This article provides a comprehensive guide on drafting a professional Management Letter on Deferred Revenue Amortization Schedules. It explains how to document recognition policies, ensure compliance with accounting standards, and maintain accurate financial reporting for unearned income. Effective communication helps auditors and stakeholders understand revenue timing and schedule accuracy. To simplify your documentation process, below are some ready to use template.

Image cover: Mastering Deferred Revenue: Amortization Schedule Management Templates and Best Practices

Letter Samples List

- Management Letter on Deferred Revenue Amortization Schedules

- Audit Findings Letter Regarding Deferred Revenue Amortization Schedules

- Internal Control Advisory Letter on Deferred Revenue Amortization Schedules

- Compliance Letter for Deferred Revenue Amortization Schedule Accuracy

- Significant Deficiency Letter on Deferred Revenue Amortization Schedules

- Post-Audit Management Letter Addressing Deferred Revenue Amortization Schedules

- Interim Audit Letter on Deferred Revenue Amortization Schedule Reconciliations

- Management Letter on Revenue Recognition Compliance for Deferred Revenue Amortization Schedules

- Process Improvement Letter for Deferred Revenue Amortization Schedules

- Material Weakness Letter Regarding Deferred Revenue Amortization Schedules

- System Controls Letter for Deferred Revenue Amortization Schedules

- Final Audit Communication Letter on Deferred Revenue Amortization Schedules

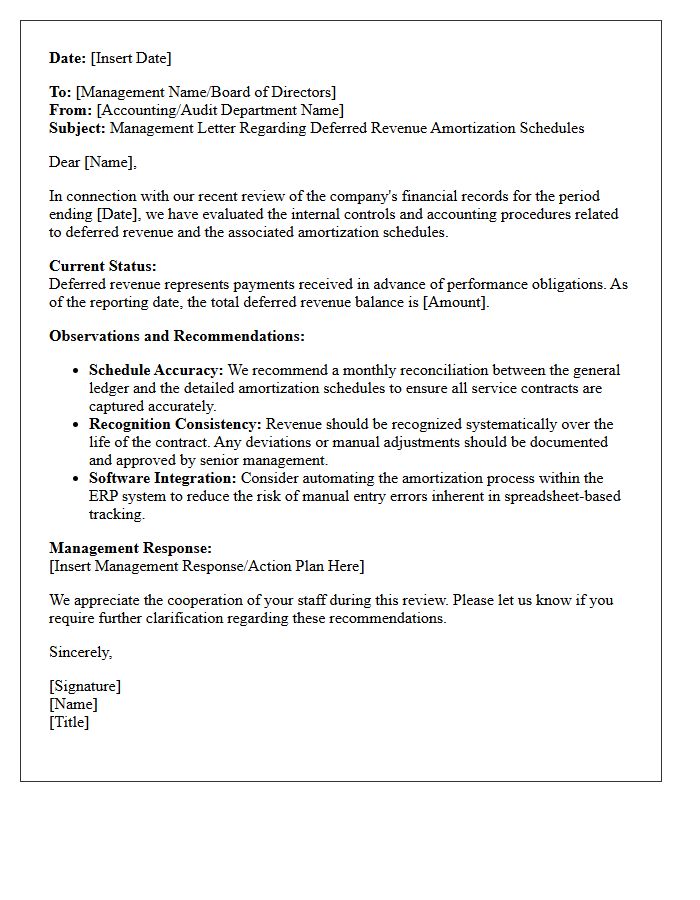

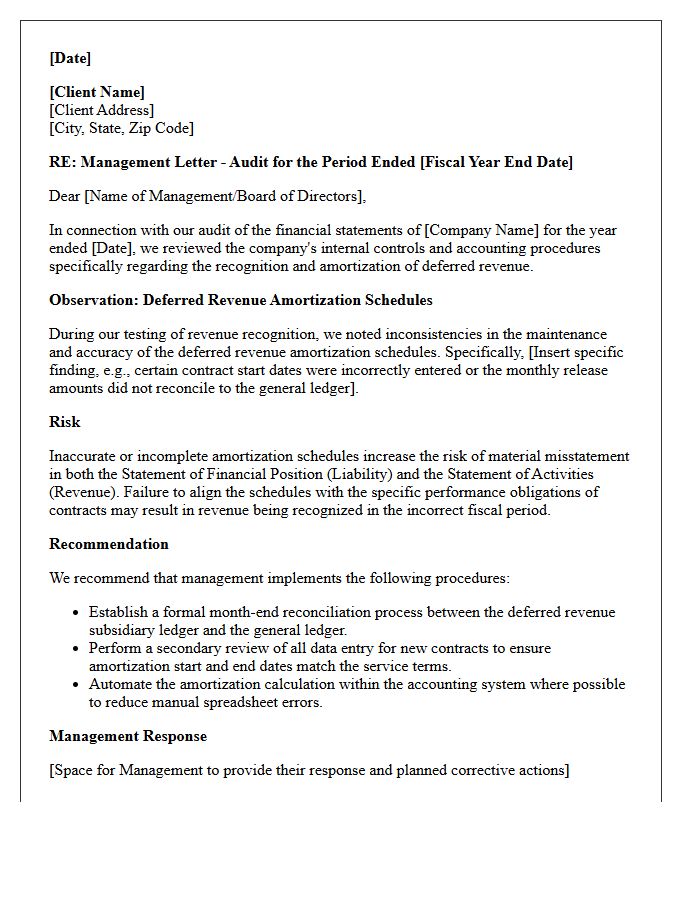

Management Letter on Deferred Revenue Amortization Schedules

A management letter regarding deferred revenue amortization schedules ensures financial reporting accuracy by validating revenue recognition timing. It addresses the critical alignment between performance obligations and contractual periods to prevent material misstatements. Auditors evaluate the reliability of calculations and internal controls governing the matching principle. Effective oversight minimizes audit risk, confirming that income is recorded only when earned. This formal communication highlights necessary adjustments to schedules, ensuring transparency for stakeholders and compliance with accounting standards like ASC 606 or IFRS 15.

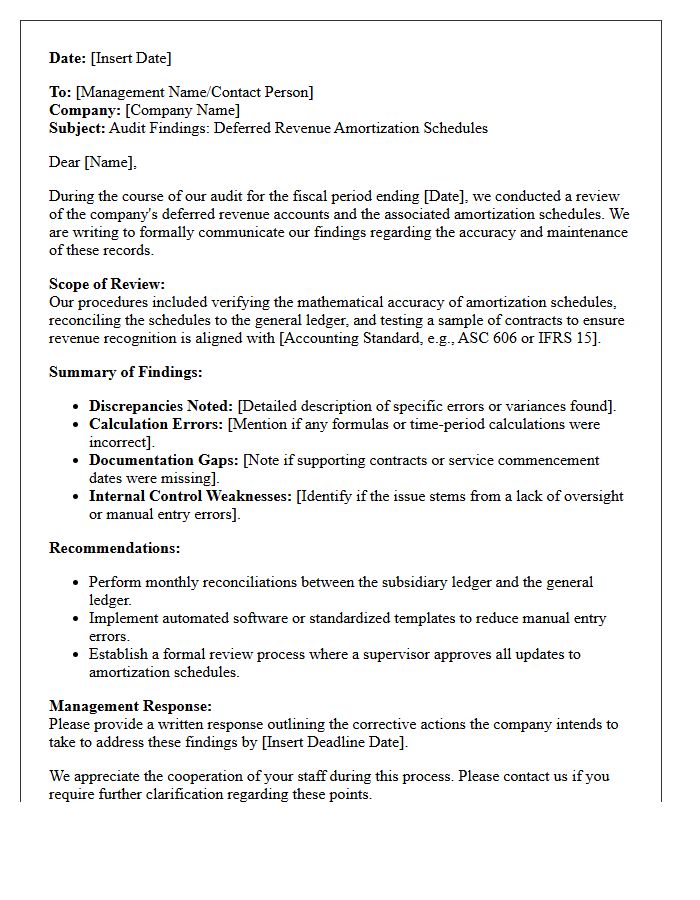

Audit Findings Letter Regarding Deferred Revenue Amortization Schedules

An Audit Findings Letter addresses discrepancies in deferred revenue amortization schedules, ensuring compliance with ASC 606 standards. Auditors scrutinize the recognition timing to prevent premature income reporting. Key issues often include mathematical errors, inconsistent service periods, or misalignment between contract terms and ledger entries. Addressing these findings is crucial for maintaining financial statement accuracy and internal control integrity. Companies must provide corrective action plans to justify revenue deferral methodologies and ensure that future performance obligations are valued correctly according to professional accounting frameworks.

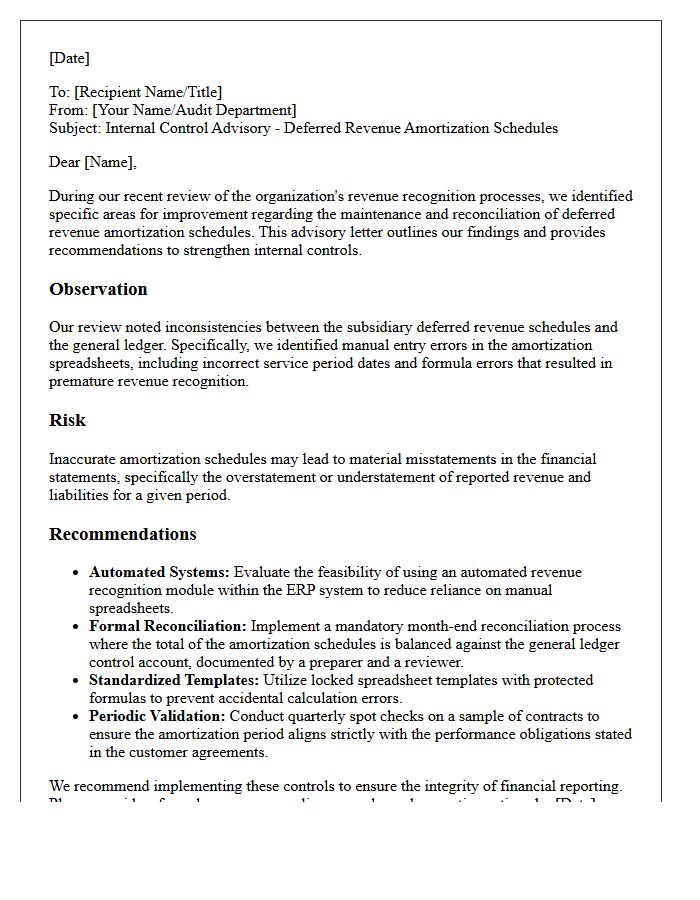

Internal Control Advisory Letter on Deferred Revenue Amortization Schedules

An Internal Control Advisory Letter regarding deferred revenue amortization schedules identifies risks in financial reporting accuracy. It highlights deficiencies where improper calculations or inconsistent recognition periods lead to misstated earnings. To ensure compliance with accounting standards, organizations must maintain rigorous reconciliation procedures and automated tracking systems. Strengthening these controls prevents manual entry errors and ensures that revenue is recognized only when earned, protecting the integrity of the financial statements and providing management with reliable data for strategic decision-making.

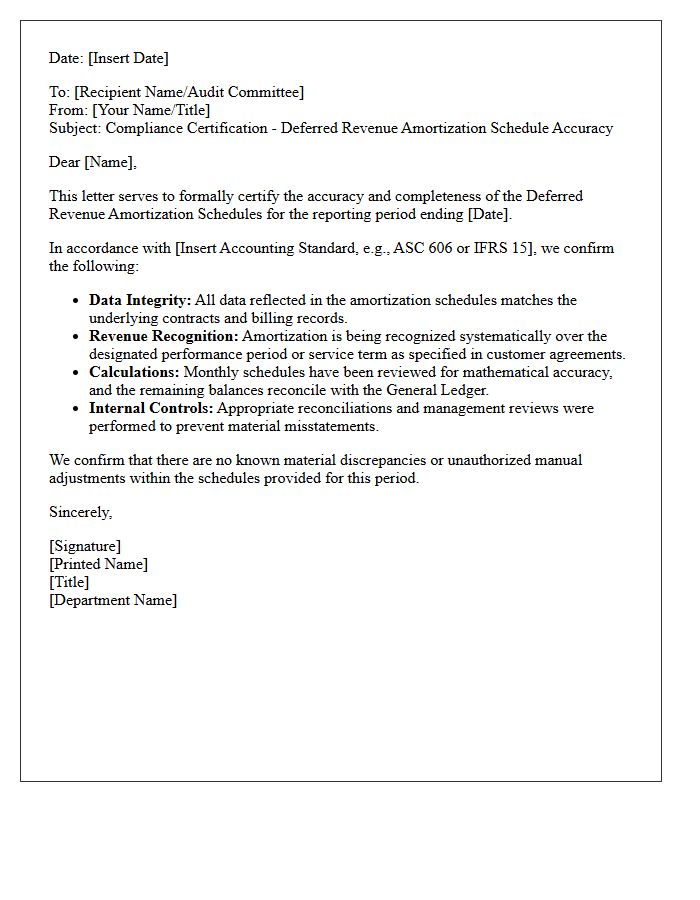

Compliance Letter for Deferred Revenue Amortization Schedule Accuracy

A compliance letter serves as formal certification that a company's deferred revenue amortization reflects accurate performance obligations. It ensures that income recognition aligns with GAAP or IFRS 15 standards, preventing financial misstatement. Auditors use this document to verify that the amortization schedule precisely matches delivery timelines and contractual terms. Maintaining this accuracy is vital for financial transparency, stakeholder trust, and passing annual audits without discrepancies. Key focus areas include verifying opening balances, recognizing periodic adjustments, and confirming that unearned fees are properly classified on the balance sheet.

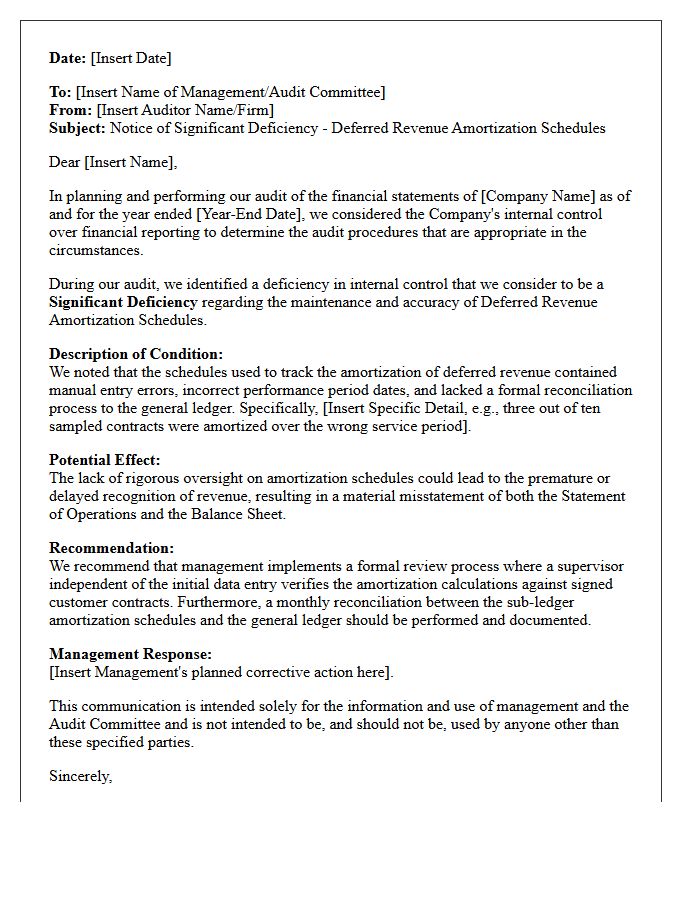

Significant Deficiency Letter on Deferred Revenue Amortization Schedules

A significant deficiency letter regarding deferred revenue amortization schedules alerts management to internal control weaknesses. It typically highlights inaccurate recognition periods or spreadsheet errors that risk misstating financial statements. Addressing this requires reconciling deferred balances to underlying contracts and implementing automated tracking. Proper oversight ensures revenue aligns with performance obligations under ASC 606 standards, preventing audit adjustments and improving reporting integrity. Timely remediation is essential to strengthen the control environment and maintain stakeholder confidence in the company's financial health.

Post-Audit Management Letter Addressing Deferred Revenue Amortization Schedules

A post-audit management letter regarding deferred revenue amortization schedules highlights critical internal control improvements. It focuses on ensuring that unearned income is recognized over the correct accounting period in compliance with revenue recognition standards like ASC 606. Accurate schedules prevent material misstatements by aligning cash receipts with performance obligations. Auditors use these letters to recommend systematic tracking tools, reducing manual entry errors and ensuring financial statement accuracy. Proper management of these schedules is essential for maintaining stakeholder trust and ensuring long-term audit compliance through robust revenue lifecycle oversight.

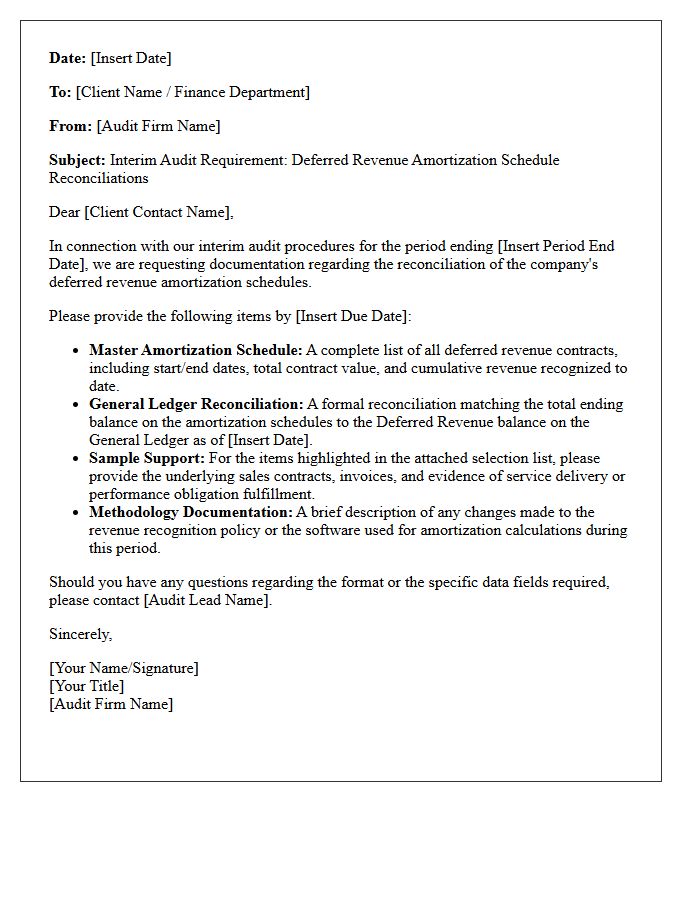

Interim Audit Letter on Deferred Revenue Amortization Schedule Reconciliations

An interim audit letter regarding deferred revenue amortization schedule reconciliations ensures accuracy in recognizing income over time. It verifies that the contract liabilities recorded on the balance sheet align perfectly with the revenue recognized in the income statement. Auditors perform this early review to identify reconciliation discrepancies or timing errors before year-end. This process mitigates risks of financial misstatement by validating revenue recognition policies against performance obligations. Ensuring these schedules are reconciled regularly maintains audit readiness and confirms that deferred balances accurately reflect future service obligations under accounting standards.

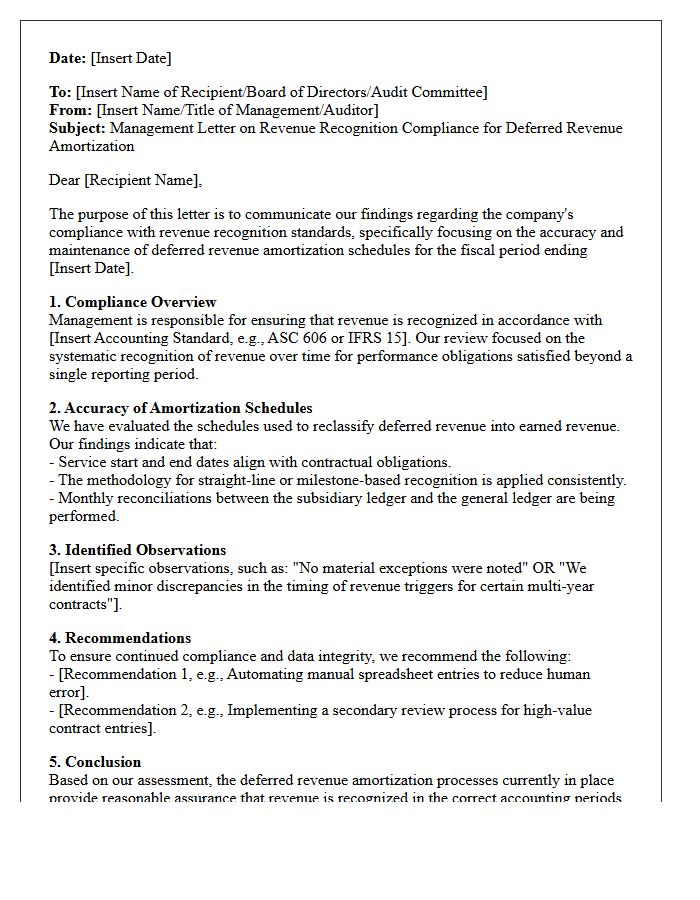

Management Letter on Revenue Recognition Compliance for Deferred Revenue Amortization Schedules

A management letter regarding revenue recognition compliance ensures that deferred revenue amortization schedules strictly align with ASC 606 or IFRS 15 standards. It identifies internal control weaknesses and verifies that performance obligations are satisfied before income is recognized. Accurate schedules prevent material misstatements by documenting the systematic release of liabilities over time. This formal communication highlights the importance of matching revenue with the delivery of services, ensuring financial transparency and regulatory adherence for stakeholders and auditors.

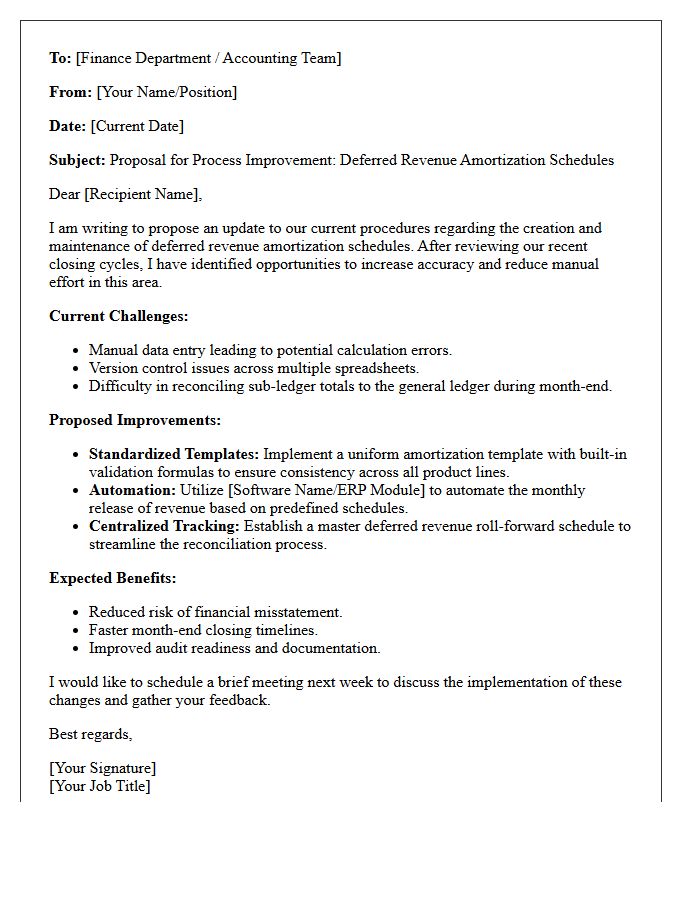

Process Improvement Letter for Deferred Revenue Amortization Schedules

A process improvement letter for deferred revenue amortization schedules focuses on enhancing financial accuracy and audit readiness. It identifies weaknesses in manual tracking, such as spreadsheet errors or timing discrepancies, and recommends automation to streamline revenue recognition. By implementing standardized templates or integrated software, organizations ensure compliance with ASC 606 standards, reduce period-end closing times, and provide a clear audit trail. This formal communication helps management mitigate risks related to overstated liabilities or incorrectly recognized income, ultimately strengthening the company's internal control environment.

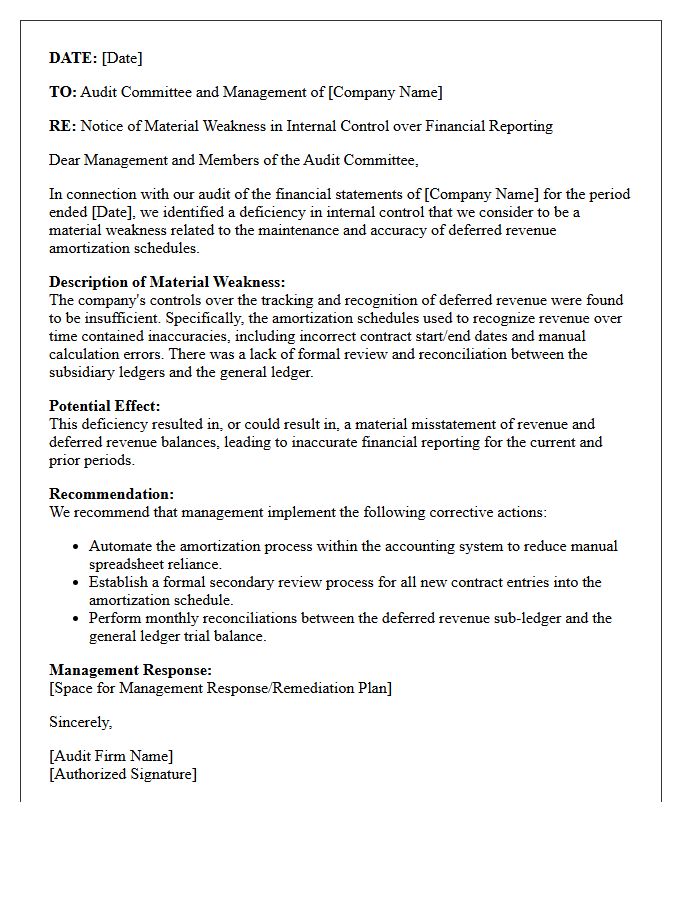

Material Weakness Letter Regarding Deferred Revenue Amortization Schedules

A material weakness letter identifies severe internal control deficiencies in financial reporting. Regarding deferred revenue amortization schedules, this typically signifies systemic errors in revenue recognition timing or calculations. Such findings indicate that the company's systems cannot prevent or detect material misstatements, potentially leading to restated earnings. Stakeholders must address these audit findings by implementing robust automated tracking, enhancing data integrity, and ensuring strict compliance with accounting standards to restore financial transparency and investor confidence in reported deferred revenue balances.

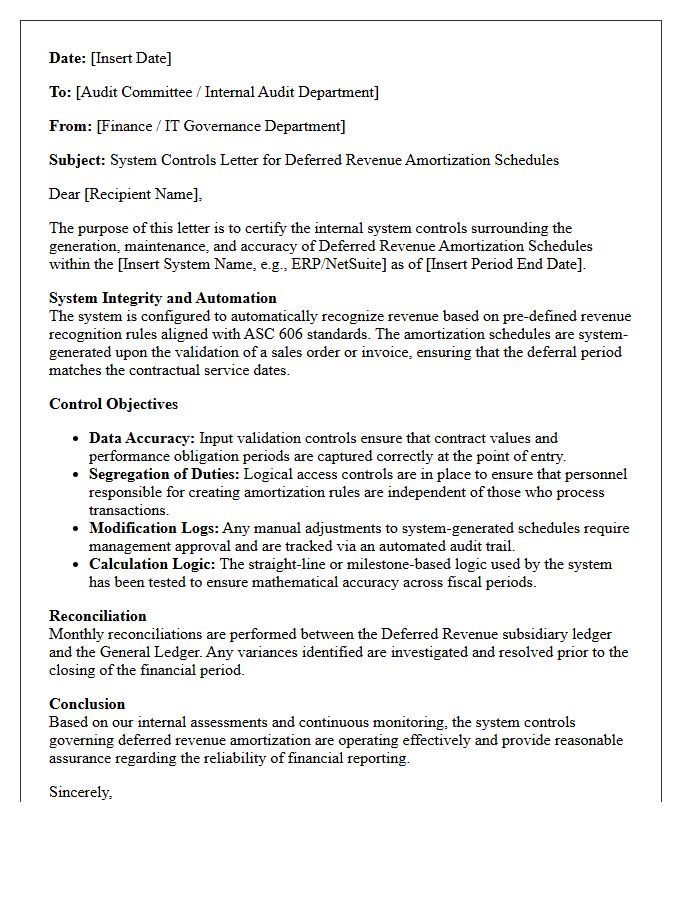

System Controls Letter for Deferred Revenue Amortization Schedules

The System Controls Letter is a vital document used to manage and authorize the Deferred Revenue Amortization Schedules within financial systems. It serves as a formal instruction to establish specific accounting parameters, ensuring that unearned income is recognized accurately over time. This control mechanism maintains compliance with revenue recognition standards by defining the start dates, durations, and calculation methods for each schedule. By implementing these rigorous system controls, organizations prevent manual errors, ensure financial integrity, and provide a clear audit trail for deferred revenue adjustments.

Final Audit Communication Letter on Deferred Revenue Amortization Schedules

The Final Audit Communication Letter serves as the definitive record of findings regarding your deferred revenue amortization schedules. This document verifies that income recognition aligns with accounting standards like ASC 606 or IFRS 15. It highlights any identified discrepancies in timing, calculation errors, or internal control weaknesses. Ensuring these schedules are accurate is critical for maintaining financial integrity, as they directly impact reported earnings and liability valuations. Management must review this letter to address outstanding adjustments and strengthen reporting transparency for stakeholders and regulatory compliance.

What is a management letter regarding deferred revenue amortization?

A management letter on deferred revenue amortization is a formal document issued by auditors that evaluates the internal controls, accuracy, and compliance of how a company recognizes income over time for services or products already invoiced but not yet delivered.

Why are accurate amortization schedules essential for deferred revenue?

Accurate schedules ensure that revenue is recognized in the correct accounting period according to GAAP or IFRS standards, preventing the misstatement of liabilities on the balance sheet and ensuring the integrity of the income statement.

What common deficiencies are identified in management letters for revenue deferral?

Common findings include manual calculation errors in spreadsheets, lack of reconciliation between the sub-ledger and the general ledger, and inconsistent application of performance obligation milestones under ASC 606 or IFRS 15.

How can a company improve its internal controls for deferred revenue reporting?

Companies can improve controls by implementing automated revenue recognition software, performing monthly roll-forward analyses, and establishing a secondary review process for high-value contract entries to verify amortization start and end dates.

What impact does an audit finding on amortization schedules have on financial statements?

Significant findings may lead to adjustments that decrease current period earnings if revenue was recognized too aggressively, or increase liabilities if the amortization period was calculated incorrectly, potentially impacting investor confidence and loan covenants.

Comments