Receiving a Notice of Incomplete Application due to unresolved credit report inquiries can delay your financing goals. Lenders require clarification on recent credit activity to assess your total debt obligations accurately. Promptly addressing these inquiries is essential for loan approval and maintaining a healthy financial profile. To simplify your response, below are some ready to use templates.

Image cover: Resolving Incomplete Applications: Credit Inquiry Clarification Templates and Guide

Letter Samples List

- Notice of Incomplete Application: Unresolved Credit Inquiries Letter

- Letter Requesting Explanation of Recent Credit Inquiries

- Outstanding Credit Inquiry Resolution Letter

- Pending Mortgage Application: Unresolved Credit Report Inquiries Letter

- Notice of Action Required: Credit Inquiry Explanation Letter

- Letter of Incomplete Mortgage Application Due to Credit Inquiries

- Undisclosed Credit Inquiry Clarification Letter

- Mortgage Application Suspension: Unresolved Credit Inquiries Letter

- Letter of Notice Regarding Missing Credit Inquiry Documentation

- Credit Report Inquiry Discrepancy and Incomplete Application Letter

- Request for Unresolved Credit Inquiry Details Letter

- Incomplete Loan Application Credit Inquiry Notice Letter

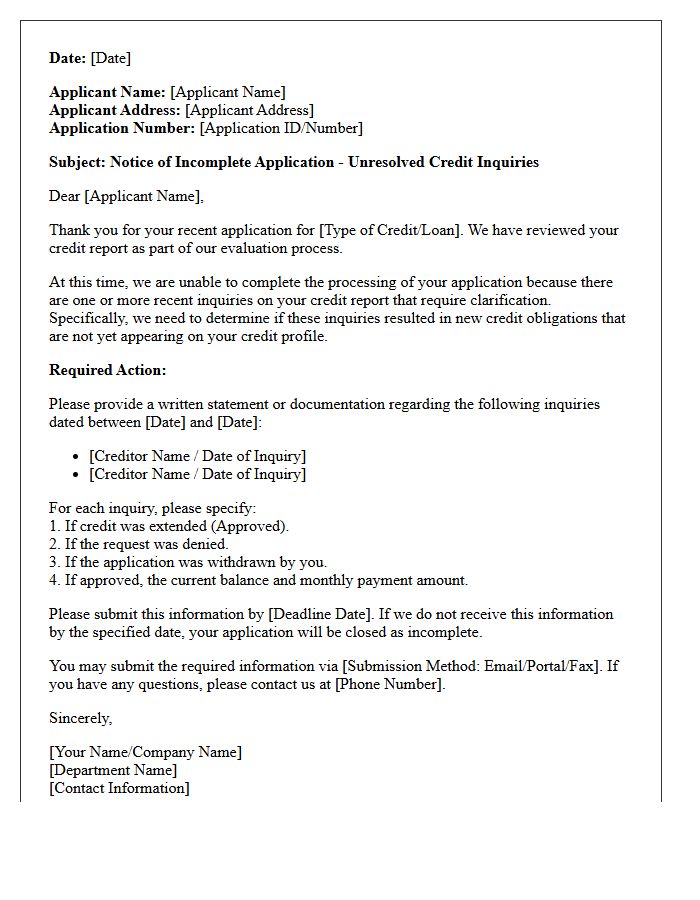

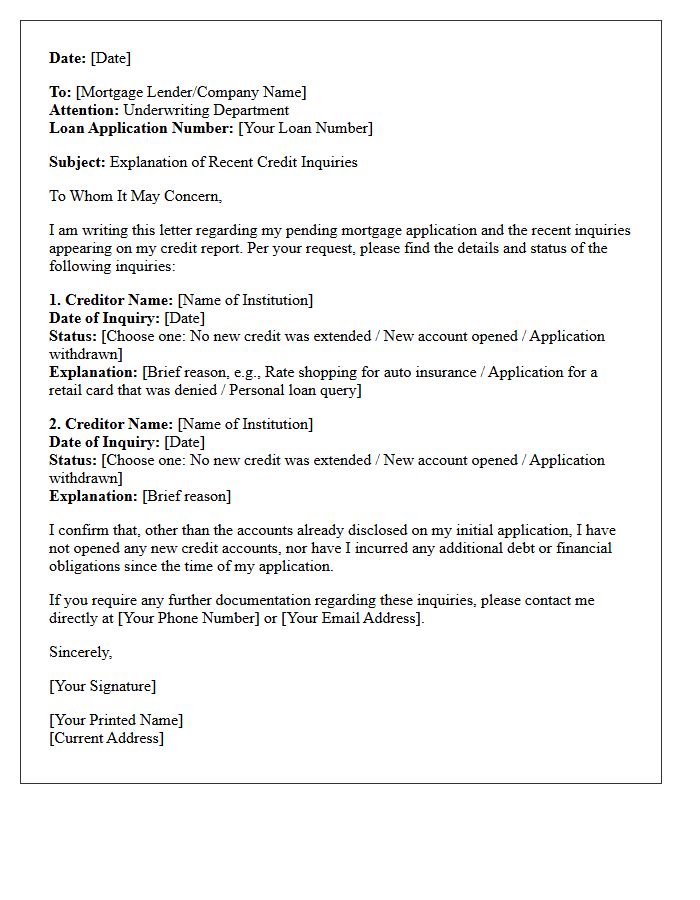

Notice of Incomplete Application: Unresolved Credit Inquiries Letter

A Notice of Incomplete Application regarding unresolved credit inquiries is a formal request from a lender requiring clarification on recent credit activity. To move forward, you must explain whether these inquiries resulted in new debt or additional credit lines. This ensures your debt-to-income ratio remains accurate for underwriting. Failure to provide a detailed letter of explanation promptly can lead to a formal denial. Always disclose if an inquiry led to a new account, as transparency is vital for final loan approval and risk assessment.

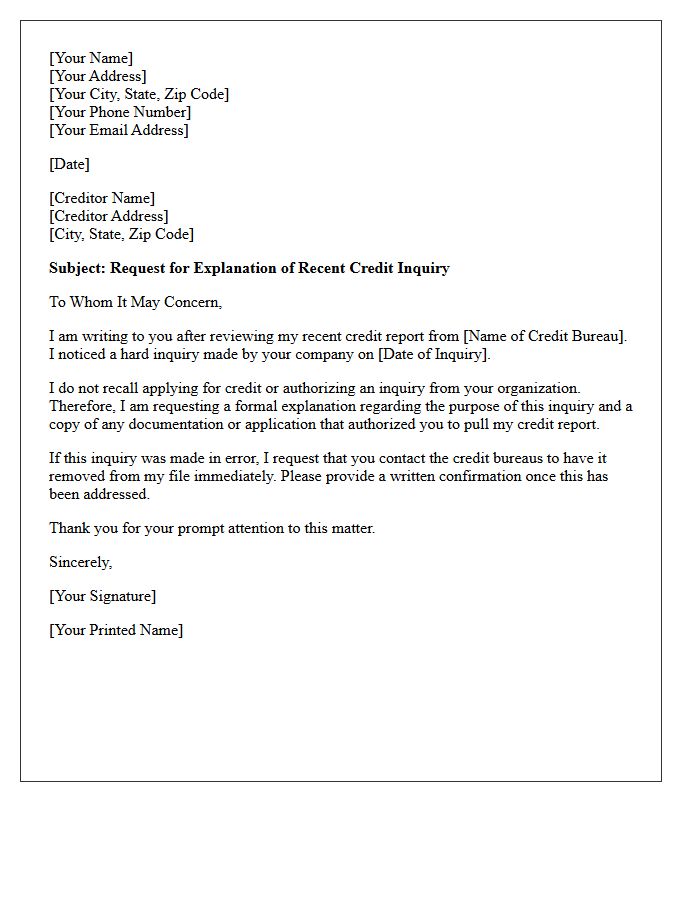

Letter Requesting Explanation of Recent Credit Inquiries

A Letter Requesting Explanation of Recent Credit Inquiries is a formal document sent to creditors or credit bureaus to clarify why specific credit checks were performed on your profile. This is essential for fraud prevention and maintaining a healthy credit score, as excessive hard inquiries can lower your rating. By demanding verification for each inquiry, you ensure that only authorized applications are recorded. If a lender cannot provide valid proof of your consent, you have the legal right to request the removal of the unauthorized entry from your credit report.

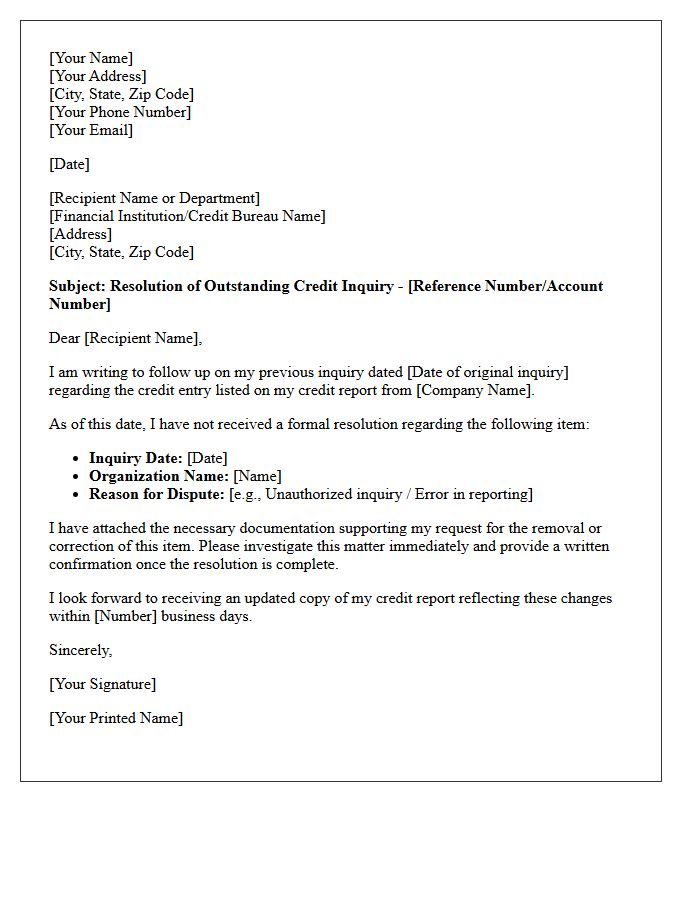

Outstanding Credit Inquiry Resolution Letter

An Outstanding Credit Inquiry Resolution Letter is a formal document used to dispute unauthorized or excessive hard pulls on your credit report. Unrecognized inquiries can lower your credit score and suggest potential identity theft. To resolve this, send a written request to the credit bureau and the inquiring creditor, demanding proof of authorization or immediate removal. Clearly state that the inquiry was not permitted under the Fair Credit Reporting Act (FCRA). Resolving these disputes helps restore your creditworthiness and ensures your financial profile accurately reflects your borrowing history.

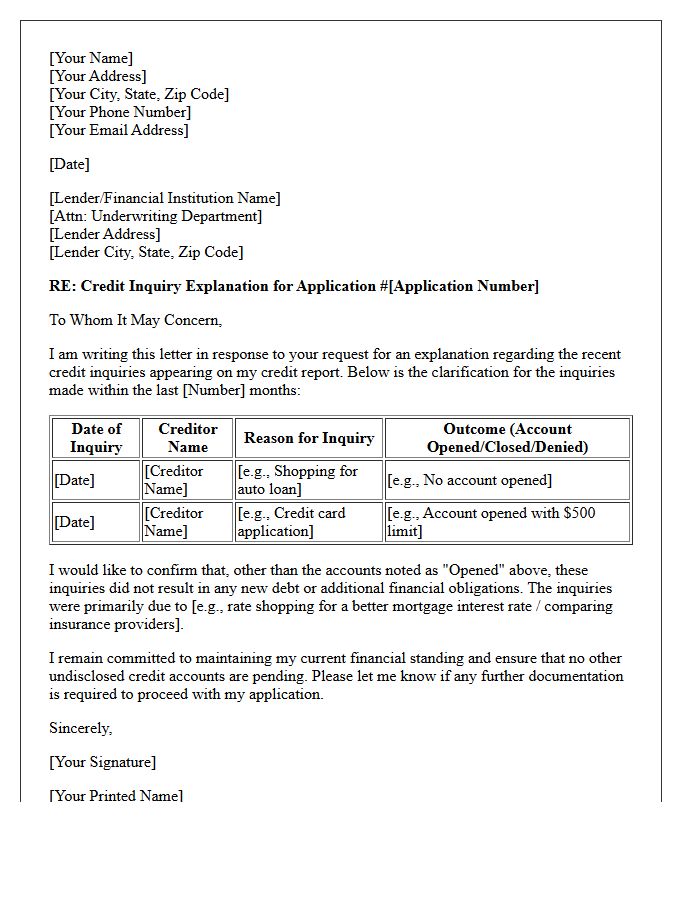

Pending Mortgage Application: Unresolved Credit Report Inquiries Letter

When processing a pending mortgage application, lenders often require an unresolved credit report inquiries letter to clarify recent financial activity. You must provide a written explanation for every hard inquiry made within the last 90 days. The primary goal is to confirm whether these inquiries resulted in new debt that could impact your debt-to-income ratio. If no account was opened, explicitly state that no new credit was extended. Providing clear, honest documentation helps underwriters assess your creditworthiness and ensures your loan approval process continues without unnecessary delays or complications.

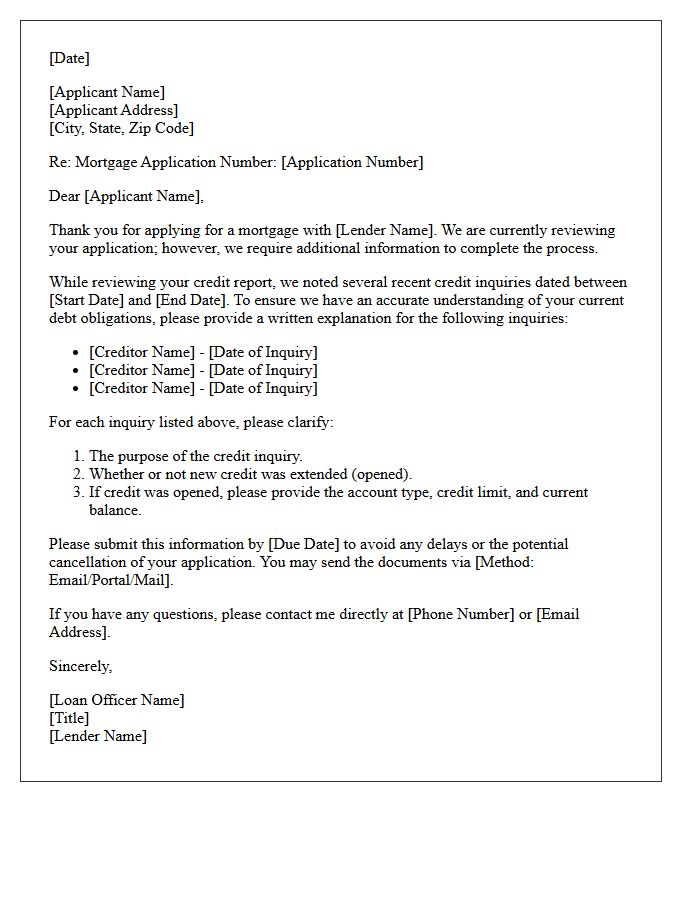

Notice of Action Required: Credit Inquiry Explanation Letter

A Notice of Action Required: Credit Inquiry Explanation Letter is a formal request from a lender asking you to clarify recent credit inquiries. To move forward with your application, you must provide a written statement explaining the purpose of each hard pull on your credit report. This process helps lenders ensure you are not acquiring undisclosed debt that could impact your debt-to-income ratio. Promptly addressing this notice is essential for final loan approval and maintaining transparency throughout the underwriting stage of your financing.

Letter of Incomplete Mortgage Application Due to Credit Inquiries

A Letter of Incomplete Mortgage Application due to credit inquiries is a request from lenders for clarification regarding recent loan activity. When an Inquiry Letter is issued, the borrower must explain if these credit checks resulted in new debt. This step is critical because undisclosed liabilities impact your debt-to-income ratio and overall eligibility. Promptly providing a signed explanation ensures the underwriting process continues without delays. Always verify that no new accounts were opened to maintain your financial stability and secure final loan approval.

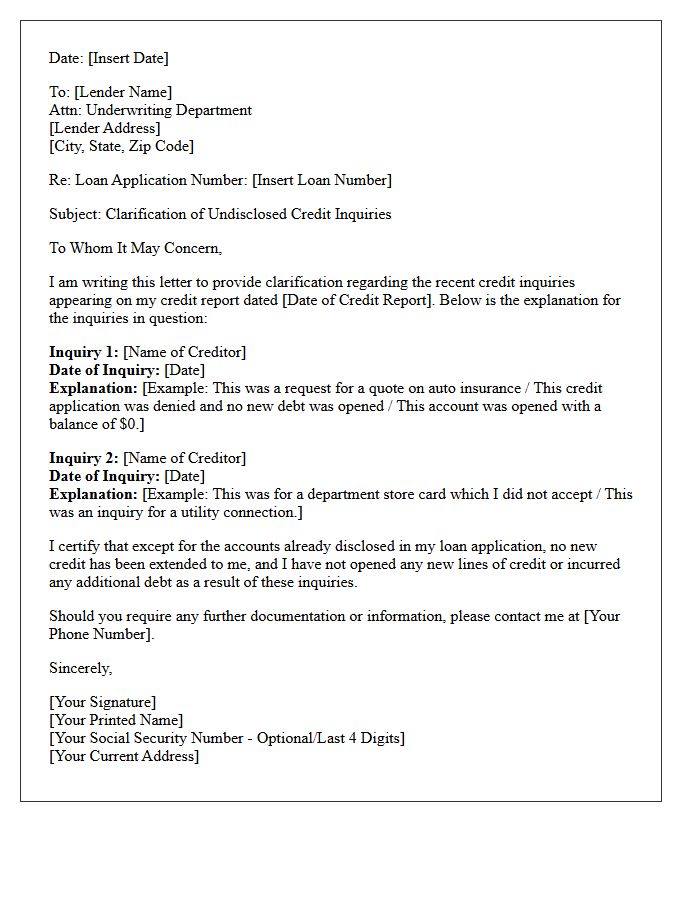

Undisclosed Credit Inquiry Clarification Letter

An Undisclosed Credit Inquiry Clarification Letter is a formal document required by mortgage lenders when new credit checks appear on your report during the loan process. Borrowers must explain the purpose of each inquiry and confirm if any new debt was opened. This step ensures your debt-to-income ratio remains accurate for final approval. To avoid processing delays, provide a clear explanation for each entry and state whether an account was established, as undisclosed liabilities can result in immediate loan denial or funding complications.

Mortgage Application Suspension: Unresolved Credit Inquiries Letter

When you receive a Mortgage Application Suspension notice due to an Unresolved Credit Inquiries Letter, your loan processing stops immediately. Lenders require you to explain every hard credit pull from the last 90 to 120 days to ensure no undisclosed debt exists. You must provide a written statement clarifying if each inquiry resulted in new credit or was declined. To resume approval, documentation for any new accounts is mandatory, as additional monthly payments directly impact your debt-to-income ratio and overall borrowing eligibility.

Letter of Notice Regarding Missing Credit Inquiry Documentation

A Letter of Notice Regarding Missing Credit Inquiry Documentation is a formal request sent to a credit reporting agency to dispute unauthorized hard pulls. Under the Fair Credit Reporting Act, bureaus must provide permissible purpose evidence for every inquiry listed on your profile. If the agency fails to produce the required documentation within thirty days, they are legally obligated to remove the entry. Monitoring these records is vital for protecting your credit score and identifying potential signs of identity theft or administrative errors in your financial history.

Credit Report Inquiry Discrepancy and Incomplete Application Letter

A credit report inquiry discrepancy occurs when a lender identifies a mismatch between your application and credit file data. Receiving an Incomplete Application Letter means the creditor cannot proceed without further verification. You must promptly address these inconsistencies to prevent identity theft or application denial. Common issues include transposed social security numbers, old addresses, or unauthorized inquiries. Always review your credit report for errors and provide the requested documentation to ensure your creditworthiness is accurately represented and your financial security is maintained.

Request for Unresolved Credit Inquiry Details Letter

A Request for Unresolved Credit Inquiry Details Letter is a formal document used to challenge unauthorized credit checks on your credit report. This letter requires credit bureaus to provide documented proof of permissible purpose for any hard inquiry. Under the Fair Credit Reporting Act (FCRA), reporting agencies must investigate and remove inquiries that lack legal authorization. Sending this dispute letter is essential for protecting your credit score from negative impacts caused by identity theft or administrative errors, ensuring your financial profile remains accurate and secure.

Incomplete Loan Application Credit Inquiry Notice Letter

An Incomplete Loan Application Credit Inquiry Notice Letter informs you that your credit report was accessed, but the lender could not finalize a decision. Under the Equal Credit Opportunity Act (ECOA), lenders must notify you if specific information is missing to complete your request. Receiving this letter does not mean you were denied; however, the hard inquiry may still impact your credit score. You typically have a set timeframe to provide the missing documentation or the file will be officially closed without further consideration from the financial institution.

What is a "Notice of Incomplete Application: Unresolved Credit Report Inquiries"?

This notice is a formal communication from a lender stating that your loan or credit application cannot be processed because there are recent credit inquiries on your credit report that have not been clarified or explained.

Why did I receive a notice about unresolved credit inquiries?

Lenders issue this notice when they see multiple applications for credit in a short period. They need to determine if those inquiries resulted in new debt obligations that could impact your debt-to-income ratio and your ability to repay a new loan.

How do I resolve a notice regarding incomplete credit report inquiries?

To resolve this, you must provide a written letter of explanation for each inquiry listed. You need to state whether the inquiry resulted in a new credit account, the amount of the new credit limit, and the current balance of that account.

Will unresolved credit inquiries cause my loan application to be denied?

Not necessarily. An "incomplete application" notice is a request for more information rather than a final denial. However, failing to provide the requested explanations or failing to disclose new debt incurred from those inquiries can lead to a formal loan rejection.

How long do I have to respond to a Notice of Incomplete Application?

The timeframe varies by lender but typically ranges from 10 to 30 days. It is critical to respond promptly, as federal law requires lenders to close applications that remain incomplete after a specific period, requiring you to start the application process over.

Comments