A Short Sale Payoff Demand Letter is a formal request sent to a mortgage lender to confirm the discounted amount required to release a lien. This critical document outlines the final terms, wire instructions, and deadlines necessary to settle the debt for less than the full balance. Understanding its requirements ensures a smooth real estate closing. Below are some ready to use template.

Image cover: Requesting Your Short Sale Payoff: Professional Demand Letter Templates and Samples

Letter Samples List

- Short Sale Payoff Demand Letter

- Date of Letter Issuance

- Mortgage Lender Company Information

- Borrower Name and Loan Account Number

- Subject Property Complete Address

- Total Outstanding Mortgage Principal and Interest

- Approved Short Sale Gross Purchase Price

- Approved Net Payoff Amount to Satisfy Lien

- Good Through Date for Short Sale Payoff

- Authorized Deductions and Closing Costs

- Wire Transfer and Payment Instructions

- Conditions for Release of Mortgage Lien

- Lender Authorization Signature and Title

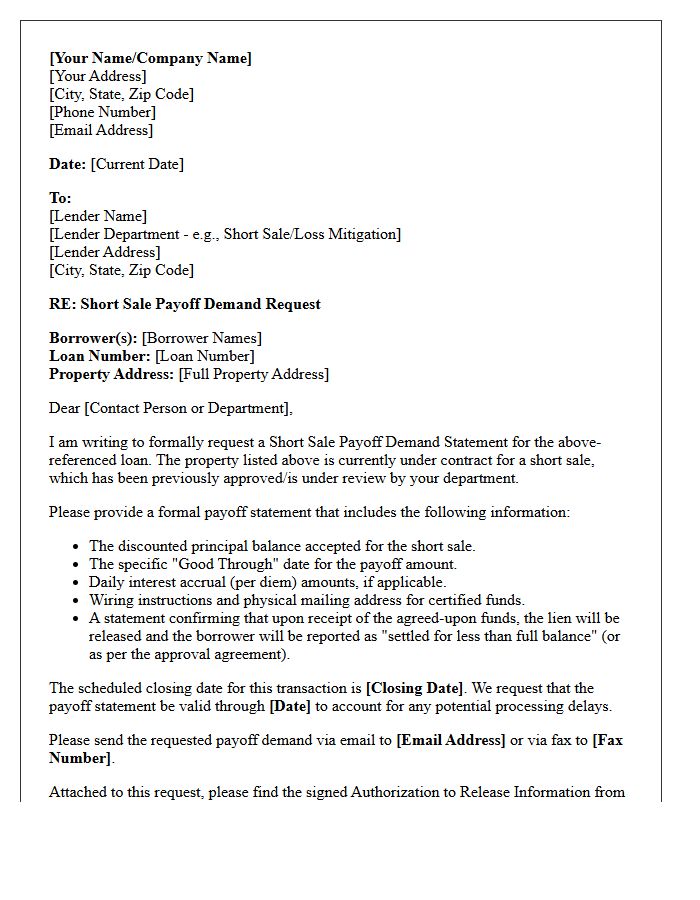

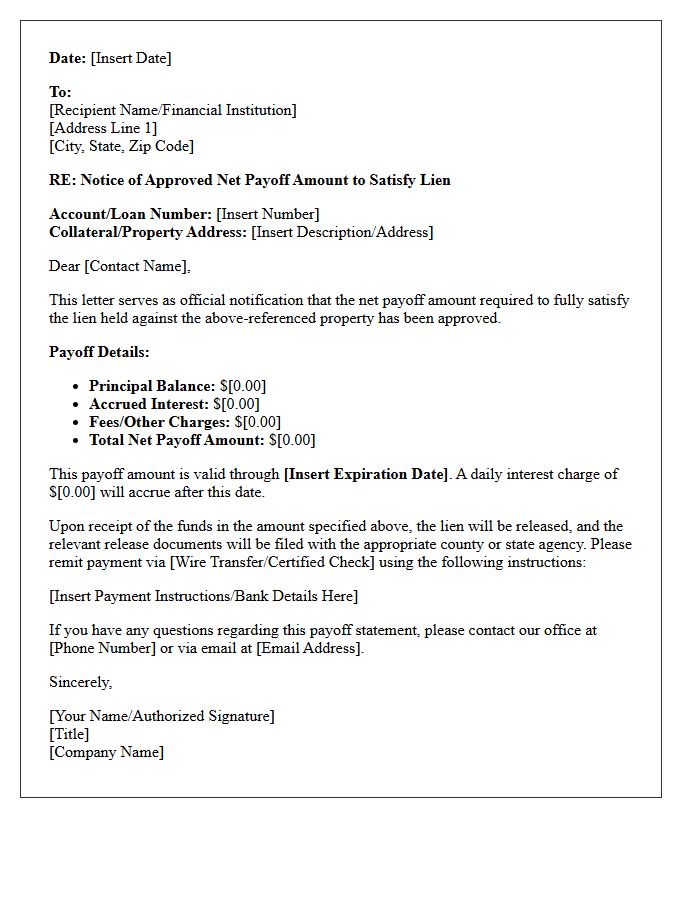

Short Sale Payoff Demand Letter

A Short Sale Payoff Demand Letter is a critical document issued by a lender outlining the specific terms for accepting less than the full mortgage balance. It confirms the approved payoff amount, established deadlines, and required wiring instructions to release the lien. Borrowers must strictly adhere to the expiration date and conditions mentioned to ensure the deficiency waiver is valid. Reviewing this letter ensures the bank agrees to settle the debt, preventing future collections and finalizing the property transfer legally and effectively.

Date of Letter Issuance

The Date of Letter Issuance serves as the official legal reference point for any formal communication. It establishes the exact moment a document becomes active, triggering critical compliance deadlines, notice periods, and statutory timelines for responses. This date is vital for maintaining an accurate chronological record and ensuring procedural validity in administrative or legal matters. Always verify this date to calculate time-sensitive obligations accurately and avoid potential penalties associated with late actions or expired legal rights within a professional framework.

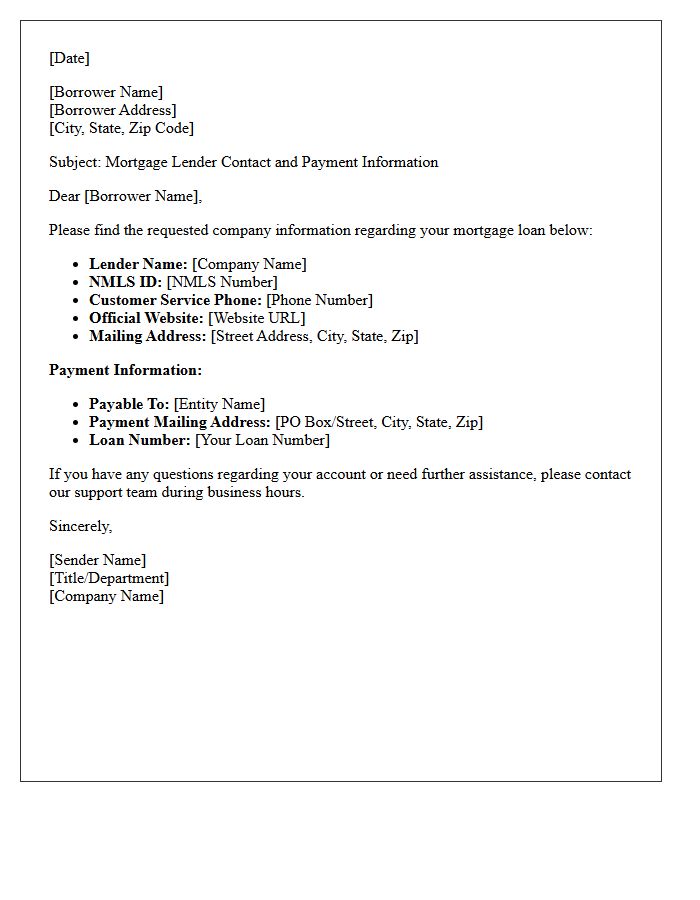

Mortgage Lender Company Information

Before selecting a mortgage lender, it is vital to verify their licensing and reputation through the NMLS database. These companies range from traditional banks to online non-bank lenders, each offering different interest rates and closing costs. Always request a Loan Estimate to compare annual percentage rates (APR) and service fees effectively. Understanding their pre-approval process and servicing policies ensures you find a reliable partner for your long-term financial commitment during the home-buying journey.

Borrower Name and Loan Account Number

When managing your finances, identifying your Borrower Name and Loan Account Number is essential for accurate record-keeping. The borrower name confirms the legal identity responsible for repayment, while the unique account number acts as a specific identifier for tracking your balance and transaction history. Always verify these details on your billing statements to ensure payments are correctly applied. Providing both pieces of information during communication with lenders prevents processing errors and helps maintain the security of your financial profile.

Subject Property Complete Address

A Subject Property Complete Address is the precise geographic identifier used in real estate transactions to uniquely distinguish a specific parcel of land or building. Providing the full street number, name, city, state, and zip code is essential for accurate title searches, property appraisals, and legal documentation. Ensuring the address is verified against official postal records prevents costly errors during the escrow process and guarantees that all legal notifications reach the correct location. Accuracy in this detail is the foundation of any valid property contract.

Total Outstanding Mortgage Principal and Interest

Understanding your Total Outstanding Mortgage Principal and Interest is essential for long-term financial planning. The principal represents the original loan amount remaining, while the interest is the cumulative cost of borrowing over the term. Together, they form the total debt obligation you must repay to own your home outright. Tracking this figure helps homeowners evaluate refinancing opportunities and assess their current home equity. Knowing the full balance ensures you can manage your monthly budget effectively and plan for future debt-free milestones.

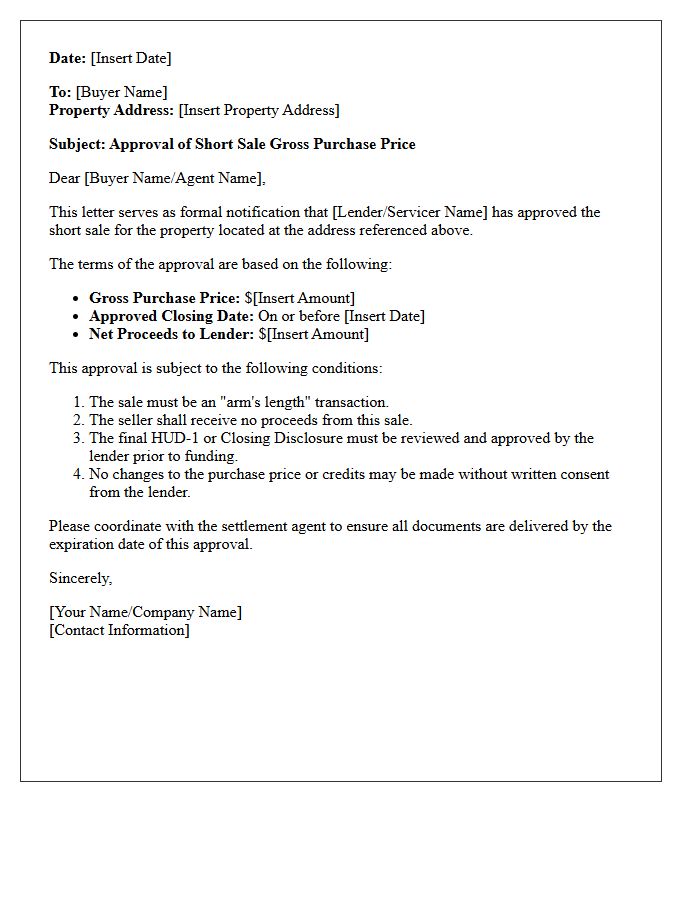

Approved Short Sale Gross Purchase Price

The Approved Short Sale Gross Purchase Price represents the total amount a lender agrees to accept from a buyer to release their lien. It is critically important to understand that this figure is the "top line" price before any deductions for commissions, back taxes, or closing costs. While the lender approves this gross amount, the sale remains contingent upon the bank issuing a formal approval letter. Buyers must ensure this price aligns with current market value, as the lender's valuation dictates the final terms of the debt settlement.

Approved Net Payoff Amount to Satisfy Lien

An Approved Net Payoff Amount is the final, legally binding figure required to fully satisfy a lien. This amount represents the exact total, including principal, interest, and legal fees, that the lienholder agrees to accept to release their claim on the property. Obtaining this verified statement is critical during a real estate closing or vehicle sale to ensure a clear title transfer. Once paid, the creditor must issue a lien release, confirming the debt is extinguished and the asset is free of encumbrances.

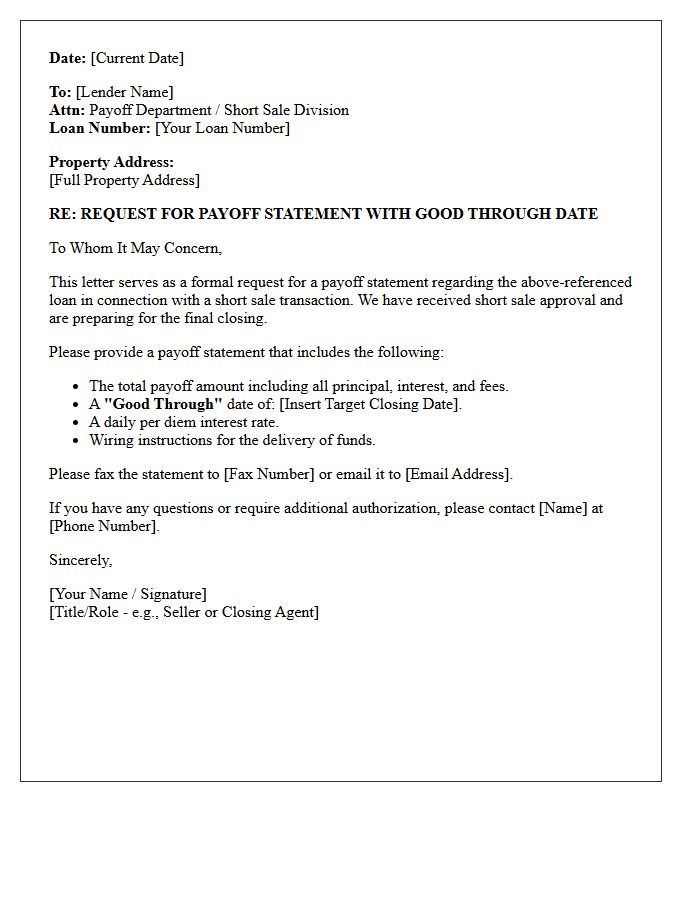

Good Through Date for Short Sale Payoff

The Good Through Date is the critical deadline in a short sale approval letter, representing the final day a lender will accept the negotiated payoff amount. It is essential to close the transaction on or before this specific date to avoid expiration. Missing this window often requires a formal extension or a new appraisal, potentially jeopardizing the entire deal. Ensuring all parties coordinate for a timely signing is the most important step in protecting the agreed-upon settlement terms and preventing foreclosure.

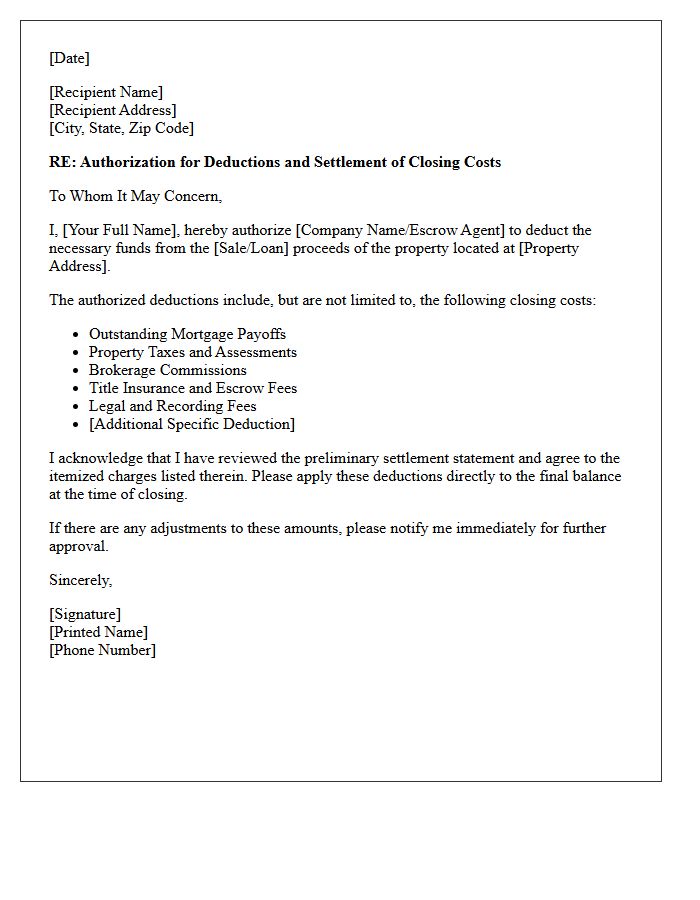

Authorized Deductions and Closing Costs

Understanding authorized deductions and closing costs is essential for transparent real estate transactions. Authorized deductions refer to specific expenses subtracted from the sale proceeds, such as taxes or professional fees. Closing costs encompass legal fees, title insurance, and appraisal charges paid at settlement. Both buyers and sellers must review the Closing Disclosure to verify all financial obligations. Accurately tracking these costs prevents unexpected out-of-pocket expenses and ensures legal compliance. Being informed about these mandatory payments facilitates a smoother transfer of property ownership and clarifies final net proceeds.

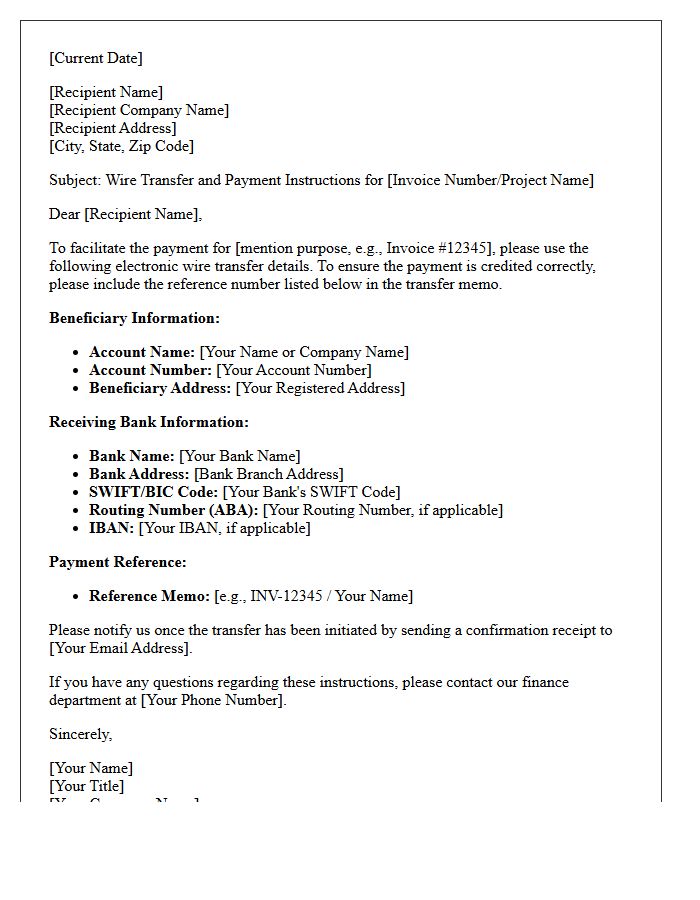

Wire Transfer and Payment Instructions

A wire transfer is an expedited method for electronic fund transfers between financial institutions. Precision is critical because these transactions are often irreversible once processed. You must verify all payment instructions directly with the recipient to prevent wire fraud and interception. Ensure the routing number, account details, and recipient name are exact. Always use a secondary communication method, like a phone call, to confirm bank details before initiating the transfer. Understanding these requirements ensures your funds reach the intended destination securely and without unnecessary delays.

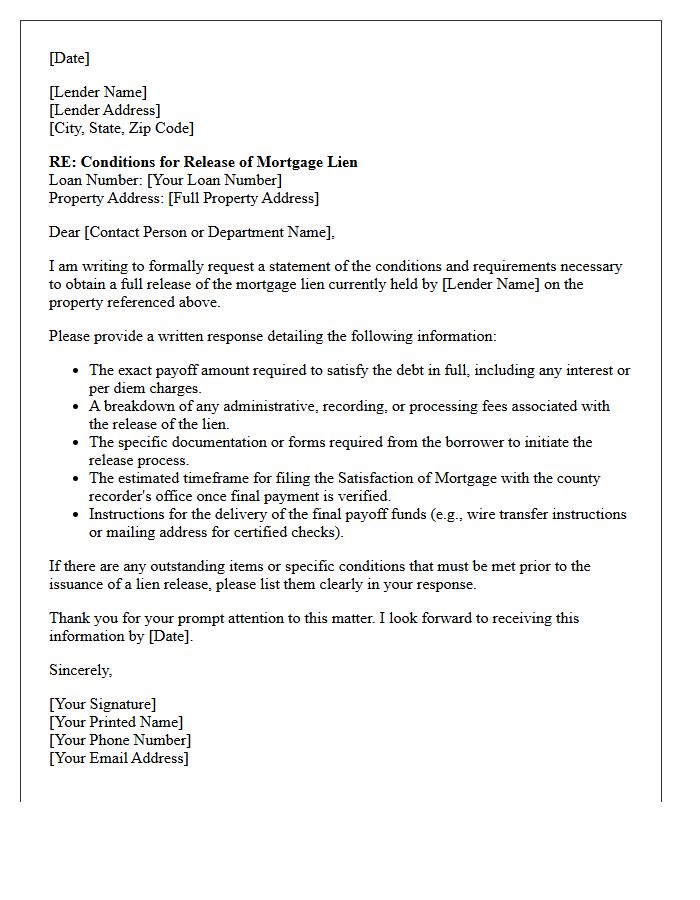

Conditions for Release of Mortgage Lien

To secure a Release of Mortgage Lien, the borrower must first complete full repayment of the loan principal and interest. Once the debt is satisfied, the lender issues a satisfaction of mortgage document. This legal instrument must be officially recorded in the local county land records to formally clear the title. Failure to record this release can result in an encumbrance, preventing the future sale or refinancing of the property. Always verify that the lien is discharged to ensure unclouded ownership rights.

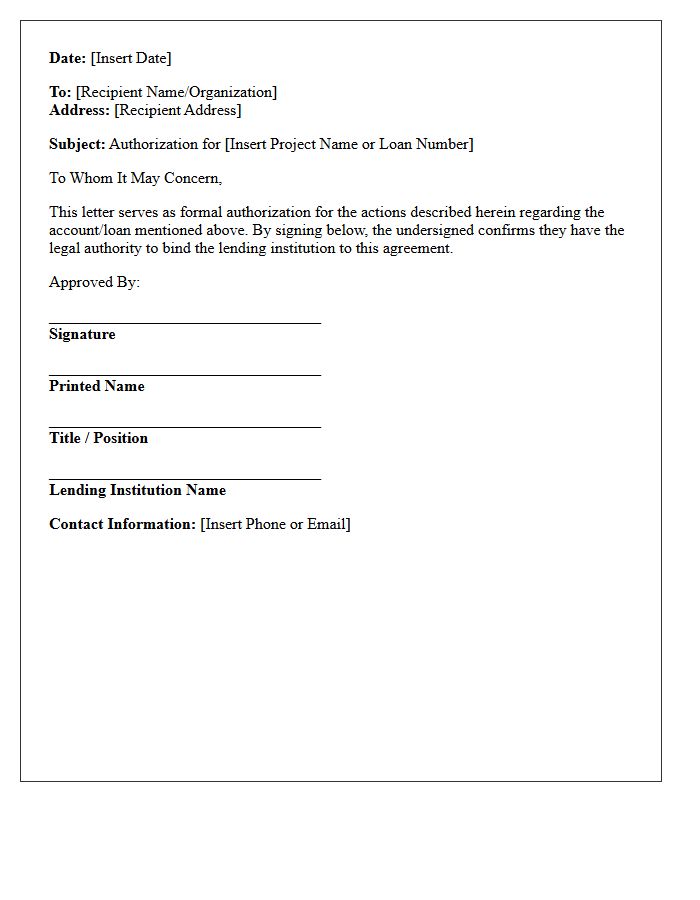

Lender Authorization Signature and Title

A Lender Authorization Signature and Title validates that a financial institution officially approves a loan document. This requirement ensures the individual signing possesses the legal authority to bind the organization to the agreement. Without a formal signature and a recognized corporate title, such as "Vice President" or "Authorized Signatory," the contract may be deemed invalid. Verifying these credentials protects all parties by confirming the transaction is legally enforceable and compliant with internal banking policies and regulatory standards.

What is a Short Sale Payoff Demand Letter?

A Short Sale Payoff Demand Letter is an official document issued by a mortgage lender specifying the discounted amount they are willing to accept to release their lien on a property. It outlines the specific terms, net proceeds required, and the expiration date for the short sale approval.

What key information is included in a payoff demand letter?

The letter typically includes the total payoff amount, the deadline for closing, wiring instructions for funds, and specific conditions such as "no cash back to the seller" and the release of deficiency judgment clauses.

How long is a short sale payoff demand letter valid?

Most payoff demand letters are valid for 30 days from the date of issuance. If the real estate closing is delayed beyond the "good through" date, the title company must request an updated letter or an extension from the lender.

Does a payoff demand letter satisfy the entire mortgage debt?

It depends on the language in the letter. A "full satisfaction" letter waives the lender's right to pursue a deficiency judgment, whereas other letters may allow the lender to seek the remaining balance from the borrower after the short sale closes.

Why would a lender reject a short sale payoff request?

A lender may reject the request if the net proceeds are lower than the property's appraised value, if the seller has significant liquid assets, or if the documentation provided in the short sale package is incomplete or expired.

Comments