Receiving a Notice of Account Sent to Collections can be overwhelming and impact your credit score significantly. This guide explains how to handle debt collectors, verify the validity of the claim, and protect your legal rights during the recovery process. Understanding your options is the first step toward financial resolution. To help you respond effectively, below are some ready to use template.

Image cover: Professional Collection Notice Templates and Best Practices for Debt Recovery

Letter Samples List

- Final Warning Letter Before Account Is Sent To Collections

- Standard Notice Letter Of Account Sent To Collections

- Unpaid Rent Notice Letter Of Account Sent To Collections

- Move-Out Balance Notice Letter Of Account Sent To Collections

- Property Damage Notice Letter Of Account Sent To Collections

- Commercial Tenant Notice Letter Of Account Sent To Collections

- Eviction Judgment Notice Letter Of Account Sent To Collections

- Homeowner Association Dues Notice Letter Of Account Sent To Collections

- Unpaid Utilities Notice Letter Of Account Sent To Collections

- Lease Break Penalty Notice Letter Of Account Sent To Collections

- Outstanding Late Fees Notice Letter Of Account Sent To Collections

- Final Ledger And Notice Letter Of Account Sent To Collections

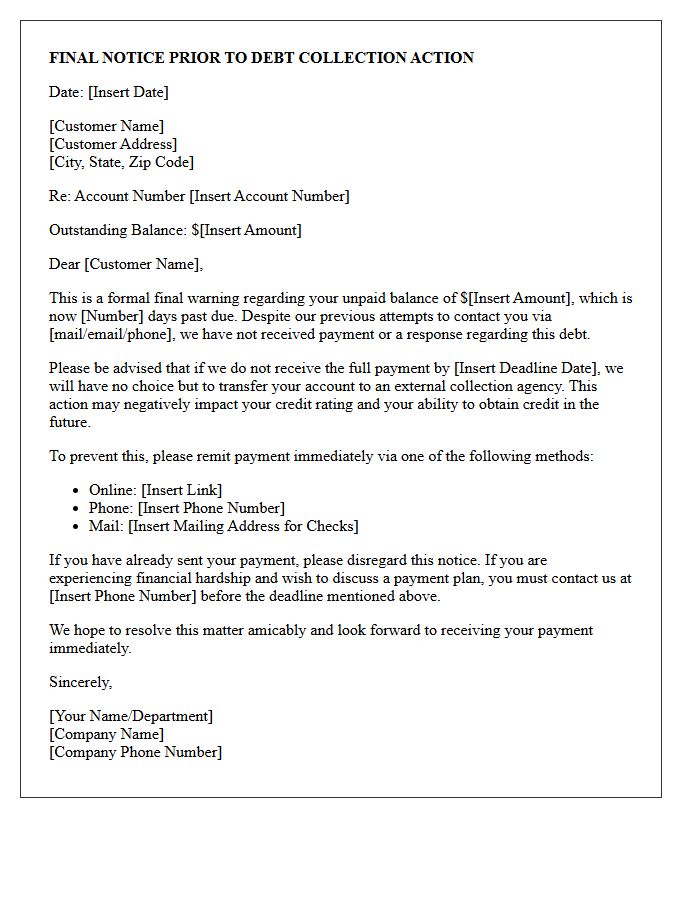

Final Warning Letter Before Account Is Sent To Collections

A Final Warning Letter is the last official notice sent before an unpaid debt is transferred to a third-party collection agency. This document serves as a final opportunity to settle the balance or establish a payment plan to avoid severe consequences. Receiving this letter indicates that internal recovery efforts have ended. Ignoring this notice can lead to credit score damage, additional late fees, and potential legal action. To protect your financial standing, you must respond immediately to verify the debt or negotiate a settlement before the deadline expires.

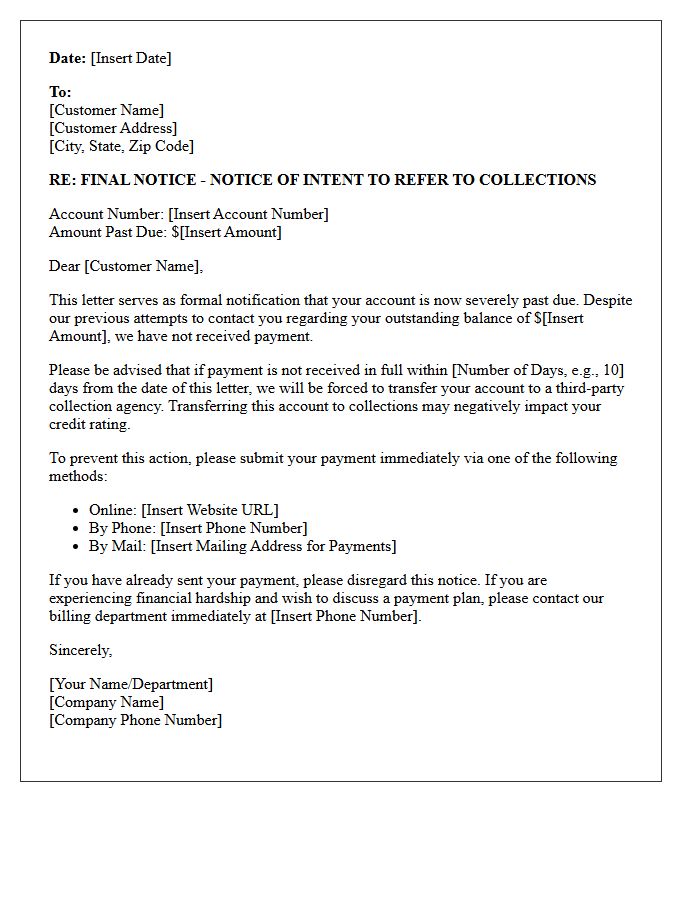

Standard Notice Letter Of Account Sent To Collections

A standard notice letter informs you that an outstanding debt has been transferred to a collection agency. Under the Fair Debt Collection Practices Act (FDCPA), this document must include the exact amount owed, the original creditor's name, and a statement regarding your right to dispute the charge. You have a 30-day validation period to request written proof of the debt. Reviewing this letter immediately is essential to protect your credit score and ensure the debt information is accurate before further enforcement actions occur.

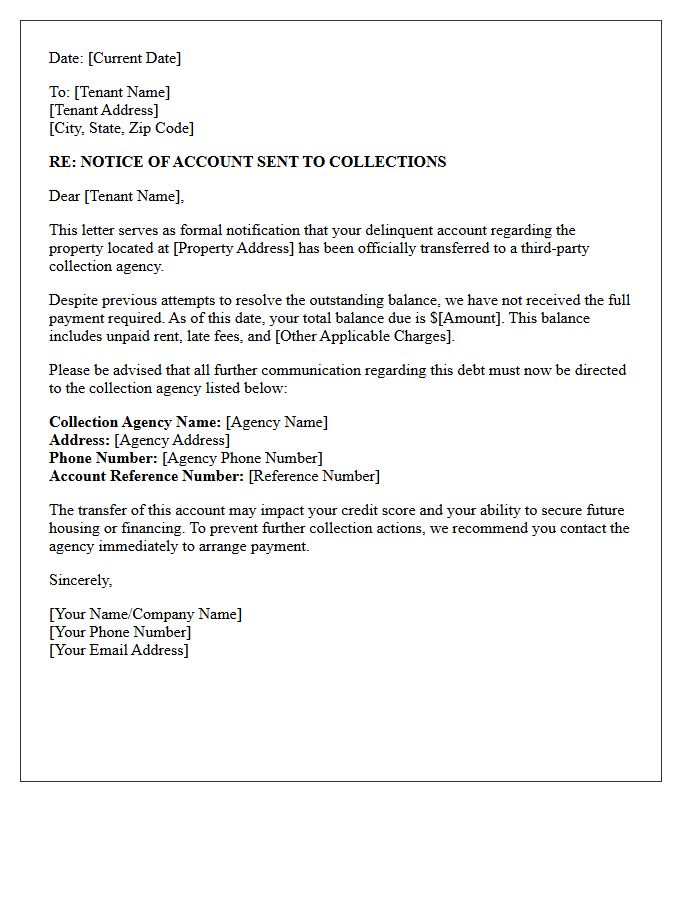

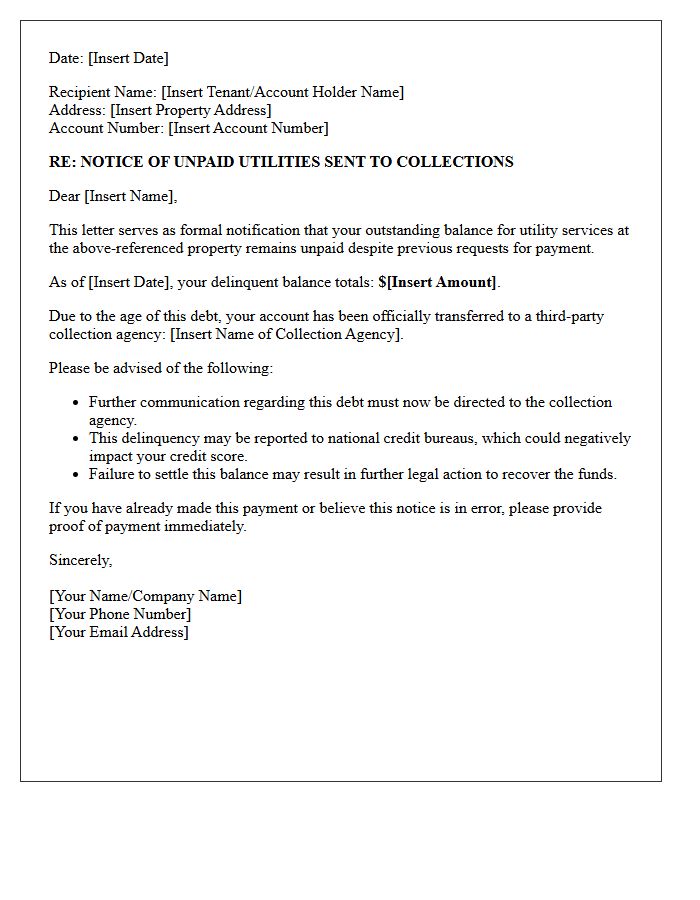

Unpaid Rent Notice Letter Of Account Sent To Collections

An unpaid rent notice serves as a final formal demand before a landlord transfers your debt to a collections agency. Receiving this letter signifies that your delinquency is being documented, which can severely damage your credit score and future housing eligibility. To protect your financial reputation, it is vital to respond immediately. You should either provide proof of payment or negotiate a settlement to prevent the account from appearing on public records, as collection entries can remain on your credit report for up to seven years.

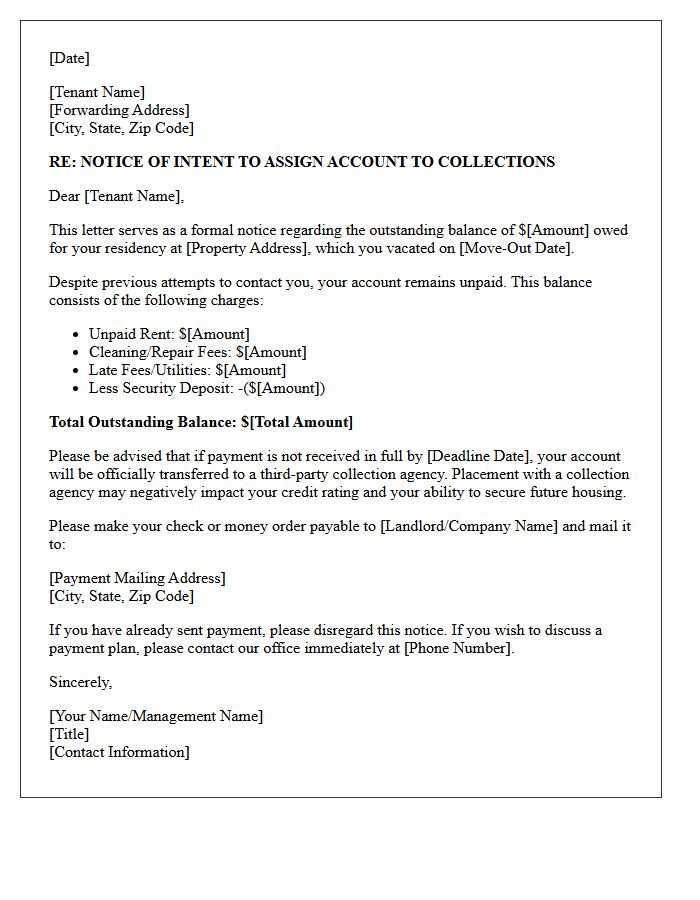

Move-Out Balance Notice Letter Of Account Sent To Collections

Receiving a Move-Out Balance Notice indicates your former landlord claims unpaid charges for rent, damages, or cleaning. When marked as Sent to Collections, the debt has been transferred to a third-party agency. This action can severely damage your credit score and hinder future housing applications. You must act quickly to request a Debt Validation Letter to verify the accuracy of the charges. Under the Fair Debt Collection Practices Act, you have the right to dispute discrepancies or negotiate a settlement to prevent long-term financial consequences.

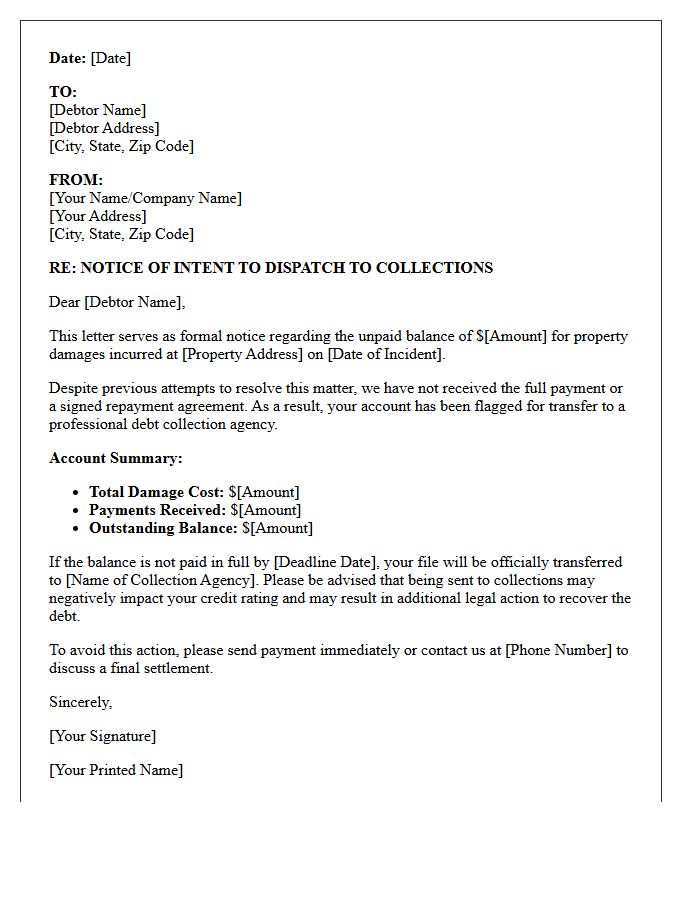

Property Damage Notice Letter Of Account Sent To Collections

A property damage notice letter regarding an account sent to collections is a formal warning that an outstanding debt remains unpaid. Receiving this indicates that the creditor has transferred your file to a third-party agency for recovery. It is crucial to respond promptly to verify the debt's accuracy and prevent negative impacts on your credit score. You should request a debt validation letter and keep detailed records of all communication. Addressing this notice immediately can help you negotiate a settlement or dispute unauthorized charges before legal action or further credit damage occurs.

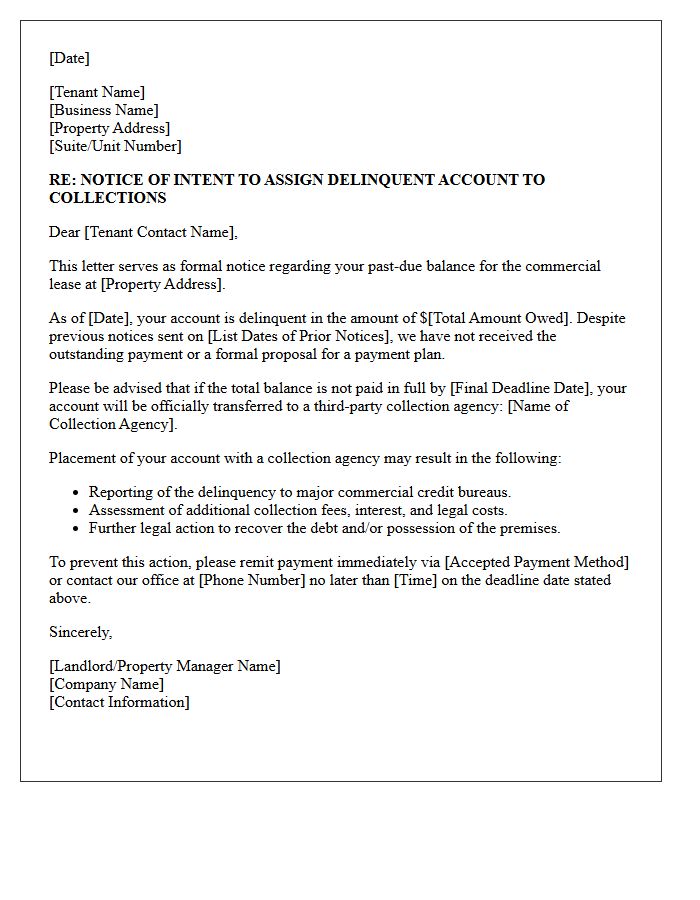

Commercial Tenant Notice Letter Of Account Sent To Collections

A Commercial Tenant Notice Letter serves as a formal warning before a delinquency is reported to credit bureaus. This document notifies the lessee that their outstanding rent arrears have been transferred to a debt collection agency. It typically outlines the total balance due, including late fees and interest, while providing a final opportunity for dispute resolution or payment. Issuing this notice is a critical step for landlords to document lease enforcement and protect their legal rights during potential eviction proceedings or commercial litigation.

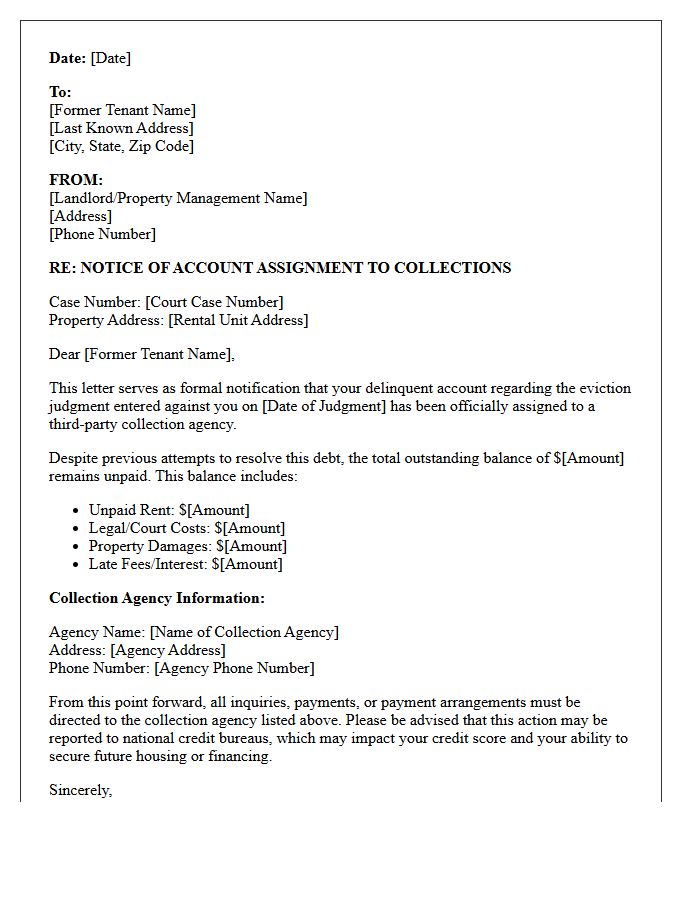

Eviction Judgment Notice Letter Of Account Sent To Collections

Receiving an eviction judgment notice signifies a legal ruling that grants a landlord possession of the property and confirms outstanding debt. When this account is sent to collections, it severely impacts your credit score and financial reputation for up to seven years. Debt collectors will pursue the balance, including back rent and legal fees. To mitigate long-term damage, you should prioritize settling the debt or negotiating a payment plan immediately to prevent aggressive collection tactics and improve your chances of securing future housing and credit approvals.

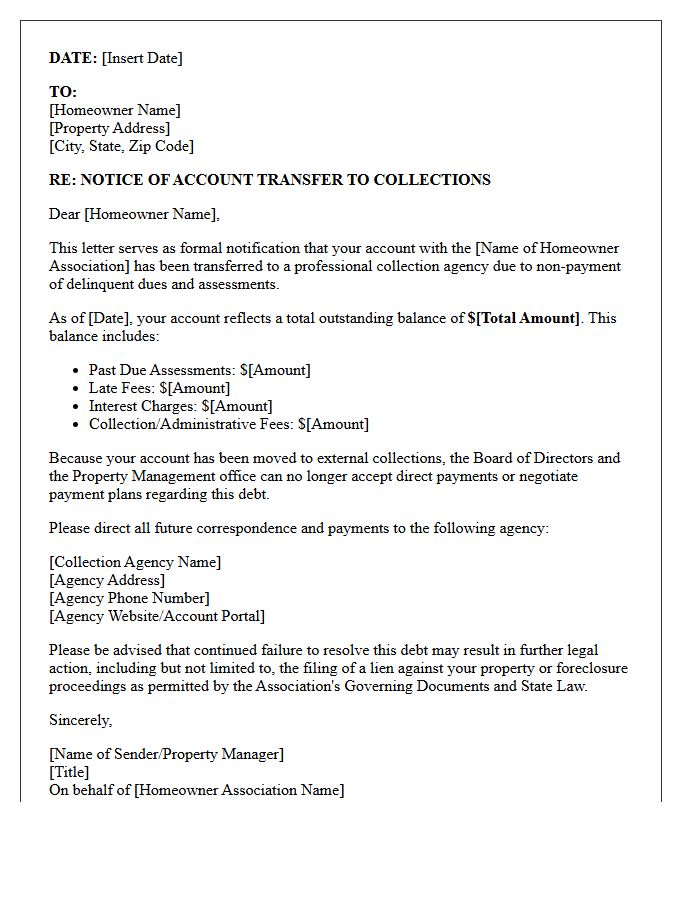

Homeowner Association Dues Notice Letter Of Account Sent To Collections

Receiving a Homeowner Association (HOA) collections notice indicates that your account is seriously delinquent. This formal letter serves as a final warning before legal action, such as a property lien or foreclosure, is initiated to recover unpaid assessments. To protect your homeownership rights, you must immediately verify the balance, review the ledger for accuracy, and contact the association to discuss a repayment plan. Ignoring this notice can lead to escalating attorney fees and administrative costs, significantly increasing your total debt and endangering your title status.

Unpaid Utilities Notice Letter Of Account Sent To Collections

Receiving an unpaid utilities notice indicates your delinquent account has been transferred to a third-party collection agency. This transition significantly impacts your credit score and may lead to service disconnection at your current or future residence. It is crucial to verify the debt amount immediately and negotiate a payment plan to prevent further legal action. Resolving this balance quickly is the most effective way to protect your financial reputation and ensure continued access to essential utility services. Always request written confirmation once the debt is settled.

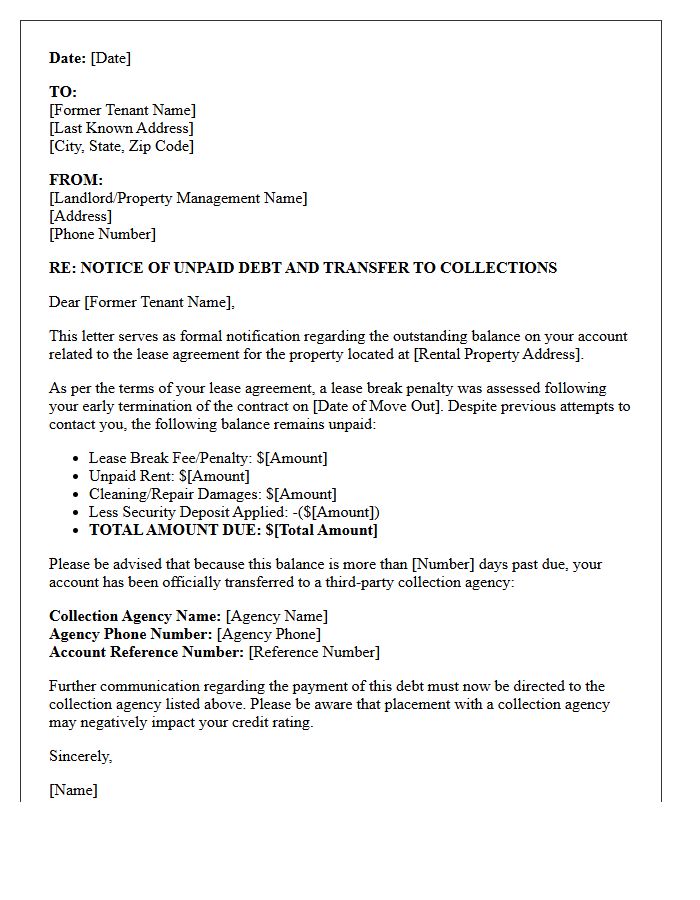

Lease Break Penalty Notice Letter Of Account Sent To Collections

If you break a lease, the landlord may issue a Lease Break Penalty Notice for unpaid rent or liquidated damages. If this balance remains unpaid, your account sent to collections can severely damage your credit score for seven years. It is critical to negotiate a settlement or verify the debt's accuracy immediately. Always request a debt validation letter to ensure the charges comply with local laws. Resolving this early prevents legal action and ensures your future ability to secure rental housing remains intact.

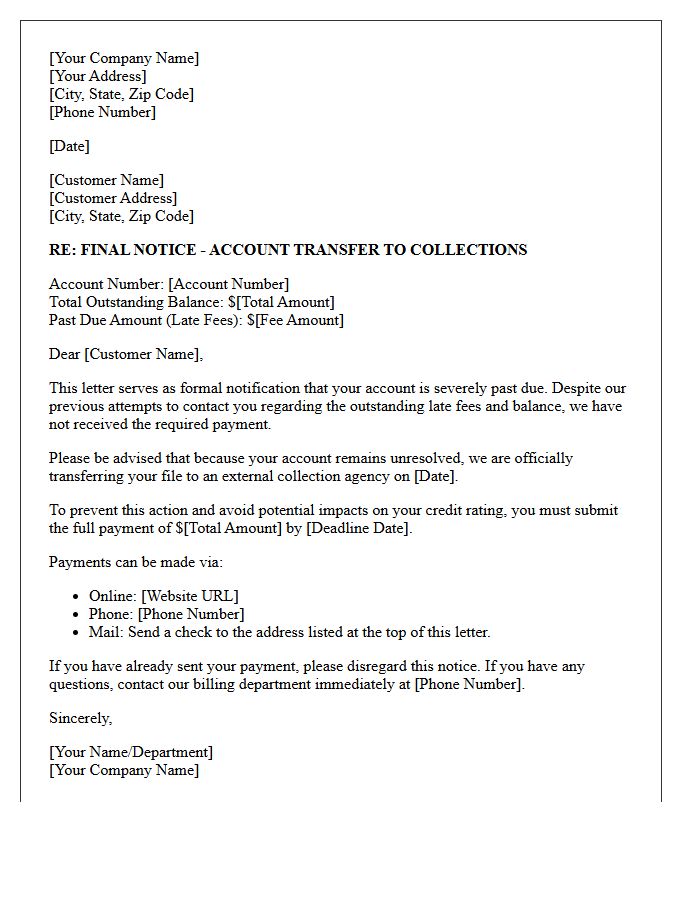

Outstanding Late Fees Notice Letter Of Account Sent To Collections

Receiving an Outstanding Late Fees Notice is a final warning before your account is officially sent to collections. This formal letter indicates that previous payment requests were ignored and legal action or credit reporting may follow. To protect your credit score, you must act immediately by paying the balance or negotiating a settlement. Once a debt reaches a collection agency, it can remain on your credit history for seven years. Always verify the debt amount and request a written validation to ensure the charges are accurate before making a payment.

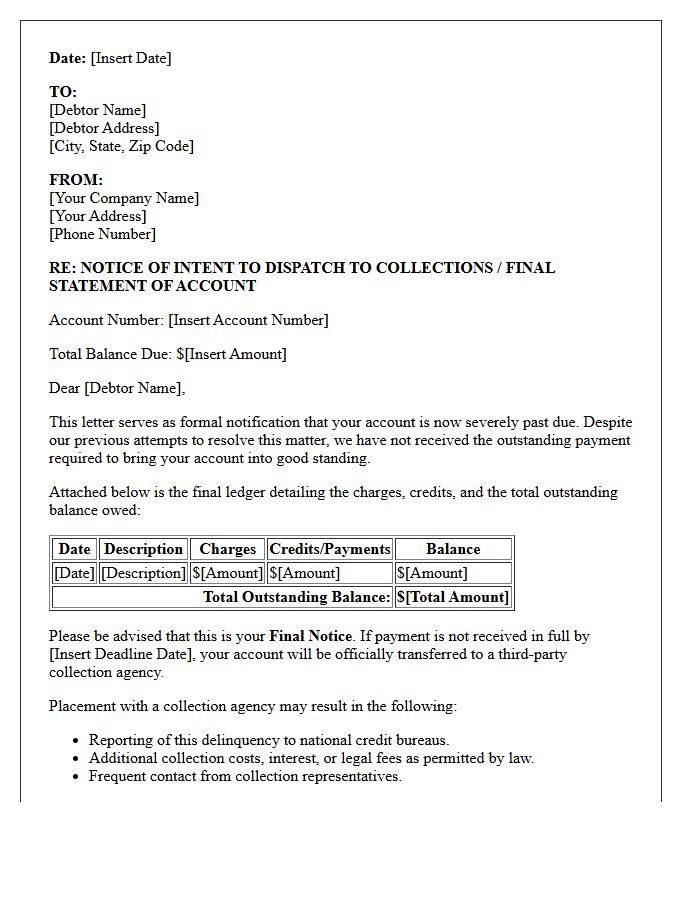

Final Ledger And Notice Letter Of Account Sent To Collections

Receiving a final ledger signifies the absolute conclusion of your billing cycle, detailing all outstanding debts, payments, and interest. If accompanied by a notice letter of account sent to collections, it indicates the creditor has transferred your debt to a third-party agency. This action can severely impact your credit score and lead to persistent recovery efforts. To mitigate long-term financial damage, verify the ledger's accuracy immediately and consider a settlement or payment plan before the default is formally reported to credit bureaus.

What does a "Notice of Account Sent to Collections" mean?

A notice of account sent to collections is a formal notification stating that your past-due debt has been transferred or sold to a third-party debt collection agency. This indicates that the original creditor has given up on collecting the debt themselves and the agency will now pursue the balance owed.

How will a collection account affect my credit score?

Having an account sent to collections can significantly lower your credit score and remain on your credit report for up to seven years from the date of the original delinquency. It signals to future lenders that you failed to fulfill the terms of a previous credit agreement, which may make it harder to secure loans or low interest rates.

Can I still pay the original creditor after receiving a collections notice?

It depends on whether the debt was assigned or sold. If the creditor still owns the debt but hired an agency to collect it, you may be able to pay them directly; however, if the debt was sold to a lead buyer, you must typically negotiate and pay the collection agency listed on the notice.

What are my rights under the Fair Debt Collection Practices Act (FDCPA)?

Under the FDCPA, you have the right to request debt validation, dispute the debt in writing within 30 days, and be free from harassment. Debt collectors are prohibited from calling at unreasonable hours, using abusive language, or threatening legal action they do not intend to take.

How should I respond to a notice of account sent to collections?

You should first verify the debt by sending a written request for debt validation to ensure the amount and creditor are accurate. Once verified, you can choose to pay the balance in full, negotiate a settlement for a lower amount, or set up a payment plan to resolve the debt and prevent further collection activity.

Comments