After receiving a loan satisfaction letter, you have officially paid off your mortgage debt. This milestone signifies that you are no longer required to pay Private Mortgage Insurance (PMI). To ensure your lender stops automatic billing and updates your account records correctly, you must formalize the request. To help you finalize this process, below are some ready to use template.

Image cover: Official Guide: Requesting PMI Removal After Mortgage Payoff (Letters & Templates)

Letter Samples List

- Notice of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

- Automatic Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

- Final Loan Satisfaction and Private Mortgage Insurance Termination Letter

- Private Mortgage Insurance Cancellation Following Full Loan Satisfaction Letter

- Lender Confirmation of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

- Mortgage Payoff and Private Mortgage Insurance Cancellation Letter

- Acknowledgment of Loan Satisfaction and Private Mortgage Insurance Cancellation Letter

- Borrower Notification of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

- Official Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

- Certificate of Loan Satisfaction and Private Mortgage Insurance Cancellation Letter

- Post-Satisfaction Private Mortgage Insurance Cancellation Approval Letter

- Account Closure and Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

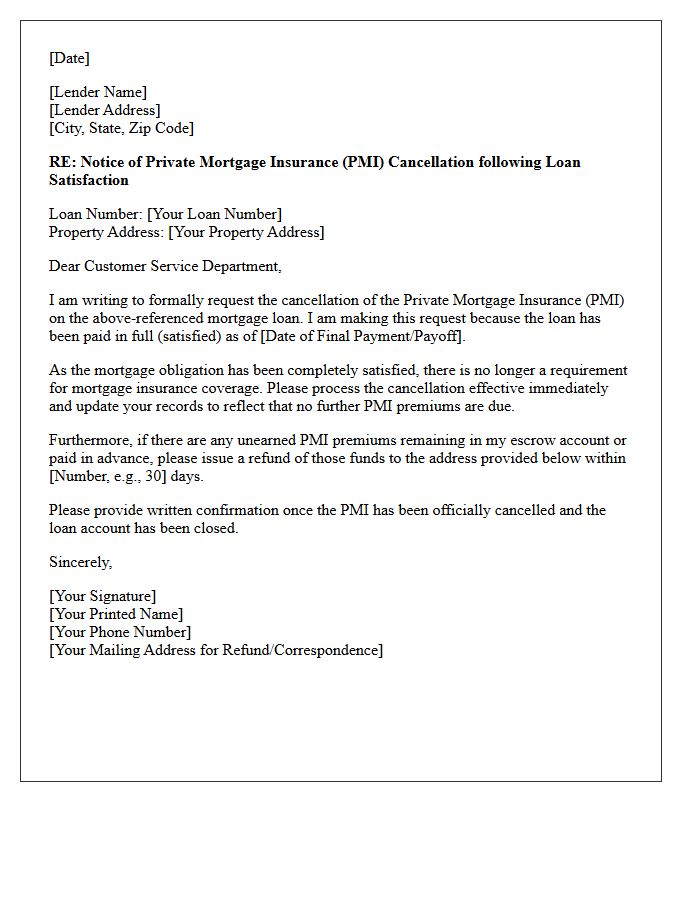

Notice of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

The Notice of Private Mortgage Insurance (PMI) Cancellation is a formal document confirming that your loan satisfaction has triggered the termination of insurance premiums. Once your mortgage is paid in full, lenders are legally required to stop charging for PMI. This letter serves as official proof that your financial obligation toward mortgage insurance has ended. Always verify your final closing statement to ensure no overpayments occurred, as any premiums collected after the payoff date must be refunded to the borrower promptly according to federal law.

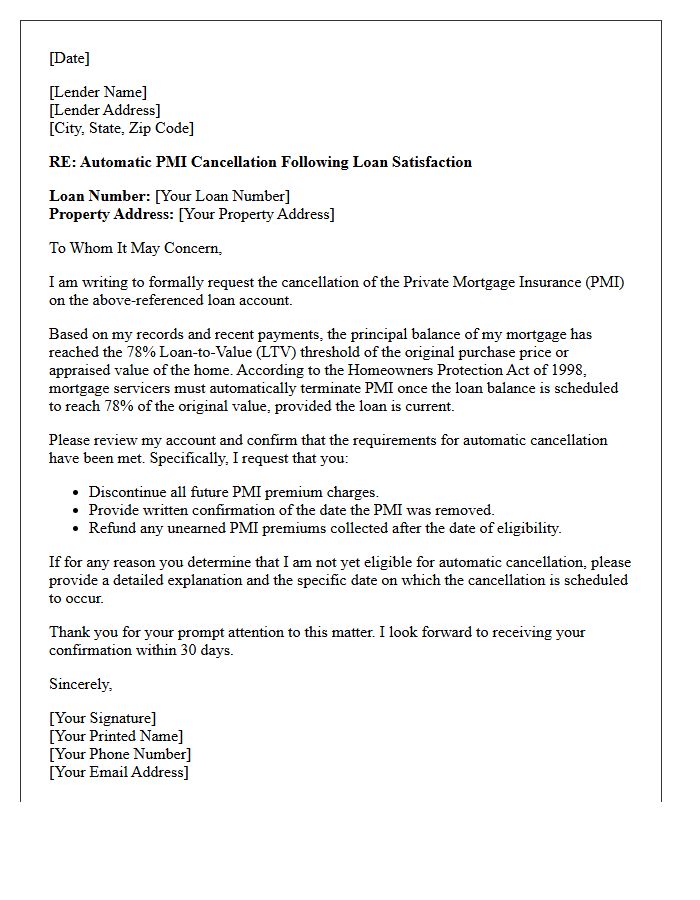

Automatic Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

Once you receive a loan satisfaction letter, it signifies your mortgage is fully paid. At this stage, automatic private mortgage insurance (PMI) cancellation occurs because the debt no longer exists. While lenders must terminate PMI once you reach 78% equity, a satisfied loan eliminates the risk entirely. Ensure your lender updates the county records and stops all escrow disbursements. Retain your satisfaction letter as legal proof that both the lien and insurance obligations are permanently dissolved, protecting your financial interest and confirming clear title ownership.

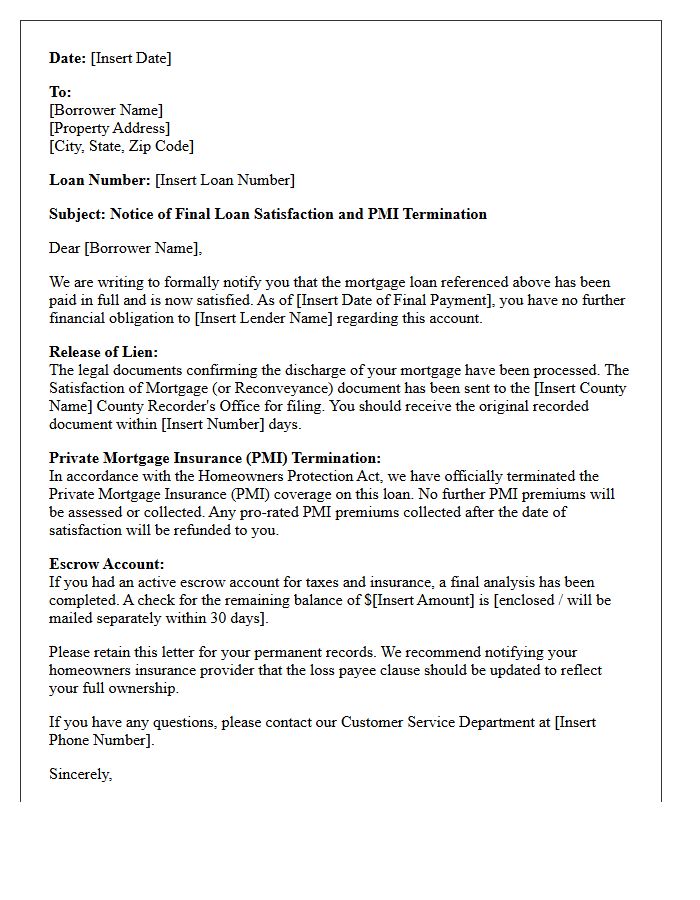

Final Loan Satisfaction and Private Mortgage Insurance Termination Letter

Receiving a Final Loan Satisfaction letter signifies your mortgage is fully repaid, confirming the legal release of the property lien. Equally vital is the Private Mortgage Insurance (PMI) Termination letter, which verifies that your equity has reached the threshold required to cancel costly premiums. Homeowners must ensure these documents are filed with the local county recorder to update the public title. Retaining these records is essential for future property sales, proving you hold clear ownership and have successfully fulfilled all financial obligations to the lender.

Private Mortgage Insurance Cancellation Following Full Loan Satisfaction Letter

Receiving a Full Loan Satisfaction Letter confirms your mortgage is paid in full, which automatically triggers Private Mortgage Insurance cancellation. Since PMI is only required to protect the lender against default risk on active balances, it must cease immediately upon debt discharge. Ensure your servicer stops all premium collections and verifies that no escrow funds are misapplied. Obtaining this formal release is the final step to legal title clearance and ensuring you no longer pay for unnecessary insurance coverage on your home.

Lender Confirmation of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

Receiving a Lender Confirmation of Private Mortgage Insurance Cancellation is vital after loan satisfaction. This document serves as formal proof that your mortgage obligation is complete and PMI charges have officially ceased. Homeowners should verify this letter to ensure no further premiums are escrowed and to update their financial records. It confirms the termination of the lender's interest in the property insurance policy. Retaining this confirmation is essential for future title transfers and verifying your full equity ownership after the final mortgage payment is processed.

Mortgage Payoff and Private Mortgage Insurance Cancellation Letter

A mortgage payoff request ensures you receive an official payoff statement reflecting the total balance, including per diem interest. Simultaneously, a PMI cancellation letter is essential for homeowners with 20% equity to stop unnecessary private mortgage insurance charges. Proactively submitting these written requests prevents overpayment and confirms the legal release of your property title. Always include your loan number and request written confirmation from your servicer to ensure the mortgage is properly satisfied and your monthly financial obligations are accurately updated.

Acknowledgment of Loan Satisfaction and Private Mortgage Insurance Cancellation Letter

An Acknowledgment of Loan Satisfaction is a formal document proving your debt is fully paid, ensuring the release of lien on your property title. Once the loan balance reaches 80% of the original value, you should also issue a Private Mortgage Insurance (PMI) Cancellation Letter to the lender. Promptly requesting these documents helps eliminate monthly insurance premiums and confirms your clear ownership. Retaining both records is essential for future property sales and protecting your financial legal standing after successfully completing your mortgage obligations.

Borrower Notification of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

When a homeowner pays off their mortgage entirely, lenders must issue a Borrower Notification of Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter. This document confirms that the loan is fully satisfied and all future PMI premiums are officially terminated. It serves as essential proof that the lien is released and no further insurance obligations exist. Borrowers should verify this letter against their final closing statement to ensure accurate escrow balancing and to confirm that no residual insurance charges remain on their account after debt resolution.

Official Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

Receiving an Official Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter is the final confirmation that your financial obligation is complete. Once your mortgage is paid in full, your lender must provide this formal documentation to verify that PMI premiums have officially ceased. This letter serves as essential proof for your records, ensuring no further escrow disbursements occur. Retain this document carefully, as it solidifies your full homeownership status and confirms that the private insurance policy, which previously protected the lender against default, has been legally terminated.

Certificate of Loan Satisfaction and Private Mortgage Insurance Cancellation Letter

A Certificate of Loan Satisfaction is a legal document proving your mortgage is paid in full, ensuring a clear property title. Simultaneously, a Private Mortgage Insurance Cancellation Letter confirms you are no longer required to pay PMI premiums once reaching specific equity thresholds. It is essential to verify both documents are filed correctly with local authorities to protect your ownership rights and optimize monthly cash flow. Always retain copies as permanent proof that your financial obligations to the lender have officially ended.

Post-Satisfaction Private Mortgage Insurance Cancellation Approval Letter

The Post-Satisfaction Private Mortgage Insurance Cancellation Approval Letter is a formal document confirming that your PMI has been terminated following the full repayment or satisfaction of your mortgage loan. This letter serves as legal proof that monthly insurance premiums are no longer required. It is essential to verify that your lender has processed this cancellation to ensure no further charges occur. Always keep this approval for your financial records to confirm the removal of insurance obligations and the successful transition to full home equity ownership.

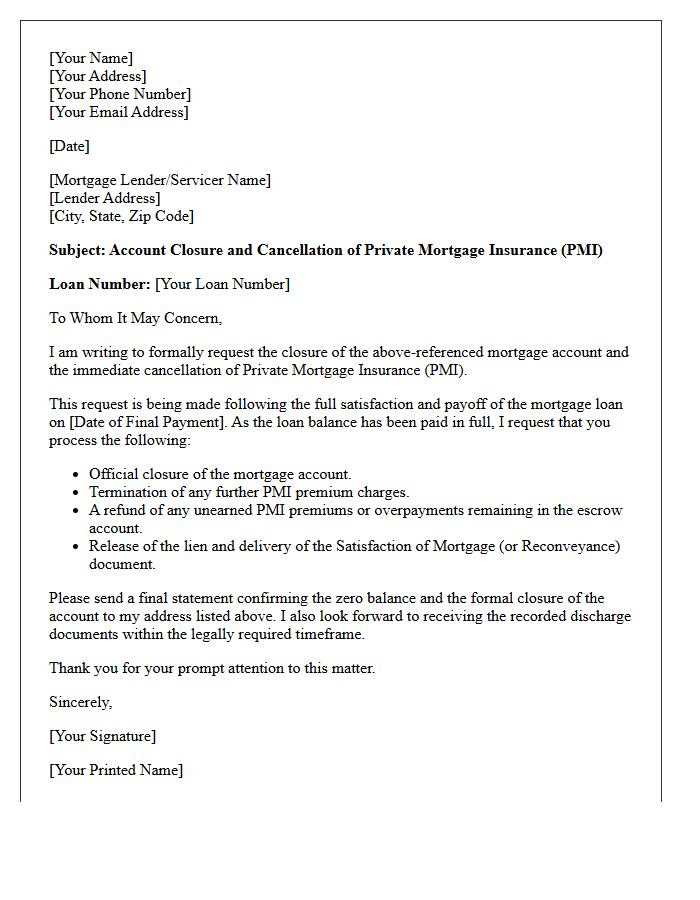

Account Closure and Private Mortgage Insurance Cancellation Following Loan Satisfaction Letter

After receiving your loan satisfaction letter, confirming Account Closure is essential to ensure no further obligations remain. This document serves as legal proof that your debt is fully repaid. You must also verify the automatic Private Mortgage Insurance (PMI) cancellation, as premiums should cease immediately upon payoff. Contact your servicer to confirm the mortgage lien release with the local county office. Finally, ensure any remaining funds in your escrow account are refunded to you within twenty business days to complete the final closing process securely.

1. When can I request Private Mortgage Insurance (PMI) cancellation after receiving a loan satisfaction letter?

Technically, a loan satisfaction letter indicates the mortgage is fully paid off; therefore, PMI is automatically terminated as the debt no longer exists. If you are referring to reaching the 80% Loan-to-Value (LTV) threshold to trigger a satisfaction of the PMI requirement, you can request cancellation once your principal balance reaches 80% of the original value of the home.

2. Does a loan satisfaction letter serve as proof that PMI payments should stop?

Yes. A loan satisfaction letter confirms the mortgage has been paid in full. Once the loan is satisfied, the lender has no legal right to continue charging Private Mortgage Insurance premiums, as there is no longer a lien to insure.

3. Will I receive a refund for unearned PMI premiums after my loan is satisfied?

If you paid your final mortgage balance in full and had pre-paid PMI premiums in an escrow account, the lender is generally required to refund any unearned portions of those premiums within 30 to 45 days following the issuance of the loan satisfaction letter.

4. What is the difference between PMI cancellation and a mortgage satisfaction piece?

PMI cancellation is the removal of the insurance premium once you reach 20% equity while the loan is still active. A mortgage satisfaction piece (or letter) is a legal document filed in public records proving the entire mortgage debt has been paid off, which inherently ends all PMI obligations.

5. Do I need to contact my PMI provider after receiving a loan satisfaction letter?

No, you do not usually need to contact the PMI provider directly. Your mortgage servicer is responsible for notifying the insurer to terminate the policy and ensuring that no further PMI premiums are collected once the loan satisfaction process is complete.

Comments