Effective governance of an Employee Stock Ownership Plan requires rigorous oversight of internal valuation processes. This article examines critical deficiencies in reporting and the essential controls needed to ensure fair market value compliance. Strengthening these protocols mitigates fiduciary risks and improves audit outcomes for plan sponsors. To streamline your documentation process, below are some ready to use template.

Image cover: Mastering ESOP Valuation Controls: Professional Templates and Management Letter Best Practices

Letter Samples List

- Management Letter Regarding Employee Stock Ownership Plan Valuation Controls

- Management Letter on Material Weaknesses in Employee Stock Ownership Plan Valuation Controls

- Management Letter on Significant Deficiencies Within Employee Stock Ownership Plan Valuation Controls

- Management Letter Concerning Participant Data Input Controls for Employee Stock Ownership Plan Valuation

- Management Letter Reviewing Controls Over Third-Party Specialist Reliance in Employee Stock Ownership Plan Valuation

- Interim Audit Management Letter on Employee Stock Ownership Plan Valuation Controls

- Year-End Management Letter Addressing Employee Stock Ownership Plan Valuation Controls

- Management Letter Identifying Deficient Review Controls in Employee Stock Ownership Plan Valuation

- Management Letter on Internal Controls Over Employee Stock Ownership Plan Valuation Assumptions

- Post-Remediation Management Letter on Employee Stock Ownership Plan Valuation Controls

- Initial Assessment Management Letter for Employee Stock Ownership Plan Valuation Controls

- Management Letter on Segregation of Duties Within Employee Stock Ownership Plan Valuation Controls

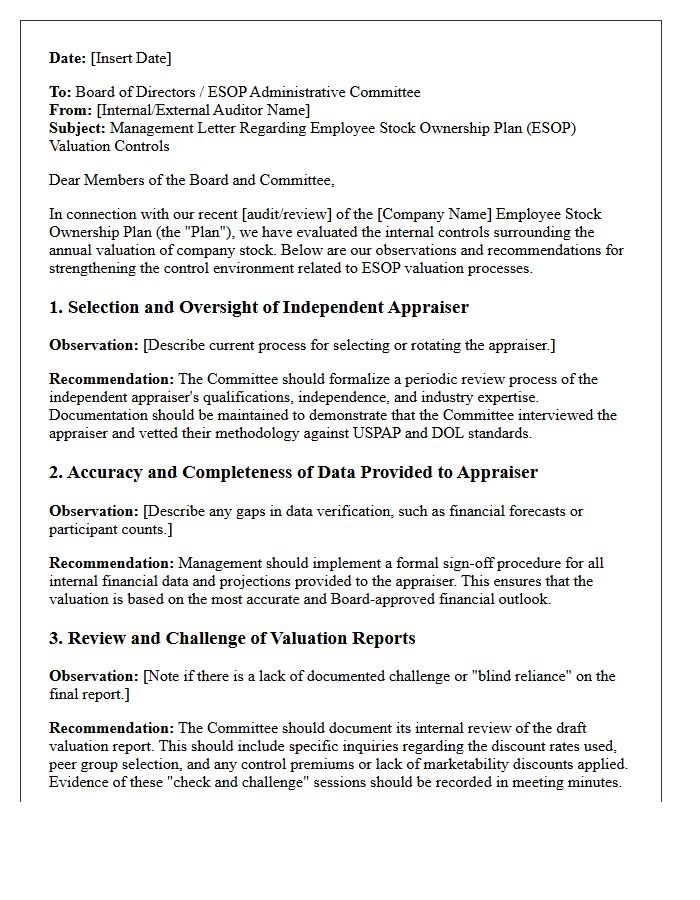

Management Letter Regarding Employee Stock Ownership Plan Valuation Controls

A management letter concerning ESOP valuation controls addresses critical deficiencies in the oversight of private company stock pricing. It highlights the need for robust internal policies to review independent appraisals, ensuring financial data accuracy and reasonable projections. Auditors use this document to identify weaknesses in how leadership evaluates fiduciary responsibilities under ERISA. Strengthening these controls mitigates the risk of stock overvaluation, protecting participants and ensuring regulatory compliance. Effective oversight frameworks are essential for maintaining the plan's integrity and preventing legal liabilities related to inaccurate share value assessments.

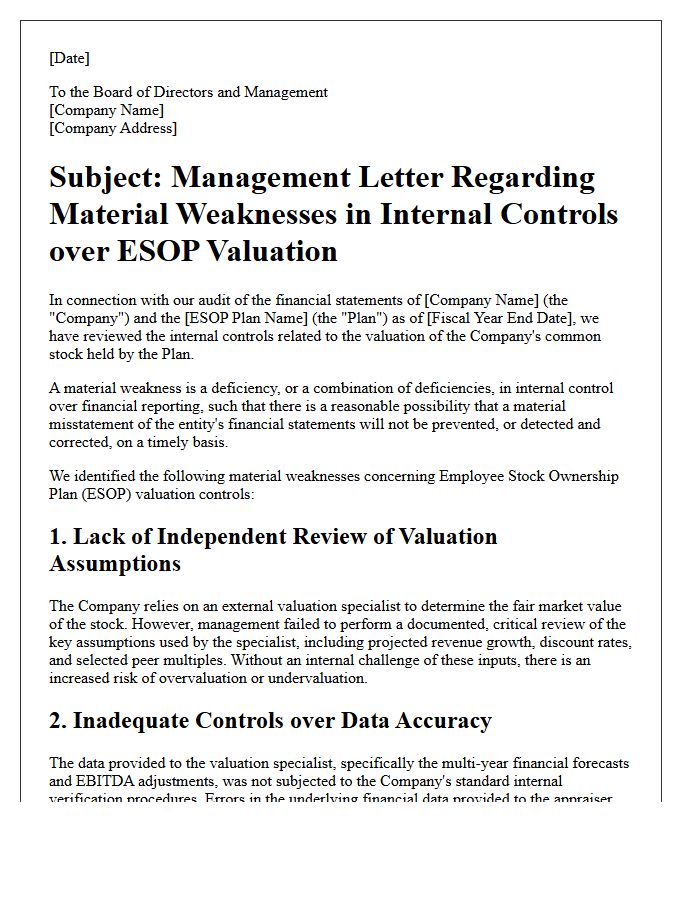

Management Letter on Material Weaknesses in Employee Stock Ownership Plan Valuation Controls

A management letter addresses a Material Weakness in internal controls over ESOP valuations. This formal document notifies stakeholders that existing procedures failed to prevent or detect significant errors in stock appraisal. Accurate financial reporting depends on robust oversight of valuation methodologies, data integrity, and fiduciary review. Failing to remediate these weaknesses risks regulatory non-compliance and inaccurate share pricing. Organizations must implement corrective actions, such as independent audits and enhanced documentation, to ensure the ESOP remains legally sound and protects participant equity value through reliable, objective assessments.

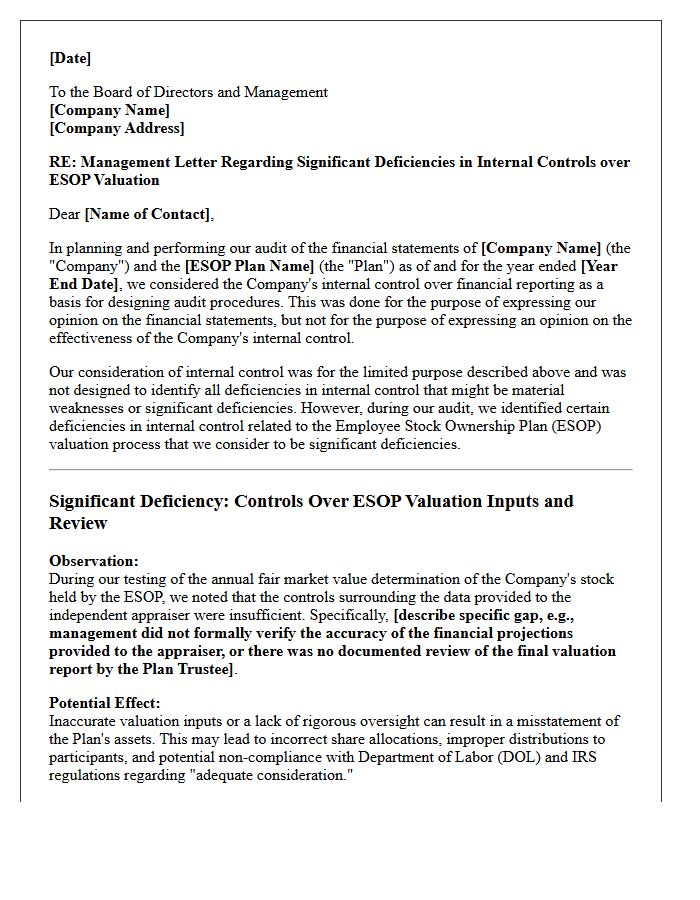

Management Letter on Significant Deficiencies Within Employee Stock Ownership Plan Valuation Controls

A management letter addresses significant deficiencies identified during an ESOP audit, specifically focusing on valuation controls. These weaknesses often involve inadequate oversight of independent appraisers, unreliable financial data, or flawed methodology assumptions. Failure to maintain robust internal controls over the valuation process can lead to inaccurate share pricing, potentially triggering ERISA non-compliance or Department of Labor scrutiny. Companies must implement remediation plans to strengthen governance, ensure data integrity, and protect plan participants' retirement assets from valuation errors.

Management Letter Concerning Participant Data Input Controls for Employee Stock Ownership Plan Valuation

A management letter regarding ESOP valuation ensures the integrity of retirement plan financial reporting. It evaluates the internal controls governing participant data input, such as wages, hours, and employment status. Since inaccurate data leads to flawed stock appraisals and compliance risks, auditors highlight data accuracy to prevent valuation errors. Maintaining robust input controls protects fiduciary liability and ensures the plan reflects a fair market value for all participants.

Management Letter Reviewing Controls Over Third-Party Specialist Reliance in Employee Stock Ownership Plan Valuation

Auditors must rigorously evaluate the Management Letter to ensure Reviewing Controls over external experts are effective. When determining an Employee Stock Ownership Plan valuation, management cannot blindly accept results. They must assess the Third-Party Specialist by validating their professional competence, the reasonableness of underlying assumptions, and the integrity of source data. Strengthening these internal oversight mechanisms mitigates financial misstatement risks and ensures regulatory compliance. Establishing robust Specialist Reliance protocols is essential for verifying that valuation outputs accurately reflect the company's fair market value within the retirement plan framework.

Interim Audit Management Letter on Employee Stock Ownership Plan Valuation Controls

An interim audit management letter regarding ESOP valuation controls identifies critical gaps in financial reporting before year-end. It focuses on the methodology used to determine share prices, ensuring inputs are objective and mathematically sound. Addressing these control deficiencies early prevents material misstatements and regulatory non-compliance. Companies must verify that independent appraisers receive accurate data and that management performs rigorous oversight of all valuation assumptions. Proactive remediation of these findings strengthens fiduciary governance and protects the plan's integrity for all participants.

Year-End Management Letter Addressing Employee Stock Ownership Plan Valuation Controls

A year-end management letter highlights critical internal control deficiencies regarding your Employee Stock Ownership Plan. Auditors focus on ESOP valuation controls to ensure the share price is accurate and compliant with ERISA standards. It is essential to document the review of financial data provided to independent appraisers and verify the reasonableness of underlying projections. Proactively addressing these recommendations mitigates fiduciary risk, prevents potential tax penalties, and ensures the plan's financial statements remain reliable for participants and regulatory bodies like the DOL.

Management Letter Identifying Deficient Review Controls in Employee Stock Ownership Plan Valuation

A management letter identifying deficient review controls in an ESOP valuation highlights critical weaknesses in oversight. It signals that management failed to adequately challenge the valuation assumptions, methodologies, or data provided by external appraisers. These deficiencies can lead to inaccurate share pricing, increasing the risk of fiduciary breaches and regulatory penalties. To ensure compliance, firms must implement robust internal verification processes, documenting their critical assessment of all financial projections and discount rates used to determine the plan's fair market value.

Management Letter on Internal Controls Over Employee Stock Ownership Plan Valuation Assumptions

A management letter addresses critical control deficiencies identified during an ESOP audit. It highlights risks regarding the valuation assumptions used to determine share prices, such as projected cash flows and discount rates. Ensuring robust internal oversight prevents financial misstatements and maintains compliance with ERISA standards. Management must implement rigorous review procedures to validate third-party appraiser data, protecting the plan's integrity and fiduciary responsibilities.

Post-Remediation Management Letter on Employee Stock Ownership Plan Valuation Controls

A Post-Remediation Management Letter serves as critical documentation confirming that a company has corrected internal control deficiencies identified during an audit. Regarding Employee Stock Ownership Plan (ESOP) valuation controls, this letter validates that leadership has implemented robust oversight, accurate data inputs, and independent review processes. It provides fiduciaries and regulators assurance that the methodology used to determine share prices is now reliable and compliant with ERISA standards. Effectively, it closes the loop on previous material weaknesses, ensuring the integrity of retirement plan assets and mitigating future legal or financial risks.

Initial Assessment Management Letter for Employee Stock Ownership Plan Valuation Controls

An Initial Assessment Management Letter identifies critical gaps in internal controls over Employee Stock Ownership Plan (ESOP) valuations. This document focuses on the reliability of financial data, the independence of the qualified appraiser, and the rigor of fiduciary oversight. It ensures that the company's valuation methodology complies with Department of Labor (DOL) standards. Addressing these findings early minimizes the risk of legal liability and ensures the plan maintains its tax-qualified status through accurate share pricing and transparent governance processes.

Management Letter on Segregation of Duties Within Employee Stock Ownership Plan Valuation Controls

A management letter regarding ESOP valuation controls addresses critical risks in financial reporting. It emphasizes the necessity of segregation of duties to prevent conflicts of interest between those managing plan assets and those performing annual appraisals. Effective oversight requires independent reviews of valuation methodologies and underlying assumptions. By separating the authorization, record-keeping, and custodial functions, companies ensure the integrity of share pricing. Documenting these internal control improvements protects fiduciaries from regulatory scrutiny and ensures participants receive a fair, unbiased assessment of their retirement benefits.

What is the purpose of a management letter regarding ESOP valuation controls?

A management letter serves to communicate internal control deficiencies, observations, and recommendations identified during the audit of an Employee Stock Ownership Plan's annual valuation process. It aims to strengthen the oversight and reliability of the fair market value determination.

Which internal controls should be documented for ESOP valuation oversight?

Management should document controls related to the selection of the independent appraiser, the review of source data provided to the valuation firm, and the formal process for challenging the appraiser's underlying assumptions, such as discount rates and projected cash flows.

How does management demonstrate "fiduciary due diligence" in the valuation process?

Fiduciary due diligence is demonstrated by performing a detailed review of the final valuation report, verifying that the methodology complies with USPAP and ERISA standards, and ensuring that the financial projections used are consistent with the company's internal budgets and market realities.

What are common control weaknesses identified in ESOP management letters?

Common weaknesses include the lack of a secondary review of the valuation report, failure to reconcile audited financial statements with the data used by the appraiser, and inadequate documentation regarding the selection and application of control premiums or lack of marketability discounts.

How can a company improve its internal controls over ESOP valuation reporting?

Companies can improve controls by establishing a formal Valuation Committee, implementing a standardized checklist for report review, and maintaining a clear audit trail that shows how management validated the growth rates and peer group multiples used in the equity calculation.

Comments