This article provides a comprehensive overview of internal controls for inventory valuation and obsolescence procedures. Learn how to identify slow-moving stock, apply lower of cost or net realizable value principles, and strengthen financial reporting accuracy. Effective management letters help stakeholders mitigate valuation risks and optimize warehouse efficiency. To assist your documentation process, below are some ready to use template.

Image cover: Inventory Valuation and Obsolescence: Management Letter Guide and Professional Templates

Letter Samples List

- Management Letter on Inventory Valuation Deficiencies

- Audit Findings Letter Regarding Obsolescence Procedures

- Management Letter on Inadequate Inventory Costing Methods

- Advisory Letter for Inventory Obsolescence Reserve Policies

- Internal Control Letter on Inventory Valuation Practices

- Management Letter Regarding Slow-Moving Inventory Assessment

- Deficiency Letter on Inventory Obsolescence Identification

- Audit Recommendation Letter for Inventory Valuation Accuracy

- Management Letter on Physical Inventory and Valuation Controls

- Post-Audit Letter Detailing Inventory Obsolescence Risks

- Management Letter Addressing Lower of Cost or Net Realizable Value

- Statutory Audit Letter on Inventory Impairment Procedures

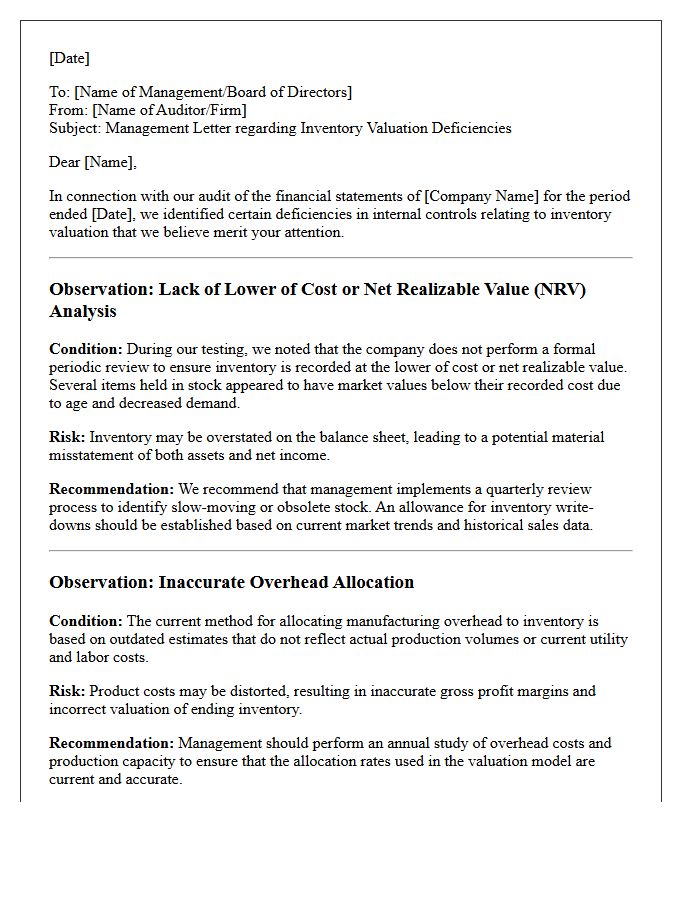

Management Letter on Inventory Valuation Deficiencies

A management letter regarding inventory valuation deficiencies outlines material weaknesses in how a company calculates the value of its stock. Auditors issue this document to highlight errors in costing methods, obsolescence reserves, or physical count reconciliations. These findings are critical because incorrect valuations directly distort the balance sheet and reported net income. Addressing these issues through improved internal controls ensures financial accuracy, maintains investor confidence, and prevents significant audit adjustments during year-end reporting. Proactive remediation of these deficiencies is essential for sound financial governance and operational transparency.

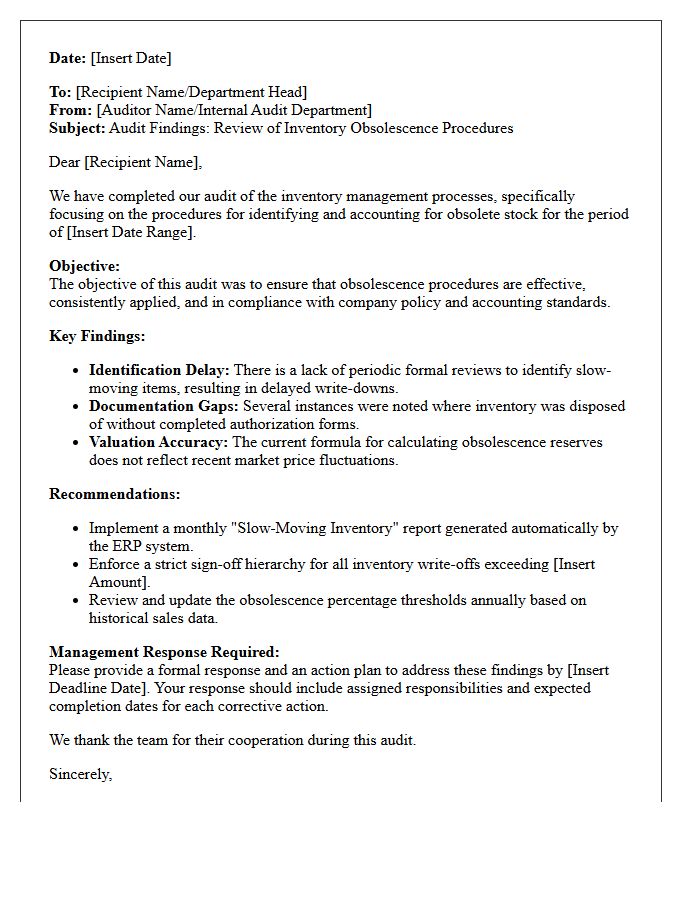

Audit Findings Letter Regarding Obsolescence Procedures

An Audit Findings Letter regarding obsolescence procedures evaluates how a company identifies and writes down outdated inventory. It highlights weaknesses in valuation accuracy and compliance with accounting standards like GAAP or IFRS. Auditors examine if management's methods for detecting slow-moving stock are consistent and data-driven. Addressing these findings is critical to prevent financial misstatements and ensure the balance sheet reflects true market value. Timely remediation improves operational efficiency and strengthens internal controls against inflated asset reporting.

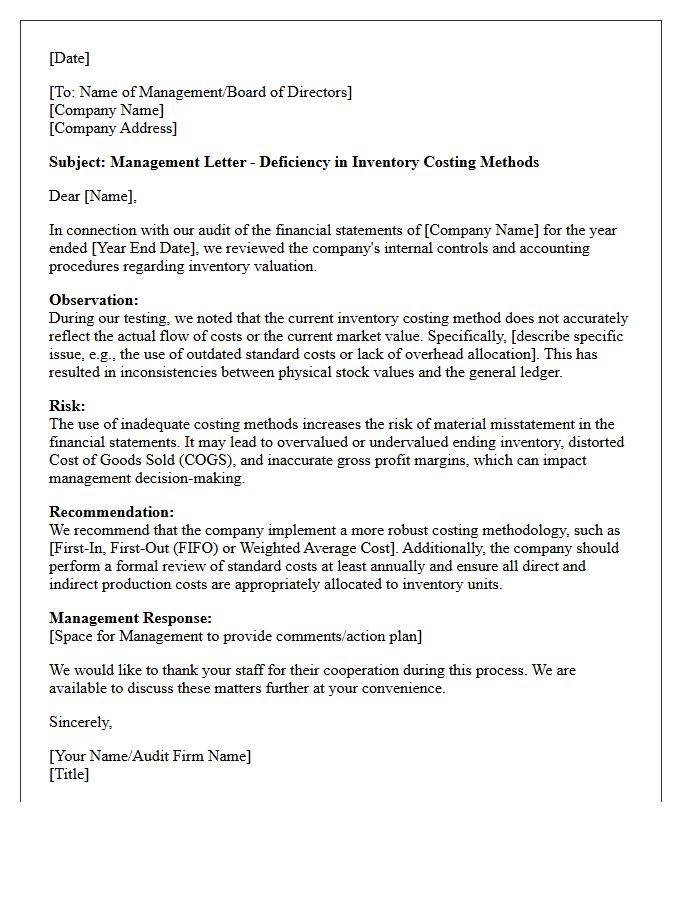

Management Letter on Inadequate Inventory Costing Methods

A management letter addressing inadequate inventory costing methods serves as a formal notification from auditors regarding systemic weaknesses in financial reporting. It highlights how improper valuation techniques, such as failing to apply Lower of Cost or Net Realizable Value, can lead to material misstatements on the balance sheet. Companies must rectify these deficiencies to ensure compliance with accounting standards and improve the accuracy of profit margins. Addressing these observations promptly enhances internal controls and provides stakeholders with reliable financial data for informed decision-making and operational efficiency.

Advisory Letter for Inventory Obsolescence Reserve Policies

An Advisory Letter for Inventory Obsolescence Reserve Policies provides essential guidance on managing devalued stock. It outlines methodologies for identifying slow-moving or outdated items and establishes accounting standards for financial reporting. This document ensures businesses maintain accurate asset valuations by setting clear triggers for impairment. By defining reserve calculations and disposal procedures, the letter helps mitigate financial risk, ensures regulatory compliance, and improves balance sheet integrity through transparent inventory management practices.

Internal Control Letter on Inventory Valuation Practices

An Internal Control Letter on inventory valuation ensures that financial reporting reflects the true value of physical stock. This formal document identifies weaknesses in valuation methodologies, such as FIFO or LIFO, and highlights risks regarding obsolete or damaged goods. By addressing these gaps, management improves accuracy and prevents material misstatements. Robust controls safeguard assets, streamline auditing processes, and ensure compliance with accounting standards. Monitoring these practices is essential for maintaining financial integrity and operational efficiency within a company's supply chain management framework.

Management Letter Regarding Slow-Moving Inventory Assessment

A management letter concerning slow-moving inventory assessment highlights critical risks regarding asset liquidity and financial accuracy. It evaluates if the company effectively identifies stagnant stock and applies appropriate write-downs to reflect net realizable value. Auditors use this document to recommend improved inventory controls, ensuring that overvalued items do not distort the balance sheet. Addressing these findings is essential for maintaining healthy cash flow, optimizing warehouse space, and providing stakeholders with a realistic representation of the company's current assets and overall operational efficiency.

Deficiency Letter on Inventory Obsolescence Identification

A deficiency letter regarding inventory obsolescence identification signifies that an auditor found weaknesses in how a company detects outdated or unsalable goods. This internal control failure suggests that reported asset values may be overstated, as items are not being written down to their net realizable value promptly. To remediate this, businesses must implement systematic valuation reviews and automated tracking to ensure financial statements remain accurate. Addressing these gaps is crucial for maintaining compliance and preventing significant audit adjustments during year-end reporting.

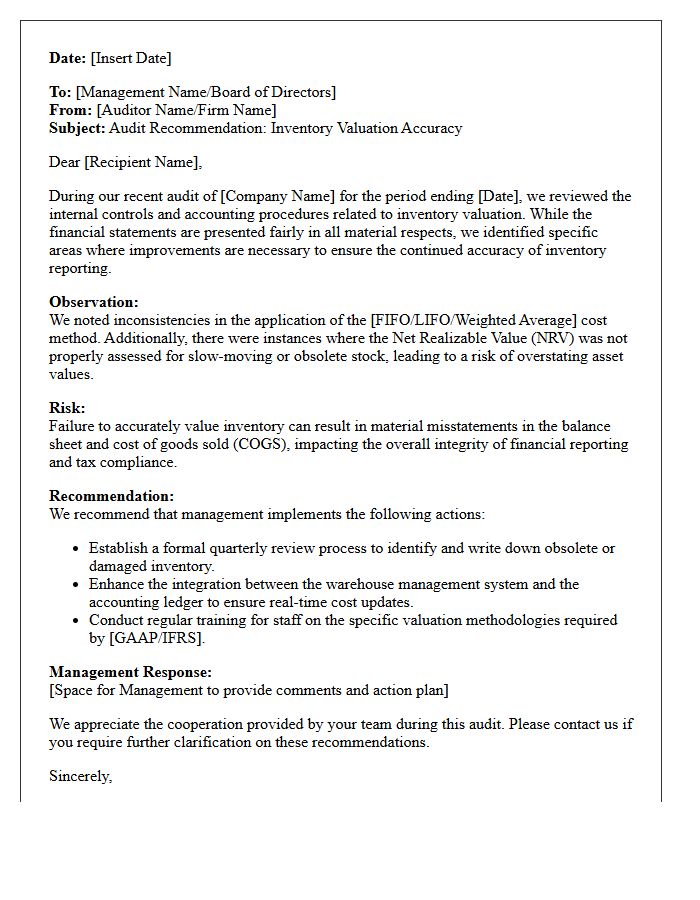

Audit Recommendation Letter for Inventory Valuation Accuracy

An audit recommendation letter serves as a formal advisory document following a financial review. Regarding inventory valuation accuracy, it highlights discrepancies between recorded book values and physical stock counts. The letter provides corrective actions to address weaknesses in internal controls, such as improper costing methods or inadequate obsolescence tracking. Implementing these suggestions ensures financial statements reflect a true and fair view of assets, minimizing the risk of material misstatements. Prioritizing these recommendations strengthens operational efficiency, improves financial reporting integrity, and ensures compliance with accounting standards like GAAP or IFRS.

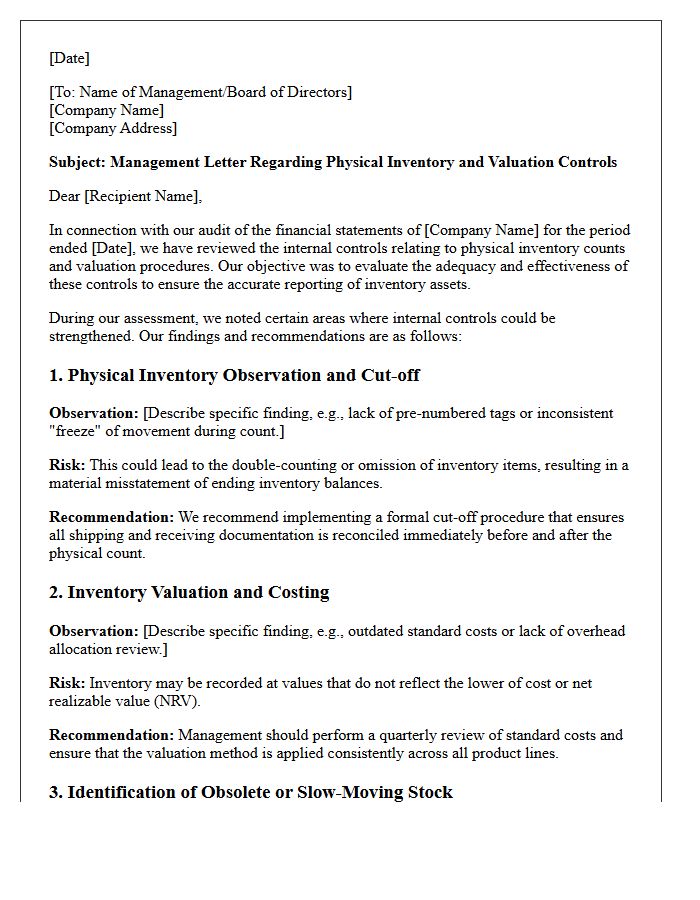

Management Letter on Physical Inventory and Valuation Controls

A management letter regarding physical inventory and valuation controls identifies critical weaknesses in safeguarding assets and reporting accuracy. It highlights discrepancies between book records and actual counts, focusing on internal control gaps such as inadequate segregation of duties or poor oversight. Addressing these observations is essential for preventing asset misappropriation and ensuring inventories are recorded at the lower of cost or net realizable value. Strengthening these protocols enhances financial statement integrity and operational efficiency by mitigating risks of valuation errors and inventory shrinkage within the organization.

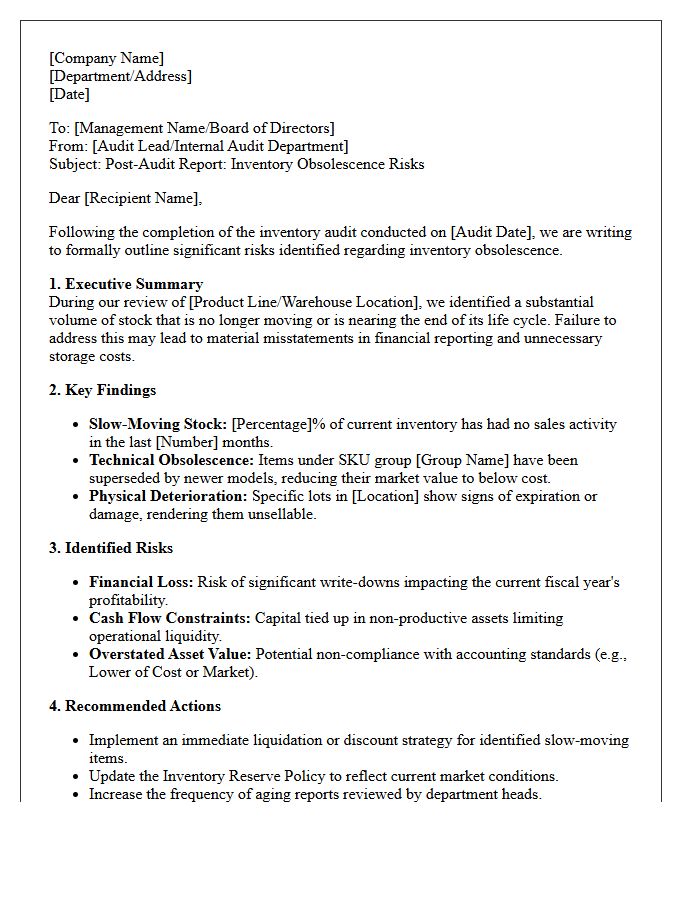

Post-Audit Letter Detailing Inventory Obsolescence Risks

A post-audit letter regarding inventory obsolescence identifies stock that has lost value due to damage, expiration, or declining market demand. This critical document highlights financial reporting risks, ensuring that inventory is recorded at the lower of cost or net realizable value. Management must address these findings to maintain audit compliance and prevent overstated assets. Understanding these risks helps businesses improve inventory management strategies, optimize cash flow, and ensure transparency for stakeholders regarding potential write-downs or future losses linked to unsalable goods.

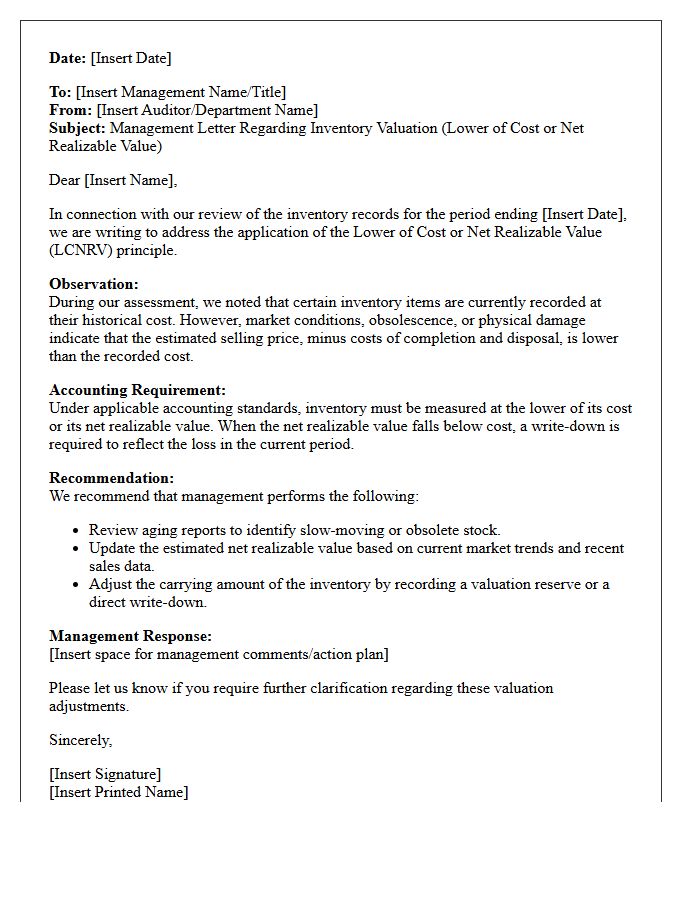

Management Letter Addressing Lower of Cost or Net Realizable Value

A management letter concerning the Lower of Cost or Net Realizable Value (LCNRV) highlights critical adjustments for inventory valuation. It ensures that assets are not overstated on the balance sheet by comparing the original purchase price against the estimated selling price minus disposal costs. If the Net Realizable Value drops below historical cost due to damage or obsolescence, a write-down is mandatory. This document provides essential audit evidence regarding financial reporting accuracy, ensuring compliance with accounting standards and reflecting true inventory liquidity for stakeholders and internal decision-makers.

Statutory Audit Letter on Inventory Impairment Procedures

A statutory audit letter outlines the procedures for evaluating inventory impairment to ensure financial statements reflect true market values. Auditors examine Net Realizable Value (NRV) by comparing cost against estimated selling prices minus completion costs. Key procedures include assessing aging reports, identifying obsolete stock, and verifying management's valuation methodology. This process confirms that assets are not overstated, maintaining compliance with accounting standards like IAS 2 or ASC 330. Understanding these requirements is essential for accurate financial reporting and mitigating risks of material misstatement during a year-end audit.

What is the primary purpose of a Management Letter regarding inventory valuation?

The primary purpose is to provide an independent assessment of whether the entity's inventory is recorded at the lower of cost or net realizable value (NRV) and to highlight deficiencies in internal controls that could lead to material misstatements in financial reporting.

How are obsolescence procedures evaluated during an inventory audit?

Procedures are evaluated by reviewing the methodology used to identify slow-moving, damaged, or excess stock, testing the accuracy of age-analysis reports, and ensuring that the allowance for obsolescence adequately reflects the decline in utility or market value of the goods.

What are the common internal control weaknesses found in inventory valuation?

Common weaknesses include the lack of periodic physical counts, failure to segregate duties between procurement and recording, inconsistent application of costing methods (such as FIFO or Weighted Average), and inadequate documentation for writing down obsolete items.

Why must management document its rationale for inventory write-downs?

Documentation is essential to support the professional judgment used in estimating net realizable value, providing an audit trail that justifies the reduction in asset value and ensures compliance with accounting standards such as GAAP or IFRS.

What actions should management take if the audit identifies gaps in inventory tracking?

Management should implement automated inventory management systems, establish rigorous month-end reconciliation processes, and perform regular "wall-to-wall" counts or cycle counts to ensure physical quantities align with the general ledger.

Comments