Receiving a Hello Letter marks the formal transition of your mortgage to an incoming servicer. This essential notice outlines where to send future payments and how to manage your escrow account during the transfer. Understanding this document ensures a seamless transition without affecting your credit score. To simplify your response, below are some ready to use templates.

Image cover: Welcome to Your New Mortgage Servicer: Introduction Letter Templates and Best Practices

Letter Samples List

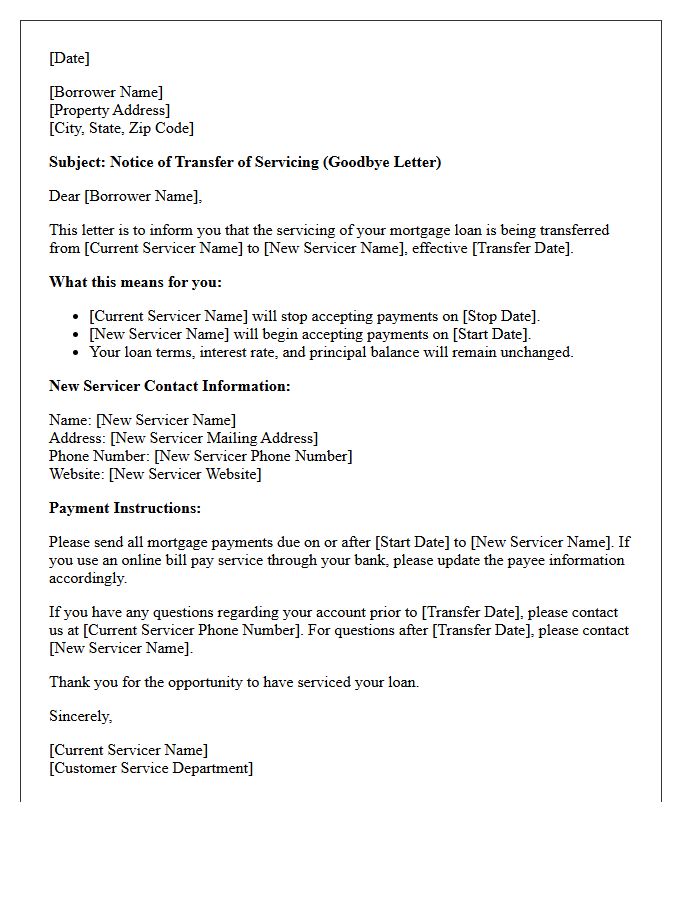

- Goodbye Letter from Outgoing Servicer

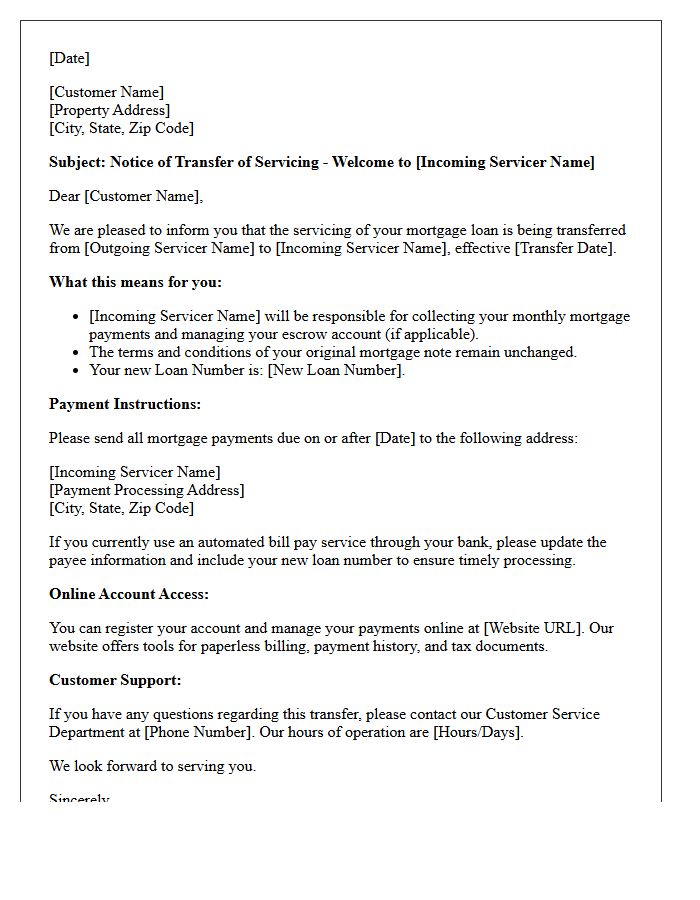

- Welcome Letter from Incoming Servicer

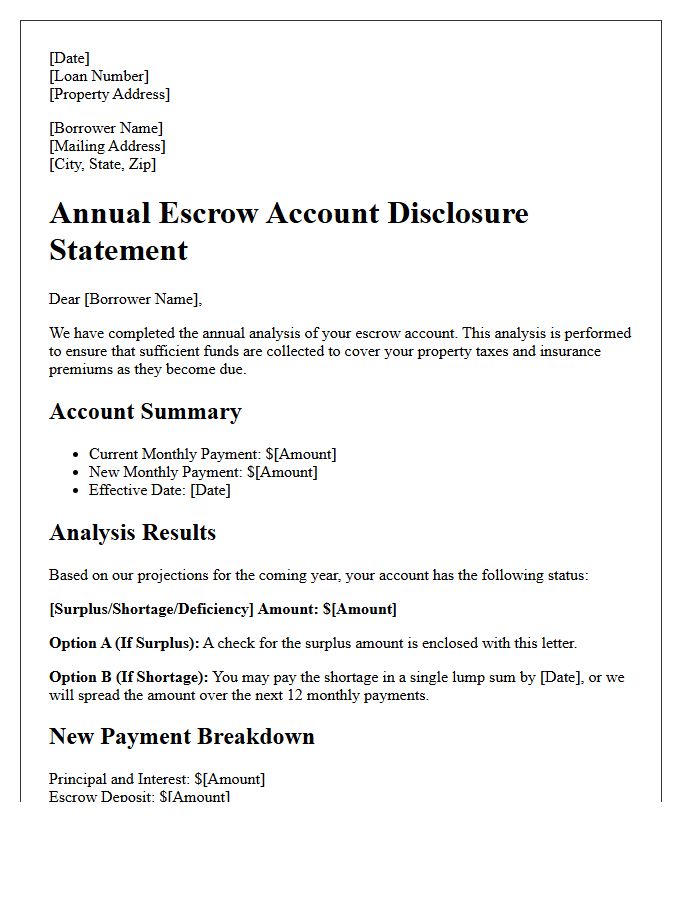

- Annual Escrow Account Analysis Letter

- Notice of Default Warning Letter

- Adjustable Rate Mortgage Change Letter

- Monthly Mortgage Payment Change Letter

- Force-Placed Insurance Notification Letter

- Loss Mitigation Application Acknowledgment Letter

- Official Mortgage Payoff Statement Letter

- Notice of Mortgage Ownership Transfer Letter

- First Mortgage Payment Instruction Letter

- Mortgage Delinquency Status Warning Letter

- Private Mortgage Insurance Cancellation Letter

Goodbye Letter from Outgoing Servicer

A goodbye letter from your outgoing mortgage servicer is a formal Notice of Transfer required by law. It informs you that the right to manage your loan has been sold to a new company. The most critical detail to verify is the effective transfer date, which dictates when you must stop paying the old servicer and begin paying the new one. This document ensures a seamless transition, protecting your credit score and payment history during the mandatory sixty-day grace period following the servicer change.

Welcome Letter from Incoming Servicer

Receiving a Welcome Letter from an incoming servicer confirms that the management of your loan has officially transferred. This document is legally required under federal law and contains critical information, including your new account number, payment mailing address, and contact details. It marks the end of the transition period, ensuring your future payments are processed correctly. Always verify the transfer date and update your banking information or autopay settings immediately to avoid late fees or credit reporting issues during the handoff between financial institutions.

Annual Escrow Account Analysis Letter

An Annual Escrow Account Analysis is a mandatory yearly review used to ensure your mortgage escrow balance covers property taxes and insurance premiums. Lenders adjust your monthly payment based on actual costs versus projections. If expenses increased, you may face a shortage, resulting in higher monthly payments or a one-time charge. Conversely, a surplus may trigger a refund check. Carefully reviewing this letter helps you understand changes in your total housing costs and verify that your servicer is accurately managing your tax and insurance disbursements.

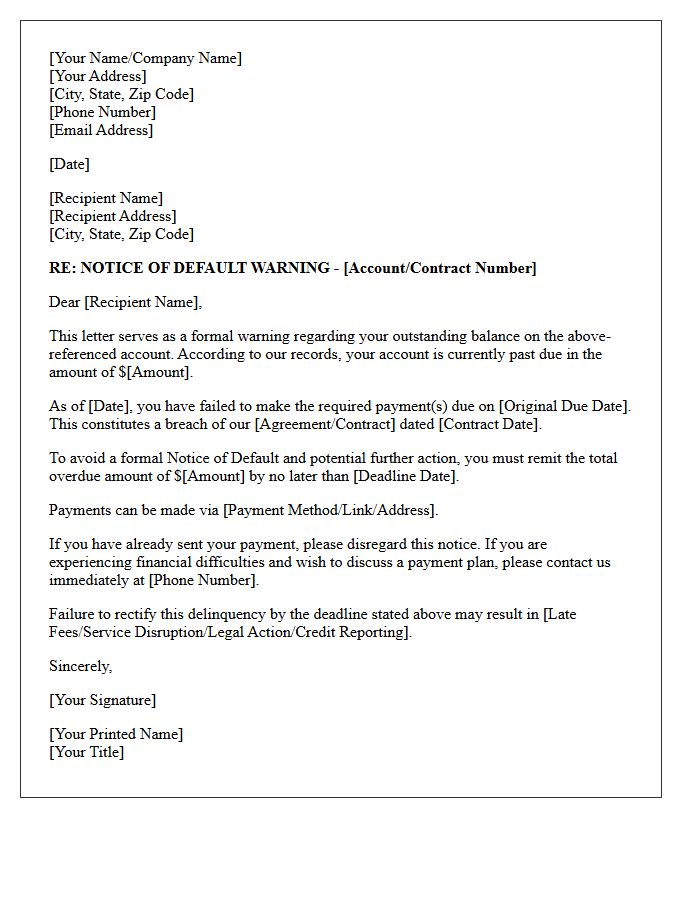

Notice of Default Warning Letter

A Notice of Default is a formal legal warning issued by a lender when a borrower falls behind on mortgage payments. Receiving this letter signifies the official start of the foreclosure process, indicating that the lender intends to reclaim the property unless the debt is resolved. It is crucial to act immediately by contacting your loan servicer to discuss repayment plans or loan modification options. Ignoring this notice can lead to the loss of your home and severe damage to your credit score.

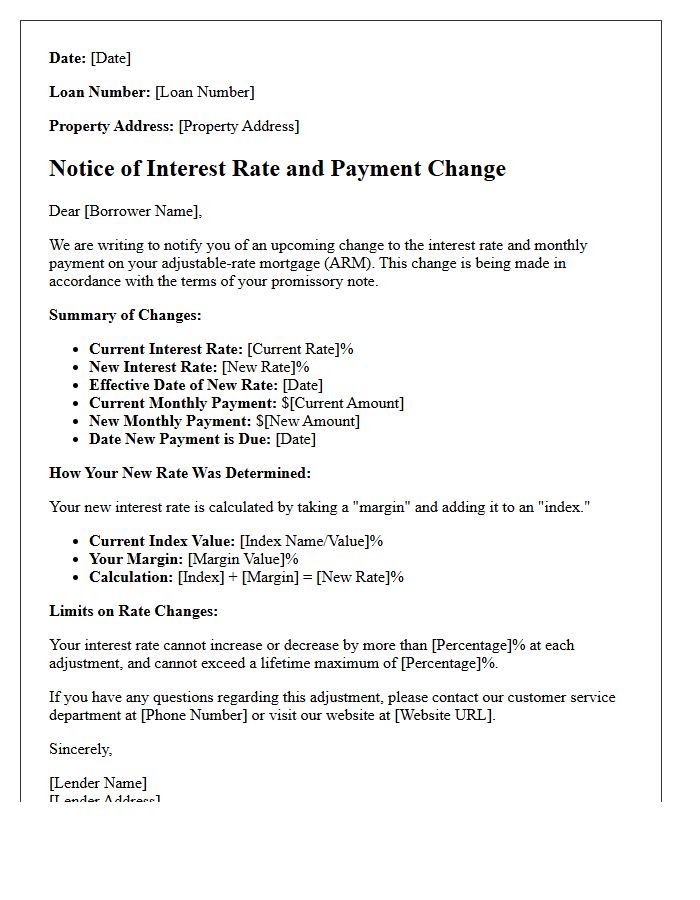

Adjustable Rate Mortgage Change Letter

An Adjustable Rate Mortgage (ARM) Change Letter is a critical notice from your lender informing you of an upcoming interest rate adjustment. This document details your new monthly payment, the current index, and the margin used for calculation. It is essential to review the payment effective date to avoid delinquency. Understanding these fluctuations helps you manage your housing budget effectively. Always verify the math against your original loan terms to ensure accuracy and consider refinancing options if the new rate significantly increases your financial burden.

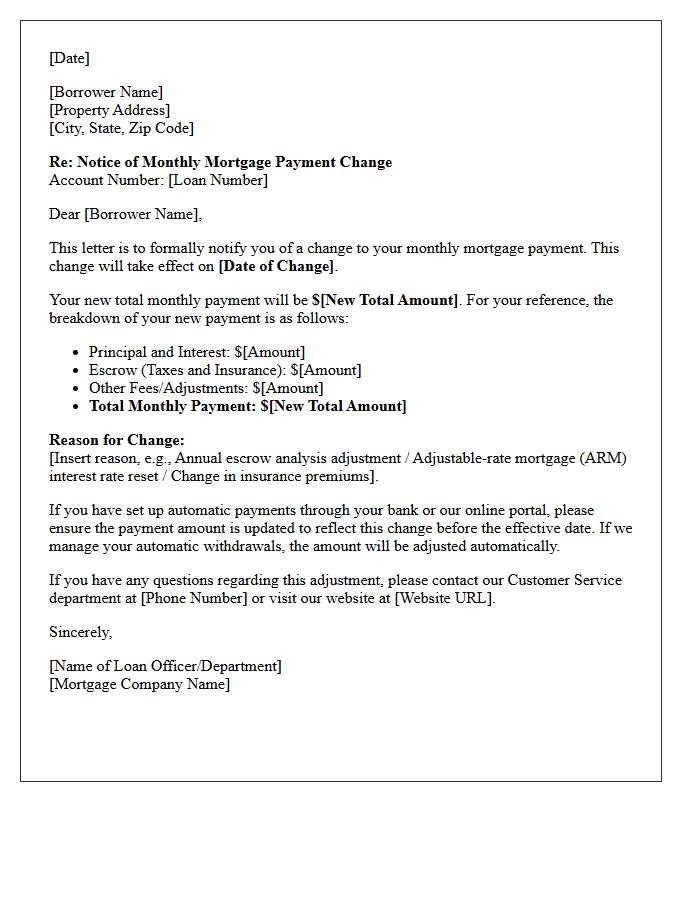

Monthly Mortgage Payment Change Letter

A Monthly Mortgage Payment Change Letter is an official notice from your lender detailing adjustments to your billing amount. This typically occurs due to escrow analysis, reflecting changes in property taxes or homeowners insurance premiums. For those with adjustable-rate mortgages (ARM), it signals an interest rate reset. Reviewing this document immediately is essential to ensure your budget remains accurate and to confirm that all tax assessments are correct. Always verify the effective date to avoid underpayment penalties or unintended escrow shortages in your future financial planning.

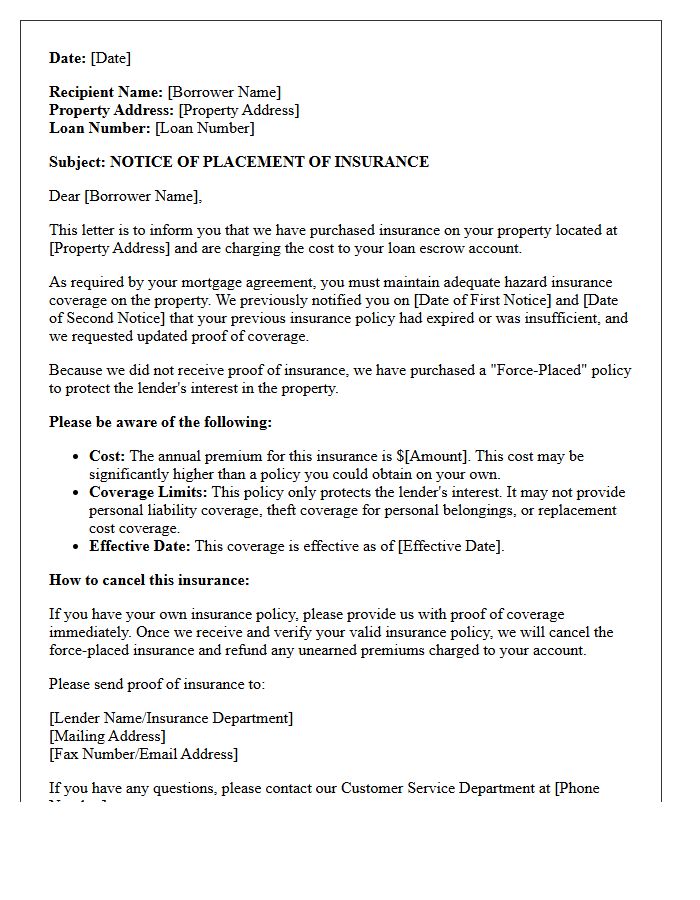

Force-Placed Insurance Notification Letter

A force-placed insurance notification letter is a legal warning sent by your mortgage lender when they believe your homeowners policy has lapsed. This notice informs you that the lender will purchase high-cost coverage on your behalf if you do not provide proof of active insurance within a specific timeframe, typically 45 days. Because this coverage is significantly more expensive and only protects the lender's financial interest in the property, you should immediately contact your insurance agent to verify your policy and prevent unnecessary escrow premium increases.

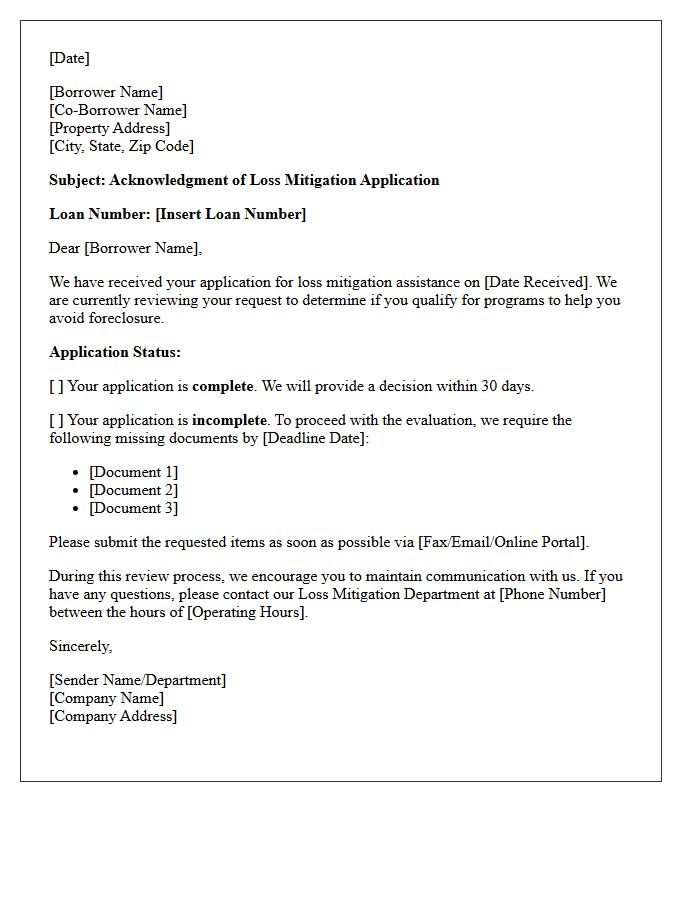

Loss Mitigation Application Acknowledgment Letter

A Loss Mitigation Application Acknowledgment Letter is a formal notice from your mortgage servicer confirming receipt of your request for foreclosure alternatives. Within five business days, the servicer must state if the application is complete or requires additional documentation. This letter is a critical consumer protection under federal law, ensuring your foreclosure rights are preserved. Review the list of missing items immediately to maintain a "complete application" status, which triggers a legal pause on the foreclosure process while your options are formally evaluated by the lender.

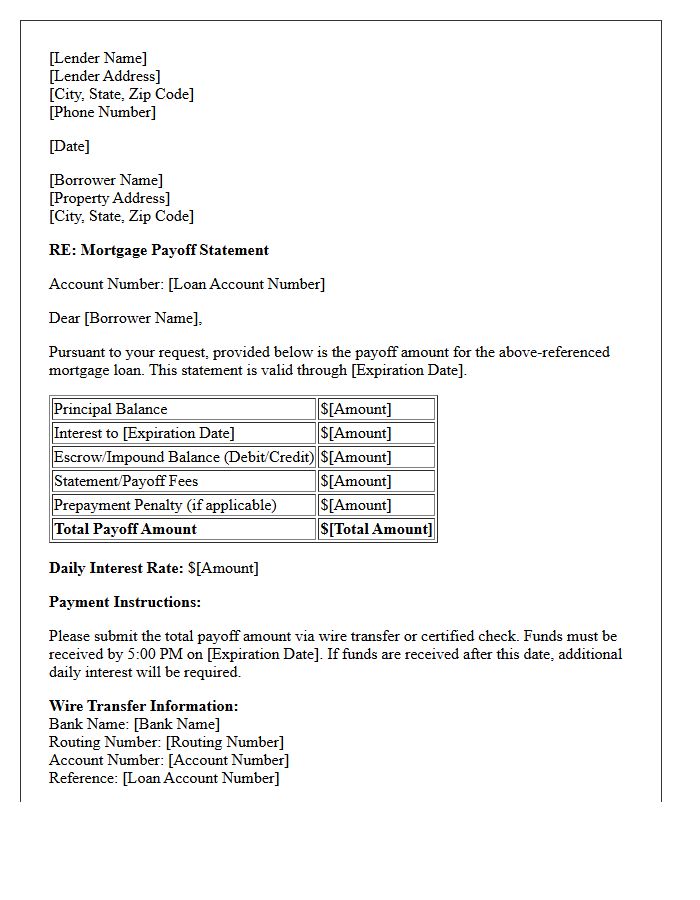

Official Mortgage Payoff Statement Letter

An Official Mortgage Payoff Statement Letter is a formal document from your lender providing the exact total amount required to fully satisfy your loan balance. Unlike a monthly statement, it includes accrued interest, statement fees, and recording costs calculated to a specific effective date. This document is essential for refinancing or selling a home, ensuring the lien is legally released. Always request this letter in writing to guarantee payment accuracy and avoid potential shortfalls that could delay your property's clear title transfer.

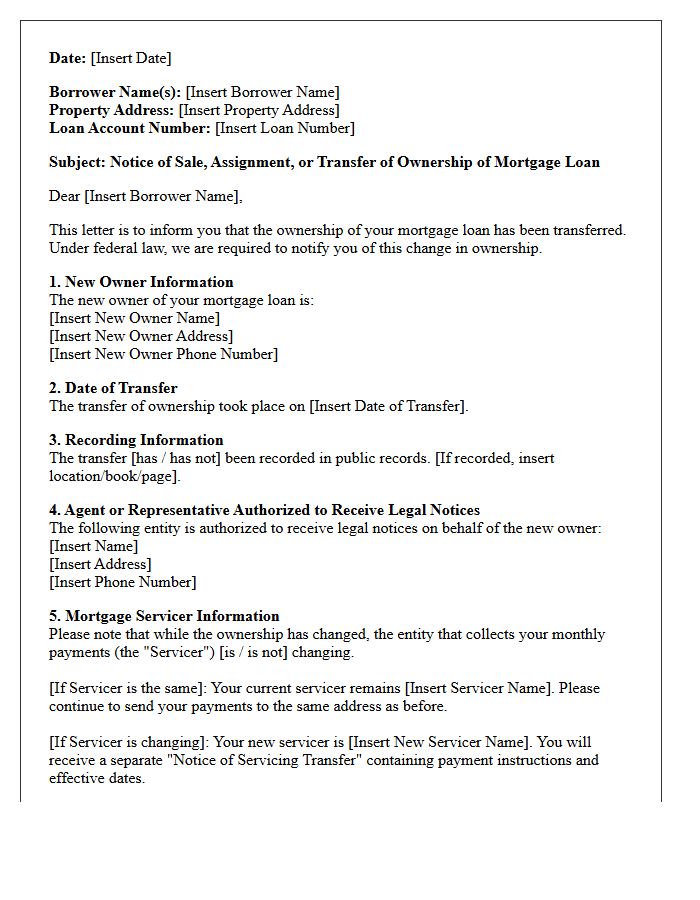

Notice of Mortgage Ownership Transfer Letter

A Notice of Mortgage Ownership Transfer Letter informs you that your mortgage loan owner has changed. This legal document is required under the Truth in Lending Act when your debt is sold to a new investor. It is important to distinguish this from a servicing transfer; while the owner changes, you typically continue making payments to the same servicer unless notified otherwise. Always verify the new owner's identity and contact information provided in the letter to ensure your records remain accurate and to prevent potential payment processing errors.

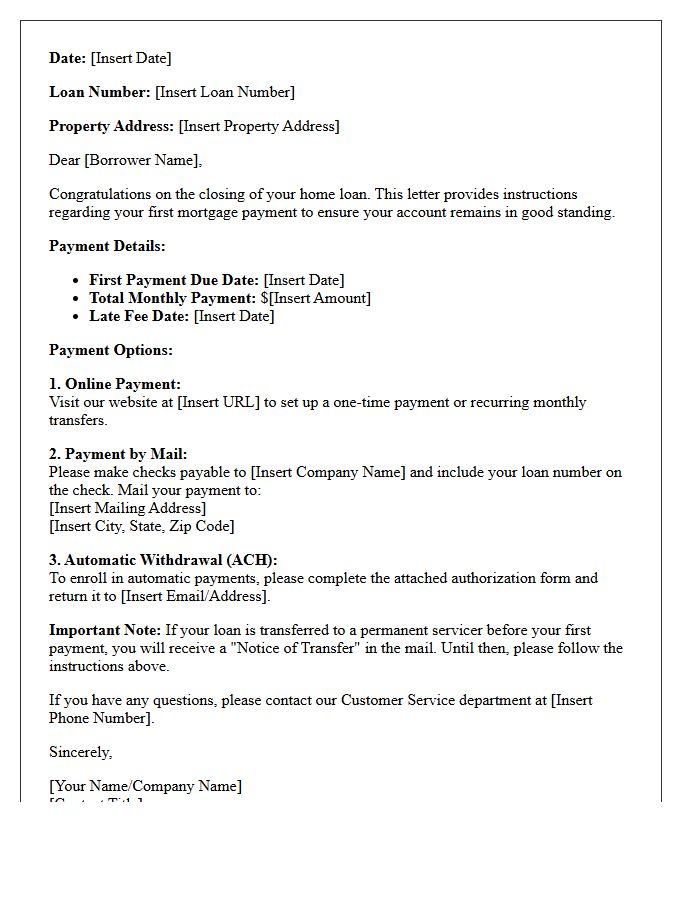

First Mortgage Payment Instruction Letter

A First Mortgage Payment Instruction Letter is a critical document received at closing that outlines how to make your initial loan payment. It prevents delinquency by specifying the exact due date, payment amount, and mailing address. Since your loan might be transferred to a new servicer shortly after closing, this letter serves as a temporary guide until you receive your first official billing statement. Always verify the payment credentials to ensure your funds are credited correctly and to maintain a healthy credit score from the start.

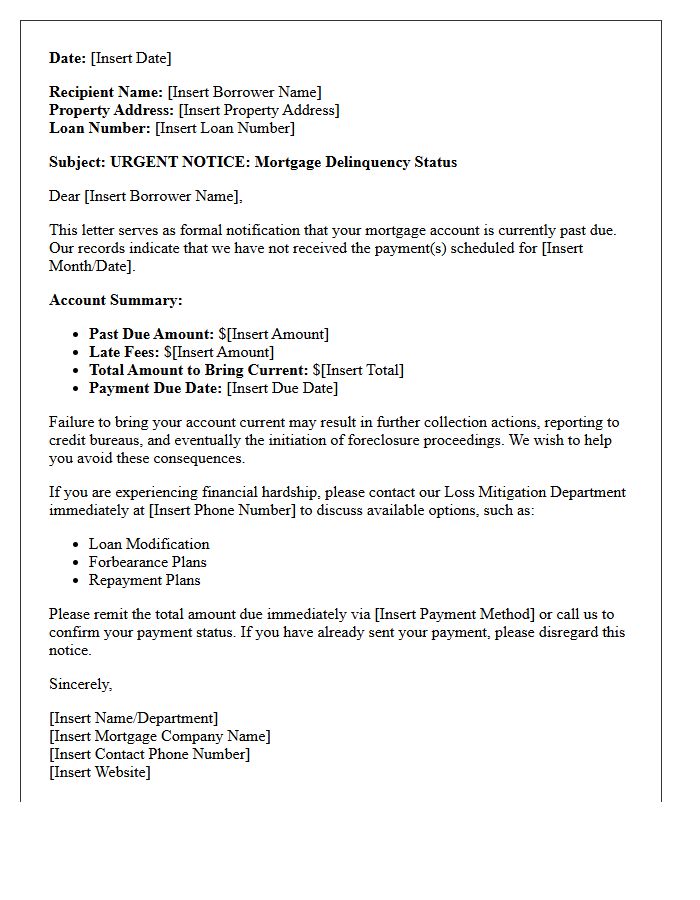

Mortgage Delinquency Status Warning Letter

A Mortgage Delinquency Status Warning Letter is a formal notice issued by lenders when a homeowner misses monthly payments. This critical document serves as a final alert before the foreclosure process begins. It outlines the specific amount overdue, including late fees, and provides a deadline to resolve the default. To protect your home, you must contact your servicer immediately to discuss loss mitigation options, such as loan modification or a repayment plan. Ignoring this warning can lead to legal action and a significant decrease in your credit score.

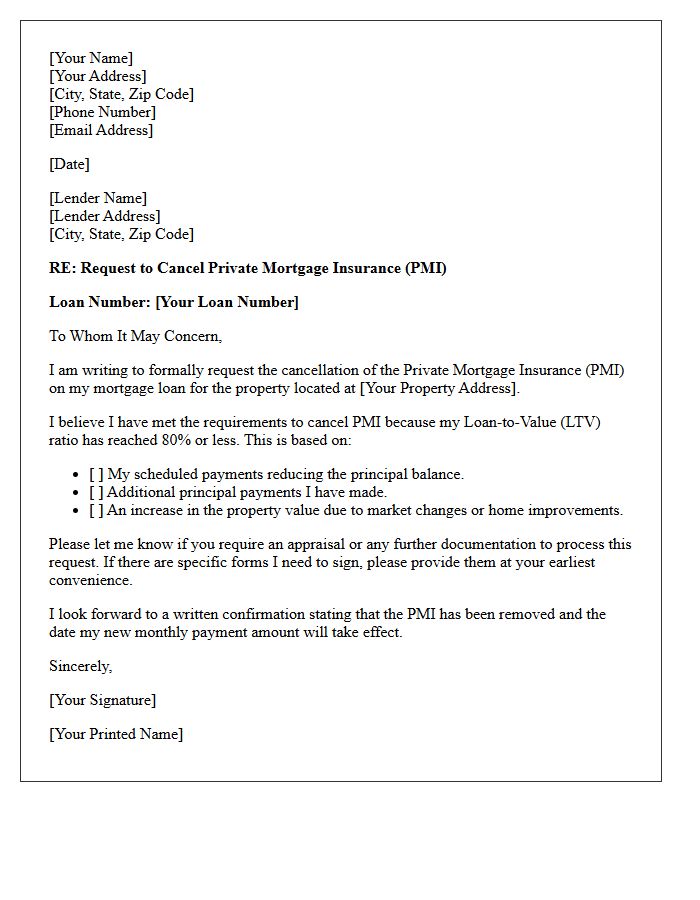

Private Mortgage Insurance Cancellation Letter

A Private Mortgage Insurance (PMI) cancellation letter is a formal written request sent to your lender once you reach 20% equity in your home. Under the Homeowners Protection Act, you have the right to request early termination of PMI premiums if your loan-to-value ratio reaches 80%. Your letter should include your loan number, property address, and a specific request for a valuation or appraisal. Proactively submitting this document can save you thousands of dollars by removing unnecessary monthly insurance costs as soon as you meet the eligibility requirements.

What is a "Hello Letter" from a mortgage servicer?

A "Hello Letter" is an official welcome notice sent by your new mortgage servicer to inform you that they have taken over the administration of your loan, including collecting payments and managing your escrow account.

When should I receive my Hello Letter from the incoming servicer?

Under federal law, the incoming servicer must send you a Hello Letter no later than 15 days after the effective date of the loan transfer to ensure you have the necessary information to make your next payment.

What information is included in a Hello Letter?

The Hello Letter contains the new servicer's contact information, the date they will begin accepting payments, the payment mailing address, and instructions on how to set up your new online account.

Will my mortgage terms change after receiving a Hello Letter?

No, a change in mortgage servicers does not change the terms of your loan; your interest rate, monthly principal and interest amount, and loan duration remain exactly the same as stated in your original promissory note.

What should I do if I receive a Hello Letter from a new servicer?

You should verify the letter's authenticity by comparing it to the "Goodbye Letter" from your previous servicer, update your automated bill pay settings, and register your account on the new servicer's website to monitor your transition.

Comments