplete Mortgage Application Letter Missing Real Estate Owned Information

A Notice of Incomplete Mortgage Application indicates your lender cannot process your loan without detailed Real Estate Owned (REO) information. This section requires a full disclosure of all properties you currently own, including their market value, outstanding mortgage balances, and monthly carrying costs. Providing accurate REO data is essential for lenders to calculate your debt-to-income ratio and overall financial risk. To avoid processing delays or a formal application denial, you must submit a complete schedule of real estate holdings promptly to satisfy underwriting requirements and move toward final approval.

Incomplete Real Estate Owned Schedule Notice Letter

An Incomplete Real Estate Owned (REO) Schedule Notice is a formal request from a lender for missing property data. This letter identifies gaps in your financial disclosure, such as omitted market values, mortgage balances, or rental income details. Failure to provide a comprehensive schedule can delay loan approval or cause application rejection. To ensure compliance, you must list all owned properties accurately, including taxes and insurance costs. Providing a complete, verified document is essential for lenders to assess your debt-to-income ratio and overall creditworthiness during the underwriting process.

Pending Mortgage Application Letter for Incomplete Schedule of Real Estate Owned

A Pending Mortgage Application Letter notifies borrowers that their loan process is stalled due to an Incomplete Schedule of Real Estate Owned (SREO). This critical document must list all properties currently held, including market values, outstanding mortgage balances, and rental income. Lenders require this to accurately calculate your Debt-to-Income ratio and verify liquidity. Failing to provide a comprehensive SREO prevents the underwriter from assessing financial risk, leading to significant funding delays. Ensure every column is filled and matches supporting tax returns or mortgage statements to resume the approval process.

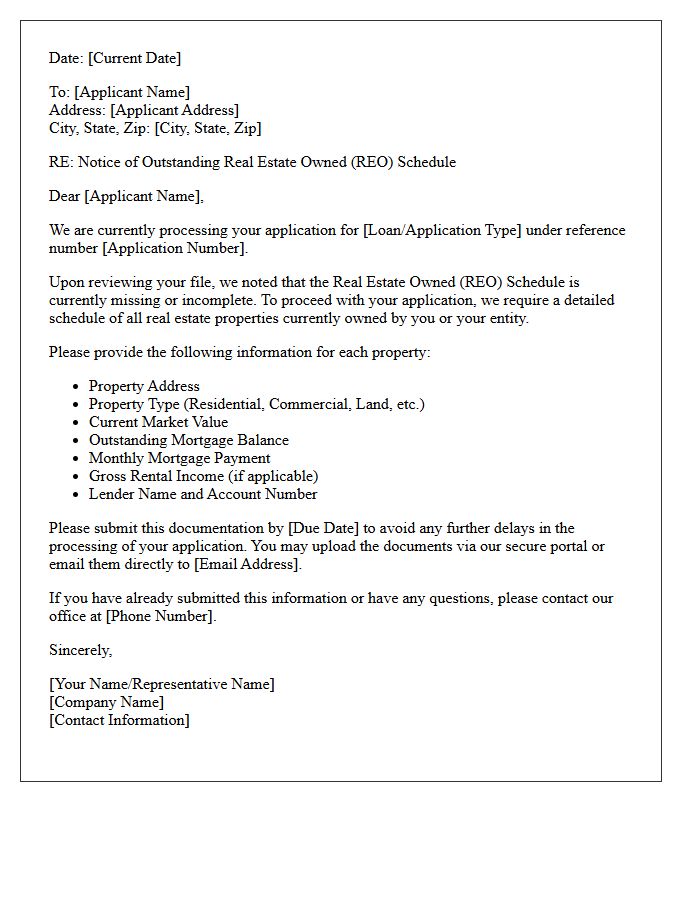

Request for Completed Schedule of Real Estate Owned Letter

A Request for Completed Schedule of Real Estate Owned Letter is a formal document used by lenders to verify a borrower's property portfolio. It requires detailed information regarding existing mortgage balances, taxes, insurance, and rental income for all held assets. Providing an accurate schedule is essential for calculating the debt-to-income ratio and evaluating overall financial risk during the underwriting process. Ensuring consistent data across all financial statements helps prevent delays in loan approval and ensures a transparent assessment of your real estate investment performance.

Action Required Letter for Incomplete Schedule of Real Estate Owned

An Action Required Letter for an incomplete Schedule of Real Estate Owned (REO) indicates that your mortgage application lacks critical details regarding properties you currently own. To prevent funding delays, you must promptly provide missing information such as current market values, outstanding mortgage balances, monthly tax payments, and insurance premiums. Lenders use this data to calculate your debt-to-income ratio and verify liquidity. Ensure all addresses and lien details match your credit report exactly to satisfy underwriting requirements and secure final loan approval.

Incomplete Application Letter Missing Schedule of Real Estate Owned Documentation

An incomplete application letter regarding missing Schedule of Real Estate Owned documentation is a formal notice that your mortgage file lacks critical property data. This highlighted requirement mandates a detailed list of all currently held properties, including their market values, outstanding debt, and rental income. Failure to provide this REO schedule promptly will stall the underwriting process and risk loan denial. Ensure every address, tax liability, and insurance premium is accurately documented to demonstrate your total debt-to-income ratio and financial stability to the lender.

Outstanding Real Estate Owned Schedule Application Notice Letter

An Outstanding Real Estate Owned Schedule Application Notice Letter is a formal request from lenders to mortgage applicants. It requires a detailed REO schedule disclosing all currently owned properties, including their market value, mortgage balances, and rental income. Accurate completion is essential for calculating the Debt-to-Income (DTI) ratio and assessing financial risk. Failure to provide this verification can delay loan processing or lead to application denial. Ensure all property data aligns with credit reports to maintain transparency during the underwriting phase of your real estate transaction.

Mortgage File Suspended Letter for Incomplete Schedule of Real Estate Owned

A mortgage file suspended letter indicates your loan application is on hold due to an incomplete Schedule of Real Estate Owned. Lenders require full transparency regarding your existing properties to calculate the debt-to-income ratio and net rental income accurately. You must provide missing details, such as current market values, outstanding mortgage balances, and monthly insurance or tax costs for all owned real estate. Promptly submitting this updated schedule is essential to resolve the underwriting suspension and move your mortgage toward final approval.

What is a Notice of Incomplete Application for an Incomplete Schedule of Real Estate Owned?

A Notice of Incomplete Application is a formal request from a lender stating that your mortgage application cannot be processed because the Schedule of Real Estate Owned (REO) section is missing required details or documentation for properties you currently own.

What specific information is required on the Schedule of Real Estate Owned?

The Schedule of Real Estate Owned must include the property address, current market value, outstanding mortgage balance, monthly gross rental income, and the total monthly expenses, including taxes, insurance, and homeowners association (HOA) fees for every property held.

Why does the lender need a complete Schedule of Real Estate Owned?

Lenders require a complete REO schedule to accurately calculate your Debt-to-Income (DTI) ratio, verify your total liabilities, and assess the net rental income or losses associated with your existing real estate portfolio.

How do I resolve a notice regarding an incomplete REO schedule?

To resolve the notice, you must update your loan application with the missing property details and provide supporting documents, such as recent mortgage statements, property tax bills, insurance declarations, and current lease agreements for all owned properties.

Will an incomplete Schedule of Real Estate Owned delay my loan approval?

Yes, an incomplete REO schedule will pause the underwriting process. Underwriters cannot issue a final approval or "Clear to Close" until all real estate liabilities and associated carrying costs are fully documented and verified.

Comments