Effective financial oversight requires addressing internal control deficiencies within your organization's payment processes. This article examines common weaknesses in cash disbursements, offering professional insights into risk mitigation and audit compliance through a formal management letter. Strengthening these procedures protects assets and ensures accurate reporting. To help you implement these standards, below are some ready to use template.

Image cover: Effective Management Letter Templates for Cash Disbursement Control Deficiencies

Letter Samples List

- Management Letter on Internal Control Deficiencies Over Cash Disbursements

- Management Letter on Segregation of Duties Deficiencies in Cash Disbursements

- Management Letter on Unauthorized Cash Disbursement Vulnerabilities

- Management Letter on the Lack of Dual Signatures for Cash Disbursements

- Management Letter on Weaknesses in Vendor Master File Controls and Cash Disbursements

- Management Letter on Inadequate Supporting Documentation for Cash Disbursements

- Management Letter on Deficiencies in Electronic Funds Transfer Disbursements

- Management Letter on Unreconciled Cash Disbursement Accounts

- Management Letter on Fraud Risks in Cash Disbursement Processes

- Management Letter on Deficiencies in Petty Cash Disbursement Controls

- Management Letter on the Untimely Review of Cash Disbursement Journals

- Management Letter on Ineffective Expense Report Disbursement Controls

- Management Letter on Automated Cash Disbursement System Deficiencies

- Management Letter on Corporate Credit Card Disbursement Irregularities

- Management Letter on the Bypass of Purchase Order Controls in Cash Disbursements

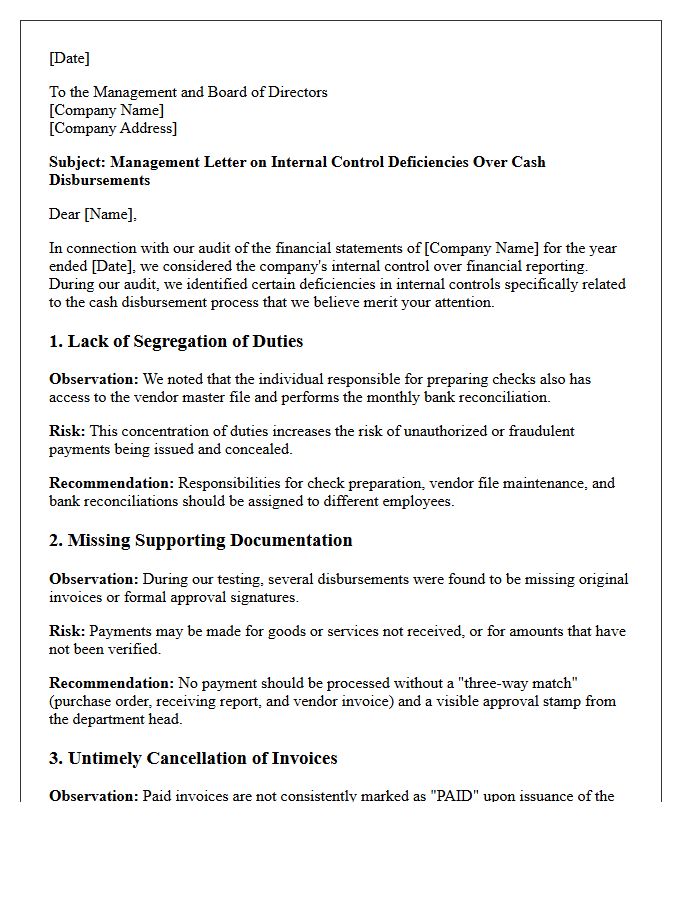

Management Letter on Internal Control Deficiencies Over Cash Disbursements

A management letter identifies critical internal control deficiencies discovered during an audit. Regarding cash disbursements, it highlights risks like unauthorized payments, lack of segregation of duties, or missing documentation. These gaps can lead to financial errors or fraud. The letter provides actionable recommendations to strengthen disbursement protocols, ensuring funds are tracked and approved correctly. Management must address these findings to improve operational financial integrity and safeguard organizational assets from potential misuse or reporting inaccuracies.

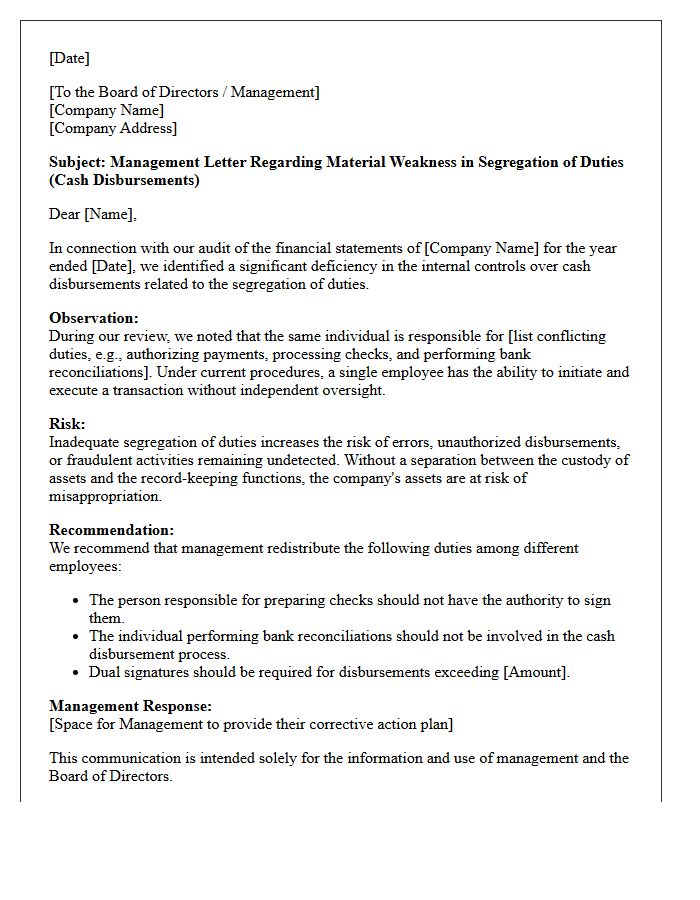

Management Letter on Segregation of Duties Deficiencies in Cash Disbursements

A management letter addressing segregation of duties deficiencies in cash disbursements identifies critical internal control weaknesses where one individual handles multiple financial phases. To prevent fraud and errors, organizations must separate the authorization, recording, and physical custody of funds. Overlapping responsibilities in processing payments or reconciling bank statements increase misappropriation risks. Implementing independent reviews and distinct roles ensures financial integrity and accountability. Addressing these findings promptly strengthens the control environment, protects liquid assets, and ensures accurate financial reporting within the procurement-to-pay cycle.

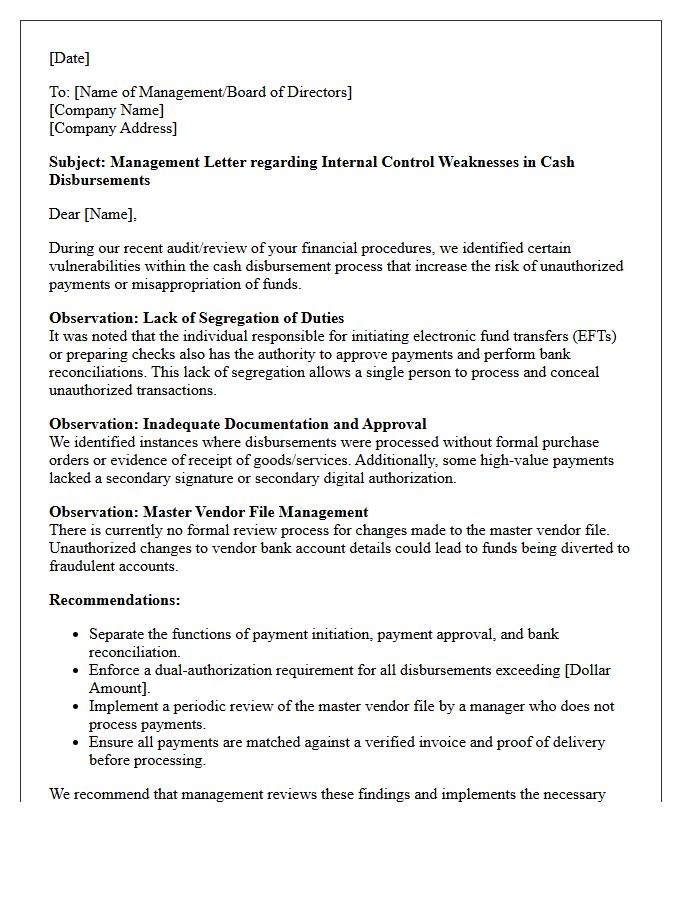

Management Letter on Unauthorized Cash Disbursement Vulnerabilities

A management letter identifies critical control weaknesses regarding unauthorized cash disbursements. It highlights vulnerabilities like lack of segregation of duties, missing approval hierarchies, and poor bank reconciliation oversight. These gaps increase the risk of fraudulent payments and asset misappropriation. Auditors use this document to recommend strengthening internal controls and implementing strict verification protocols. Addressing these findings is essential for safeguarding organizational liquidity, ensuring financial integrity, and preventing financial loss due to exploitation of systemic procedural failures.

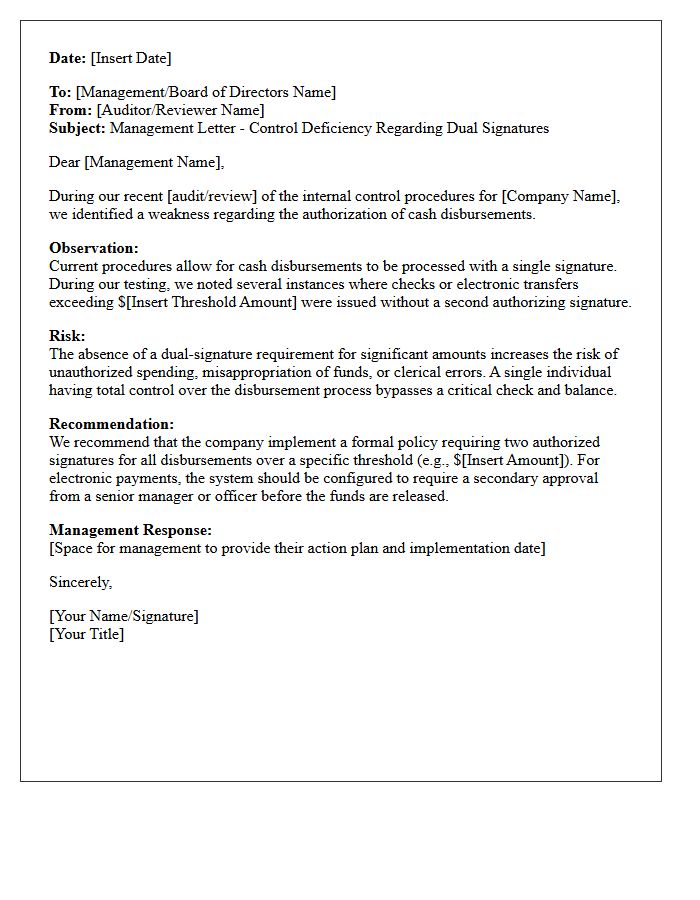

Management Letter on the Lack of Dual Signatures for Cash Disbursements

A management letter addressing the lack of dual signatures for cash disbursements highlights a significant internal control deficiency. Requiring two authorized signatures on checks or electronic transfers prevents unauthorized payments and reduces the risk of fraud or embezzlement. Without this segregation of duties, a single individual has total control over liquid assets, increasing the likelihood of financial misappropriation. Implementing a dual-signature policy ensures accountability, strengthens oversight, and protects the organization's financial integrity against potential internal theft or clerical errors during the disbursement process.

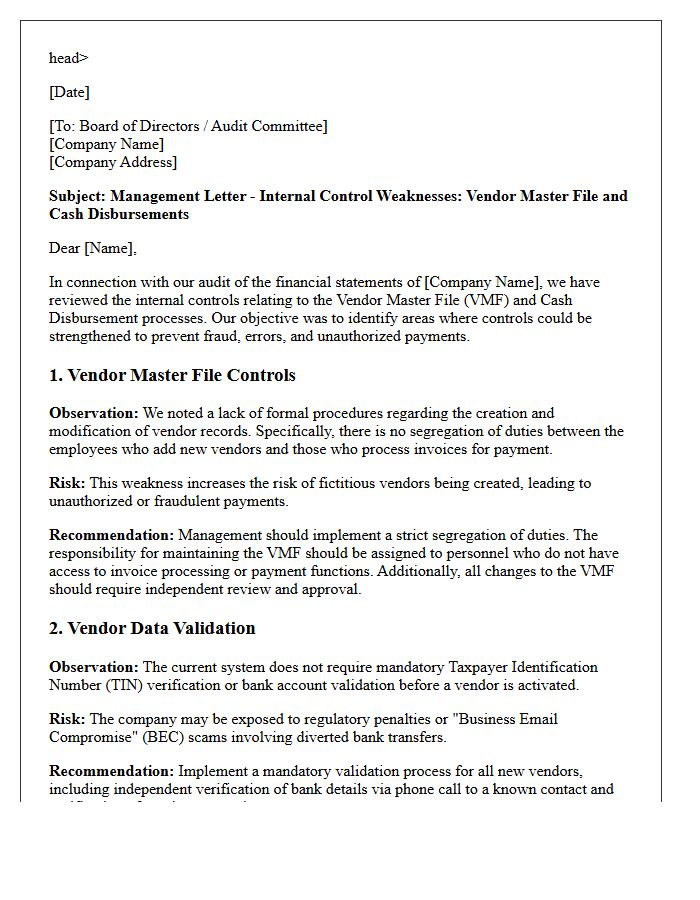

Management Letter on Weaknesses in Vendor Master File Controls and Cash Disbursements

A management letter identifies critical vulnerabilities within the accounts payable cycle, specifically targeting risks like duplicate payments or fraud. It highlights internal control weaknesses in the vendor master file, such as missing tax IDs or inadequate segregation of duties during profile creation. These gaps can lead to unauthorized cash disbursements and financial inaccuracies. Strengthening these processes through regular data cleansing and multi-level approvals ensures better oversight, minimizes the risk of financial leakage, and maintains the integrity of the organization's procurement-to-pay workflow.

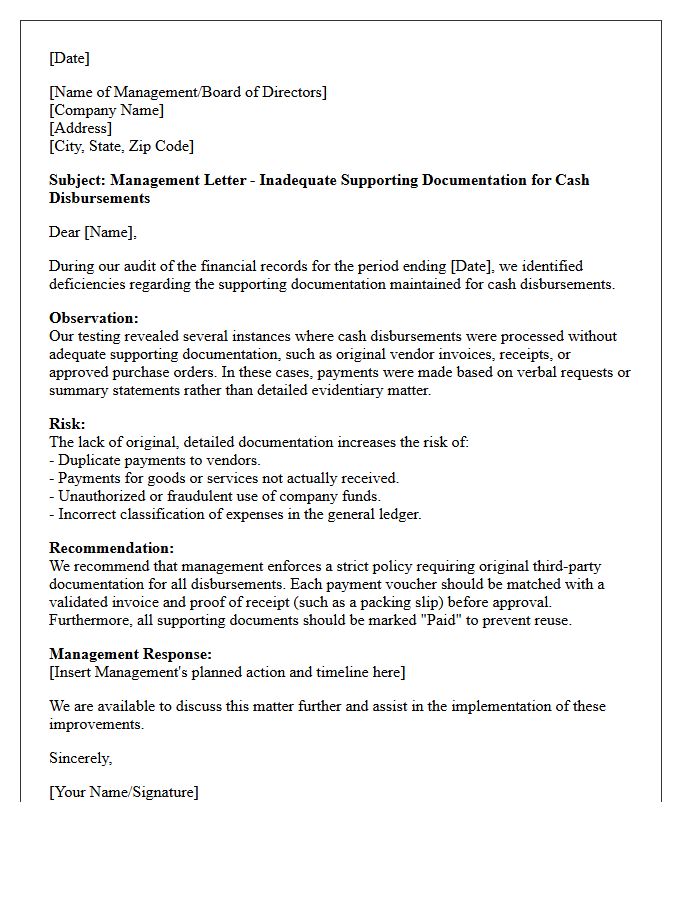

Management Letter on Inadequate Supporting Documentation for Cash Disbursements

A management letter regarding inadequate supporting documentation for cash disbursements warns of weak internal controls. Without invoices or receipts, an organization faces significant risks of fraud, unauthorized spending, and financial misstatement. This formal notification requires management to implement stricter verification procedures and maintain organized records to ensure transparency. Proper documentation acts as a vital audit trail, confirming that every payment is legitimate, accurately recorded, and business-related. Addressing these deficiencies immediately is essential to protect assets and satisfy compliance standards during external audits.

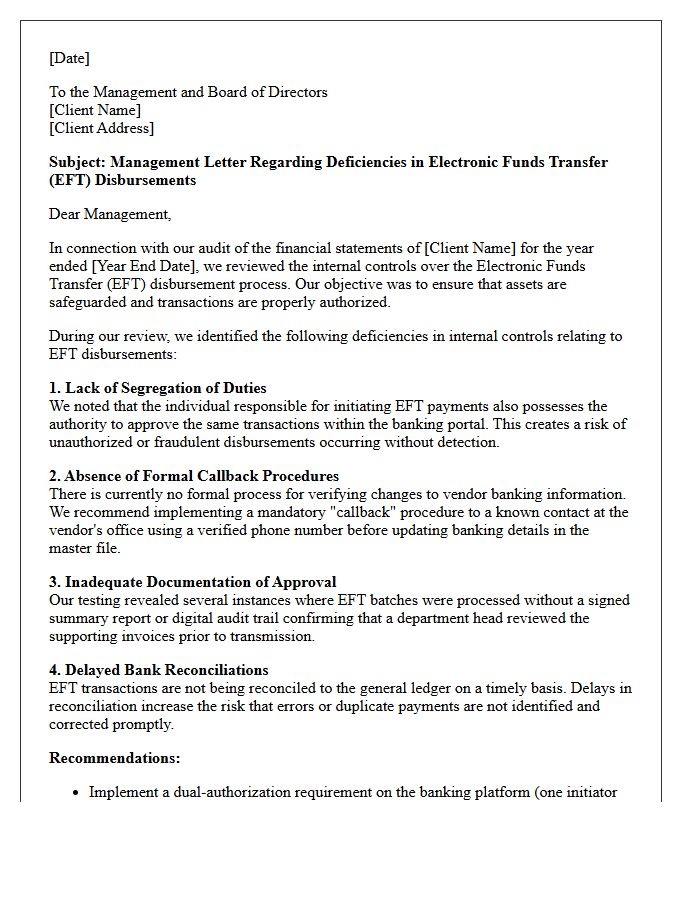

Management Letter on Deficiencies in Electronic Funds Transfer Disbursements

A management letter regarding Electronic Funds Transfer (EFT) disbursements identifies critical control gaps in digital payment processes. It highlights internal control deficiencies such as inadequate segregation of duties, missing dual authorization, or poor encryption protocols. Addressing these findings is essential to prevent unauthorized transactions and fraudulent activities. Organizations must implement corrective actions to strengthen their financial security and ensure regulatory compliance. Timely resolution of these issues mitigates operational risks and protects the entity's cash assets from cyber threats and human error during the automated disbursement cycle.

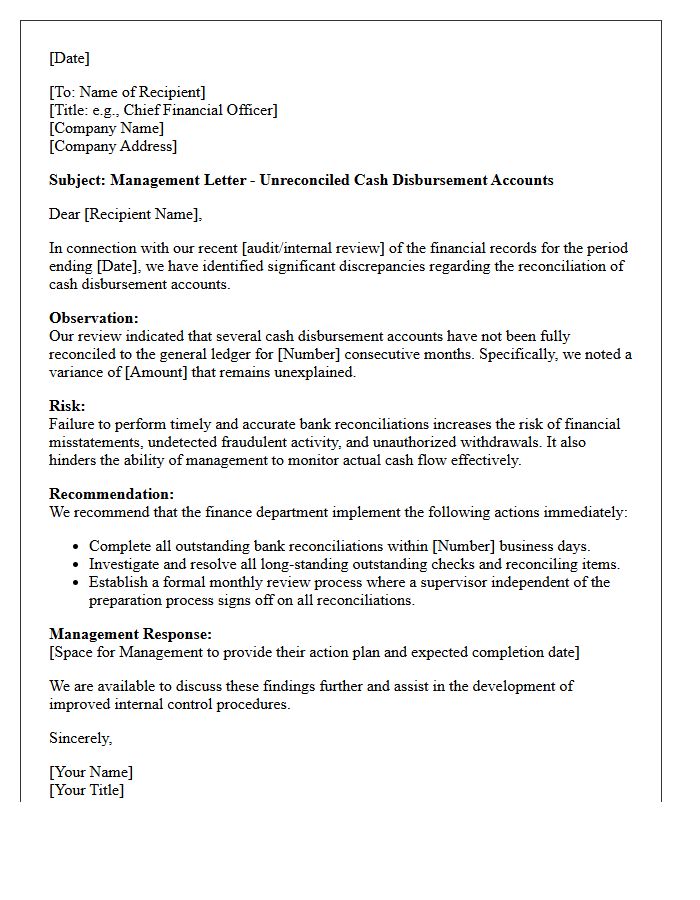

Management Letter on Unreconciled Cash Disbursement Accounts

A Management Letter identifies critical control weaknesses regarding unreconciled cash disbursement accounts, which occur when book balances fail to match bank statements. This discrepancy often signals internal control deficiencies, increasing the risk of undetected fraud, double payments, or accounting errors. Auditors issue these formal notices to urge immediate reconciliation protocols and improved oversight. Timely resolution is essential to ensure financial statement accuracy and maintain robust cash management. Addressing these gaps prevents fiscal mismanagement and strengthens the organization's overall audit trail and reporting integrity.

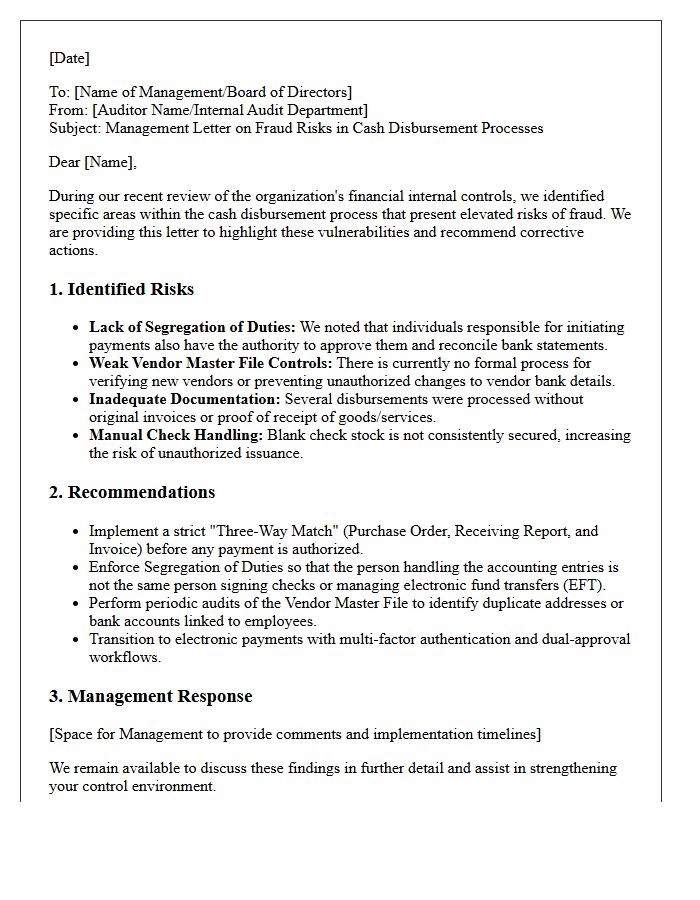

Management Letter on Fraud Risks in Cash Disbursement Processes

A Management Letter identifies critical vulnerabilities in cash disbursement workflows to prevent financial loss. It highlights control weaknesses such as inadequate segregation of duties, missing authorizations, or fraud risks like duplicate invoicing and vendor tampering. By addressing these findings, organizations implement internal controls to mitigate embezzlement and ensure regulatory compliance. Proactive monitoring of electronic transfers and check issuance remains essential for safeguarding assets. Ultimately, these recommendations serve as a strategic roadmap to strengthen financial integrity and minimize the potential for occupational fraud within payment cycles.

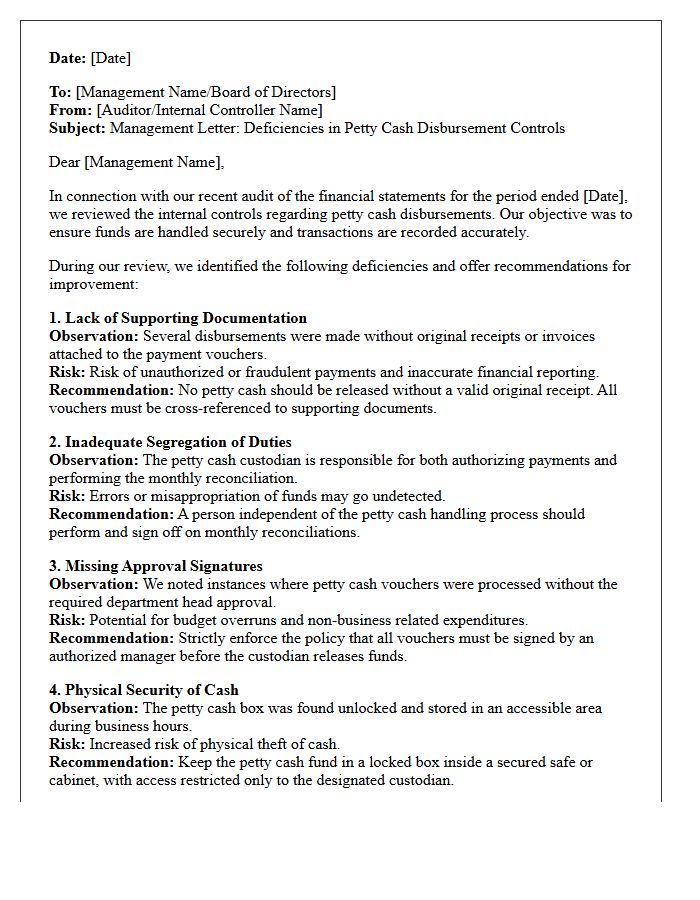

Management Letter on Deficiencies in Petty Cash Disbursement Controls

A management letter addresses critical internal control weaknesses identified during an audit of petty cash. It highlights risks such as missing receipts, lack of authorization, and inadequate segregation of duties. These gaps increase the potential for misappropriation of funds and financial inaccuracies. The document provides actionable recommendations to strengthen safeguarding protocols, ensuring all disbursements are documented, approved, and reconciled regularly. Implementing these improvements is essential for maintaining financial integrity, reducing fraud risk, and ensuring compliance with established accounting standards and organizational policies.

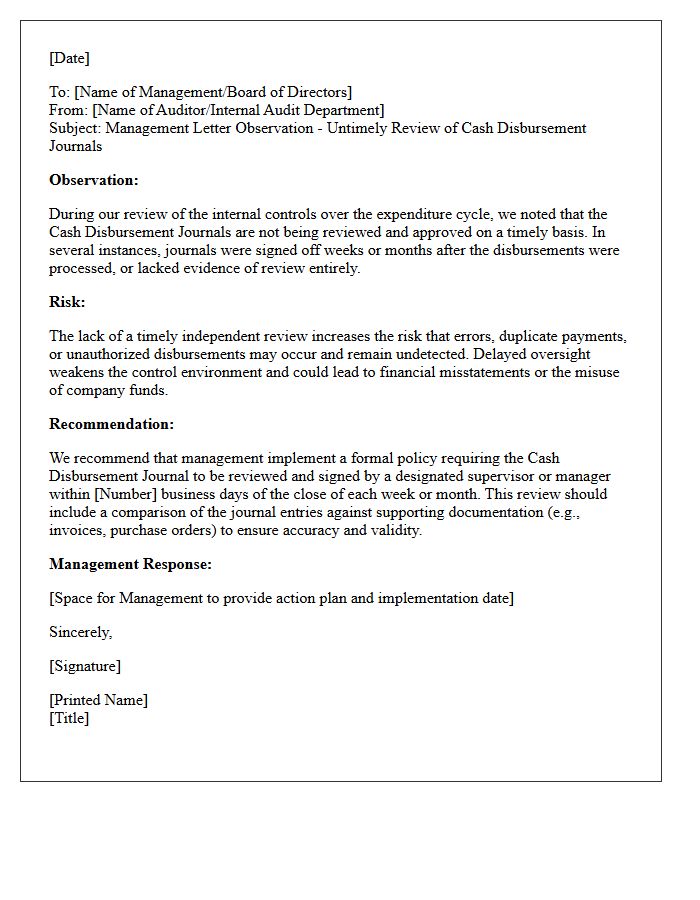

Management Letter on the Untimely Review of Cash Disbursement Journals

A management letter regarding the untimely review of cash disbursement journals highlights critical weaknesses in internal controls. Delays in verifying outgoing payments increase the risk of undetected fraud, duplicate payments, and accounting errors. Organizations must ensure a timely independent oversight process to maintain financial integrity and ensure all expenditures align with authorized budgets. Addressing these deficiencies promptly strengthens the audit trail, improves cash flow monitoring, and safeguards the entity's assets against potential misappropriation or systemic reporting inaccuracies.

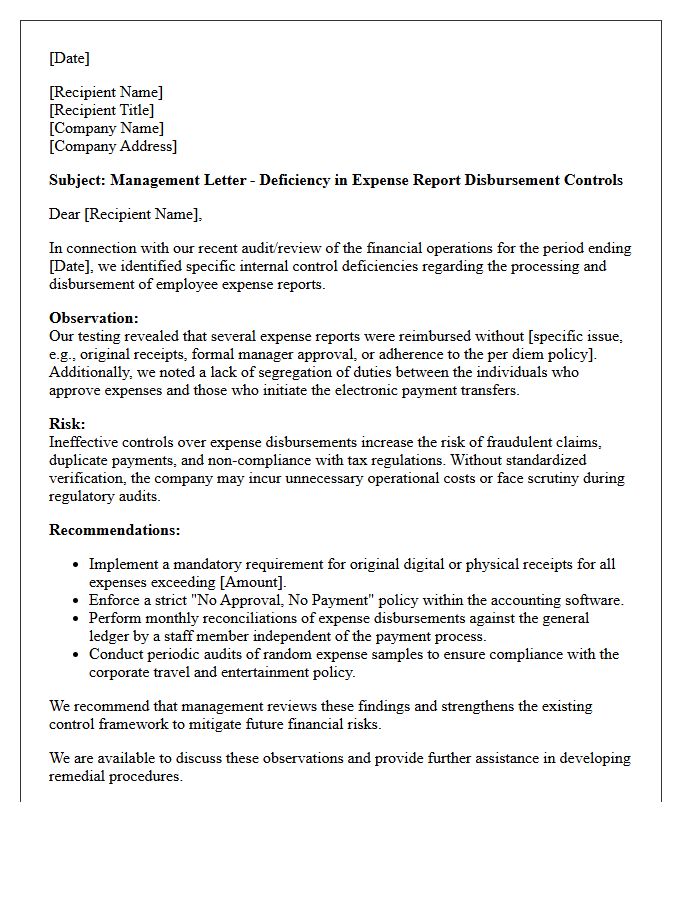

Management Letter on Ineffective Expense Report Disbursement Controls

A management letter addressing ineffective expense report disbursement controls serves as a formal warning regarding financial vulnerabilities. It highlights systemic weaknesses in the reimbursement process, such as missing receipts, lack of managerial oversight, or inadequate policy enforcement. These gaps increase the risk of fraudulent claims and financial misstatements. To mitigate these threats, organizations must implement strict approval workflows, automated verification tools, and regular audits. Addressing these findings promptly ensures fiscal integrity, maintains regulatory compliance, and protects the company's bottom line from avoidable losses and operational inefficiencies.

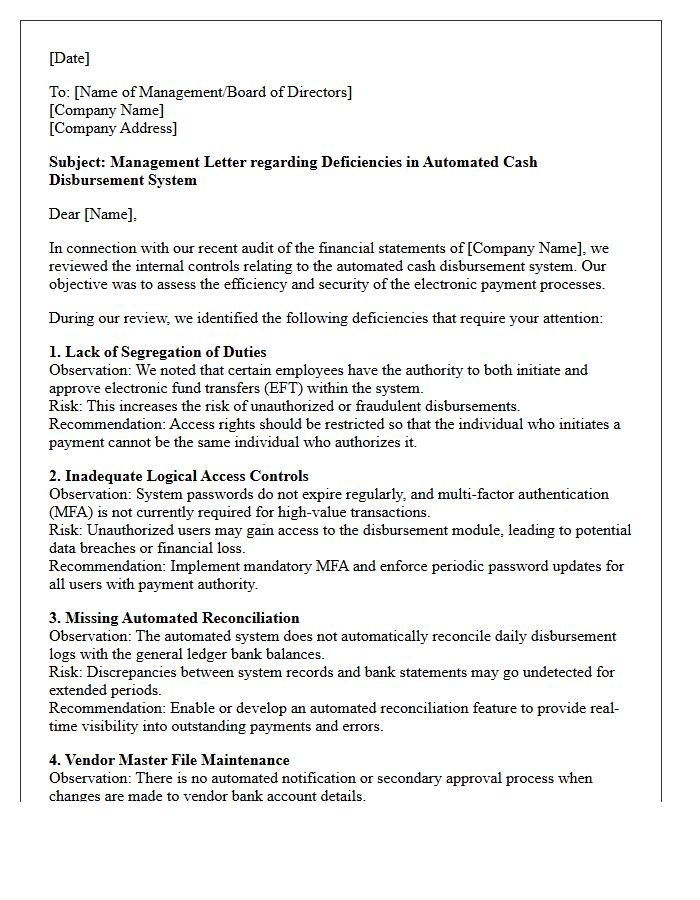

Management Letter on Automated Cash Disbursement System Deficiencies

A management letter regarding automated cash disbursement system deficiencies highlights critical internal control weaknesses that could lead to fraud or financial errors. It identifies risks such as unauthorized electronic fund transfers, inadequate segregation of duties, and weak system access protocols. Organizations must prioritize remediating these findings to ensure the integrity of outgoing payments and maintain regulatory compliance. Implementing robust automated controls and periodic audits is essential to safeguarding liquid assets from exploitation within digital accounting workflows.

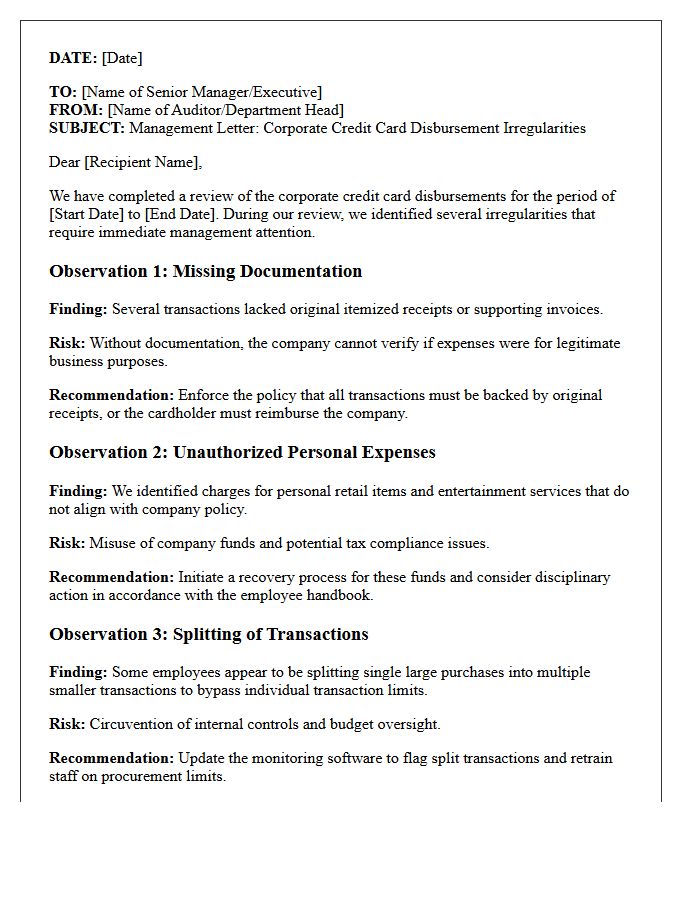

Management Letter on Corporate Credit Card Disbursement Irregularities

A management letter regarding corporate credit card irregularities serves as a critical formal notice to leadership about internal control weaknesses. It identifies unauthorized transactions, missing documentation, or personal expenses charged to firm accounts. This document outlines specific financial risks, such as fraud or embezzlement, and provides corrective recommendations to strengthen oversight. Addressing these deficiencies promptly is essential to maintain audit compliance, safeguard company assets, and ensure accountability across all levels of the organization during the disbursement process.

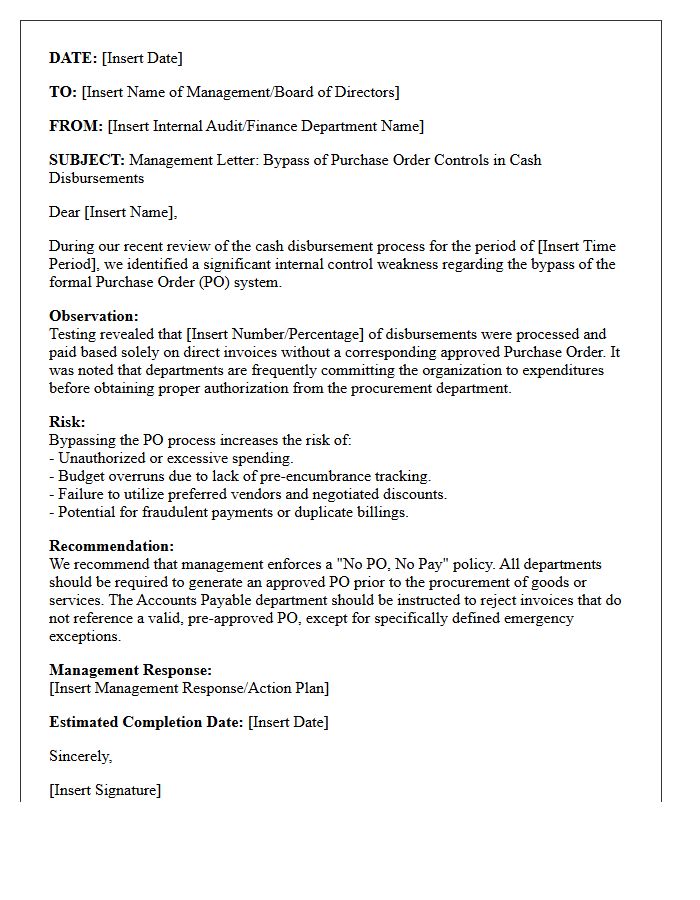

Management Letter on the Bypass of Purchase Order Controls in Cash Disbursements

A management letter addressing the bypass of purchase order controls in cash disbursements alerts stakeholders to significant internal control weaknesses. When staff circumvent formal PO systems, it increases the risk of unauthorized spending, budget overruns, and potential fraud. Auditors use this document to recommend stricter procurement oversight and improved validation procedures. Implementing these corrections ensures that all cash outflows are properly authorized, documented, and aligned with organizational policy, ultimately protecting the entity's financial integrity and preventing unmanaged liabilities from compromising the balance sheet.

What is a management letter regarding internal control deficiencies in cash disbursements?

A management letter is a formal document issued by external auditors to an organization's management that identifies weaknesses in the internal controls governing cash outflows. It outlines specific risks, such as unauthorized payments or lack of segregation of duties, and provides professional recommendations for remedial action to prevent fraud and errors.

What are the most common internal control deficiencies found in cash disbursement processes?

Common deficiencies include a lack of segregation of duties between payment authorization and record-keeping, missing supporting documentation for invoices, failure to cancel paid vouchers to prevent duplicate payments, and inadequate oversight of electronic fund transfers (EFT) or signature authority.

How does a lack of segregation of duties impact cash disbursement security?

When a single employee has the authority to authorize payments, record transactions, and perform bank reconciliations, the risk of undetected fraud increases significantly. Proper segregation ensures that no individual has total control over a transaction lifecycle, creating a system of checks and balances that deters misappropriation of funds.

What recommendations are typically included in a management letter for improving cash controls?

Auditors typically recommend implementing dual-signature requirements for high-value checks, enforcing strict "three-way matching" between purchase orders, receiving reports, and vendor invoices, and ensuring that bank reconciliations are reviewed monthly by a supervisor who is independent of the disbursement process.

Why is it critical for management to respond to deficiencies identified in the audit letter?

Promptly addressing identified deficiencies reduces the organization's exposure to financial loss and reputational damage. Furthermore, demonstrating active remediation of control weaknesses is essential for maintaining stakeholder trust, ensuring regulatory compliance, and potentially reducing future audit costs or insurance premiums.

Comments