Effective financial oversight requires accurate Capital Expenditure Tracking and strict adherence to asset capitalization policies. This article explores essential internal controls, reporting standards, and documentation practices needed to maintain compliance and ensure balance sheet integrity. Mastering these processes minimizes audit risks and optimizes long-term asset management. To help you get started, below are some ready to use template.

Image cover: Best Practices for Capital Expenditure Tracking and Fixed Asset Capitalization: Reporting Templates and Audit Samples

Letter Samples List

- Official Letterhead Of The Accounting Firm

- Date And Addressee Of The Management Letter

- Introduction To The Capital Expenditure Management Letter

- Scope Of Fixed Asset And Capitalization Review

- Executive Summary Of Letter Findings

- Observation On Deficient Capital Expenditure Tracking

- Observation On Delayed Fixed Asset Capitalization

- Risk Assessment Outlined In The Management Letter

- Letter Recommendation For Tracking System Implementation

- Letter Recommendation For Capitalization Policy Update

- Client Management Response To The Letter

- Remediation Timeline For Letter Recommendations

- Concluding Signatures Of The Accounting Firm Letter

Official Letterhead Of The Accounting Firm

An official letterhead of an accounting firm serves as a critical tool for establishing professional credibility and legal validity. It must clearly display the firm's legal name, registered office address, and contact details. For many jurisdictions, including regulatory compliance identifiers like CPA or ICAEW designations is mandatory. This document ensures that financial statements, audit reports, and tax filings are recognized as authoritative records. Using a consistent, well-designed letterhead reinforces brand trust while providing essential transparency for clients, stakeholders, and government authorities during official correspondence.

Date And Addressee Of The Management Letter

The Management Letter must be dated as close to the audit report date as possible, but never after. This ensures that management's representations cover all transactions up to the point of the auditor's signature. It is formally addressed to the Board of Directors or those charged with governance, rather than individual employees. This specific timing and addressee structure establishes legal accountability and confirms that the financial statements reflect all subsequent events known to the organization's highest leadership levels before final issuance.

Introduction To The Capital Expenditure Management Letter

The Capital Expenditure Management Letter is a formal document used to propose and justify significant investments in long-term assets. It outlines the strategic necessity, financial implications, and expected return on investment for major purchases. By providing a clear cost-benefit analysis, this letter helps stakeholders make informed decisions regarding budget allocation. Its primary goal is to ensure that every capital outlay aligns with the organization's long-term growth objectives while maintaining fiscal responsibility and operational efficiency.

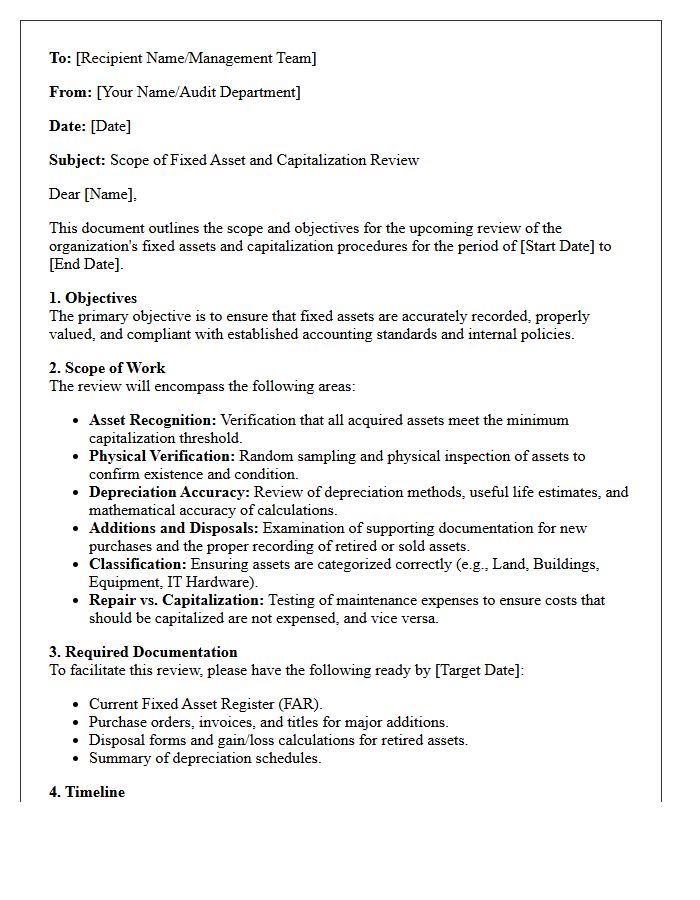

Scope Of Fixed Asset And Capitalization Review

A Fixed Asset and Capitalization Review ensures financial accuracy by verifying the existence, valuation, and classification of long-term resources. The scope typically involves evaluating expenditure thresholds to determine if costs should be recorded as assets or immediate expenses. It includes auditing depreciation methods, useful life estimates, and disposal records to maintain regulatory compliance. This process identifies internal control weaknesses, prevents balance sheet misstatements, and optimizes tax benefits. Understanding these parameters is essential for precise financial reporting and effective resource management within any organization.

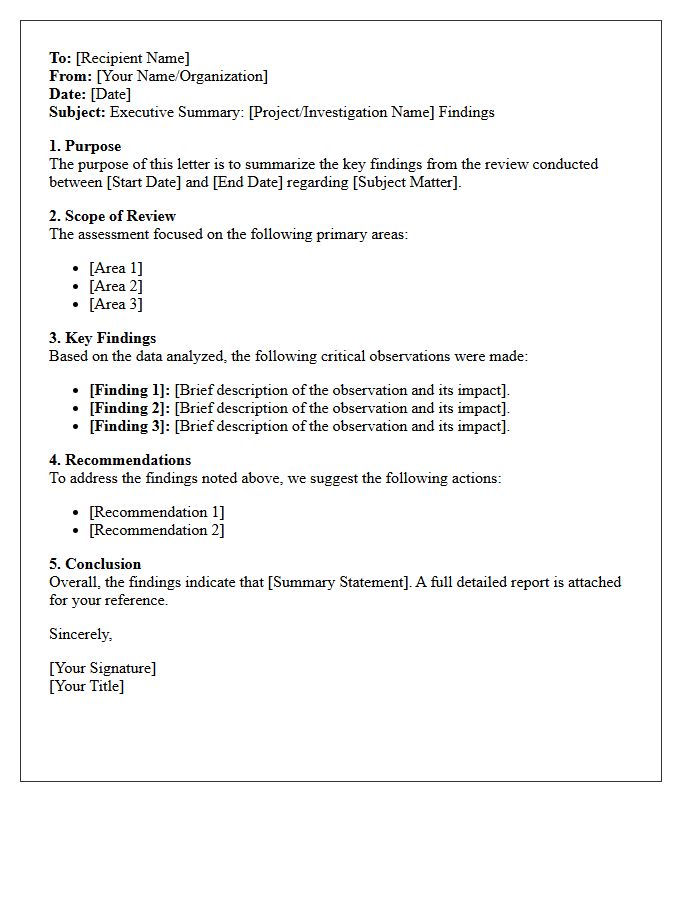

Executive Summary Of Letter Findings

An Executive Summary of Letter Findings provides a concise overview of critical discoveries identified during an investigation or audit. It distills complex data into actionable insights, highlighting compliance issues, risks, and necessary corrective measures. This high-level synthesis ensures decision-makers quickly grasp the primary conclusions without reviewing lengthy documentation. By focusing on material evidence and strategic recommendations, the summary facilitates informed governance and timely resolution of outstanding concerns.

Observation On Deficient Capital Expenditure Tracking

Inefficient capital expenditure tracking often leads to severe budget overruns and misallocated resources. Organizations must prioritize real-time visibility to monitor asset acquisition and project lifecycles accurately. Without precise data, stakeholders cannot evaluate the long-term return on investment or ensure compliance with financial regulations. Establishing robust monitoring protocols is essential to prevent capital leakage and improve strategic decision-making. Proper oversight ensures that every dollar spent aligns with corporate objectives, turning potential financial risks into measurable growth opportunities through disciplined fiscal management and accountability.

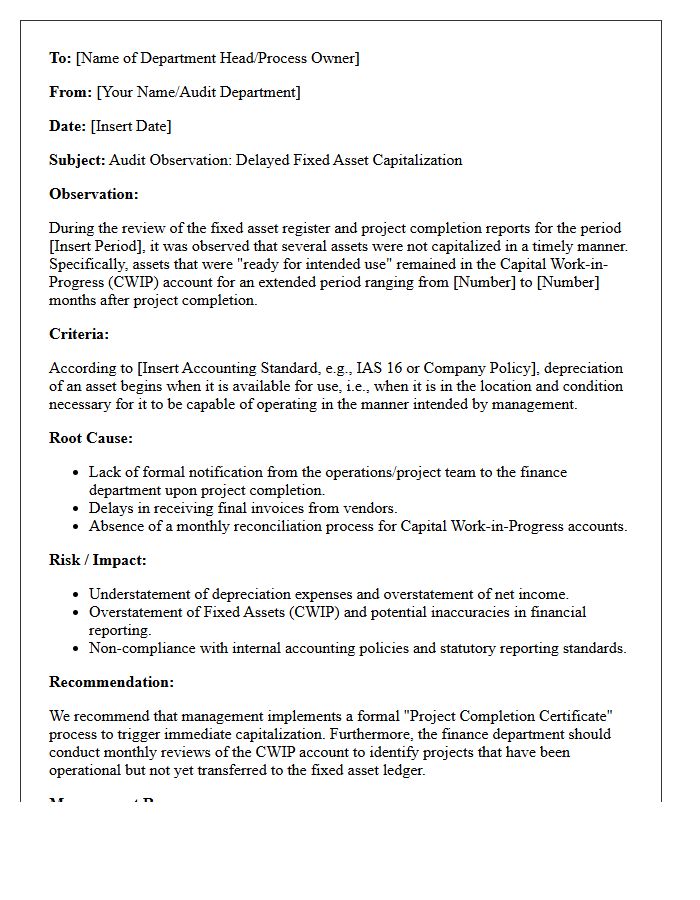

Observation On Delayed Fixed Asset Capitalization

The delayed fixed asset capitalization occurs when a company fails to record a completed asset on its balance sheet promptly. This timing mismatch often leads to understated depreciation expenses and inflated net income figures, which can trigger significant audit risks. Proper oversight ensures that assets transition from "Construction in Progress" to "Fixed Assets" exactly when they become ready for their intended use. Accurate timing is essential for maintaining regulatory compliance, ensuring reliable financial reporting, and accurately reflecting the true operational costs of the business over time.

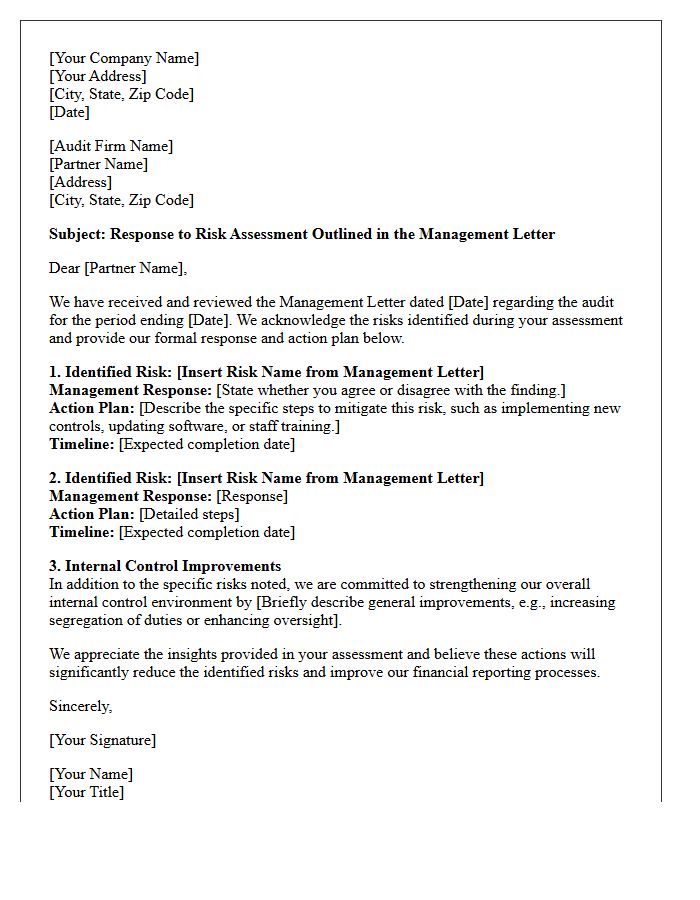

Risk Assessment Outlined In The Management Letter

A risk assessment outlined in the management letter identifies internal control weaknesses observed during an audit. This document communicates specific operational vulnerabilities and financial reporting risks to senior management and those charged with governance. By highlighting these gaps, auditors provide actionable recommendations to mitigate potential fraud or errors. Understanding these findings is essential for strengthening organizational resilience and ensuring long-term compliance. Addressing these points promptly helps protect assets and enhances the overall reliability of a company's financial oversight processes.

Letter Recommendation For Tracking System Implementation

A formal Letter of Recommendation for tracking system implementation must emphasize operational efficiency and technical compatibility. It should highlight the software's ability to provide real-time data, improve workflow transparency, and ensure accurate resource monitoring. Focus on how the system streamlines logistics management and enhances team accountability. Including specific metrics regarding time saved or error reduction demonstrates the strategic value of the integration. A well-structured endorsement serves as a professional validation, ensuring stakeholders understand the return on investment and long-term scalability of the proposed tracking solution.

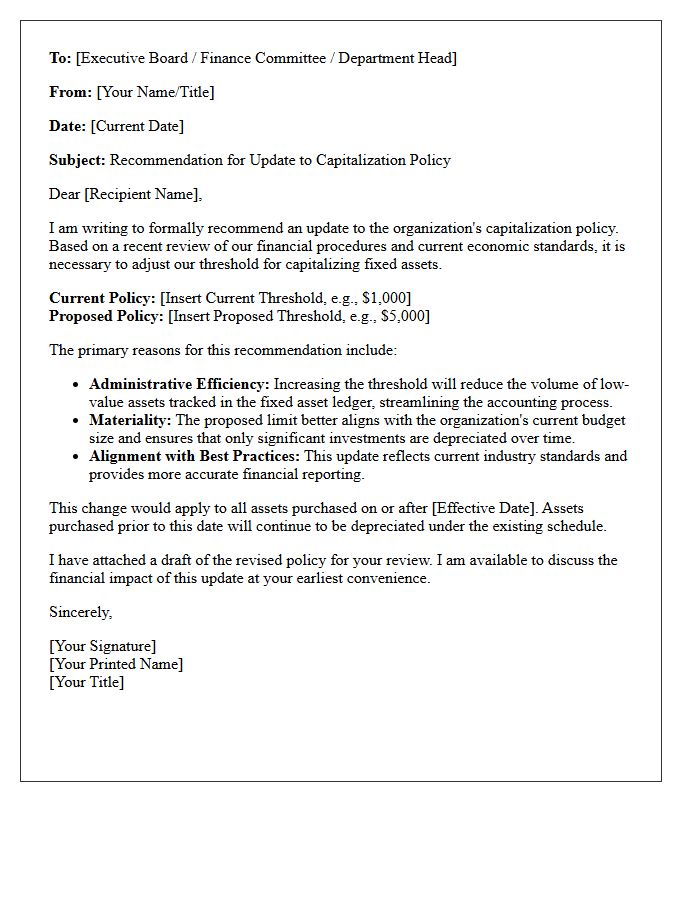

Letter Recommendation For Capitalization Policy Update

A letter recommendation for a capitalization policy update justifies raising the threshold for recording fixed assets. It explains how increasing the dollar limit reduces administrative burdens and simplifies financial reporting. The proposal should outline the impact on depreciation and clarify which expenditures will be expensed immediately versus capitalized. Providing a clear cost-benefit analysis ensures stakeholders understand how the change aligns with current economic conditions and organizational growth, ultimately improving long-term accounting efficiency and ensuring compliance with regulatory standards.

Client Management Response To The Letter

A management response letter serves as a formal reply to audit findings or consultancy recommendations. It is crucial to address each identified risk with a clear action plan, specified timelines, and assigned accountability. This document demonstrates management's commitment to internal controls and operational improvements. To ensure effectiveness, the response must be objective, evidence-based, and focused on remediation strategies. Properly articulating these steps builds stakeholder trust and ensures that organizational weaknesses are systematically mitigated, reflecting a proactive approach to corporate governance and professional accountability.

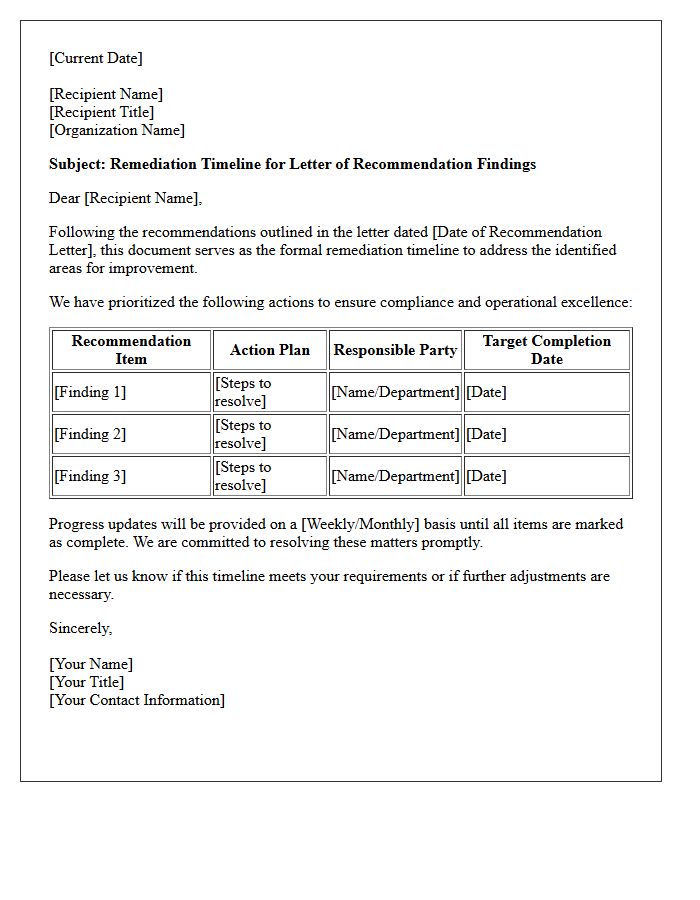

Remediation Timeline For Letter Recommendations

The remediation timeline for recommendation letters depends on institutional deadlines and specific program requirements. Generally, students should request revisions four to six weeks before the application due date to allow faculty sufficient time. If a letter requires corrections due to errors or updated information, aim for a ten-day turnaround to ensure all documents remain synchronized. Proactive communication and providing clear submission instructions are essential to prevent delays. Staying ahead of these benchmarks ensures that your professional portfolio remains competitive and complete throughout the academic or employment application cycle.

Concluding Signatures Of The Accounting Firm Letter

The concluding signatures of an accounting firm letter serve as a formal authentication of the document's contents. This section typically includes the professional signature of the lead partner, the firm's legal name, and the specific date of issuance. These elements establish legal accountability and confirm that the engagement complied with relevant auditing standards. A valid signature ensures the report is legally binding, providing stakeholders with assurance regarding the financial statements' credibility and the firm's professional endorsement of the disclosed data.

What is a management letter regarding capital expenditure tracking?

A management letter is a formal communication from auditors to senior leadership that identifies internal control weaknesses in how an organization monitors, approves, and records capital expenditures (CapEx) compared to its budget.

What are the primary criteria for fixed asset capitalization?

Fixed asset capitalization occurs when a purchase meets the organization's minimum cost threshold (capitalization limit) and provides a future economic benefit extending beyond one fiscal year, such as equipment, buildings, or infrastructure.

How does a management letter address deficiencies in CapEx tracking?

The letter typically highlights issues such as budget overruns, lack of competitive bidding, or failure to distinguish between repairs (expenses) and improvements (capitalized assets), providing recommendations for stronger oversight and reconciliation.

Why is timely capitalization of fixed assets critical for financial reporting?

Promptly moving items from Construction-in-Progress (CIP) to "Placed in Service" status ensures that depreciation expense begins correctly, preventing the overstatement of asset values and ensuring compliance with GAAP or IFRS standards.

What internal controls should be implemented for fixed asset management?

Effective controls include maintaining a centralized fixed asset register, performing periodic physical inventory counts, ensuring proper segregation of duties between procurement and recording, and enforcing strict authorization workflows for all capital projects.

Comments