Operational delays often stem from a fragmented month-end close process. This management letter identifies systemic inefficiencies, such as manual data entry and lack of standardization, that compromise financial accuracy. Addressing these bottlenecks is essential for timely reporting and strategic decision-making. To help streamline your internal controls and communication, below are some ready to use template.

Image cover: Streamlining Month-End Close: Management Letter Templates for Addressing Process Inefficiencies

Letter Samples List

- Management Letter on Month-End Close Process Inefficiencies

- Management Letter Regarding Lack of Automation in Close Procedures

- Management Letter Addressing Bank Reconciliation Delays During Month-End

- Management Letter Concerning Accounting Software Integration Failures

- Management Letter on Staff Allocation and Training Deficiencies

- Management Letter Highlighting Habitual Late Journal Entry Submissions

- Management Letter Regarding Interdepartmental Communication Bottlenecks

- Management Letter on Risks Associated With Manual Data Entry Overreliance

- Management Letter Addressing the Absence of Standardized Close Procedures

- Management Letter Concerning Inefficient Review and Approval Workflows

- Management Letter Highlighting Inaccurate Accrual and Deferral Tracking

- Management Letter on Inadequate Audit Trails During Month-End Close

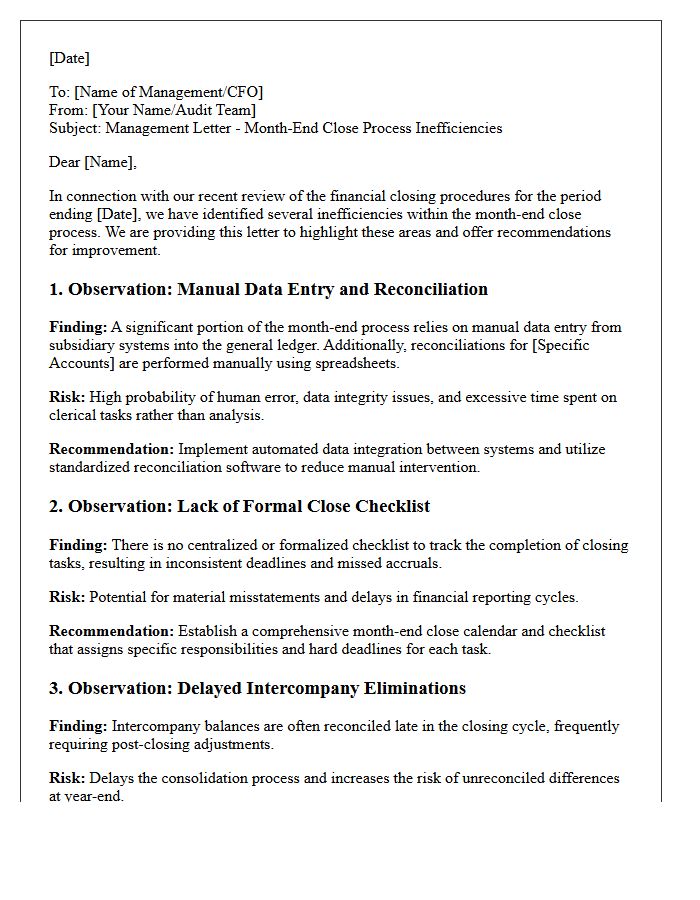

Management Letter on Month-End Close Process Inefficiencies

A management letter regarding month-end close process inefficiencies highlights critical operational gaps that delay financial reporting. It identifies redundant manual tasks, poor data integration, and a lack of standardized workflows. Addressing these weaknesses is essential for improving internal controls and ensuring data accuracy. By implementing automated reconciliations and clear task ownership, organizations can reduce the risk of material misstatements. This formal communication serves as a roadmap for leadership to streamline accounting cycles, enhance audit readiness, and provide timely financial insights for strategic decision-making.

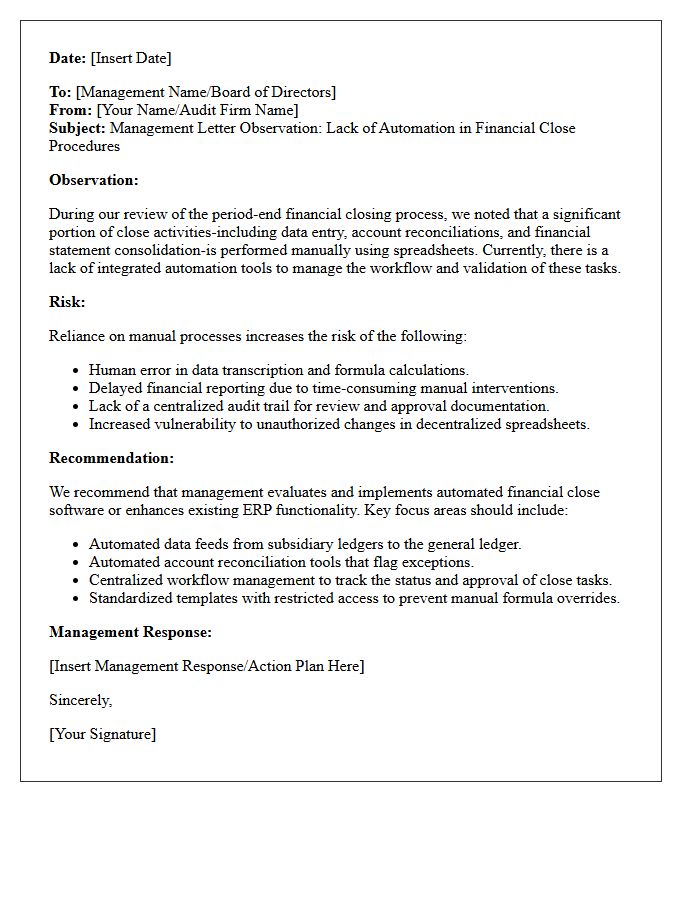

Management Letter Regarding Lack of Automation in Close Procedures

A management letter addressing a lack of automation in month-end close procedures highlights significant risks to financial reporting integrity. Manual processes are prone to human error, delays, and inefficiency, often leading to audit findings regarding internal control weaknesses. Implementing automated workflows and integrated systems enhances data accuracy and accelerates reporting timelines. Addressing these deficiencies is essential for scalability and reducing the operational burden on accounting teams, ensuring a more reliable audit trail and improved transparency for stakeholders and decision-makers throughout the organization.

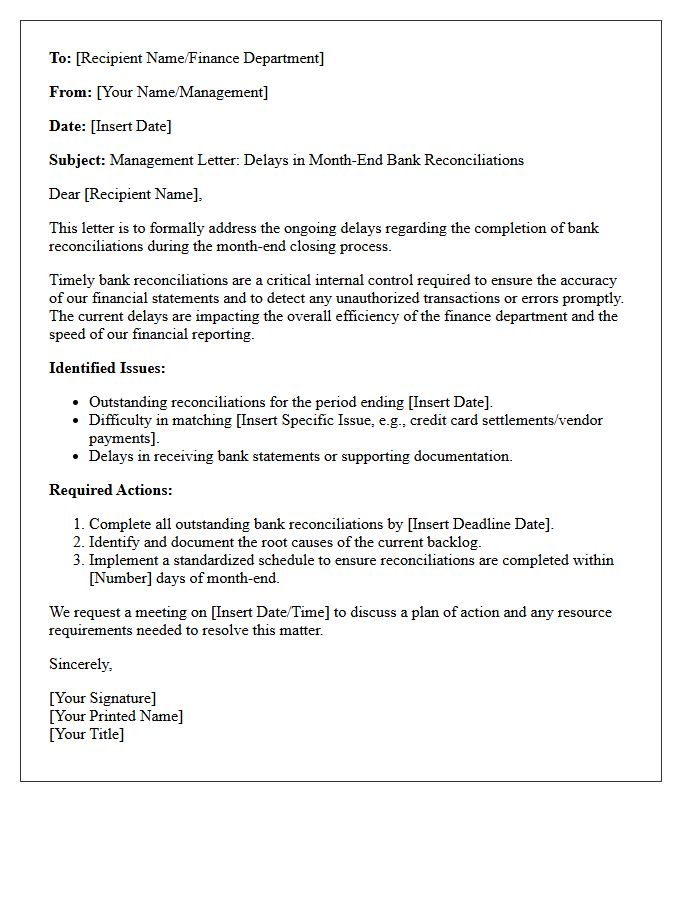

Management Letter Addressing Bank Reconciliation Delays During Month-End

Addressing bank reconciliation delays is critical for maintaining financial integrity. Persistent reporting lags during month-end procedures often indicate underlying weaknesses in internal controls or transaction processing. This formal management letter highlights the necessity of timely reconciliations to ensure accurate financial statements and prompt fraud detection. Implementing standardized workflows and automated tools can mitigate risks associated with unresolved discrepancies. Strengthening these oversight processes minimizes operational bottlenecks, ensures regulatory compliance, and provides stakeholders with reliable, real-time data for informed strategic decision-making and robust audit readiness.

Management Letter Concerning Accounting Software Integration Failures

A management letter addressing accounting software integration failures highlights critical risks to financial data integrity. These discrepancies often stem from API synchronization errors or incompatible data mapping between platforms. Such failures can lead to distorted financial reporting, internal control weaknesses, and increased operational costs. Management must prioritize reconciliation protocols and system audits to ensure seamless data flow. Addressing these integration gaps promptly is essential for maintaining audit readiness and making informed business decisions based on accurate, real-time financial insights across all connected organizational systems.

Management Letter on Staff Allocation and Training Deficiencies

A management letter serves as a formal communication highlighting critical internal control weaknesses regarding staff allocation and training. It identifies where insufficient staffing levels or skill gaps jeopardize operational efficiency and financial accuracy. By addressing these deficiencies, organizations can mitigate risks such as burnout, high turnover, and procedural errors. Implementing the auditor's recommendations ensures that personnel are strategically deployed and adequately trained, fostering a robust governance framework and long-term institutional stability. Effective resolution of these findings is essential for maintaining organizational integrity and achieving peak performance.

Management Letter Highlighting Habitual Late Journal Entry Submissions

A management letter addressing habitual late journal entry submissions highlights a significant internal control deficiency. Delayed entries compromise the accuracy and timeliness of financial reporting, increasing the risk of material misstatements. This recurring issue often signals inadequate staffing or inefficient closing processes. Auditors emphasize that consistent delays hinder effective oversight and prevent management from making informed decisions based on real-time data. To mitigate this risk, organizations must enforce strict reporting deadlines and implement automated workflows to ensure all financial records are updated promptly and reliably throughout the fiscal period.

Management Letter Regarding Interdepartmental Communication Bottlenecks

A management letter addressing interdepartmental communication bottlenecks identifies systemic delays that hinder operational efficiency. It highlights how fragmented information silos disrupt cross-functional workflows and delay decision-making. The document recommends implementing integrated software solutions and standardized reporting protocols to foster transparency. By streamlining internal dialogue, leadership can mitigate risks, improve resource allocation, and enhance overall productivity. Addressing these barriers is essential for maintaining organizational agility and ensuring that strategic objectives are met across all departments without unnecessary friction or costly administrative overlaps.

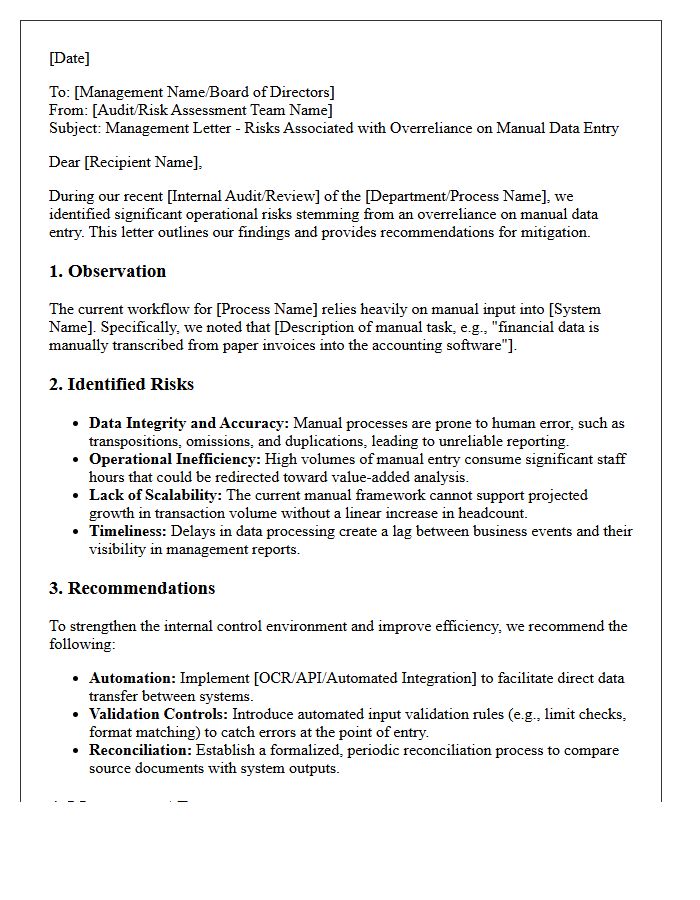

Management Letter on Risks Associated With Manual Data Entry Overreliance

Overreliance on manual data entry significantly increases operational risk and compromises financial integrity. A management letter highlights how human error leads to data inaccuracies, causing reporting delays and costly reconciliation efforts. Organizations must prioritize automation to mitigate these risks. Failure to implement automated validation controls exposes the firm to fraud and regulatory non-compliance. Strengthening internal systems by replacing manual processes with integrated software solutions ensures data reliability, enhances efficiency, and provides a more secure audit trail for critical business decision-making and long-term strategic planning.

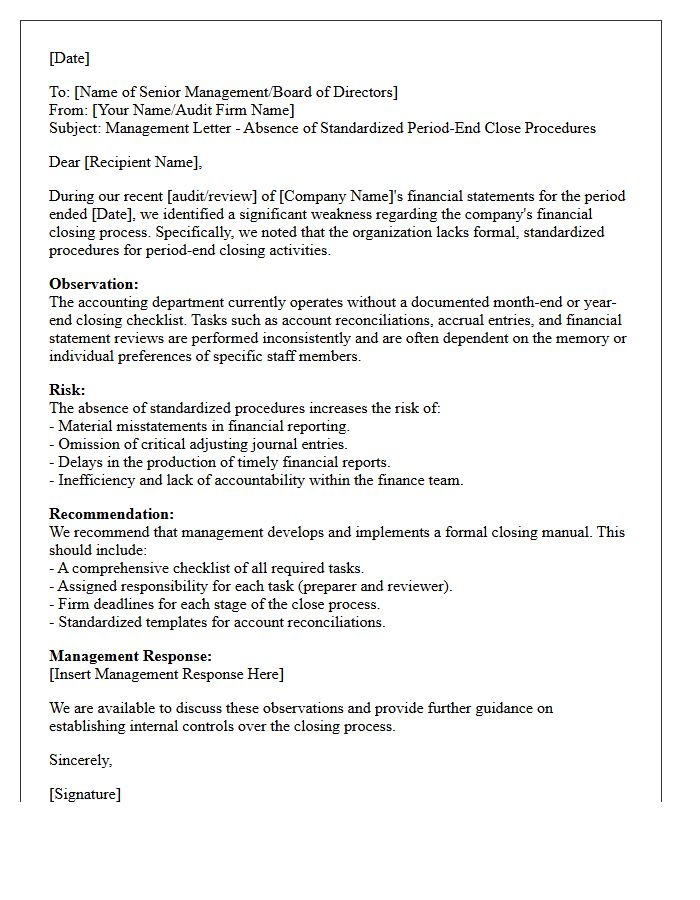

Management Letter Addressing the Absence of Standardized Close Procedures

A management letter addressing the absence of standardized close procedures highlights critical risks to financial reporting integrity. Without uniform workflows, organizations face inconsistent data, internal control weaknesses, and increased potential for material errors. Standardizing the month-end process ensures accountability, improves audit readiness, and enhances the reliability of financial statements. Implementing documented checklists and formal review steps mitigates operational silos and streamlines resource allocation. Addressing these deficiencies is essential for maintaining regulatory compliance and providing management with timely, accurate information for strategic decision-making and risk mitigation.

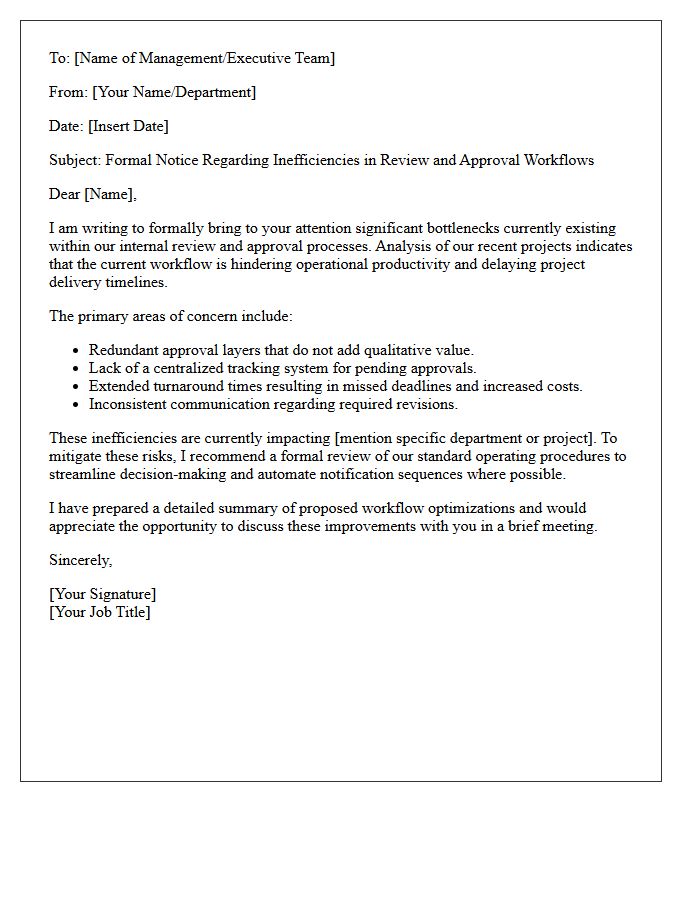

Management Letter Concerning Inefficient Review and Approval Workflows

A management letter addressing inefficient review and approval workflows highlights critical bottlenecks that delay operations and increase costs. These systemic weaknesses often stem from redundant authorization layers or lack of automated tracking, leading to potential financial misstatements. To mitigate risks, organizations must streamline decision-making paths and implement clear accountability standards. Enhancing these processes ensures operational efficiency and strengthens the internal control environment, ultimately protecting the integrity of financial reporting and resource allocation.

Management Letter Highlighting Inaccurate Accrual and Deferral Tracking

A management letter identifies significant control deficiencies, specifically targeting inaccurate accrual and deferral tracking. Mismanaging these period-end adjustments distorts financial statements, leading to incorrect profit reporting and tax compliance issues. Organizations must implement rigorous reconciliation processes to ensure expenses and revenues align with the correct accounting period. Strengthening internal controls over timing differences mitigates audit risks and prevents material misstatements. Consistent monitoring of cutoff procedures is essential for maintaining transparent, GAAP-compliant financial records and ensuring stakeholders receive reliable data for informed decision-making.

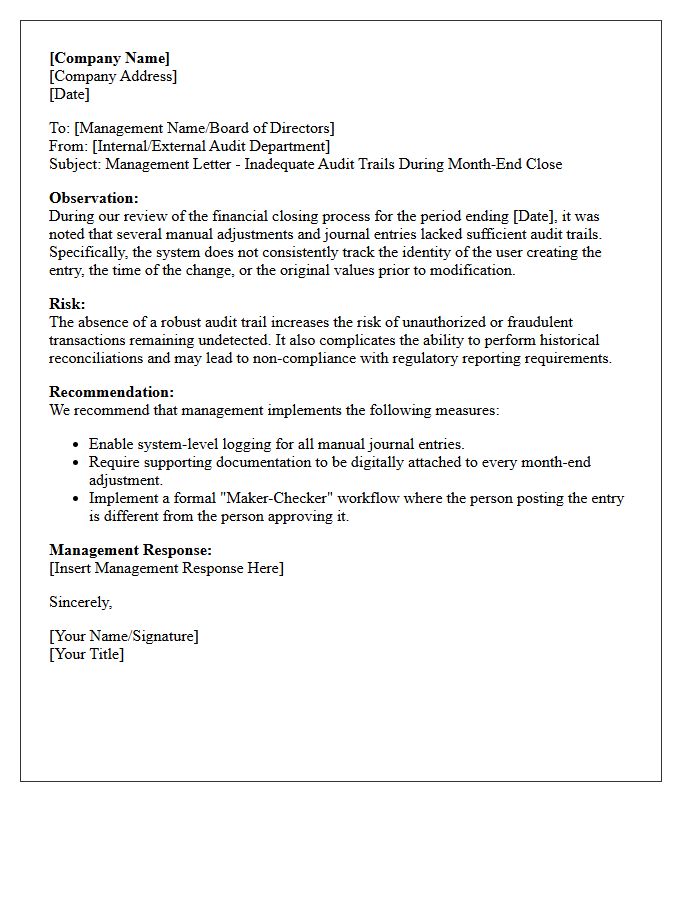

Management Letter on Inadequate Audit Trails During Month-End Close

A management letter addressing inadequate audit trails during month-end close warns of significant internal control weaknesses. Without detailed logs tracking journal entries and adjustments, organizations face increased risks of unauthorized transactions and financial misstatements. Establishing robust documentation ensures accountability and simplifies the verification of data integrity. Management must implement automated system tracking and formalized review processes to strengthen oversight. Resolving these gaps is essential for maintaining compliance, preventing fraud, and ensuring that financial reporting remains transparent and reliable for both internal stakeholders and external auditors.

What is a management letter regarding month-end close process inefficiencies?

A management letter is a formal document issued by internal or external auditors that identifies internal control weaknesses and operational inefficiencies discovered during the audit of the month-end close process, offering specific recommendations for improvement.

What are the most common causes of delays in the month-end close?

Delays are typically caused by manual data entry errors, lack of standardized checklists, late submission of intercompany reconciliations, and a heavy reliance on complex spreadsheets rather than automated accounting systems.

How does an inefficient month-end close impact financial reporting?

Inefficiencies can lead to increased risks of material misstatement, delayed financial insights for stakeholders, increased labor costs due to overtime, and a reactive rather than proactive approach to financial management.

What recommendations are typically found in a management letter for closing process optimization?

Common recommendations include implementing automated reconciliation tools, enforcing strict cut-off deadlines for sub-ledger entries, standardizing the chart of accounts, and establishing a centralized task management system to track progress.

How can management demonstrate remediation of close process inefficiencies?

Management can demonstrate remediation by updating Standard Operating Procedures (SOPs), reducing the number of days to close, decreasing the volume of post-closing adjustments, and providing documented evidence of timely review and approval cycles.

Comments