Managing state-level tax obligations is critical for modern businesses. This article explores the complexities of Sales Tax Nexus and economic nexus compliance, highlighting how transaction thresholds and physical presence trigger tax liabilities across different jurisdictions. Understanding these regulatory requirements helps mitigate financial risks and ensures operational transparency. To assist your business communication, below are some ready to use template.

Image cover: Navigating Sales Tax Nexus: Management Letter Templates and Compliance Best Practices

Letter Samples List

- Management Letter on Sales Tax Nexus and Economic Nexus Compliance

- Advisory Letter Regarding Multistate Economic Nexus Thresholds

- Accounting Firm Review Letter of Sales Tax Nexus Obligations

- Compliance Letter on Remote Seller and Economic Nexus Liabilities

- Management Letter Detailing Physical and Economic Nexus Findings

- Strategic Advisory Letter on State Sales Tax Nexus Exposures

- Evaluation Letter of Economic Nexus and Taxability Matrices

- Post-Audit Management Letter on Sales Tax Nexus Compliance

- Risk Assessment Letter Regarding Economic Nexus and Wayfair Compliance

- Management Letter on Sales Tax Nexus and Voluntary Disclosure Agreements

- Executive Summary Letter on Multi-Jurisdictional Economic Nexus

- Accounting Firm Management Letter for Sales Tax Nexus Remediation

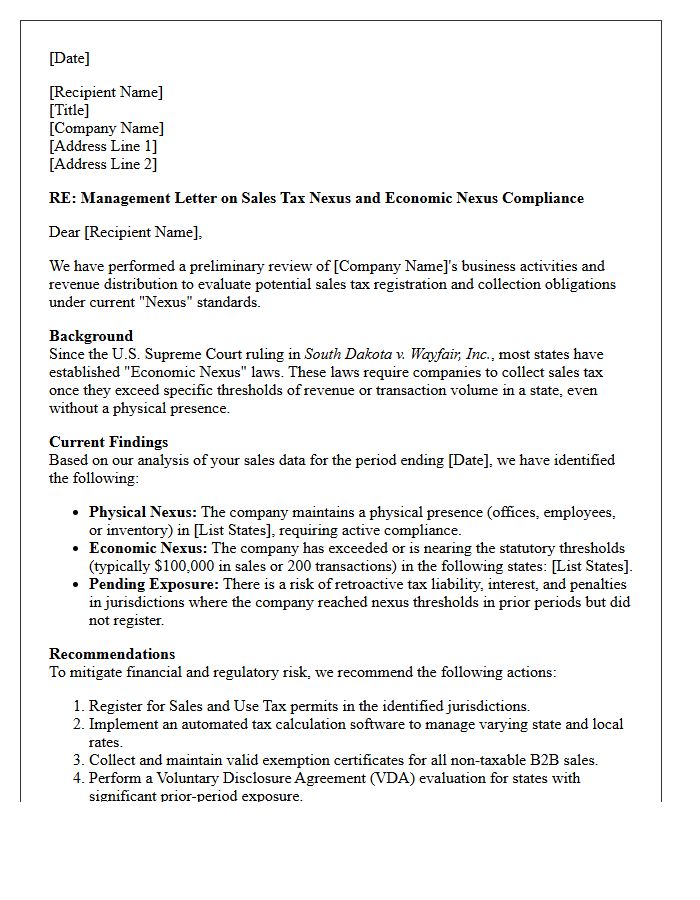

Management Letter on Sales Tax Nexus and Economic Nexus Compliance

A management letter regarding sales tax nexus serves as a critical compliance roadmap for modern businesses. It identifies where physical presence or economic nexus thresholds-based on revenue or transaction volume-trigger mandatory tax collection obligations. This document highlights potential financial liabilities and internal control weaknesses, ensuring the company mitigates risks of audits, penalties, and interest. By addressing multi-state tax complexities, the letter helps management implement robust compliance strategies to navigate evolving jurisdictional rules and maintain fiscal integrity across diverse markets.

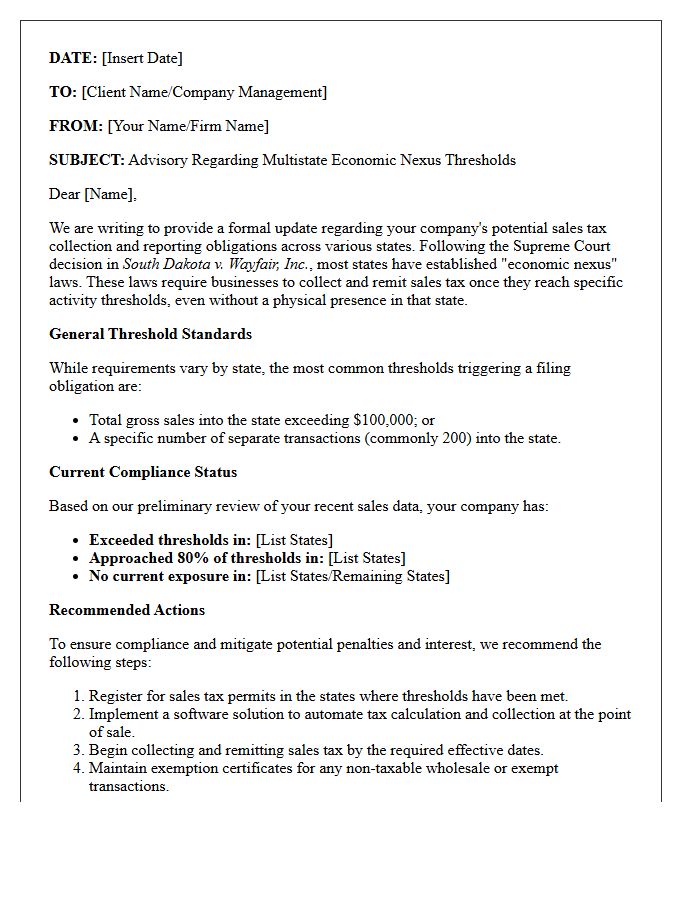

Advisory Letter Regarding Multistate Economic Nexus Thresholds

An Advisory Letter Regarding Multistate Economic Nexus Thresholds provides essential guidance for businesses operating across state lines. It outlines specific revenue or transaction volume limits that trigger tax collection obligations, even without a physical presence. Understanding these economic nexus standards is crucial for maintaining compliance and avoiding significant penalties. Companies must regularly monitor legislative updates as thresholds vary by jurisdiction. Prioritizing nexus studies helps identify potential liabilities and ensures accurate sales tax registration and reporting in every state where business activities meet established legal criteria.

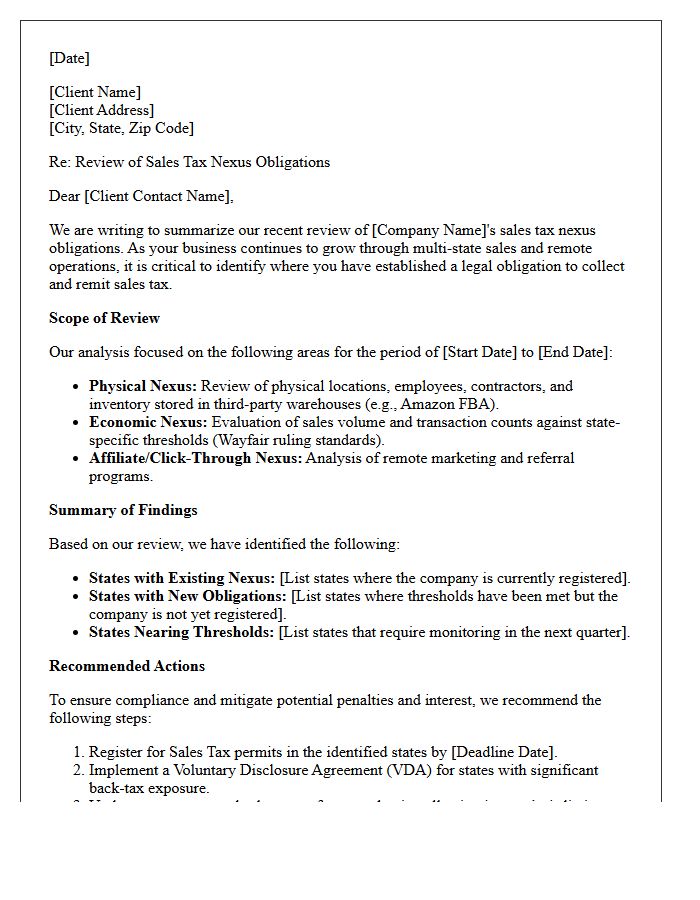

Accounting Firm Review Letter of Sales Tax Nexus Obligations

An accounting firm review letter regarding sales tax nexus evaluates where your business has established a physical or economic presence requiring tax collection. This compliance audit identifies exposure across different jurisdictions based on revenue thresholds or personnel locations. Understanding these obligations is vital to mitigate financial risk and avoid significant back taxes, penalties, and interest. The letter provides a formal roadmap for voluntary disclosure or registration, ensuring your business remains legally compliant with evolving state regulations and protects your bottom line during future tax audits.

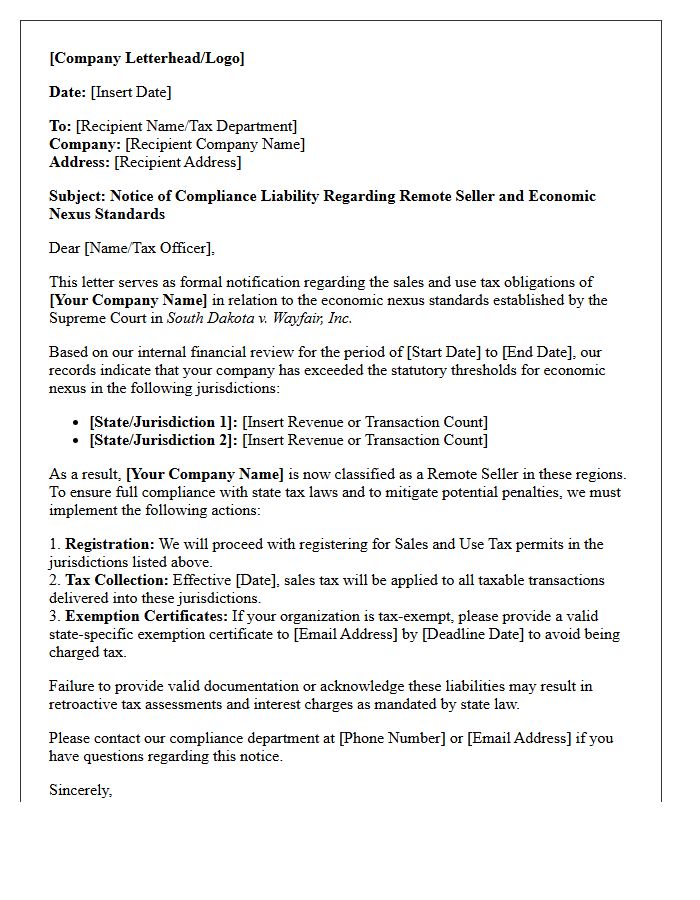

Compliance Letter on Remote Seller and Economic Nexus Liabilities

A compliance letter notifies businesses of potential Economic Nexus liabilities triggered by exceeding state-specific sales thresholds. Remote sellers must understand that physical presence is no longer required to create tax collection obligations. Receiving this notice often indicates that a state's revenue department has identified your business as meeting its "South Dakota v. Wayfair" criteria. Promptly addressing these letters is critical to avoid unpaid back taxes, penalties, and interest. Proper evaluation of your nexus footprint ensures long-term regulatory adherence and mitigates significant financial risks across multiple jurisdictions.

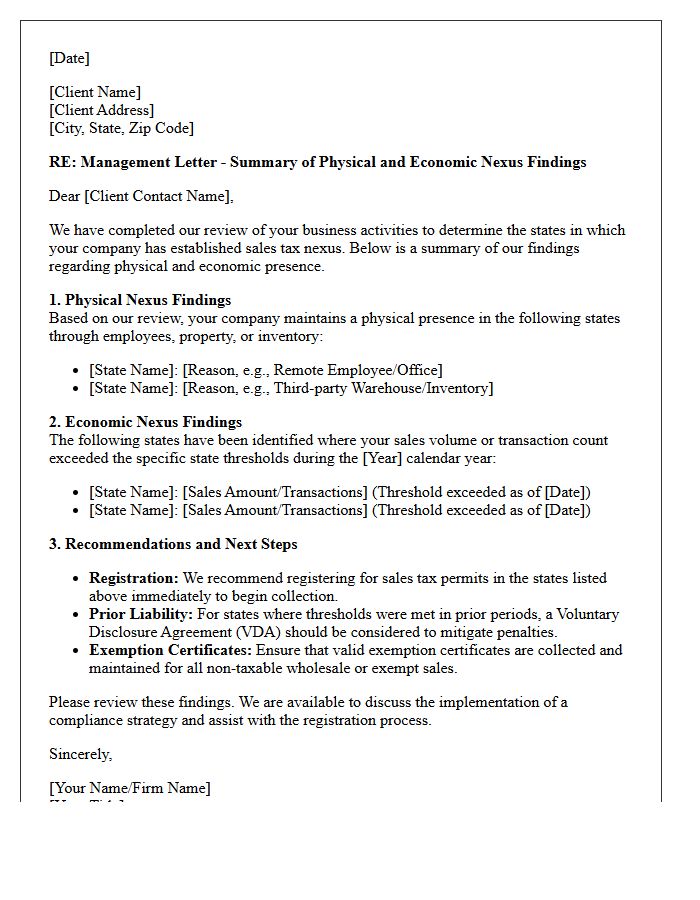

Management Letter Detailing Physical and Economic Nexus Findings

A management letter summarizing physical and economic nexus findings identifies where a business has established tax obligations. Physical nexus occurs through offices, employees, or inventory, while economic nexus is triggered by meeting specific revenue thresholds or transaction volumes in a state. This report highlights potential sales tax liabilities and registration requirements, ensuring the company maintains compliance. It serves as a vital tool for risk mitigation, helping management address past exposure and implement automated systems to manage multi-state tax complexities effectively across diverse jurisdictions.

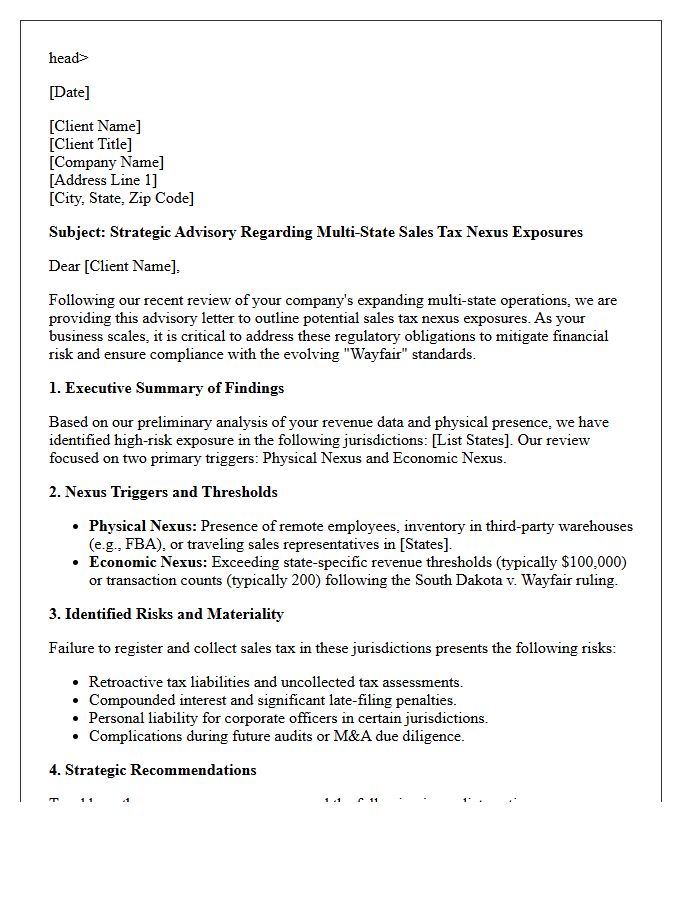

Strategic Advisory Letter on State Sales Tax Nexus Exposures

A Strategic Advisory Letter identifies potential tax liabilities triggered by economic nexus thresholds and physical presence. It evaluates multi-state activities to pinpoint where your business must register, collect, and remit sales tax. By analyzing historical exposure and current compliance gaps, this document provides a roadmap for mitigating risks and avoiding costly penalties. Understanding these obligations is essential for maintaining financial integrity and ensuring your company remains compliant with evolving state-level nexus regulations across diverse jurisdictions.

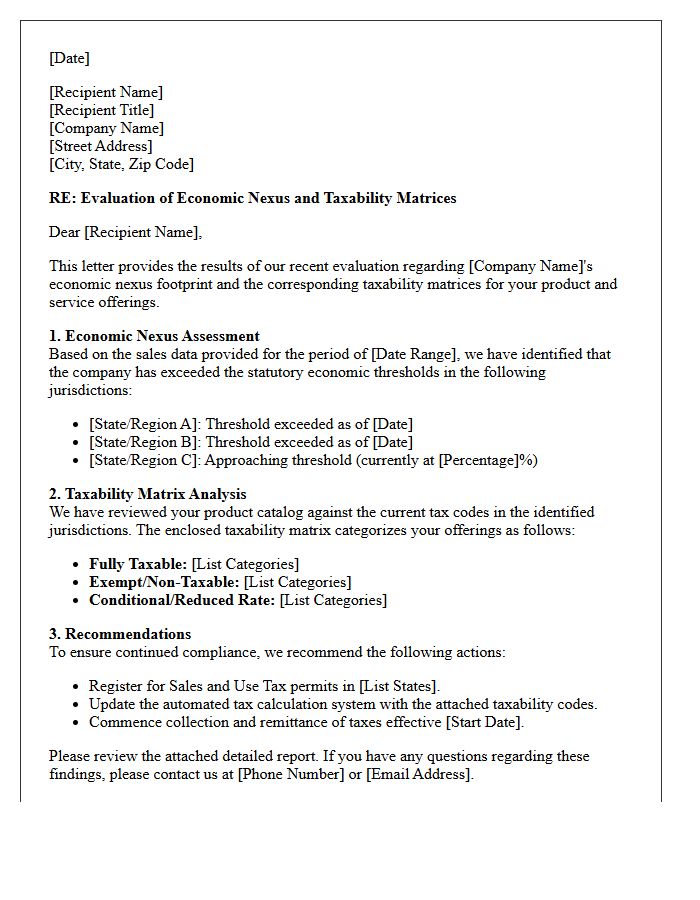

Evaluation Letter of Economic Nexus and Taxability Matrices

An Evaluation Letter of Economic Nexus is a critical document determining if your business meets state-specific sales thresholds for tax collection. It works alongside Taxability Matrices, which clarify how specific products or services are categorized under local laws. Together, these tools ensure compliance by identifying where you have a legal obligation to register and which items are subject to tax. Regularly reviewing these documents mitigates audit risks and prevents costly penalties in the complex landscape of multistate commerce.

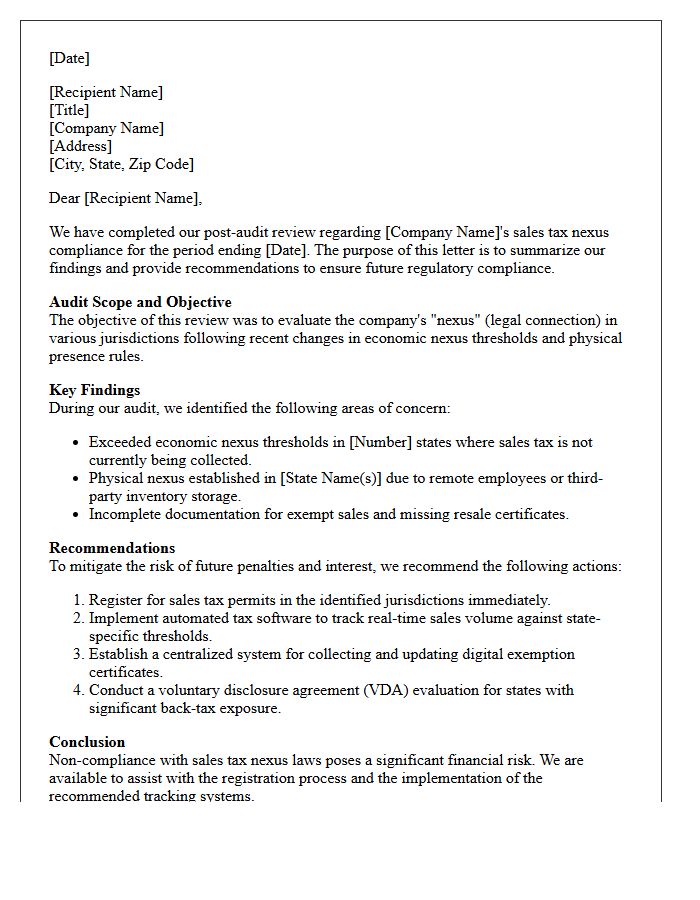

Post-Audit Management Letter on Sales Tax Nexus Compliance

A Post-Audit Management Letter regarding Sales Tax Nexus Compliance serves as a critical strategic roadmap for businesses. It identifies specific taxable presence triggers, such as physical locations or economic thresholds, that were missed during the audit period. This document outlines necessary remediation steps to mitigate future penalties and interest. By addressing these findings, management can implement robust internal controls and automated tracking systems. Ultimately, it ensures ongoing regulatory adherence and prevents costly financial exposure across multiple state jurisdictions through proactive risk management and accurate reporting practices.

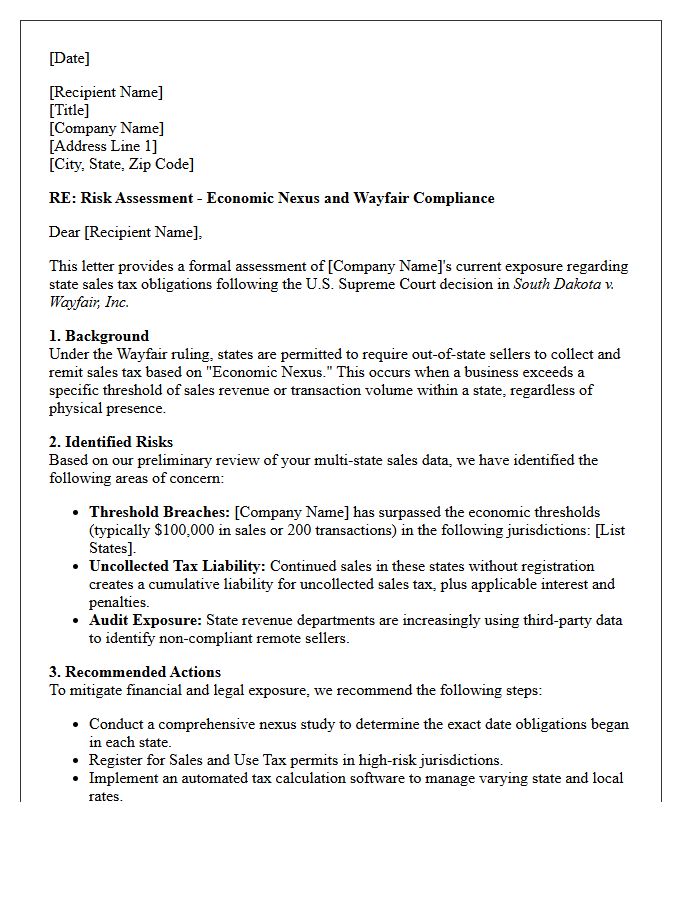

Risk Assessment Letter Regarding Economic Nexus and Wayfair Compliance

A Risk Assessment Letter identifies potential tax liabilities triggered by the Wayfair Supreme Court ruling. This document evaluates your business activities against varying state economic nexus thresholds, typically based on sales revenue or transaction volume. By analyzing historical data, it quantifies exposure for uncollected sales tax, interest, and penalties. Securing this assessment is the first step toward achieving compliance, mitigating financial audits, and determining if Voluntary Disclosure Agreements are necessary to minimize back-tax burdens in jurisdictions where your economic presence has established a legal obligation to collect tax.

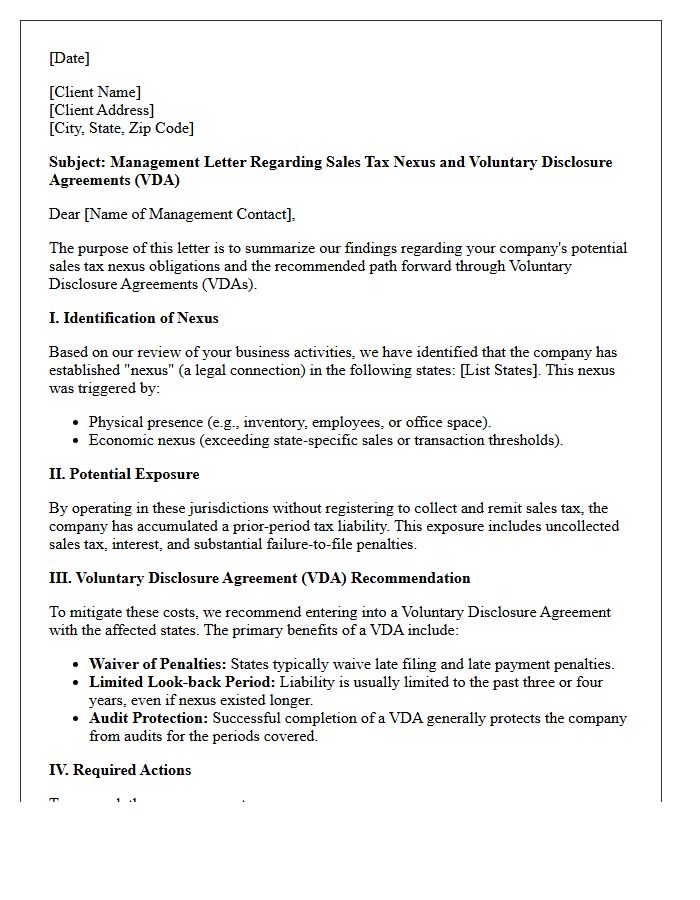

Management Letter on Sales Tax Nexus and Voluntary Disclosure Agreements

A management letter addresses Sales Tax Nexus, which is the legal link established when a business has sufficient physical or economic presence in a state to trigger tax collection duties. If a company discovers past liabilities, Voluntary Disclosure Agreements (VDAs) offer a critical solution. These programs allow businesses to proactively report unpaid taxes in exchange for limited look-back periods and the waiver of penalties. Understanding these obligations is essential for mitigating financial risk, ensuring multi-state compliance, and maintaining accurate financial reporting for auditors and stakeholders.

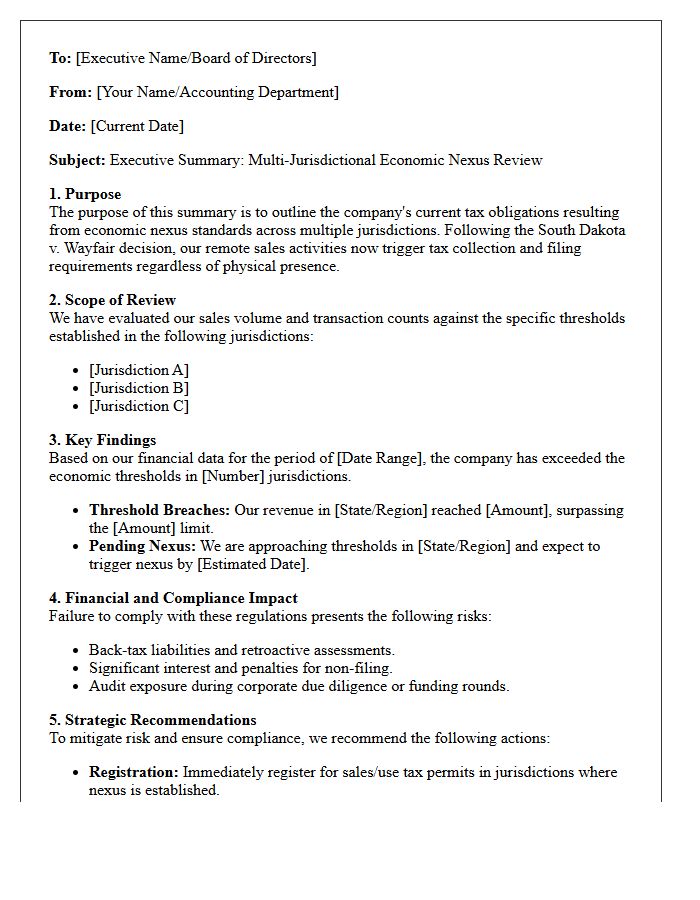

Executive Summary Letter on Multi-Jurisdictional Economic Nexus

An executive summary letter on multi-jurisdictional economic nexus outlines a business's tax obligations across various states. The most critical factor is the Wayfair decision, which established that physical presence is no longer required to trigger sales tax responsibilities. Companies must monitor revenue thresholds and transaction counts to ensure compliance with diverse state laws. This high-level document identifies potential tax liabilities, evaluates risks, and provides actionable recommendations for navigating complex regulatory landscapes. Understanding these nexus triggers is essential for mitigating financial exposure and maintaining legal standing in multiple taxing jurisdictions.

Accounting Firm Management Letter for Sales Tax Nexus Remediation

An accounting firm management letter for sales tax nexus remediation outlines critical steps to resolve historical non-compliance. It identifies states where your business established physical or economic presence, triggering tax collection obligations. The document details the potential financial exposure from unpaid taxes, penalties, and interest. Key recommendations typically include pursuing Voluntary Disclosure Agreements (VDAs) to limit lookback periods and waive penalties. Addressing these findings promptly is essential for mitigating financial risk, ensuring regulatory compliance, and preparing your company for future audits or potential merger and acquisition activity.

What is a sales tax nexus management letter?

A management letter on sales tax nexus is a formal document issued by tax professionals or internal auditors that evaluates a company's legal obligation to collect and remit sales tax in specific jurisdictions. It identifies where the business has established a physical or economic presence and provides actionable recommendations for achieving state-level compliance.

How is economic nexus determined for multi-state businesses?

Economic nexus is determined based on a business's financial activity within a state, rather than physical presence. Most states set specific thresholds, typically $100,000 in gross sales or 200 separate transactions annually; once these limits are surpassed, the business is legally required to register, collect, and remit sales tax in that state.

What are the primary risks of non-compliance with sales tax nexus laws?

Non-compliance carries significant financial and legal risks, including the accrual of unpaid back taxes, substantial interest charges, and heavy penalties. Furthermore, business owners can be held personally liable for uncollected "trust fund" taxes, and unresolved tax liabilities can hinder future audits, mergers, or acquisitions.

Does a physical presence still trigger sales tax nexus?

Yes, physical presence remains a primary trigger for sales tax nexus. Activities such as maintaining an office, storing inventory in a third-party warehouse (like Amazon FBA), having remote employees, or sending sales representatives into a state for trade shows can establish a physical nexus, regardless of transaction volume.

What steps should management take after identifying a new nexus obligation?

Once a nexus obligation is identified, management should perform a historical exposure analysis to determine potential back taxes. Following this, the company should register with the state's Department of Revenue, implement automated tax calculation software, and consider a Voluntary Disclosure Agreement (VDA) to mitigate penalties for prior periods of non-compliance.

Comments