Effective financial oversight requires a formal Management Letter on Accounts Receivable Aging and Allowance for Doubtful Accounts to address valuation risks. This report evaluates the collectability of outstanding invoices and ensures bad debt provisions align with accounting standards. Strengthening these internal controls improves cash flow accuracy and financial statement integrity. To assist your reporting, below are some ready to use template.

Image cover: Mastering Accounts Receivable Aging and Allowance for Doubtful Accounts: Management Letter Samples and Templates

Letter Samples List

- Management Letter on Accounts Receivable Aging and Allowance Deficiencies

- Audit Observations Letter Regarding Accounts Receivable Aging Practices

- Management Letter on Allowance for Doubtful Accounts Methodology Review

- Advisory Letter on Accounts Receivable Aging Categorization Discrepancies

- Management Letter Concerning Accounts Receivable Valuation and Aging Controls

- Findings Letter on Allowance for Doubtful Accounts Estimation Adequacy

- Management Letter on Historical Accounts Receivable Aging Trends

- Control Weakness Letter Regarding Accounts Receivable Aging Reports

- Management Letter on Allowance for Doubtful Accounts Policy Compliance

- Recommendation Letter for Improving Accounts Receivable Aging Oversight

- Management Letter on Uncollectible Accounts and Allowance Assumptions

- Evaluation Letter of Accounts Receivable Aging and Provision Procedures

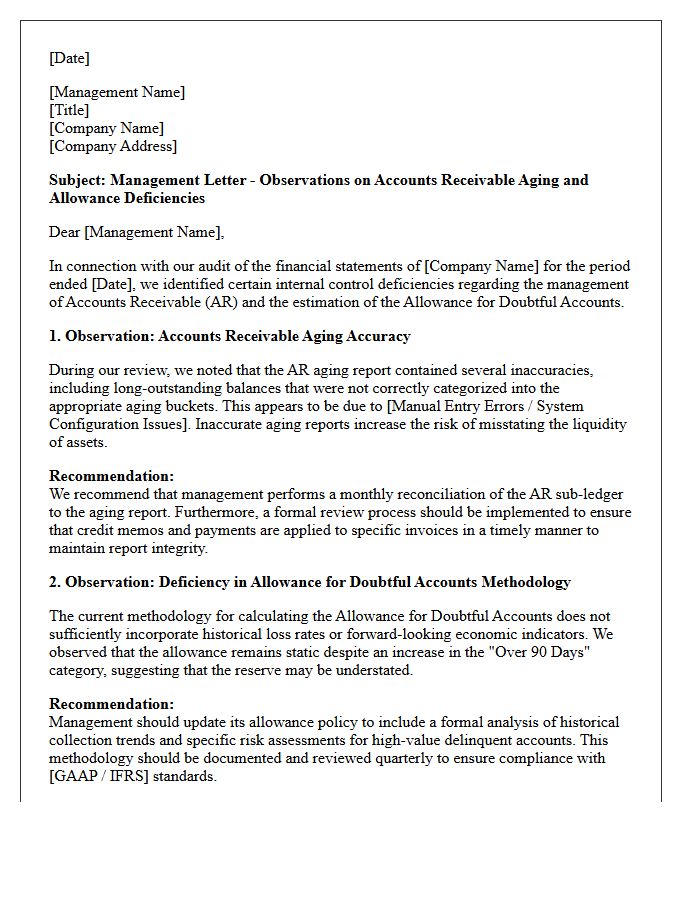

Management Letter on Accounts Receivable Aging and Allowance Deficiencies

A management letter addresses critical internal control weaknesses regarding Accounts Receivable Aging and Allowance for Doubtful Accounts. It highlights inaccuracies in debt categorization and insufficient valuation methods for bad debt reserves. These deficiencies suggest that the financial statements may misrepresent asset liquidity and net realizable value. Timely remediation is essential to ensure GAAP compliance, improve collection cycles, and provide stakeholders with a transparent view of the company's credit risk and operational health.

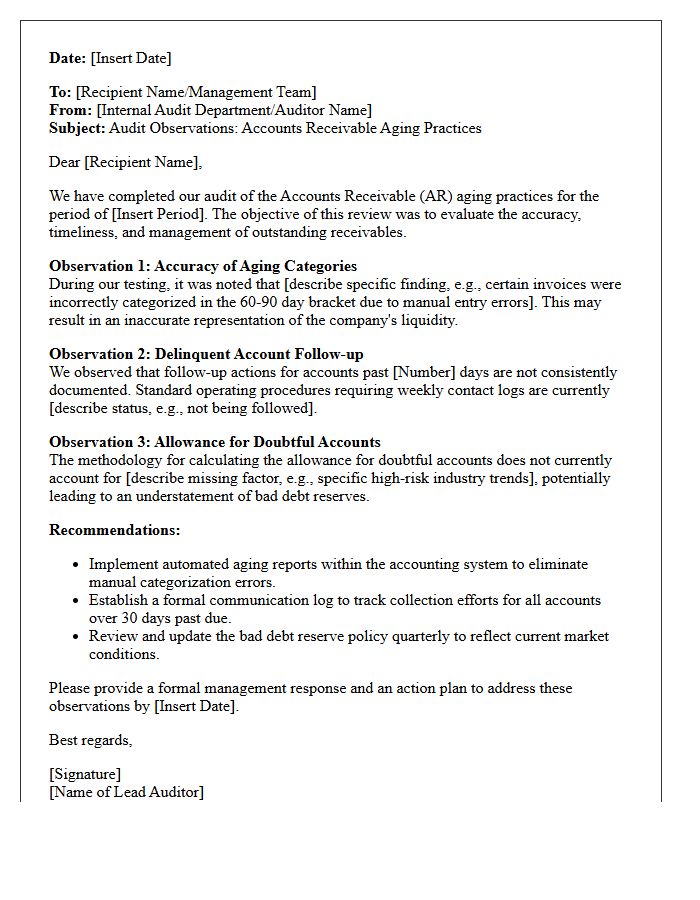

Audit Observations Letter Regarding Accounts Receivable Aging Practices

An Audit Observations Letter regarding accounts receivable aging practices identifies risks in how a company tracks overdue payments. It highlights valuation accuracy issues where long-outstanding balances may require write-offs. This document ensures internal controls are strengthened to prevent financial misstatement. By addressing these findings, management improves cash flow predictability and ensures the aging report reflects true collectability. Proper categorization of receivables is essential for maintaining compliance with accounting standards and providing stakeholders with a transparent view of the company's current asset liquidity and overall financial health.

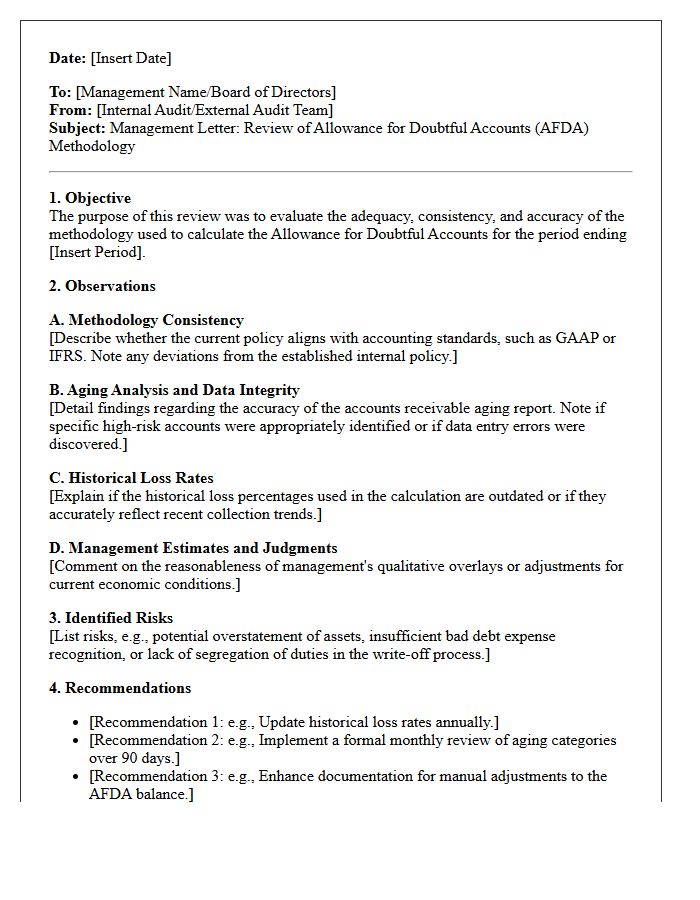

Management Letter on Allowance for Doubtful Accounts Methodology Review

A Management Letter provides essential feedback on the Allowance for Doubtful Accounts methodology during an audit. It evaluates if the estimation process for uncollectible receivables aligns with financial reporting frameworks like GAAP or IFRS. Auditors use this document to highlight internal control weaknesses, such as outdated loss rates or insufficient data validation. Addressing these findings ensures the balance sheet reflects a realistic valuation of assets. Effective oversight of this methodology reduces the risk of material misstatements and improves the overall accuracy of financial statements and credit risk assessment.

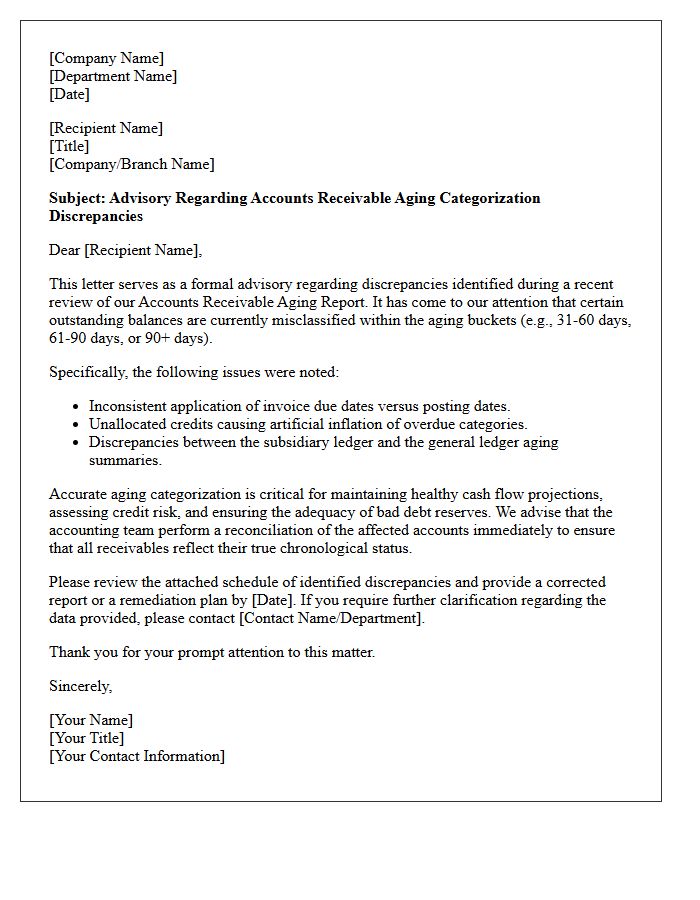

Advisory Letter on Accounts Receivable Aging Categorization Discrepancies

An advisory letter regarding accounts receivable aging discrepancies alerts organizations to inconsistencies between subsidiary ledgers and general ledger balances. It is crucial for maintaining financial reporting accuracy and identifying potential internal control weaknesses. These letters highlight risks such as overlooked bad debt or misstated liquidity levels. Timely reconciliation of these categorizations ensures that aging schedules correctly reflect overdue invoices, which is essential for effective cash flow management and audit compliance. Addressing these discrepancies promptly prevents material misstatements in financial statements and improves the overall integrity of a company's credit management processes.

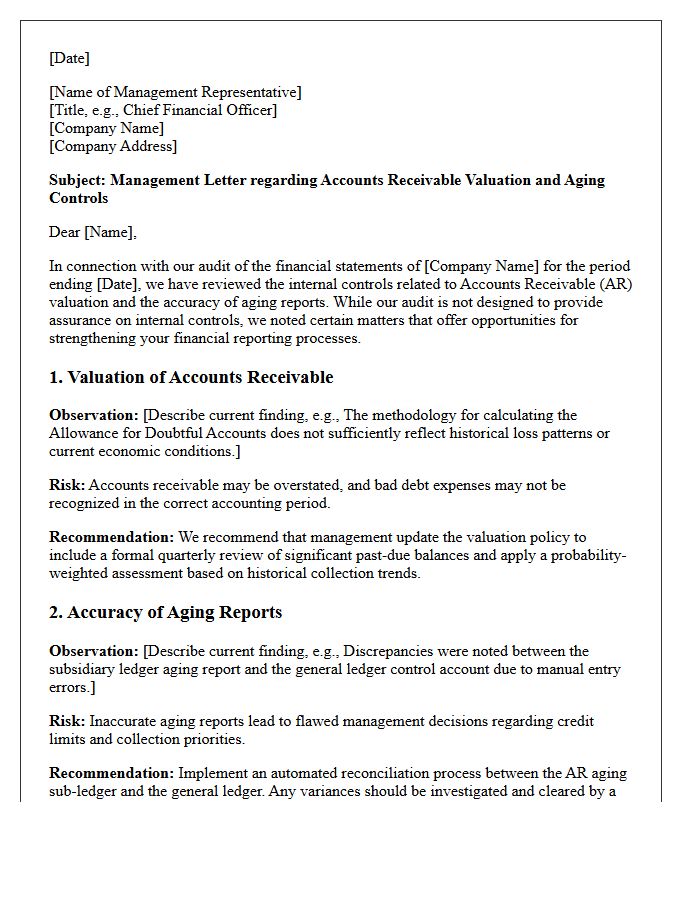

Management Letter Concerning Accounts Receivable Valuation and Aging Controls

A management letter regarding accounts receivable focuses on the valuation of outstanding invoices and the effectiveness of aging controls. It evaluates if the allowance for doubtful accounts accurately reflects potential losses. Auditors examine the accuracy of aging reports to ensure timely collection efforts and identify long-overdue balances. Strengthening these internal controls reduces the risk of financial misstatement and improves cash flow predictability. Management must implement rigorous reconciliation procedures and periodic reviews of customer credit limits to safeguard assets and ensure financial reporting integrity remains reliable for stakeholders.

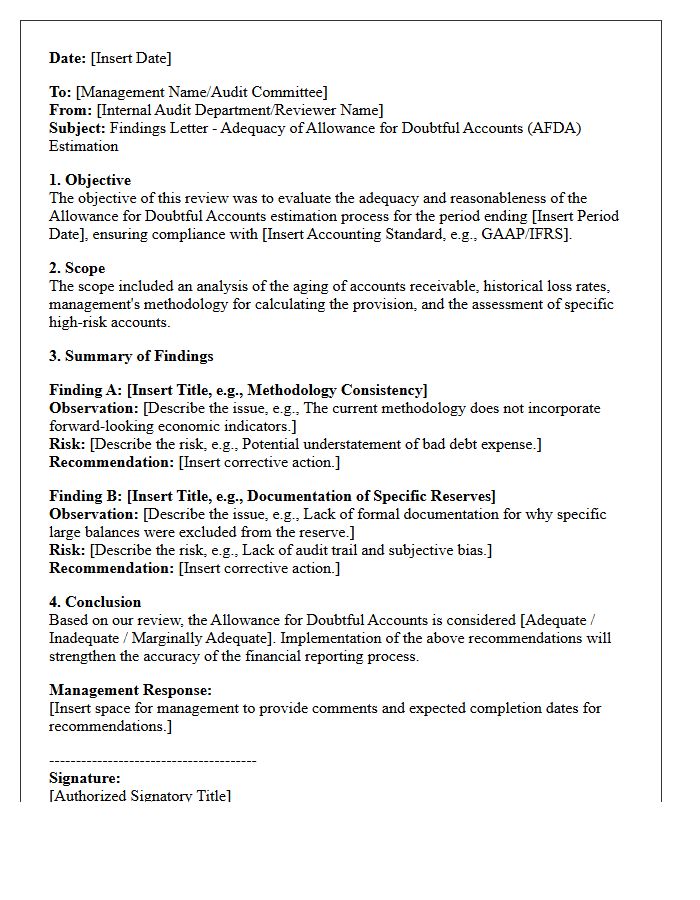

Findings Letter on Allowance for Doubtful Accounts Estimation Adequacy

A Findings Letter assessing the Allowance for Doubtful Accounts (AFDA) evaluates whether a company's bad debt reserves accurately reflect its accounts receivable collectability. Auditors analyze historical loss data, current economic conditions, and aging reports to determine if the estimation method is adequate. If the provision is insufficient, the letter outlines required adjustments to prevent overstated net income and assets. Ensuring a precise AFDA estimation is vital for financial statement integrity and compliance with accounting standards, directly impacting a firm's reported profitability and risk management profile.

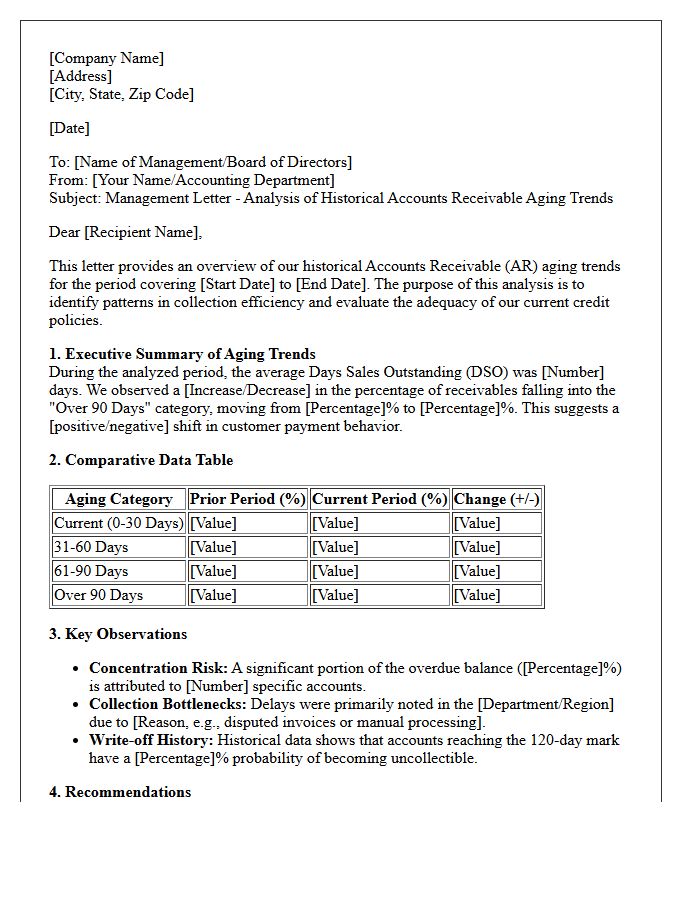

Management Letter on Historical Accounts Receivable Aging Trends

A management letter regarding historical accounts receivable aging trends evaluates the collectability of outstanding debts over time. It highlights liquidity risks by identifying shifts in customer payment behaviors and the effectiveness of credit policies. By analyzing these long-term patterns, management can pinpoint chronic delays, estimate the allowance for doubtful accounts more accurately, and implement strategies to improve cash flow. Understanding these trends is essential for assessing financial stability and ensuring the reported value of assets remains realistic and verifiable for stakeholders.

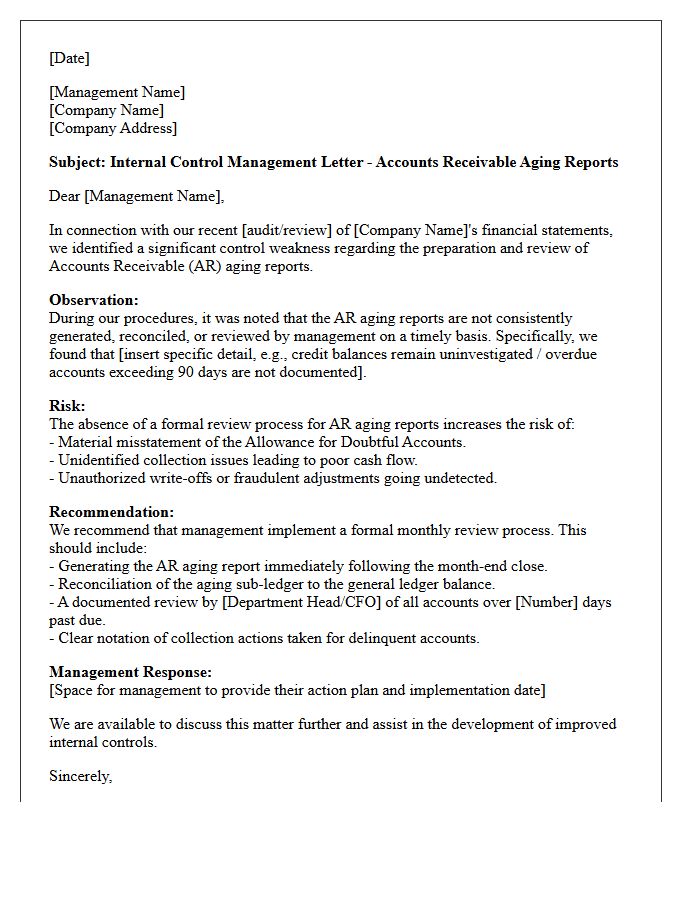

Control Weakness Letter Regarding Accounts Receivable Aging Reports

A control weakness letter identifies critical deficiencies in financial oversight, specifically targeting accounts receivable aging reports. These letters highlight risks like inaccurate bad debt estimations, poor collection tracking, and potential revenue leakage. Management must address these findings to ensure financial statement integrity and robust internal controls. Failure to rectify documented gaps can lead to material misstatements, increased audit scrutiny, and weakened cash flow management. Understanding these weaknesses is essential for maintaining transparent reporting and operational efficiency within the organization's credit cycle.

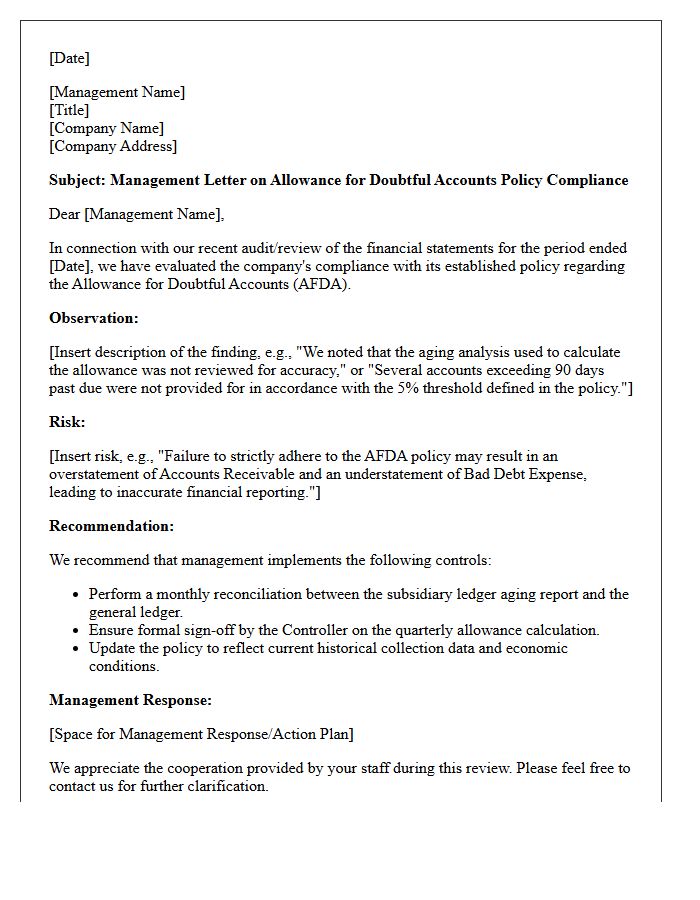

Management Letter on Allowance for Doubtful Accounts Policy Compliance

A management letter serves as a critical communication tool for auditors to report internal control weaknesses. Regarding the Allowance for Doubtful Accounts, this document highlights gaps in policy compliance, ensuring bad debt estimates align with financial reporting standards. It identifies issues such as outdated aging schedules or insufficient documentation for write-offs. Prioritizing compliance with established accounting policies reduces the risk of material misstatements. Management must address these findings to strengthen credit risk oversight and ensure the valuation of receivables remains accurate and transparent for stakeholders.

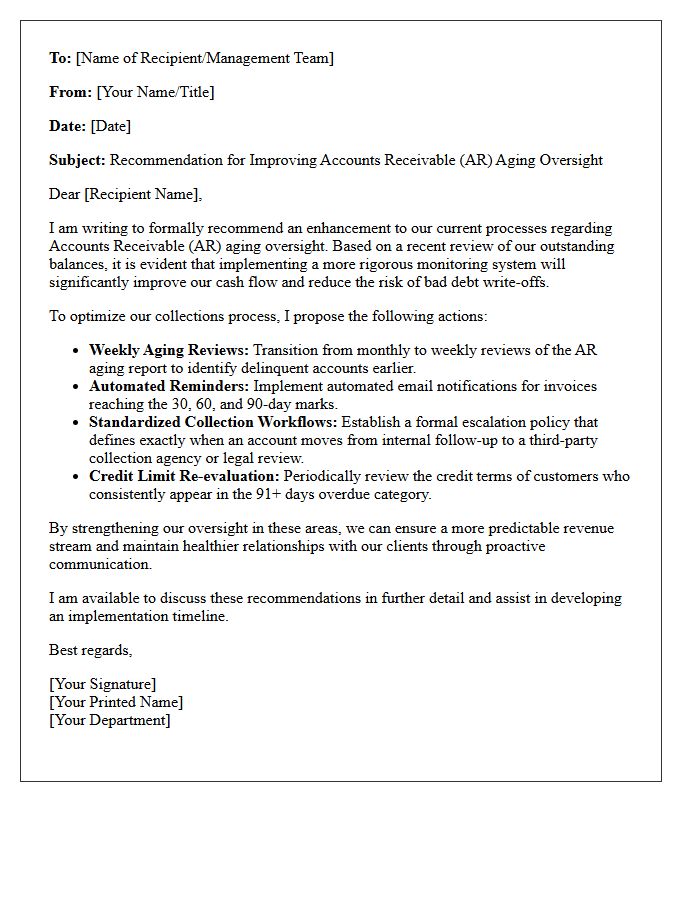

Recommendation Letter for Improving Accounts Receivable Aging Oversight

A formal recommendation letter for improving accounts receivable aging oversight should emphasize standardized reporting to ensure financial transparency. It is crucial to implement automated tracking tools that categorize overdue invoices by specific time buckets. This proactive approach identifies high-risk accounts early, reducing the average collection period and enhancing operational cash flow. Highlighting the need for regular review cycles and clear escalation protocols ensures consistent accountability. By refining these internal controls, management can minimize bad debt write-offs and maintain a healthy balance sheet through more effective credit management strategies.

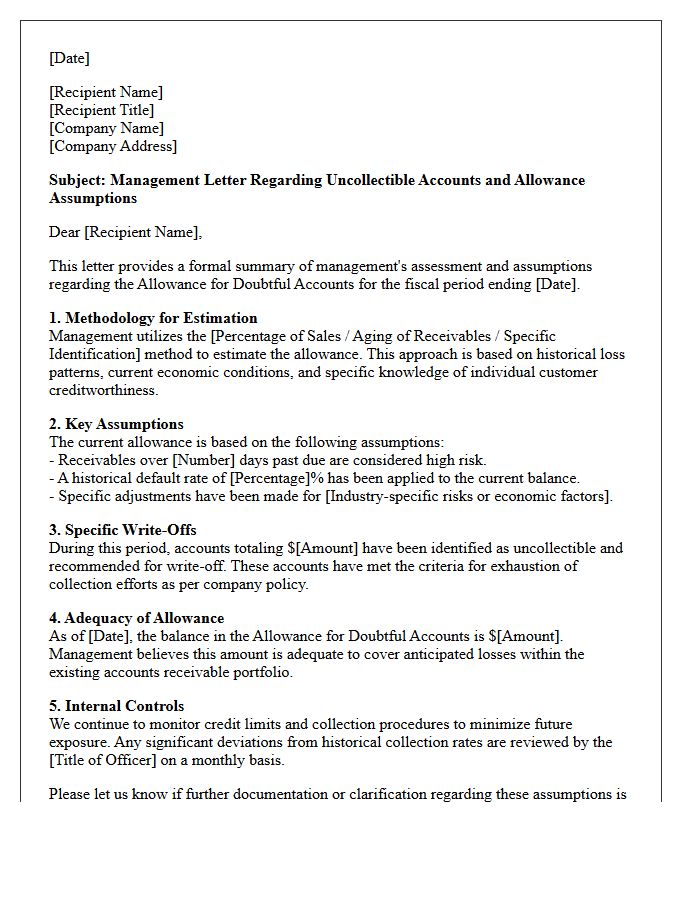

Management Letter on Uncollectible Accounts and Allowance Assumptions

A management letter regarding uncollectible accounts evaluates the reasonableness of allowance assumptions used to estimate bad debt. It focuses on the methodology for assessing credit risk and the adequacy of the allowance for doubtful accounts relative to historical trends. Auditors use this document to highlight potential weaknesses in internal controls and suggest improvements for receivables valuation. Accurate estimations are critical for ensuring that financial statements reflect the net realizable value of assets, preventing material misstatements caused by overly optimistic or outdated collection expectations.

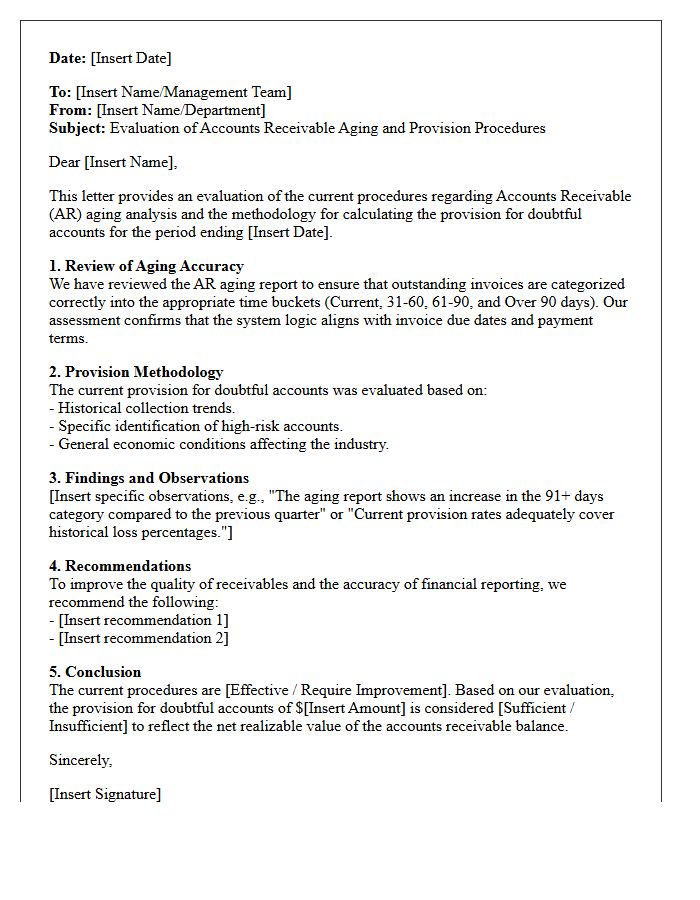

Evaluation Letter of Accounts Receivable Aging and Provision Procedures

An Accounts Receivable Aging report is a vital financial tool used to assess the liquidity of outstanding invoices. It categorizes balances by time elapsed, helping management identify overdue accounts and potential credit risks. This evaluation facilitates precise Provision Procedures, ensuring that the Allowance for Doubtful Accounts accurately reflects expected losses. By analyzing these trends, companies maintain realistic asset valuations on their balance sheets and optimize collection strategies, which is essential for preserving healthy cash flow and ensuring long-term financial stability.

What is the purpose of a management letter regarding accounts receivable aging?

The management letter serves as a formal communication from auditors to company leadership, identifying internal control weaknesses in the accounts receivable process and providing recommendations to improve the accuracy of aging reports and collection efficiency.

How does an accounts receivable aging report influence the allowance for doubtful accounts?

An aging report categorizes outstanding invoices by the length of time they have remained unpaid; management uses these time buckets to apply historical loss percentages, which directly calculates the required reserve for the allowance for doubtful accounts.

What are the common audit findings related to the allowance for doubtful accounts?

Common findings include inconsistent methodologies for estimating bad debt, failure to update historical loss rates to reflect current economic conditions, and inadequate documentation for why specific large, overdue balances were not written off.

Why should management perform a periodic review of the accounts receivable aging schedule?

Periodic reviews ensure that disputed invoices are identified early, credit limits are adjusted for high-risk customers, and the financial statements accurately reflect the net realizable value of the company's receivables.

What internal controls improve the reliability of accounts receivable valuations?

Reliability is improved through the segregation of duties between credit approval and billing, monthly reconciliation of the sub-ledger to the general ledger, and a formal approval process for all manual adjustments to the allowance for doubtful accounts.

Comments