A Management Letter addressing post-merger financial integration deficiencies identifies critical gaps in reporting, internal controls, and data consolidation after a merger. This document helps leadership mitigate operational risks and align accounting policies across the new entity. Ensuring seamless fiscal synchronization is vital for long-term corporate stability. To assist your reporting process, below are some ready to use template.

Image cover: Mastering the Post-Merger Financial Integration Audit: Management Letter Templates and Reporting Samples

Letter Samples List

- Management Letter on Incomplete Chart of Accounts Harmonization

- Management Letter Highlighting Deficiencies in ERP System Consolidation

- Letter Detailing Material Weaknesses in Post-Merger Internal Controls

- Management Letter on Unreconciled Intercompany Balances and Transactions

- Letter Regarding Deficiencies in Acquired Asset Valuation and Impairment

- Management Letter Addressing Inconsistent Revenue Recognition Policies

- Letter Noting Deficiencies in Legacy Financial Data Migration

- Management Letter on Inadequate Segregation of Duties Following Integration

- Letter of Findings on Consolidated Statutory Reporting Delays

- Management Letter Regarding Undisclosed Post-Merger Tax Compliance Liabilities

- Letter Outlining Deficiencies in Combined Treasury and Cash Management

- Management Letter on Insufficient Cross-Training Within Merged Finance Departments

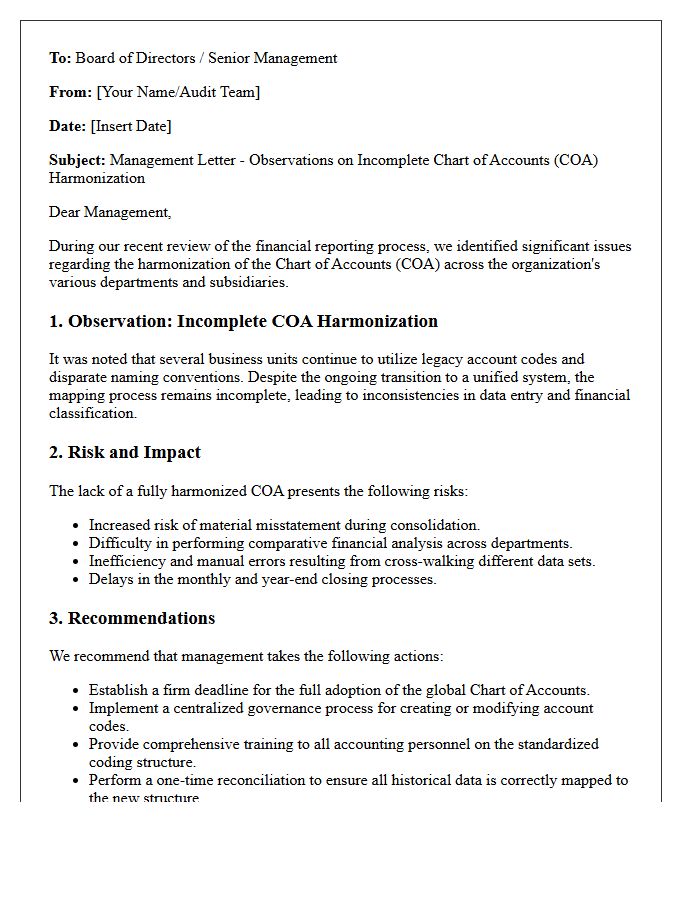

Management Letter on Incomplete Chart of Accounts Harmonization

A management letter regarding incomplete chart of accounts harmonization warns stakeholders about financial reporting risks. When ledger structures remain inconsistent across departments, it hinders data consolidation and accurate auditing. This document highlights internal control weaknesses that lead to reconciliation errors and manual adjustments. Achieving a unified framework is essential for regulatory compliance, operational efficiency, and transparent fiscal oversight. Organizations must prioritize standardized coding to ensure reliable financial statements and informed strategic decision-making.

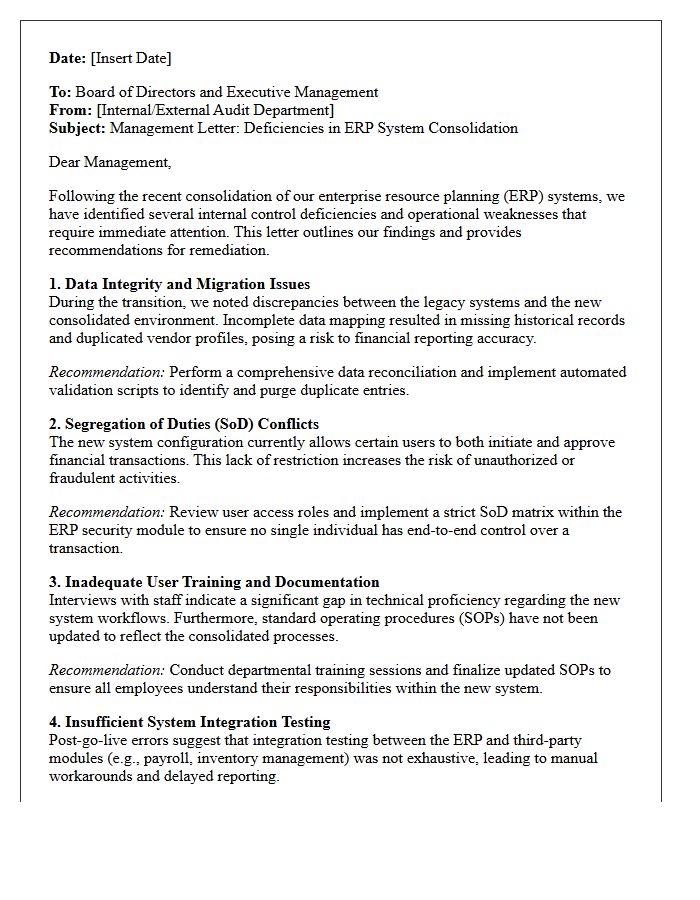

Management Letter Highlighting Deficiencies in ERP System Consolidation

A management letter identifies critical control gaps following ERP system consolidation. During the merger of disparate platforms, data migration errors or inconsistent workflows often create financial reporting risks. This document outlines specific internal control deficiencies, such as inadequate user access reviews or failed automated reconciliations. Addressing these observations is essential for ensuring data integrity and regulatory compliance. Management must prioritize remediation efforts to strengthen the unified system architecture and prevent material misstatements within the newly integrated environment.

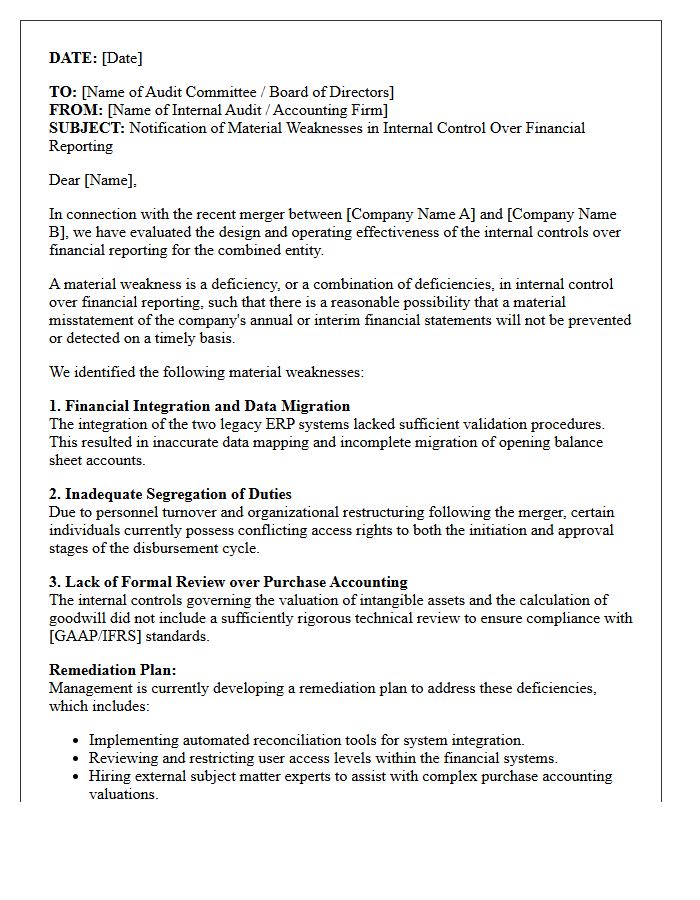

Letter Detailing Material Weaknesses in Post-Merger Internal Controls

A post-merger Letter Detailing Material Weaknesses is a critical governance document identifying severe deficiencies in the combined entity's internal reporting. It alerts stakeholders that financial misstatements are likely due to ineffective controls or integration failures. Addressing these gaps is essential for regulatory compliance and investor confidence. Management must prioritize remediation strategies to strengthen the control environment, ensuring accurate financial disclosure and mitigating operational risks during the high-stakes transition period following an acquisition.

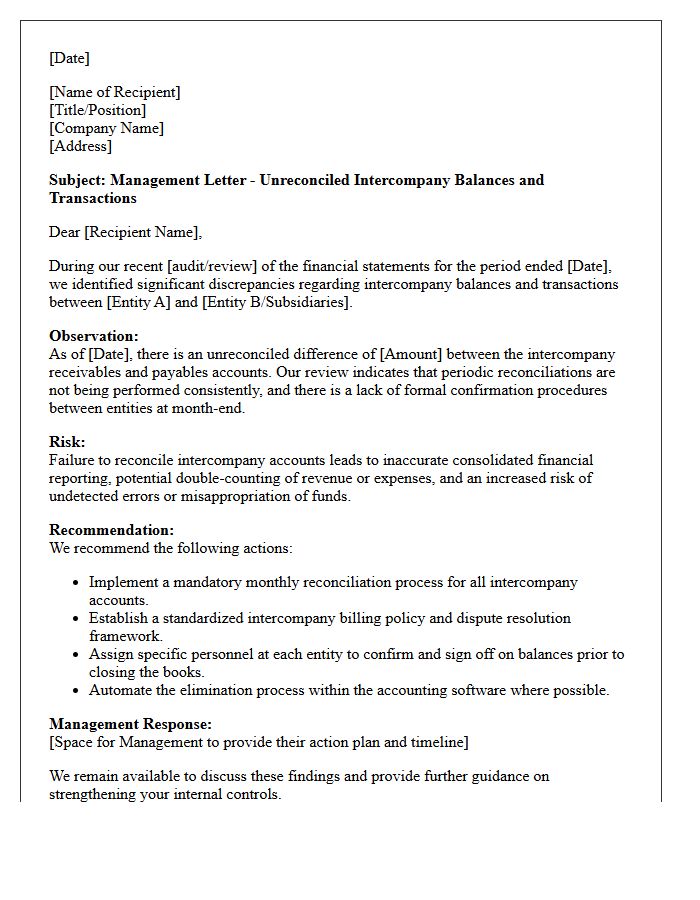

Management Letter on Unreconciled Intercompany Balances and Transactions

A management letter regarding unreconciled intercompany balances highlights critical discrepancies between related entities that can distort consolidated financial reporting. These imbalances often signal internal control weaknesses or process inefficiencies in transaction matching. Failure to resolve these differences increases the risk of financial misstatement and complicates the audit trail. Effective oversight requires rigorous monthly reconciliations and standardized accounting policies to ensure data integrity. Addressing these findings promptly is essential for maintaining accurate financial transparency and ensuring compliance with regulatory reporting standards across the entire corporate group structure.

Letter Regarding Deficiencies in Acquired Asset Valuation and Impairment

A letter regarding deficiencies in acquired asset valuation and impairment serves as a formal regulatory or audit notification. It identifies critical errors in how a company calculates the fair value of purchased assets or recognizes impairment losses when asset values decline. These letters often highlight inadequate documentation, flawed methodology, or incorrect assumptions in financial reporting. Addressing these issues is essential to ensure compliance with accounting standards, maintain financial integrity, and prevent potential legal or regulatory penalties resulting from misstated financial statements.

Management Letter Addressing Inconsistent Revenue Recognition Policies

A management letter addressing inconsistent revenue recognition policies highlights critical financial risks. It identifies deviations from accounting standards like ASC 606 or IFRS 15, which can lead to misstated earnings. The letter recommends standardizing internal controls and formalizing procedures across all business units to ensure reporting accuracy. Addressing these discrepancies is essential for maintaining investor confidence, securing audit compliance, and providing a transparent view of the company's actual performance. Timely remediation prevents future regulatory issues and strengthens the overall integrity of financial statements.

Letter Noting Deficiencies in Legacy Financial Data Migration

A Deficiency Note is a formal document issued during legacy financial data migration to identify data integrity gaps, missing records, or formatting errors. It serves as a critical audit trail, ensuring that inconsistencies between the source system and the new platform are resolved before final sign-off. Addressing these migration risks promptly prevents downstream reporting failures and maintains financial compliance. Stakeholders must review these notes to validate reconciliation accuracy and ensure that the migrated ledger balances align perfectly with historical financial statements.

Management Letter on Inadequate Segregation of Duties Following Integration

A management letter addressing inadequate segregation of duties following a corporate integration highlights critical internal control deficiencies. When systems or teams merge, overlapping responsibilities often create fraud risks and unauthorized transaction opportunities. Auditors issue these findings to mandate the separation of authorization, custody, and record-keeping functions. Organizations must implement compensating controls or reassign tasks to ensure robust financial integrity and regulatory compliance during the post-merger transition period.

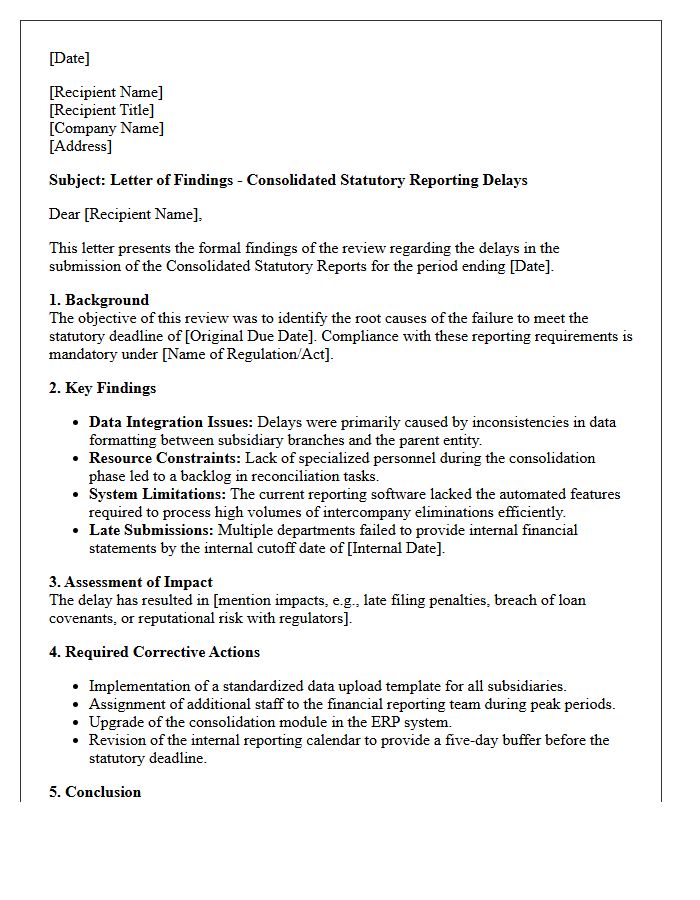

Letter of Findings on Consolidated Statutory Reporting Delays

A Letter of Findings regarding Consolidated Statutory Reporting Delays serves as a formal notification from regulators concerning failures to meet financial submission deadlines. It identifies specific compliance gaps and internal control weaknesses that hindered timely disclosures. Organizations receiving this document must address the root causes of reporting lags to avoid potential penalties. Understanding these findings is essential for improving governance frameworks and ensuring accurate, transparent data delivery to authorities. Proactive remediation helps maintain regulatory standing and prevents further enforcement actions or legal scrutiny within the financial reporting ecosystem.

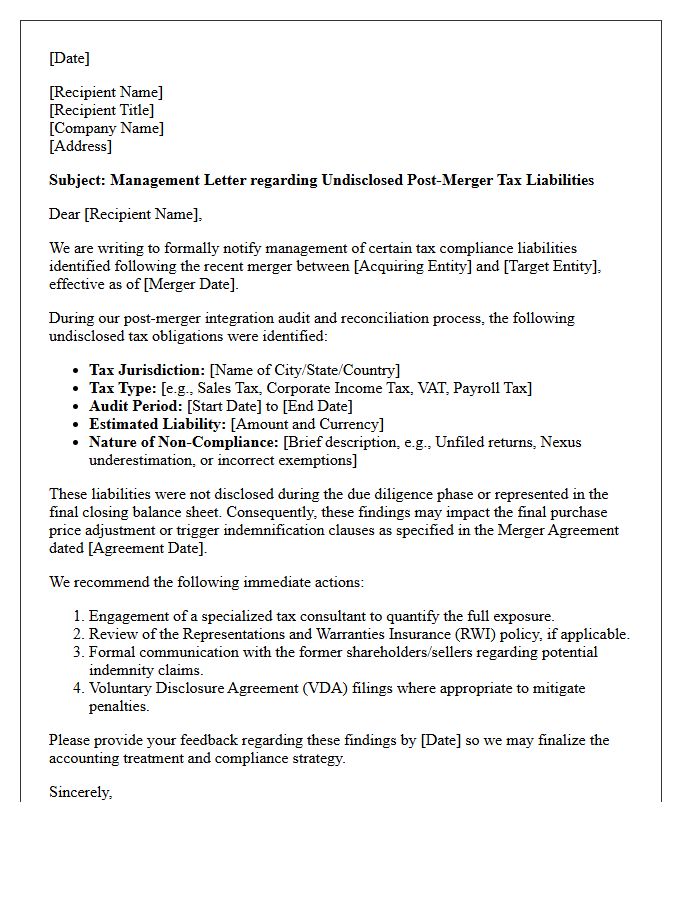

Management Letter Regarding Undisclosed Post-Merger Tax Compliance Liabilities

A management letter concerning undisclosed post-merger tax compliance liabilities serves as a formal notification of unrecorded financial obligations discovered after an acquisition. It highlights successor liability risks, where the purchasing entity becomes responsible for the target company's unpaid taxes, interest, and penalties. This document is essential for financial transparency and adjusting valuations. It outlines specific non-compliance issues, such as nexus exposure or payroll errors, ensuring that management acknowledges these risks and implements corrective actions to mitigate future legal or regulatory impacts on the merged organization's balance sheet.

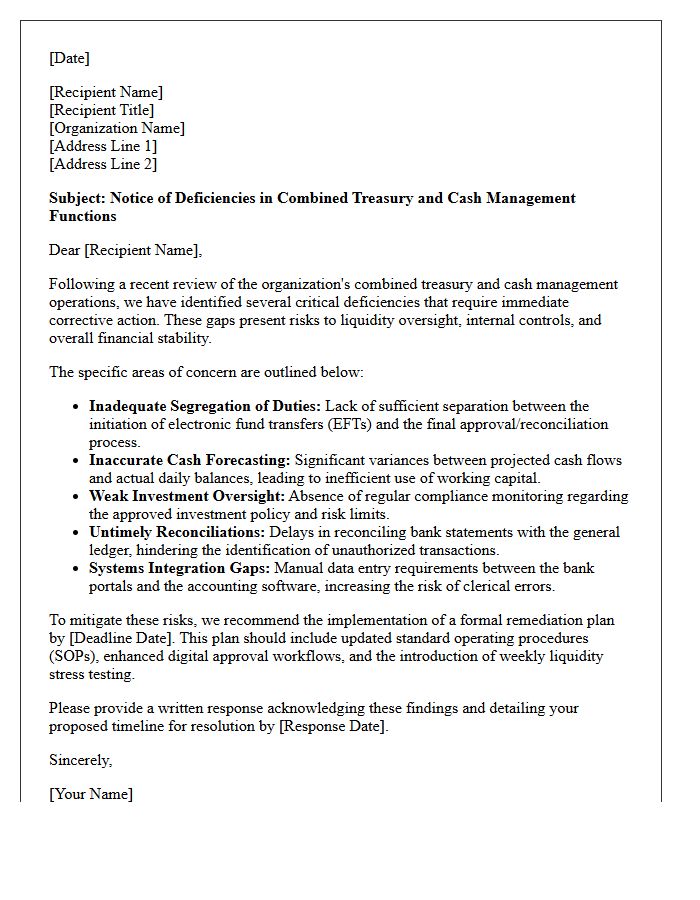

Letter Outlining Deficiencies in Combined Treasury and Cash Management

A Letter Outlining Deficiencies is a formal notification issued by auditors or regulators identifying internal control weaknesses within an organization's financial operations. This document highlights critical gaps in Treasury and Cash Management, such as inadequate segregation of duties, poor liquidity monitoring, or insufficient oversight of fund transfers. Addressing these findings is essential to mitigate financial risks, prevent fraud, and ensure accurate reporting. Organizations must implement corrective actions to strengthen their cash governance framework and maintain regulatory compliance while safeguarding institutional assets from potential loss or mismanagement.

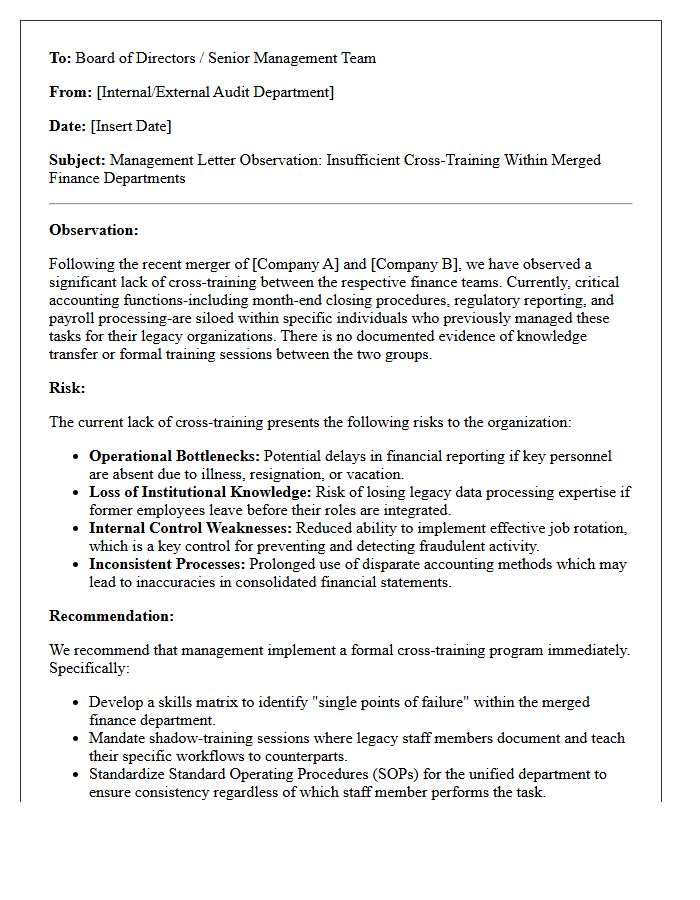

Management Letter on Insufficient Cross-Training Within Merged Finance Departments

Following a merger, a management letter frequently highlights the risk of insufficient cross-training within the consolidated finance department. When legacy teams operate in silos, the organization faces operational vulnerability and potential reporting delays if key personnel depart. Establishing a formal knowledge-sharing framework is essential to ensure business continuity and maintain internal controls. Leaders must prioritize standardized procedures to eliminate single-point-of-failure risks, ensuring that multiple staff members possess the expertise to execute critical financial tasks across the newly integrated entity.

What are the primary objectives of a Management Letter regarding post-merger financial integration?

The primary objective is to communicate identified internal control deficiencies, operational inefficiencies, and accounting inconsistencies discovered during the consolidation of two entities. It provides actionable recommendations to strengthen the control environment and ensure the accuracy of the combined financial reporting.

Which common internal control deficiencies are highlighted after a merger?

Common deficiencies include a lack of standardized chart of accounts, inconsistent revenue recognition policies, fragmented ERP systems, and inadequate segregation of duties within the newly combined finance team. These gaps often lead to data integrity issues and increased risks of material misstatement.

How does a Management Letter address financial reporting risks during integration?

The letter identifies risks such as improper valuation of acquired assets, unrecorded liabilities, and errors in purchase price allocation (PPA). By documenting these risks, management can implement corrective adjustments to ensure compliance with relevant accounting frameworks like GAAP or IFRS.

What role does the Management Letter play in optimizing the post-merger treasury function?

It highlights weaknesses in cash management protocols, such as redundant bank accounts, inconsistent wire transfer authorizations, and poor visibility into consolidated cash positions. The recommendations aim to centralize treasury operations and improve liquidity management across the new enterprise.

Why is it critical to remediate integration deficiencies identified in the Management Letter?

Prompt remediation is essential to prevent audit qualifications in subsequent periods, reduce the cost of compliance, and realize the intended financial synergies of the merger. Addressing these findings ensures that the financial data used for strategic decision-making is reliable and transparent.

Comments