A Rate Lock Float-Down Denial Notice is a formal document issued by lenders when a borrower's request to lower their interest rate is rejected. This occurs if market conditions or specific loan criteria do not meet the float-down agreement's requirements. Understanding the reasons for denial is essential for managing your mortgage expectations. To assist you, below are some ready to use templates.

Image cover: Rate Lock Float-Down Denial: Notification Templates and Response Samples

Letter Samples List

- Standard Rate Lock Float-Down Denial Letter

- Minimum Rate Drop Threshold Unmet Float-Down Denial Letter

- Missed Application Deadline Float-Down Denial Letter

- Expired Rate Lock Period Float-Down Denial Letter

- Credit Score Reduction Float-Down Denial Letter

- Ineligible Loan Program Float-Down Denial Letter

- Change In Loan Amount Float-Down Denial Letter

- Property Appraisal Shortfall Float-Down Denial Letter

- Secondary Market Pricing Float-Down Denial Letter

- Missing Borrower Documentation Float-Down Denial Letter

- Unapproved Property Type Float-Down Denial Letter

- Construction Delay Rate Float-Down Denial Letter

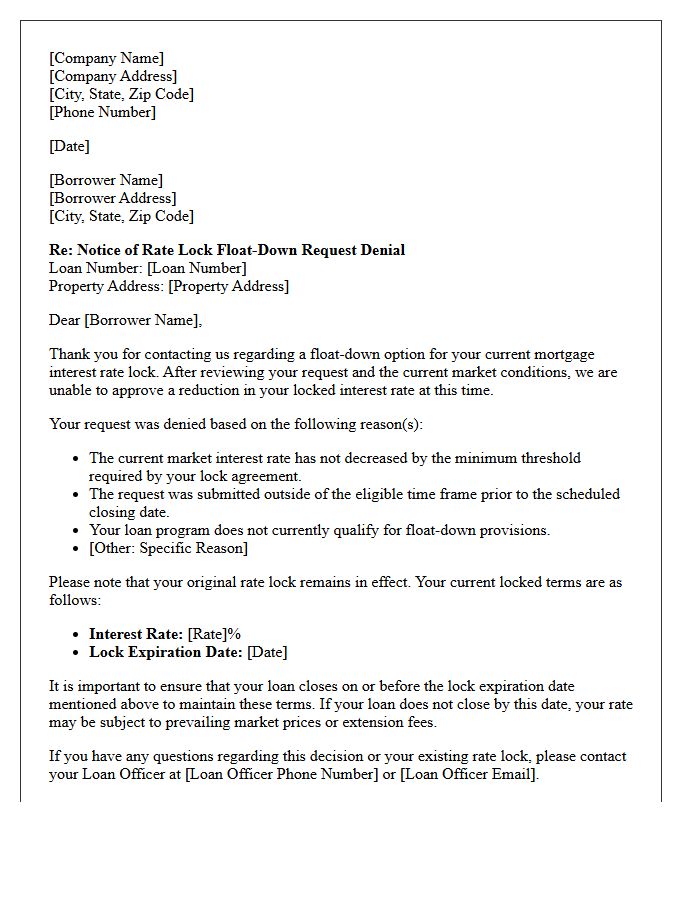

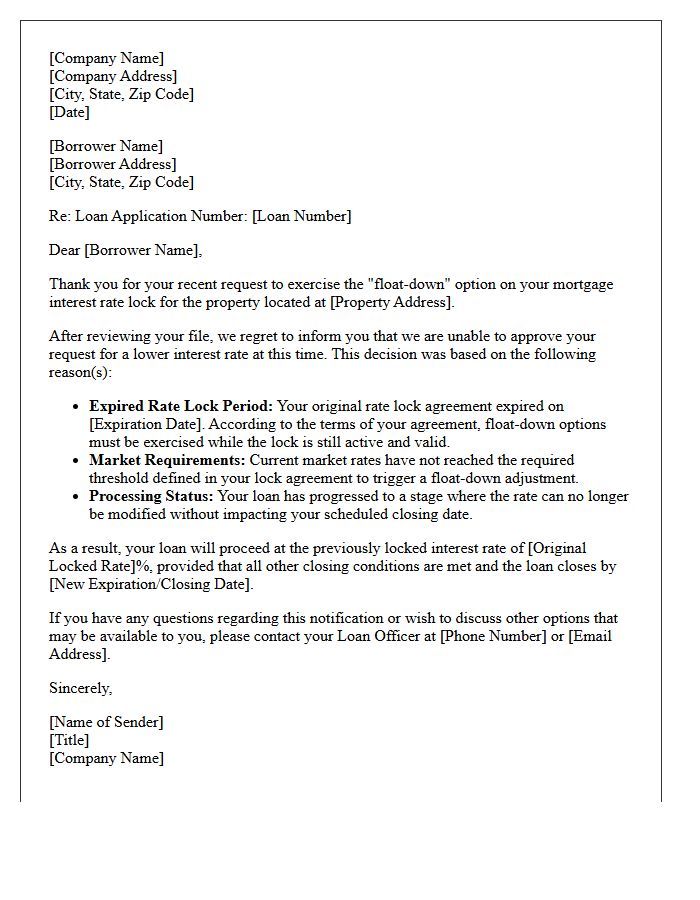

Standard Rate Lock Float-Down Denial Letter

A Standard Rate Lock Float-Down Denial Letter formally notifies a borrower that their request for a lower interest rate has been rejected. This typically occurs because the market interest rate did not drop significantly enough to meet the float-down provision requirements specified in the original agreement. Lenders issue this document to maintain the initial locked rate, ensuring the loan terms remain fixed despite minor market fluctuations. Understanding the specific eligibility criteria and expiration dates within your lock agreement is essential to navigating these financing adjustments effectively.

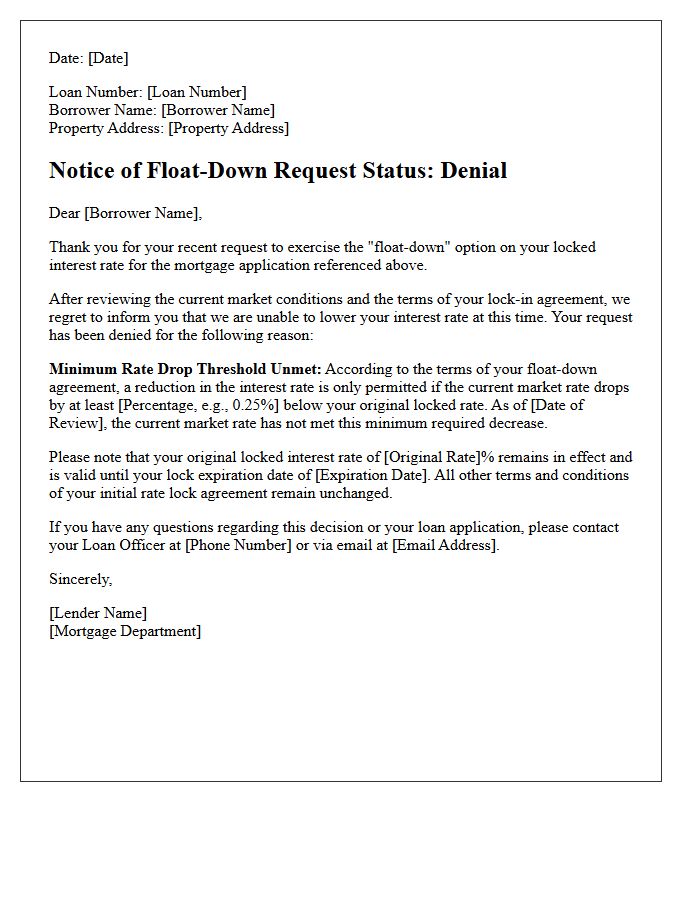

Minimum Rate Drop Threshold Unmet Float-Down Denial Letter

A Minimum Rate Drop Threshold Unmet denial letter is issued when a borrower requests a float-down option, but current market interest rates have not decreased significantly enough to trigger the adjustment. Lenders typically require the rate to drop by a specific margin, such as 0.125% or 0.25%, before approving a lower rate. If this threshold is not reached, the original locked-in rate remains in effect. This document serves as formal notification that the contractual requirements for a rate reduction were not satisfied during the lock-in period.

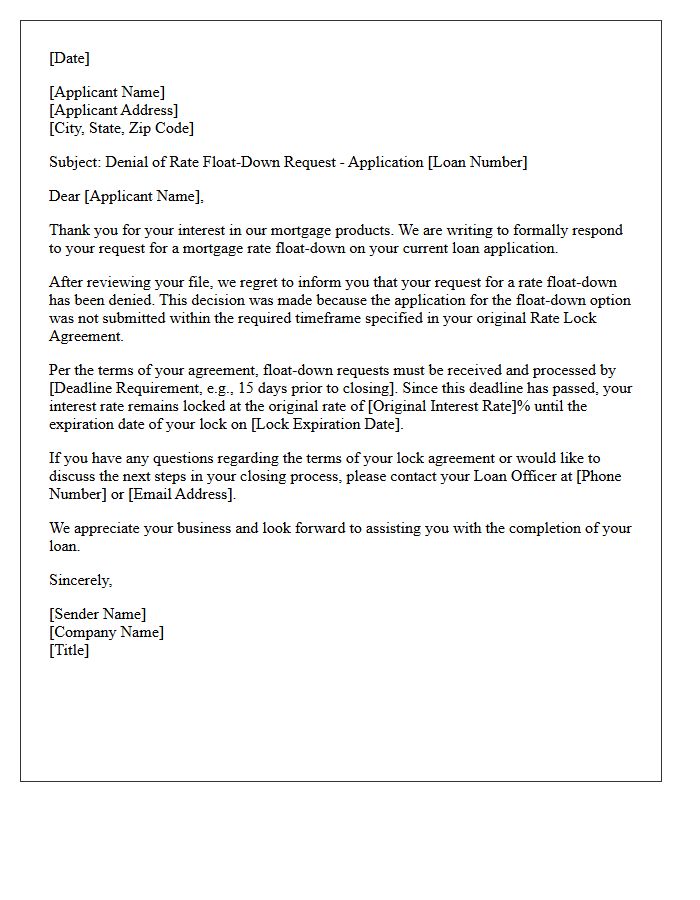

Missed Application Deadline Float-Down Denial Letter

A Missed Application Deadline Float-Down Denial Letter is a formal notice from a mortgage lender stating that a borrower's request for a lower interest rate was rejected. To qualify for a float-down option, borrowers must typically submit their request within a strict timeframe after market rates decrease. If you fail to meet this contractual deadline, the lender maintains your original locked-in rate. This letter serves as official documentation that your application did not comply with the specific timing requirements outlined in your initial rate lock agreement.

Expired Rate Lock Period Float-Down Denial Letter

An Expired Rate Lock Period Float-Down Denial Letter informs borrowers that their request for a lower interest rate was rejected. This typically occurs because the original lock-in agreement has lapsed or the market hasn't improved sufficiently to trigger the float-down provision. To avoid higher financing costs, borrowers must monitor expiration dates closely and maintain continuous communication with their lender. If denied, you may need to re-lock at current market rates, which could involve additional fees or a higher monthly mortgage payment.

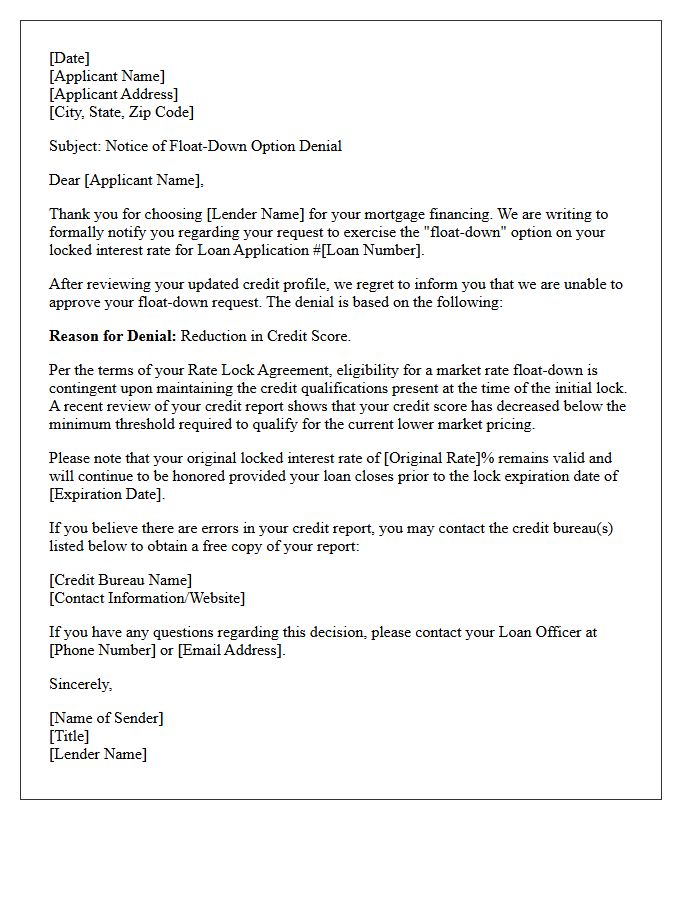

Credit Score Reduction Float-Down Denial Letter

A Credit Score Reduction Float-Down Denial Letter informs mortgage applicants that their request for a lower interest rate was rejected. Lenders offer float-down options if market rates drop, but eligibility often depends on maintaining your original credit profile. If your credit score decreases during the underwriting process, you may no longer meet the investor requirements for the improved rate. Receiving this letter means your current loan terms remain unchanged based on your initial lock-in agreement, as a lower score represents increased lending risk that disqualifies you from the reduction.

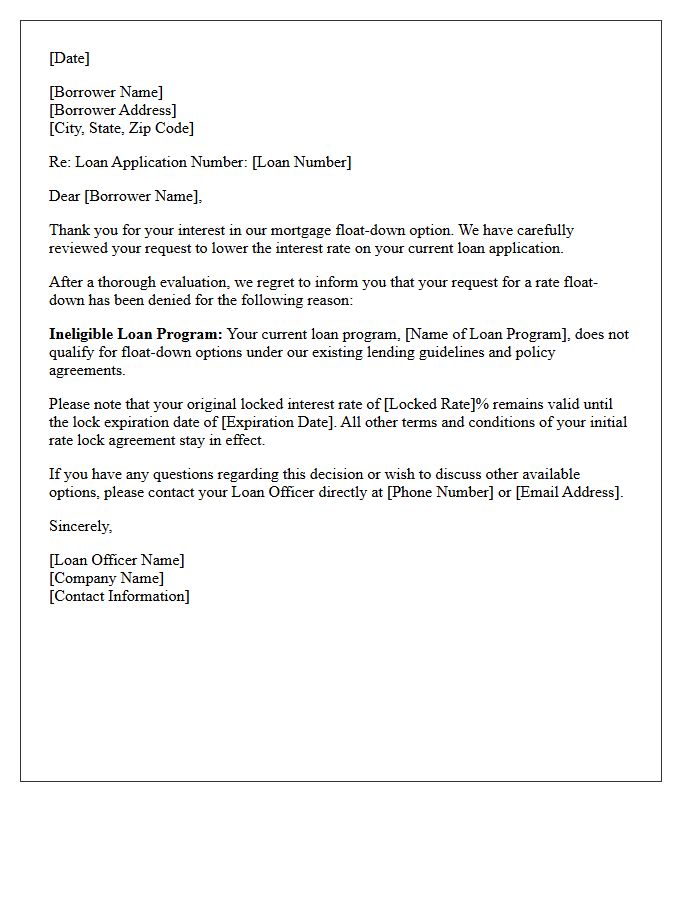

Ineligible Loan Program Float-Down Denial Letter

An Ineligible Loan Program Float-Down Denial Letter is a formal notice issued when a borrower fails to meet specific criteria for a lower interest rate market adjustment. This typically occurs because the current loan product does not support float-down options or the required rate drop threshold was not met. Receiving this letter means your original locked-in rate remains in effect despite market fluctuations. It is crucial to review the eligibility requirements outlined in your agreement to understand why the request was declined and how it affects your final mortgage terms.

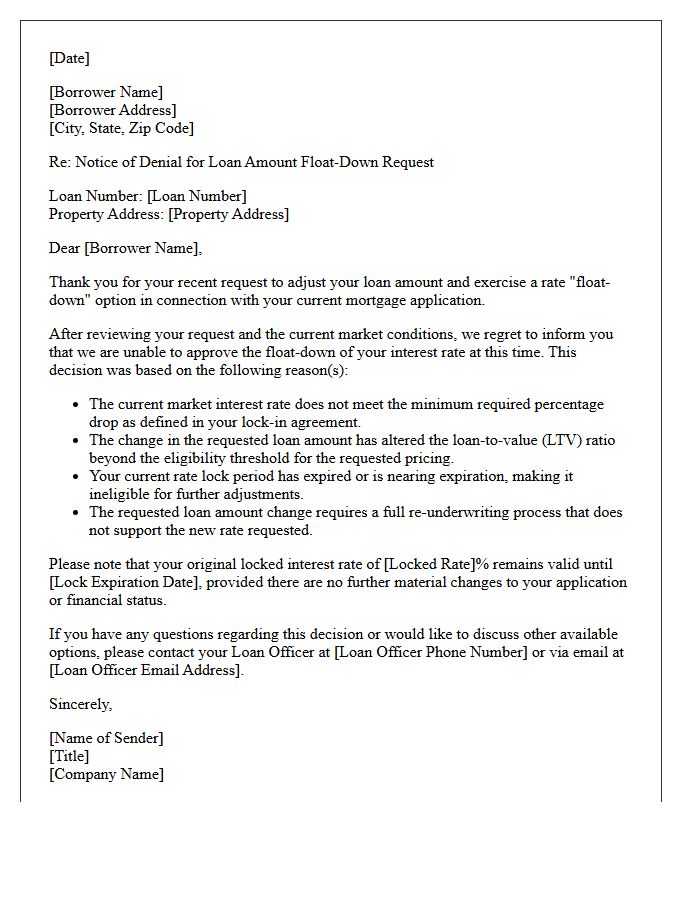

Change In Loan Amount Float-Down Denial Letter

A Change In Loan Amount Float-Down Denial Letter informs borrowers that their request to lower their interest rate following a decrease in the total loan balance has been rejected. Lenders typically deny these requests if the new loan amount no longer meets specific eligibility thresholds or secondary market guidelines. Receiving this formal notice means your original locked rate remains in effect despite the reduction in principal. It is crucial to review the stated reasons for denial to understand how loan-to-value ratios or internal pricing policies impacted the decision.

Property Appraisal Shortfall Float-Down Denial Letter

A Property Appraisal Shortfall Float-Down Denial Letter is a formal notice from a lender rejecting a borrower's request for a lower interest rate. This typically occurs when a valuation gap exists between the purchase price and the appraised value. Because the home serves as collateral, a lower appraisal increases the loan-to-value ratio, potentially violating the financial requirements needed to exercise a float-down option. Consequently, the lender maintains the original locked-in rate to mitigate risk associated with the decreased equity buffer.

Secondary Market Pricing Float-Down Denial Letter

A Secondary Market Pricing Float-Down Denial Letter informs a borrower that their request for a lower interest rate has been rejected. Lenders issue this when market conditions do not meet the specific float-down option criteria defined in the initial lock agreement. Key factors for denial typically include the current market rate not dropping sufficiently below the locked rate or the request falling outside the eligible timeframe. Understanding this document is crucial as it confirms that your original interest rate lock remains in effect until the specified expiration date.

Missing Borrower Documentation Float-Down Denial Letter

A Missing Borrower Documentation Float-Down Denial Letter is a formal notice issued when a mortgage lender rejects a request for a lower interest rate. This denial typically occurs because the applicant failed to submit required financial records within the specified lock-in period. To secure a float-down option, borrowers must provide updated income or asset verification promptly. Failing to meet these strict documentation deadlines results in the loan remaining at the original higher rate or leads to a total expiration of the rate lock agreement.

Unapproved Property Type Float-Down Denial Letter

An Unapproved Property Type Float-Down Denial Letter is a formal notification from a lender rejecting a request for a lower interest rate because the real estate does not meet specific eligibility criteria. When a borrower attempts to exercise a float-down option, the property must adhere to strict guidelines regarding its classification, such as condos or mixed-use spaces. If the asset type is deemed ineligible or falls outside secondary market standards, the rate reduction is denied. This ensures the loan-to-value ratios and risk assessments remain consistent with the original underwriting approval for that specific property category.

Construction Delay Rate Float-Down Denial Letter

A Construction Delay Rate Float-Down Denial Letter is a formal notification from a lender rejecting a borrower's request to lower their interest rate. This typically occurs when a project extension surpasses the rate lock period or fail to meet specific market conditions. The most critical factor is that lenders often deny these requests if current market rates have not decreased significantly below the original locked rate. Borrowers must carefully review their lock-in agreement to understand the specific expiration dates and any non-refundable fees associated with construction-to-permanent financing delays.

What is a Rate Lock Float-Down Denial Notice?

A Rate Lock Float-Down Denial Notice is a formal notification from a mortgage lender informing an applicant that their request to lower their locked interest rate to current market levels has been rejected based on specific policy criteria.

Why was my mortgage rate float-down request denied?

Common reasons for denial include the market rate not dropping below the required threshold (typically 0.25% or more), the request being made outside the eligible window, or the loan file already reaching the final approval stage where changes are no longer permitted.

Can I appeal a float-down option denial?

While formal appeals are rare, you can request a secondary review if you believe the lender used an incorrect market index or if your contract terms regarding the float-down provision were misinterpreted during the evaluation process.

Does a float-down denial affect my original rate lock?

No, a denial of a float-down request does not cancel your existing rate lock. Your original locked interest rate remains valid and protected until the expiration date specified in your initial rate lock agreement.

What are the alternatives if my rate lock float-down is rejected?

If denied, your options include proceeding with the original locked rate, paying additional points to buy down the rate, or "breaking" the lock by switching lenders, though the latter may result in lost fees and a restarted application process.

Comments