Effective corporate governance requires a robust Management Letter on Fraud Risk Management to identify vulnerabilities and strengthen internal controls. Implementing comprehensive whistleblower policies ensures ethical transparency and early detection of misconduct. Proactive oversight protects organizational assets and maintains stakeholder trust by establishing clear reporting channels and preventive measures. Below are some ready to use template.

Image cover: A Comprehensive Guide to Fraud Risk Management and Whistleblower Policy Templates for Management Letters

Letter Samples List

- Management Letter on Fraud Risk Management and Whistleblower Policies in Accounting Firms

- Audit Management Letter Concerning Fraud Prevention and Whistleblower Protocols

- Advisory Letter Regarding Fraud Risk Assessment and Whistleblower Mechanisms

- Confidential Letter on Accounting Firm Fraud Risk Controls and Whistleblower Programs

- Management Letter Detailing Fraud Risk Governance and Whistleblower Guidelines

- Strategic Management Letter on Whistleblower Policies and Fraud Mitigation

- Internal Audit Letter Reviewing Fraud Risk Management and Whistleblower Procedures

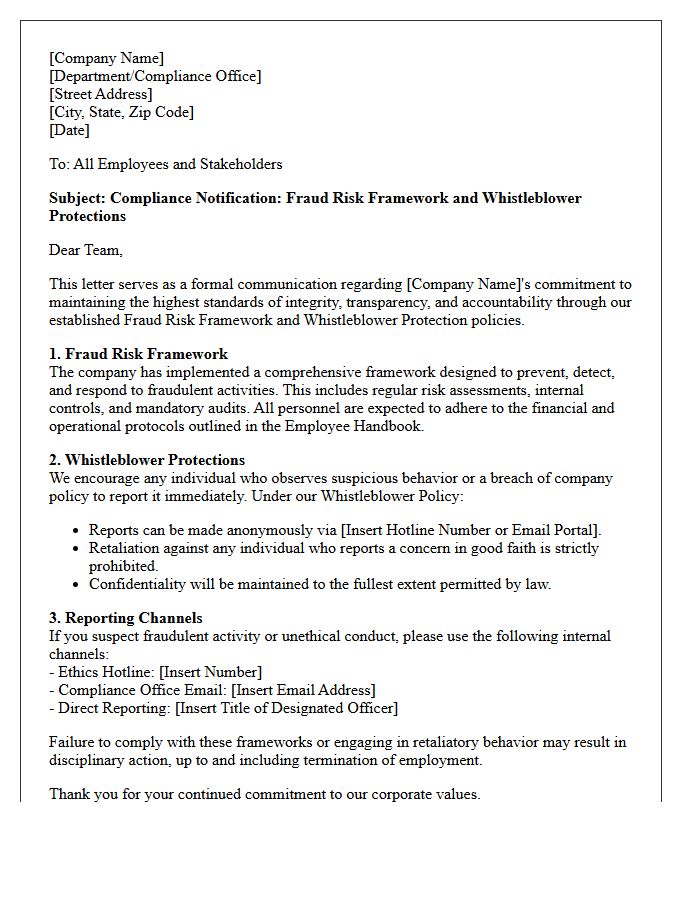

- Compliance Letter on Fraud Risk Frameworks and Whistleblower Protections

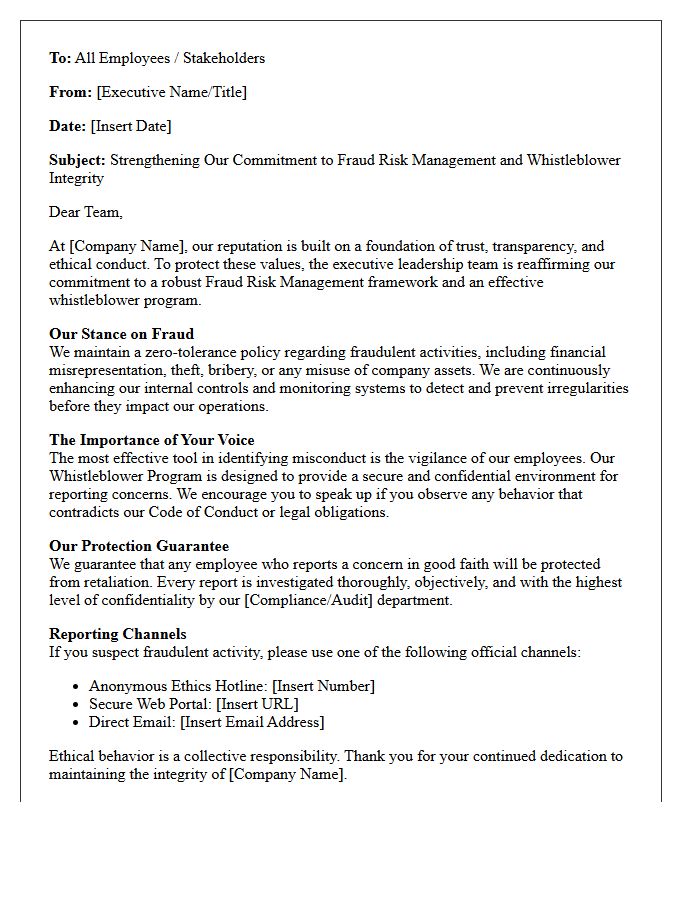

- Executive Letter Addressing Fraud Risk Management and Whistleblower Effectiveness

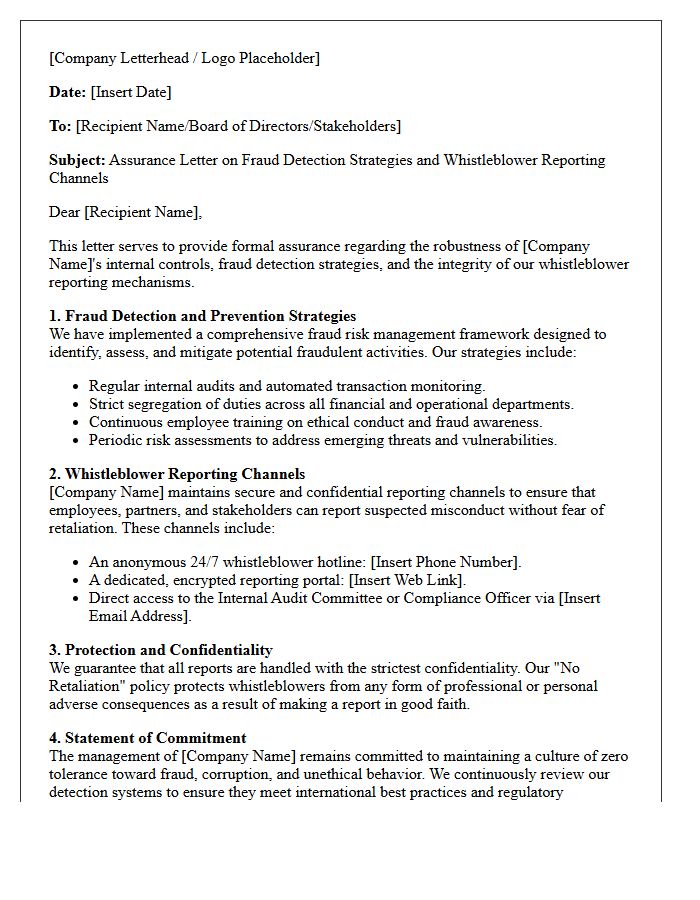

- Assurance Letter on Fraud Detection Strategies and Whistleblower Reporting Channels

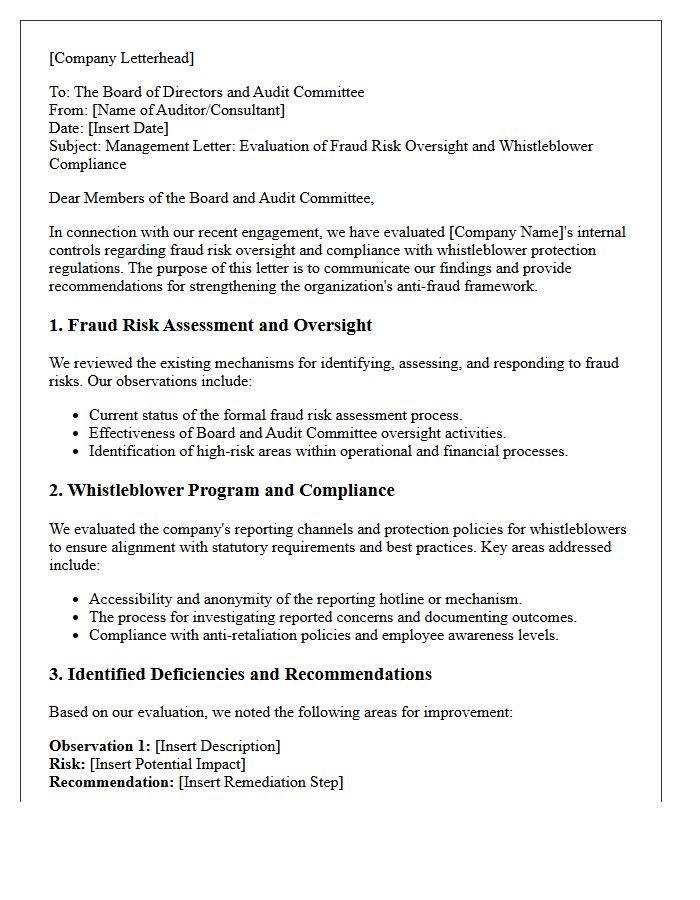

- Management Letter Evaluating Fraud Risk Oversight and Whistleblower Compliance

- Board Advisory Letter on Fraud Risk Management and Whistleblower Best Practices

- Post-Audit Letter Highlighting Fraud Risk Defenses and Whistleblower Policies

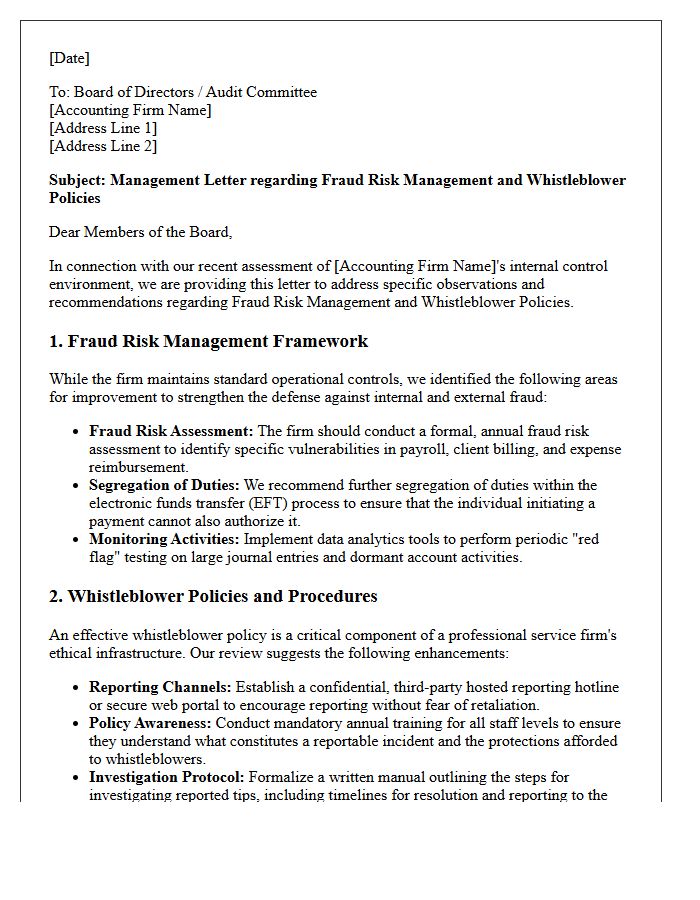

Management Letter on Fraud Risk Management and Whistleblower Policies in Accounting Firms

A management letter serves as a critical communication tool for accounting firms to evaluate internal controls. It identifies weaknesses in fraud risk management, ensuring proactive measures are taken to prevent financial irregularities. A robust whistleblower policy is equally vital, providing a secure channel for reporting misconduct without fear of retaliation. By addressing these areas, firms enhance transparency and strengthen their ethical framework. Implementing these recommendations mitigates legal liabilities and protects the organization's reputation, fostering a culture of accountability and integrity within the financial reporting process.

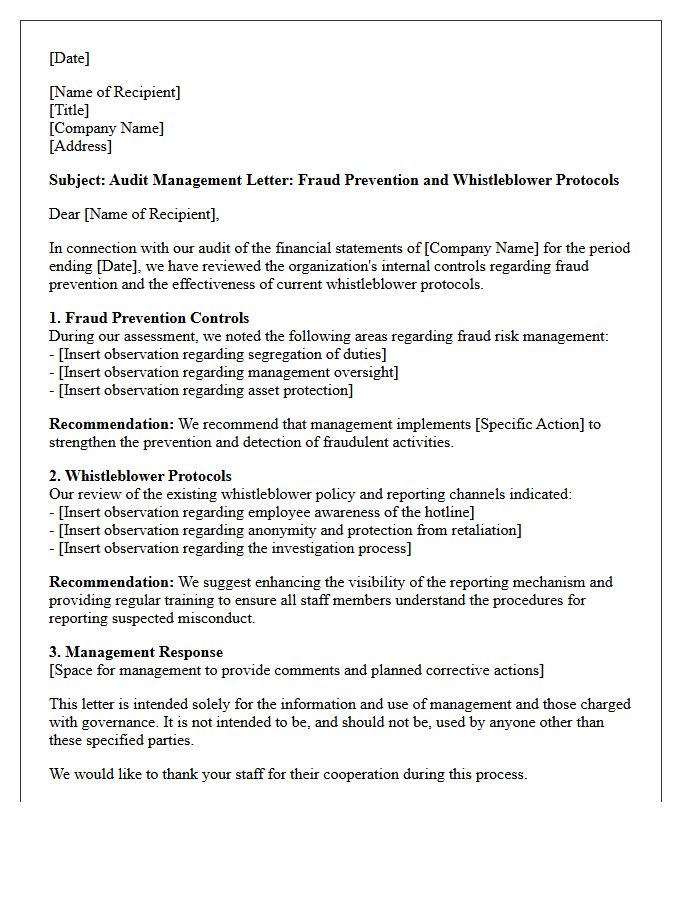

Audit Management Letter Concerning Fraud Prevention and Whistleblower Protocols

An audit management letter evaluates an organization's internal controls, specifically addressing fraud prevention and the effectiveness of whistleblower protocols. It identifies vulnerabilities such as weak oversight or lack of reporting anonymity. Strengthening these areas ensures compliance and builds a culture of accountability. Key recommendations often focus on implementing secure reporting channels and clear anti-fraud policies to mitigate risks. Understanding these findings is essential for management to protect assets, ensure regulatory alignment, and prevent financial misconduct through proactive risk management strategies.

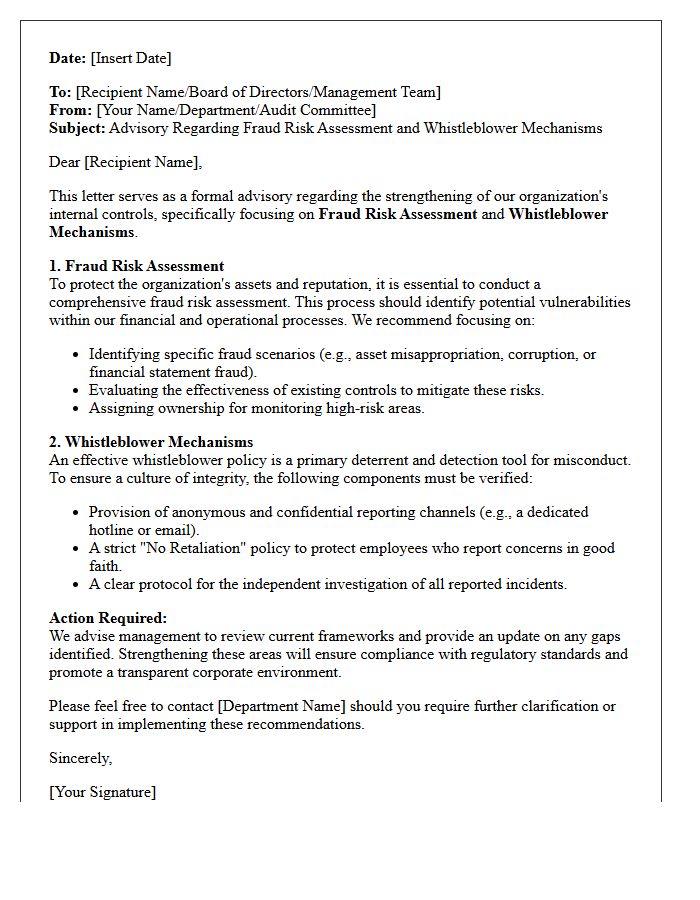

Advisory Letter Regarding Fraud Risk Assessment and Whistleblower Mechanisms

An advisory letter serves as a critical governance tool designed to strengthen organizational integrity. It emphasizes the necessity of a comprehensive fraud risk assessment to proactively identify vulnerabilities within internal controls. Furthermore, the document highlights that effective whistleblower mechanisms are essential for fostering a transparent culture where employees can securely report misconduct. By implementing these strategic recommendations, entities can significantly mitigate financial loss, ensure regulatory compliance, and protect their professional reputation against deceptive practices.

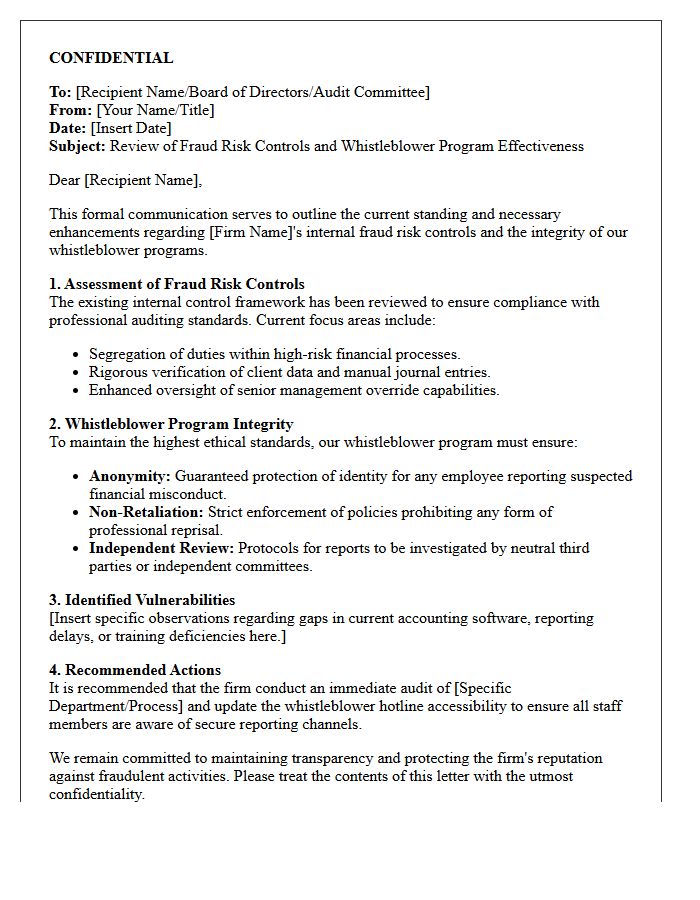

Confidential Letter on Accounting Firm Fraud Risk Controls and Whistleblower Programs

A confidential letter concerning accounting firm fraud risk controls serves as a critical assessment of internal oversight. It evaluates the effectiveness of whistleblower programs in identifying financial irregularities and ethical breaches. These documents outline vulnerabilities in audit procedures and management integrity, ensuring compliance with regulatory standards. Understanding these assessments is vital for maintaining transparency and preventing corporate malpractice. They provide a roadmap for strengthening governance frameworks and protecting stakeholders from systemic risks associated with fraudulent reporting or inadequate reporting mechanisms.

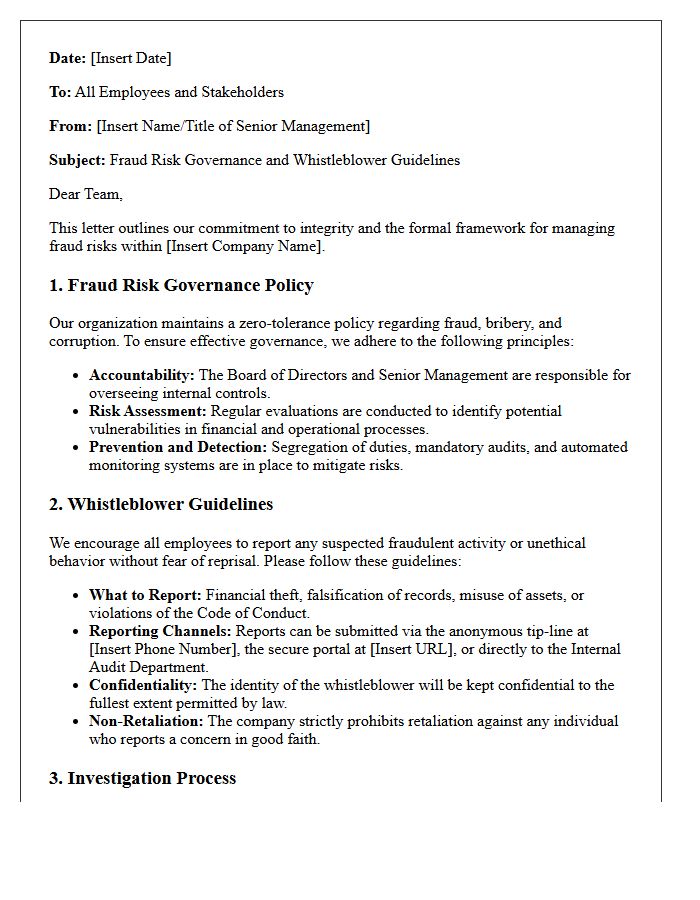

Management Letter Detailing Fraud Risk Governance and Whistleblower Guidelines

A Management Letter serves as a vital communication tool between auditors and stakeholders, specifically addressing Fraud Risk Governance. It outlines structured frameworks to prevent financial misconduct while ensuring regulatory compliance. A critical component involves Whistleblower Guidelines, which establish secure, anonymous reporting channels for employees to disclose irregularities without fear of retaliation. By formalizing these protocols, organizations strengthen their internal controls, promote a culture of transparency, and proactively mitigate potential legal or reputational damages. Understanding these directives is essential for maintaining robust ethical standards and organizational integrity.

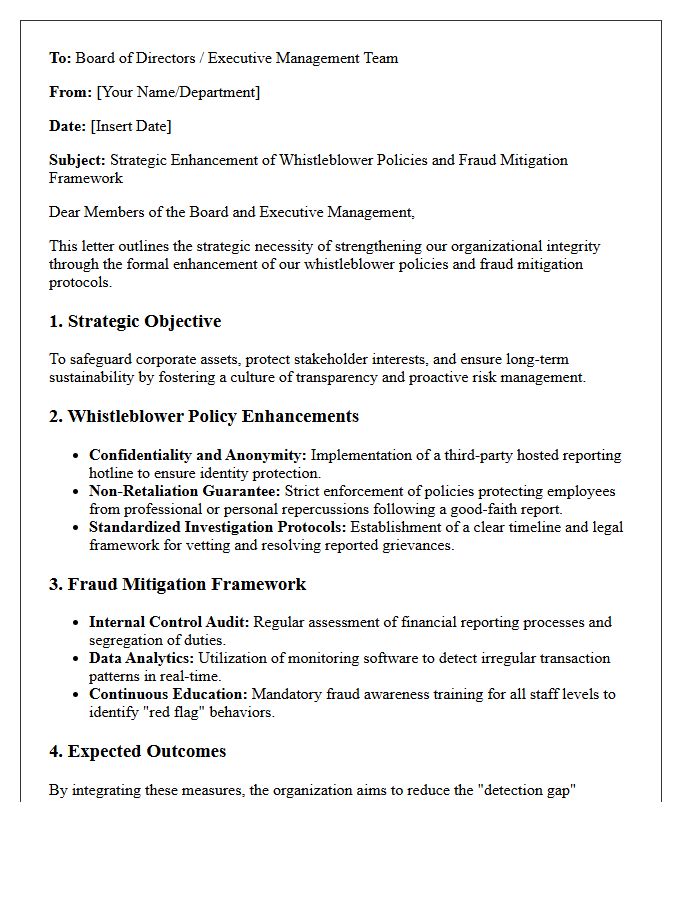

Strategic Management Letter on Whistleblower Policies and Fraud Mitigation

A strategic management letter is essential for establishing robust whistleblower policies to enhance corporate governance. By implementing confidential reporting channels and anti-retaliation protections, organizations foster a culture of transparency. This proactive approach ensures effective fraud mitigation, allowing leadership to detect internal irregularities before they escalate. Prioritizing these ethical frameworks protects institutional reputation and maintains compliance. Establishing clear guidelines through a formal letter demonstrates a commitment to integrity and long-term financial stability, safeguarding the organization's assets against potential misconduct or systemic risks.

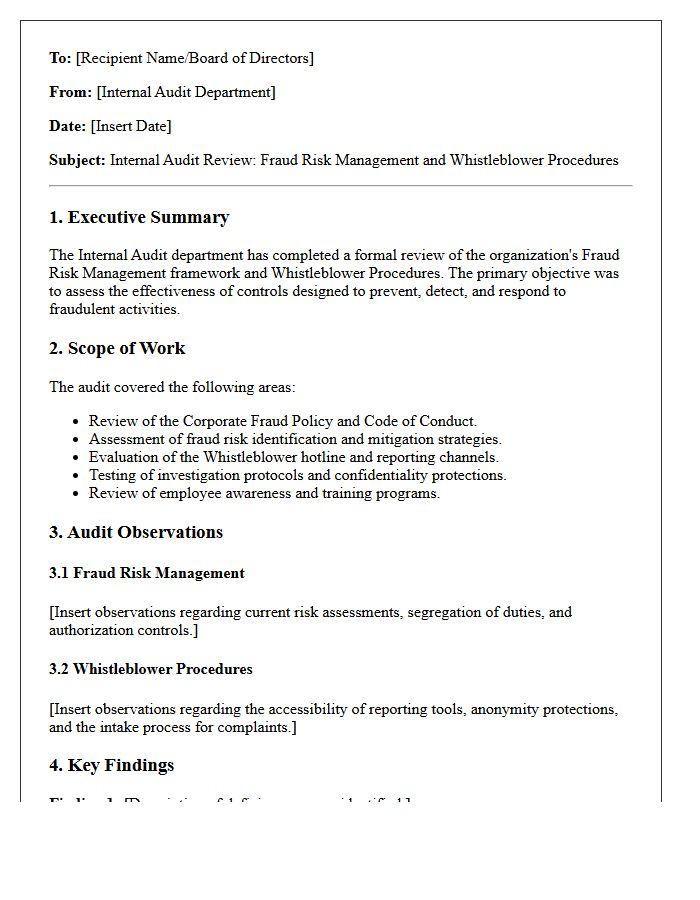

Internal Audit Letter Reviewing Fraud Risk Management and Whistleblower Procedures

An internal audit letter evaluating fraud risk management ensures organizational integrity by identifying vulnerabilities in financial controls. This review assesses the effectiveness of whistleblower procedures, verifying that reporting channels are confidential, accessible, and protected against retaliation. Auditors examine if prevention strategies align with regulatory standards to mitigate deceptive activities. Strengthening these frameworks fosters transparency, discourages misconduct, and protects corporate assets. A robust audit confirms that investigative protocols are timely and objective, ultimately enhancing stakeholder trust and promoting a resilient ethical culture within the enterprise.

Compliance Letter on Fraud Risk Frameworks and Whistleblower Protections

Financial institutions must adhere to a Compliance Letter ensuring robust Fraud Risk Frameworks and enhanced Whistleblower Protections. These mandates require organizations to implement internal controls, conduct regular risk assessments, and establish secure reporting channels for employees. Prioritizing regulatory compliance helps detect illicit activities early while protecting informants from retaliation. Failure to align with these guidelines can lead to severe legal penalties and reputational damage. Maintaining transparent governance through a structured framework is essential for financial integrity and long-term institutional security.

Executive Letter Addressing Fraud Risk Management and Whistleblower Effectiveness

The executive letter emphasizes the critical need for a robust fraud risk management framework to protect organizational integrity. It highlights that whistleblower effectiveness is the cornerstone of early detection, requiring a culture of transparency and non-retaliation. Leadership must ensure reporting channels are accessible and investigations are handled with objective rigor. By prioritizing these controls, executives mitigate financial loss and strengthen stakeholder trust, transforming ethical oversight into a strategic advantage against evolving internal and external threats.

Assurance Letter on Fraud Detection Strategies and Whistleblower Reporting Channels

An Assurance Letter serves as a formal verification of an organization's commitment to integrity. It confirms the implementation of robust fraud detection strategies designed to mitigate financial and operational risks. Furthermore, it validates the existence of secure, anonymous whistleblower reporting channels, ensuring employees can report misconduct without fear of retaliation. This document provides stakeholders with documented confidence that internal controls are active, monitored, and compliant with regulatory standards, fostering a culture of transparency and ethical accountability within the corporate structure.

Management Letter Evaluating Fraud Risk Oversight and Whistleblower Compliance

A management letter on fraud risk oversight assesses how effectively an organization identifies and prevents deceptive practices. It highlights critical gaps in internal controls and evaluates whistleblower compliance to ensure employees have secure channels for reporting misconduct. Robust oversight reduces legal liability and financial loss while fostering a culture of integrity. Organizations must prioritize regular audits of these systems to verify that anti-fraud policies align with current regulatory standards and protect the entity's reputation. Clear reporting structures are essential for maintaining transparency and long-term operational stability.

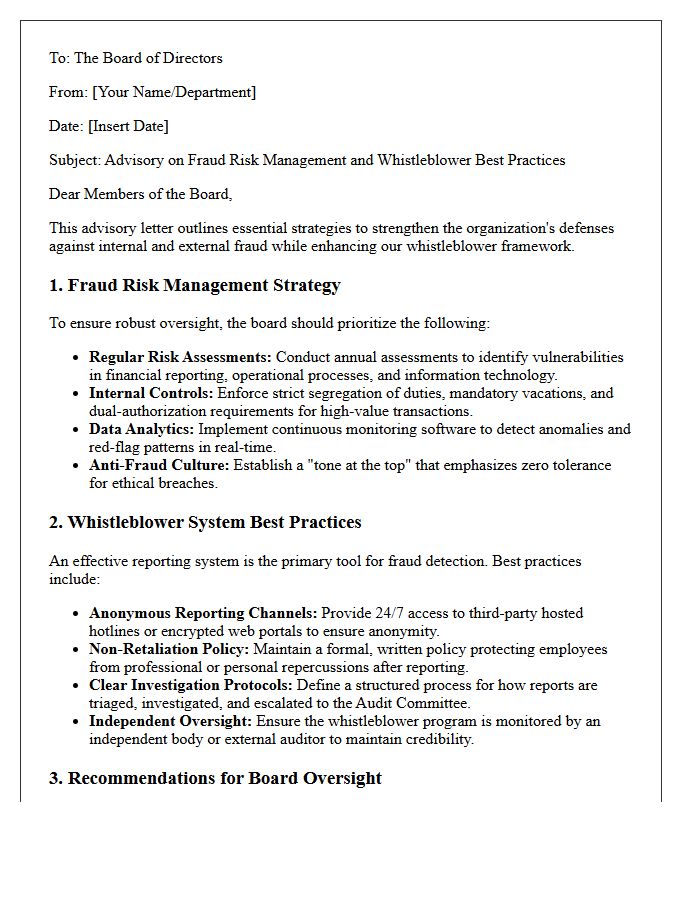

Board Advisory Letter on Fraud Risk Management and Whistleblower Best Practices

The Board Advisory Letter provides a strategic framework for governance, emphasizing that fraud risk management is a core fiduciary duty. It outlines critical protocols for oversight, urging boards to implement whistleblower best practices that ensure anonymity and legal protection. By fostering a transparent culture, organizations can detect internal threats early. Effective compliance monitoring and clear reporting lines are essential to mitigate financial loss and reputational damage. Boards must transition from reactive responses to proactive risk mitigation strategies to ensure long-term corporate integrity and operational resilience.

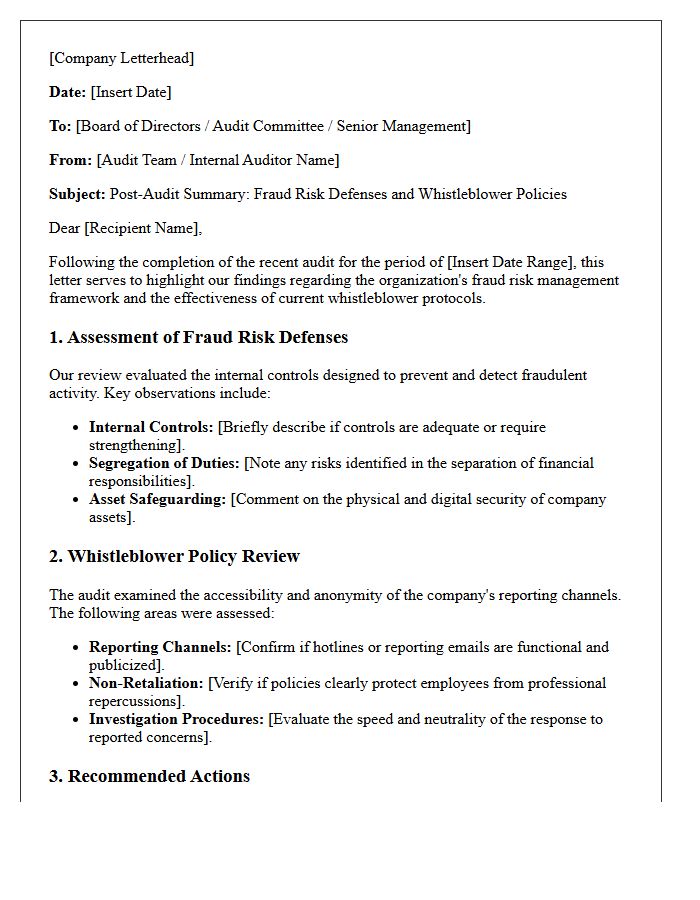

Post-Audit Letter Highlighting Fraud Risk Defenses and Whistleblower Policies

A post-audit letter serves as a critical governance tool to strengthen fraud risk defenses and internal controls. It identifies systemic vulnerabilities while mandating robust whistleblower policies to ensure ethical reporting channels. By addressing these findings, organizations enhance financial transparency and mitigate legal liabilities. Implementing these recommendations protects assets and fosters a culture of accountability. Reviewing this document is essential for stakeholders to understand remaining compliance gaps and the proactive measures required to prevent future occupational fraud or financial misstatements.

What is the primary purpose of a Management Letter regarding fraud risk management?

The Management Letter serves as a formal communication from auditors to senior leadership, identifying internal control weaknesses related to fraud prevention and providing actionable recommendations to strengthen the organization's fraud risk management framework.

How does a robust whistleblower policy mitigate organizational fraud risk?

A robust whistleblower policy mitigates risk by establishing a secure, confidential channel for employees to report irregularities, which acts as a powerful deterrent and ensures that potential fraudulent activities are detected and addressed at an early stage.

What are the essential components of an effective fraud risk management framework?

An effective framework must include a comprehensive fraud risk assessment, clear segregation of duties, ongoing monitoring of internal controls, a formal code of ethics, and a transparent investigation process for reported concerns.

Why is "tone at the top" emphasized in Management Letters concerning fraud?

Auditors emphasize the "tone at the top" because management's commitment to integrity and ethical behavior dictates the organizational culture; without visible support from leadership, whistleblower policies and fraud controls are often bypassed or ignored.

What common deficiencies do auditors find in whistleblower protection programs?

Common deficiencies include a lack of anonymous reporting options, insufficient protection against retaliation for whistleblowers, inadequate employee training on how to report concerns, and the absence of an independent oversight body to review reported cases.

Comments