Effective corporate governance requires rigorous oversight of Related Party Transactions to ensure transparency and legal compliance. This article explores the essential disclosure requirements and audit standards necessary for maintaining financial integrity and preventing conflicts of interest. Learn how to draft a professional management letter that meets regulatory expectations. To help you get started, below are some ready to use template.

Image cover: Mastering Related Party Disclosures: Expert Management Letter Templates and Reporting Samples

Letter Samples List

- Management Letter Regarding Undisclosed Related Party Transactions

- Management Letter Concerning Incomplete Disclosures of Related Party Transactions

- Management Letter on Internal Control Deficiencies Over Related Party Transactions

- Management Letter Addressing the Absence of Formal Related Party Agreements

- Management Letter on Non-Compliance With Related Party Disclosure Frameworks

- Management Letter Regarding Unapproved Related Party Transactions

- Management Letter on Inaccurate Valuation of Related Party Transactions

- Management Letter Concerning Intercompany Balances and Related Party Disclosures

- Management Letter Addressing Transfer Pricing and Related Party Disclosures

- Management Letter on Material Weaknesses in Related Party Transaction Identification

- Management Letter Regarding Key Management Personnel Compensation Disclosures

- Management Letter on Board Approval Deficiencies for Related Party Transactions

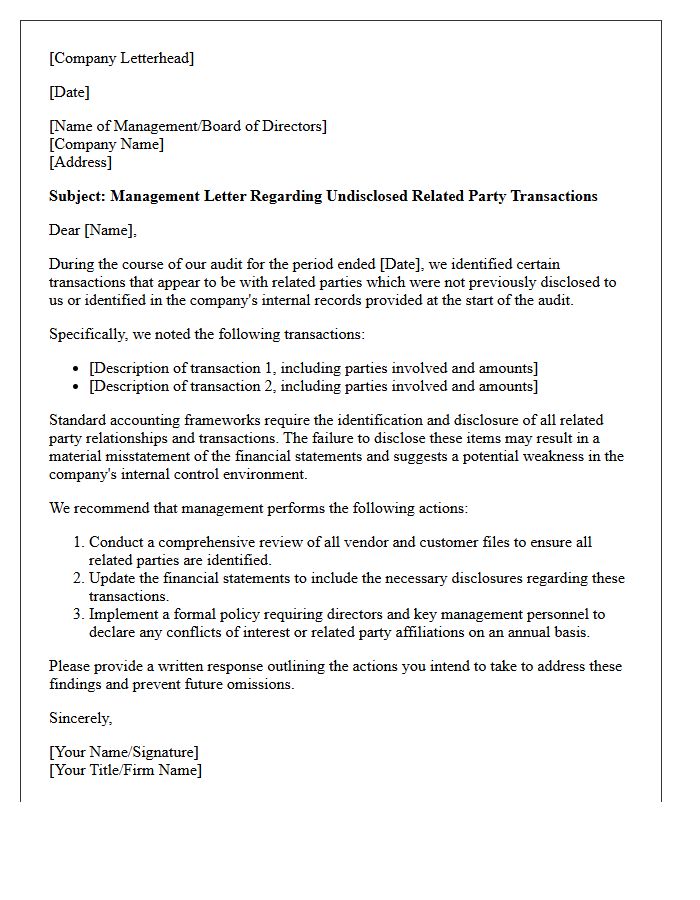

Management Letter Regarding Undisclosed Related Party Transactions

A management letter concerning undisclosed related party transactions serves as a formal notification of internal control deficiencies. Auditors issue this document when they identify hidden relationships or financial dealings between a company and its affiliates that were not properly reported. This communication is crucial because failing to disclose these conflicts of interest can significantly distort financial statements and mislead stakeholders. Management must address these findings by improving transparency and strengthening oversight to ensure all material transactions are accurately captured, authorized, and disclosed according to accounting standards to maintain corporate integrity.

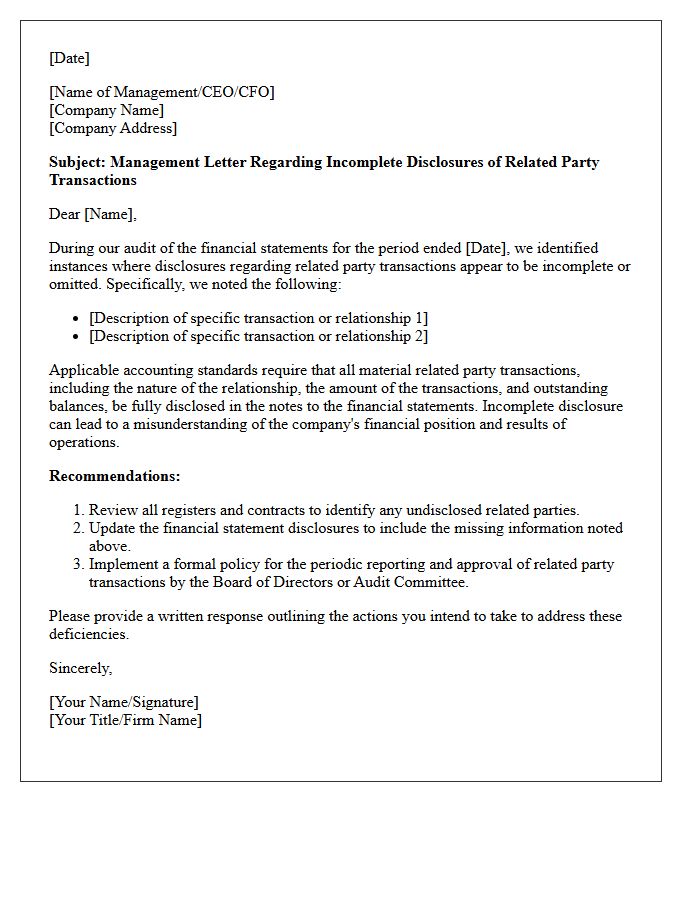

Management Letter Concerning Incomplete Disclosures of Related Party Transactions

A management letter addressing incomplete disclosures of related party transactions is a critical audit communication. It highlights failures to report financial dealings between a company and its insiders, such as executives or entities under shared control. These omissions increase the risk of fraud, material misstatement, and conflicts of interest. Auditors use this document to demand corrective actions, ensuring transparency and regulatory compliance. Accurate reporting is essential to provide investors with a true representation of financial health and to prevent hidden siphonage of corporate assets through undisclosed preferential agreements.

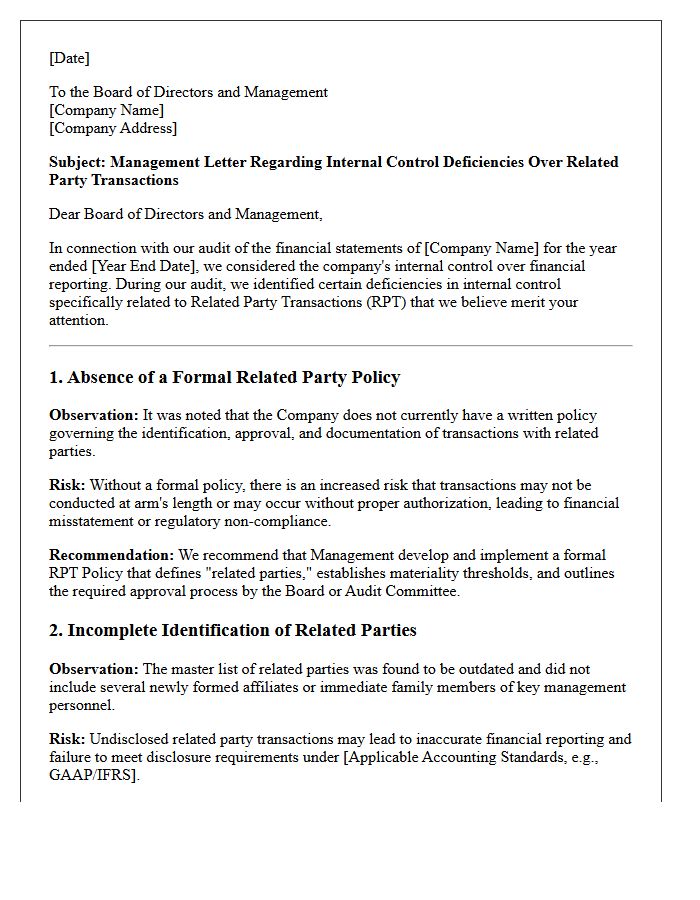

Management Letter on Internal Control Deficiencies Over Related Party Transactions

A management letter regarding related party transactions identifies material weaknesses or significant deficiencies in how a company monitors dealings with affiliates. It highlights the risk of undisclosed conflicts of interest and potential financial misstatements. Auditors issue these findings to recommend stronger oversight and internal controls, ensuring all transactions are conducted at arm's length. Proper documentation and transparent disclosure are essential to maintain regulatory compliance, protect shareholder interests, and prevent fraudulent activity within the organization's reporting framework.

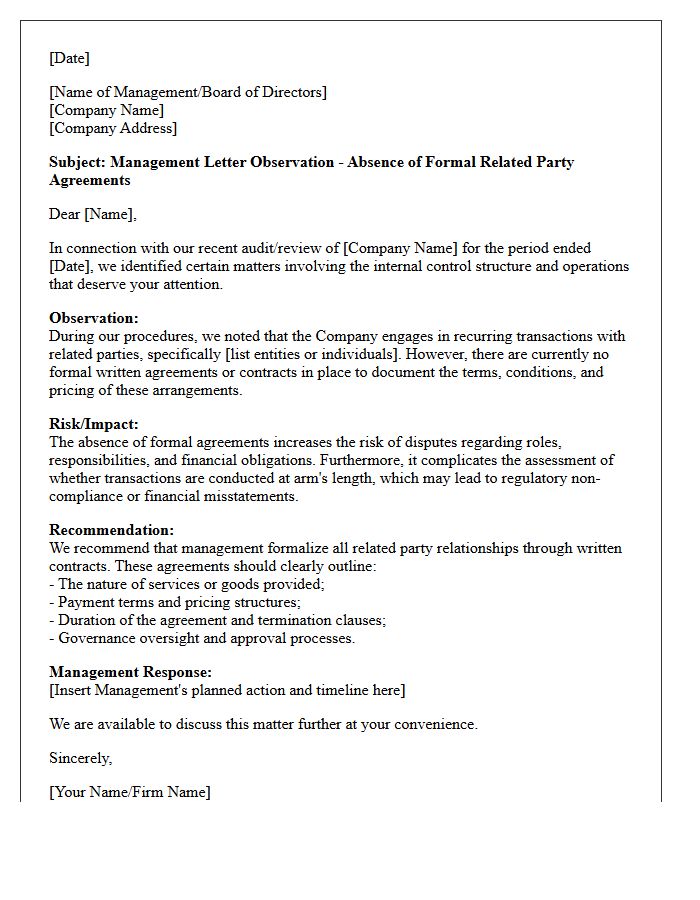

Management Letter Addressing the Absence of Formal Related Party Agreements

A management letter concerning the absence of formal related party agreements highlights a critical internal control deficiency. Without written contracts, organizations face significant risks regarding the valuation, terms, and legal enforceability of intercompany transactions. Auditors issue these findings to ensure management documents all arm's length dealings to prevent financial misstatements or conflicts of interest. Establishing formal documentation is essential for maintaining regulatory compliance, ensuring transparent financial reporting, and protecting the interests of all stakeholders involved in related party activities.

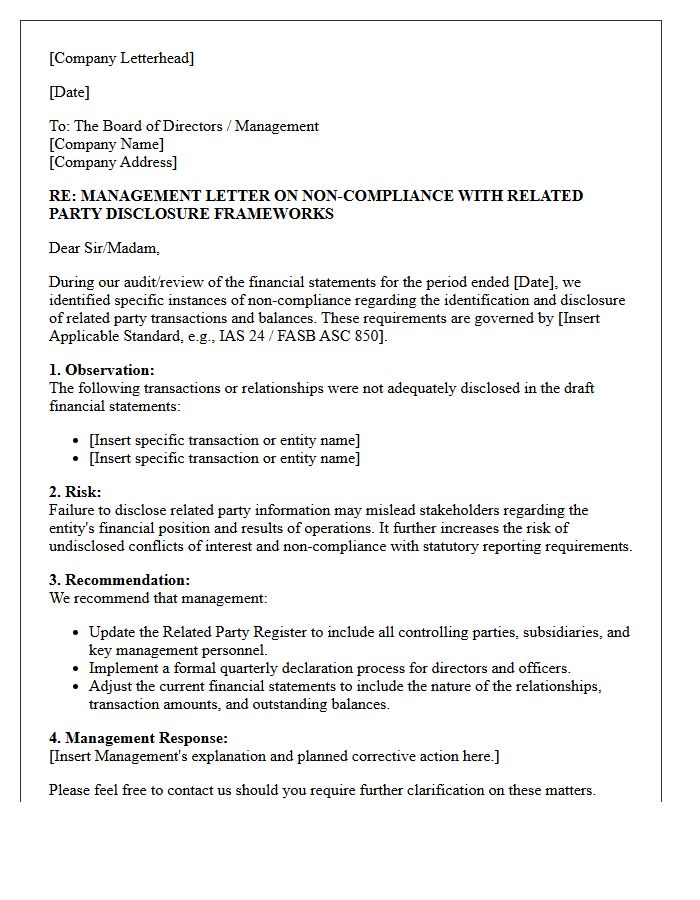

Management Letter on Non-Compliance With Related Party Disclosure Frameworks

A management letter regarding non-compliance with related party disclosure frameworks alerts leadership to failures in reporting transactions with affiliated entities. These omissions create significant audit risks and may violate statutory financial standards. Ensuring transparency is vital for maintaining stakeholder trust and preventing conflicts of interest. Auditors use these letters to recommend immediate remediation steps, such as improving internal controls and data tracking. Addressing these deficiencies is essential to avoid qualified audit opinions, legal penalties, and potential financial misstatements that undermine the integrity of an organization's financial reporting.

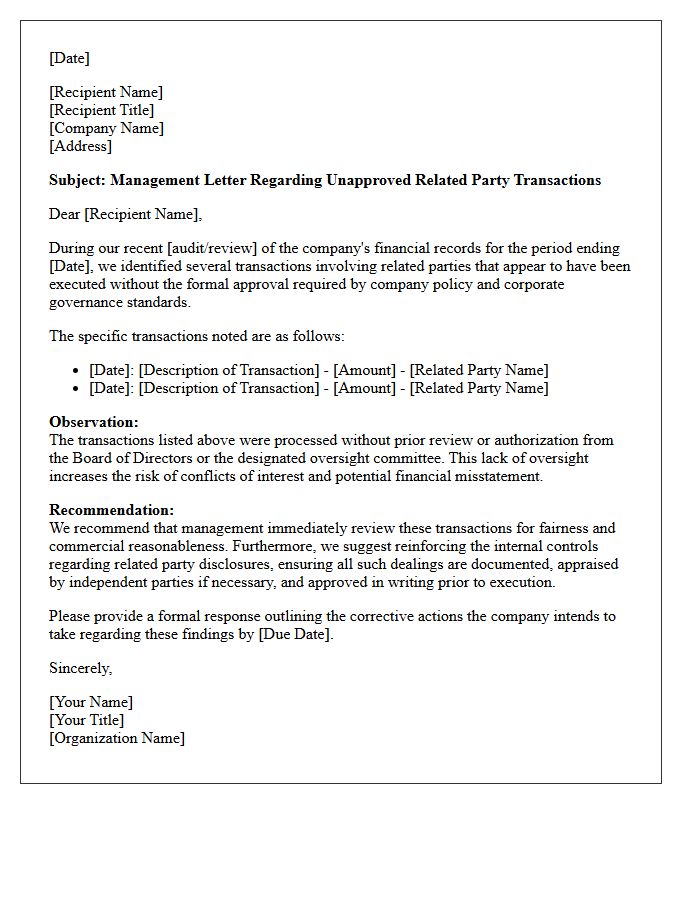

Management Letter Regarding Unapproved Related Party Transactions

A management letter concerning unapproved related party transactions alerts leadership to potential conflicts of interest and internal control weaknesses. It highlights transactions with affiliates or insiders that lacked formal board authorization, posing risks to financial integrity. To ensure regulatory compliance and transparency, companies must implement rigorous monitoring systems. Addressing these findings is essential to prevent fraud, protect shareholder value, and maintain corporate governance standards. Prompt corrective action mitigates legal exposure and strengthens the overall reliability of financial reporting frameworks.

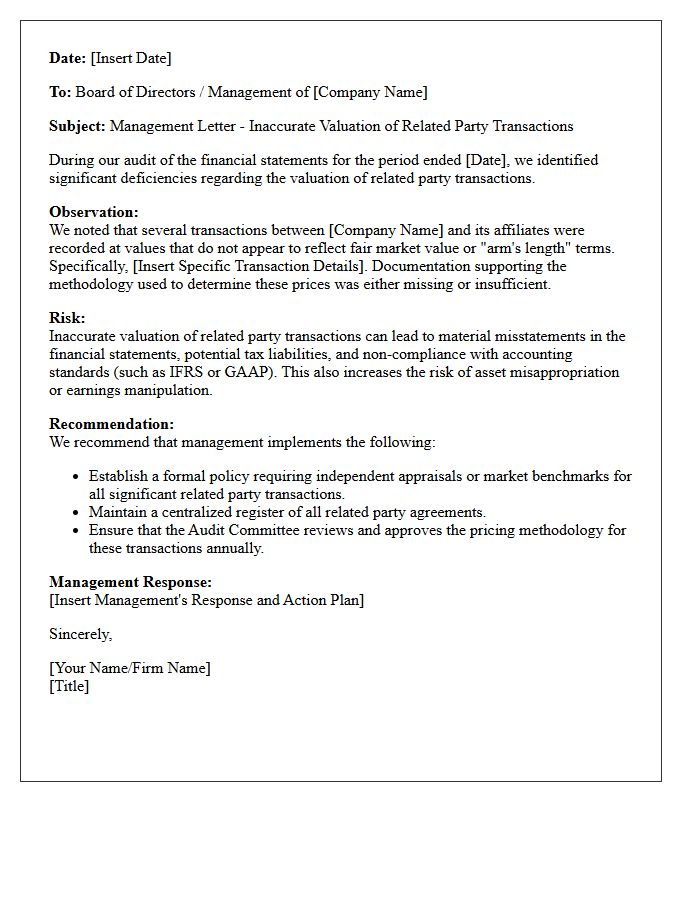

Management Letter on Inaccurate Valuation of Related Party Transactions

A management letter addressing the inaccurate valuation of related party transactions alerts leadership to significant financial reporting risks. These findings often highlight a lack of independent appraisal or objective benchmarks, which can lead to material misstatements. Ensuring these dealings occur at arm's length is essential for regulatory compliance and shareholder transparency. Auditors use this document to recommend stronger internal controls and fair value documentation. Addressing these discrepancies promptly prevents potential legal issues, tax penalties, and preserves the integrity of the company's financial health and corporate governance standards.

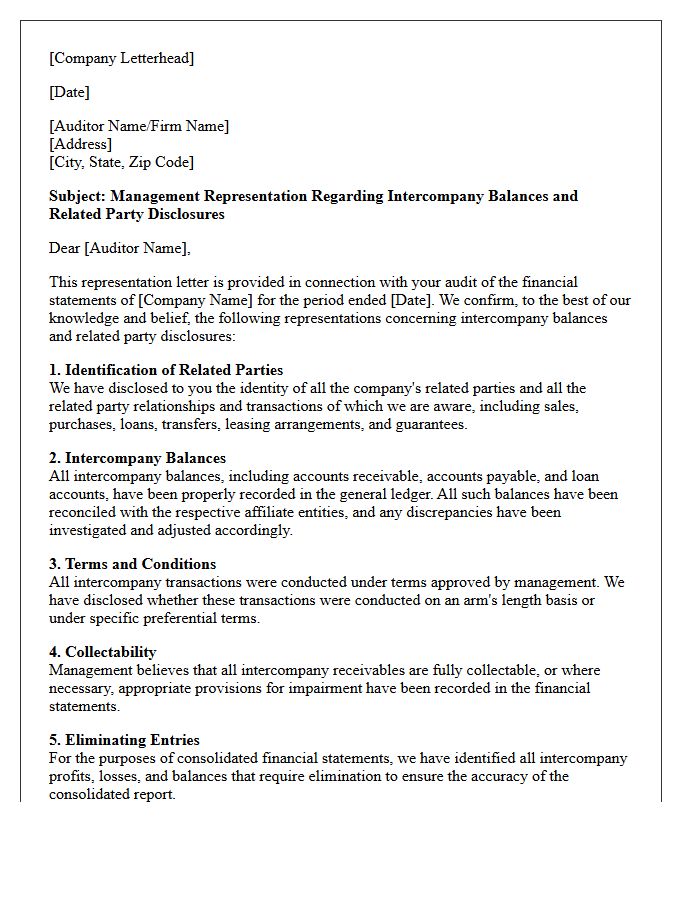

Management Letter Concerning Intercompany Balances and Related Party Disclosures

A management letter regarding intercompany balances and related party disclosures ensures financial transparency and internal control integrity. It highlights the necessity of reconciling reciprocal accounts to eliminate reporting discrepancies. Accurate related party disclosures are critical for stakeholders to evaluate potential conflicts of interest and the substance of transactions. This document identifies control weaknesses, such as inadequate documentation or valuation issues, that could misrepresent the entity's consolidated position. Proper management oversight of these balances mitigates audit risks and ensures compliance with accounting standards, reflecting a true and fair view of the organization's financial health.

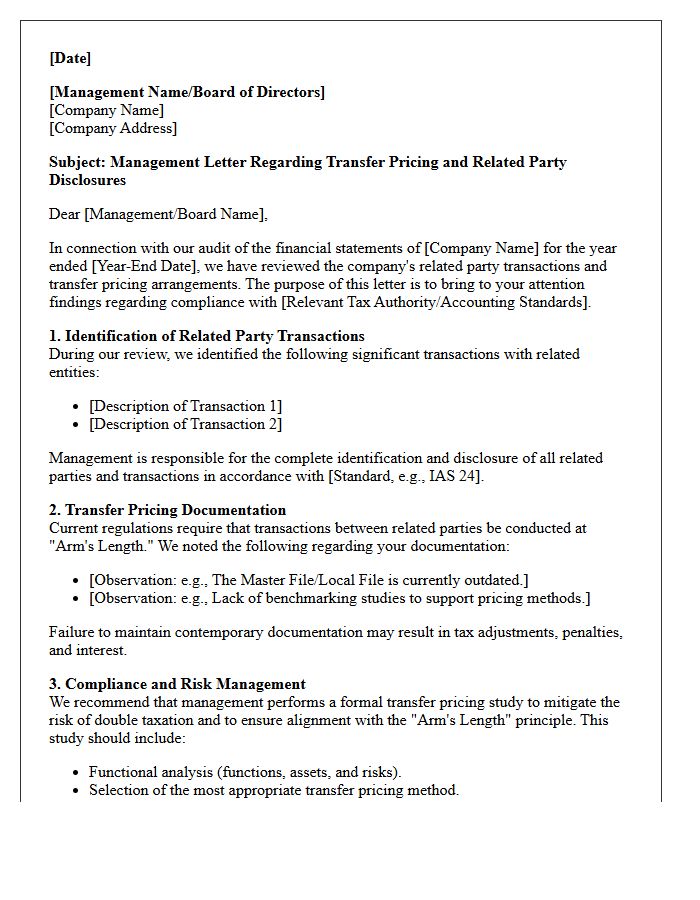

Management Letter Addressing Transfer Pricing and Related Party Disclosures

A management letter concerning transfer pricing ensures that intercompany transactions reflect arm's length pricing to mitigate tax risks. Auditors use these documents to verify that related party disclosures are transparent and compliant with financial reporting standards. Proper documentation prevents tax adjustments, penalties, and ensures that cross-border dealings do not distort the entity's financial position. Highlighting internal controls over these transactions is essential for maintaining regulatory compliance and providing stakeholders with a clear view of economic substance within corporate structures.

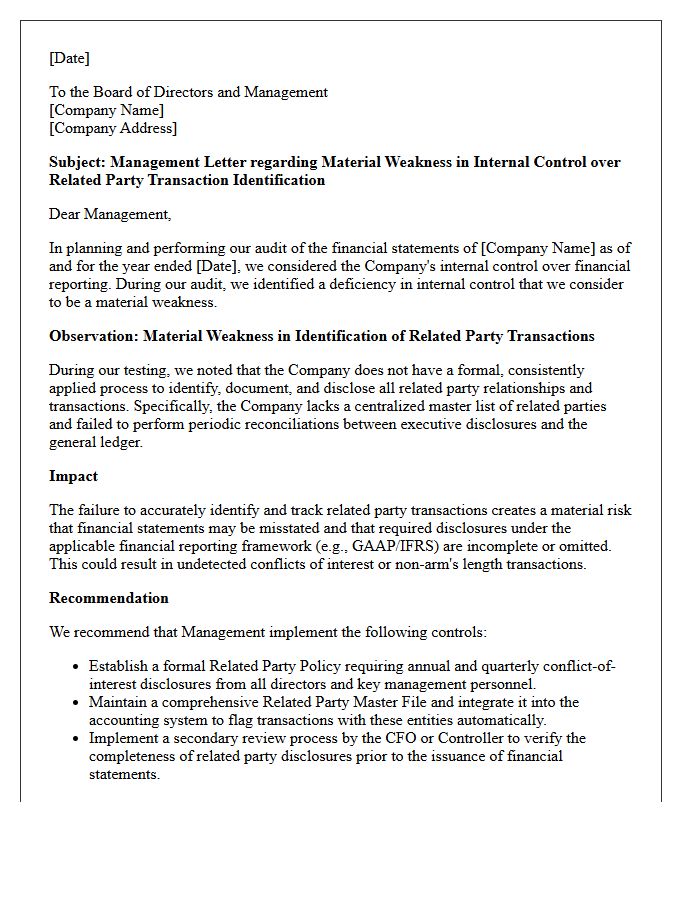

Management Letter on Material Weaknesses in Related Party Transaction Identification

A management letter serves as a formal communication from auditors highlighting internal control failures. When an organization exhibits material weaknesses in identifying related party transactions, it poses a significant risk to financial integrity. These gaps often result from inadequate disclosure protocols and poor monitoring of executive affiliations. Addressing these deficiencies is essential to prevent conflicts of interest and potential fraud. Strengthening oversight mechanisms ensures compliance with accounting standards, improves financial reporting accuracy, and maintains stakeholder trust by ensuring all significant intercompany dealings are transparently reported and properly evaluated.

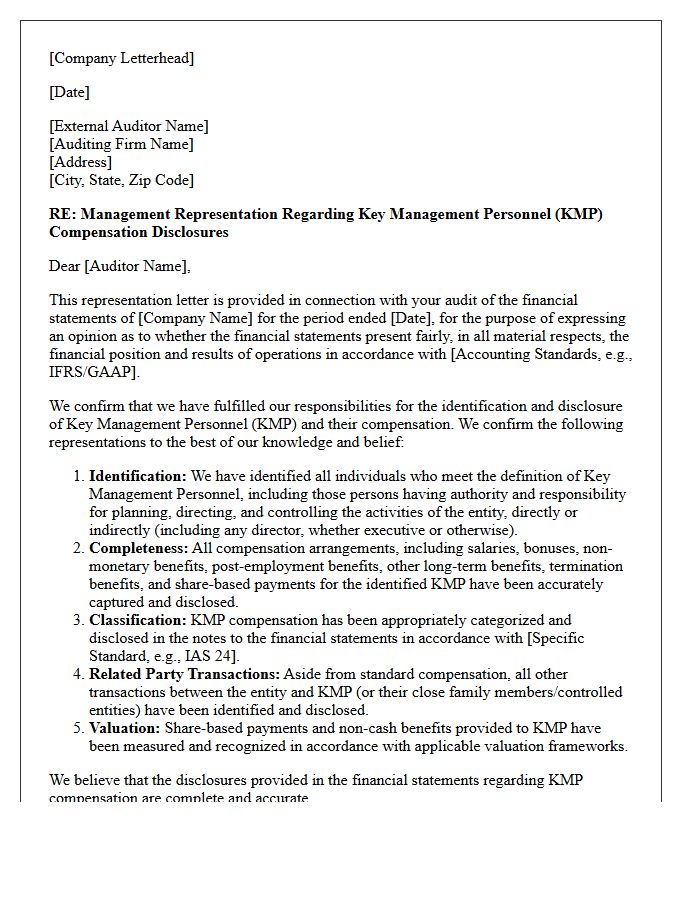

Management Letter Regarding Key Management Personnel Compensation Disclosures

A management letter concerning Key Management Personnel (KMP) compensation is vital for ensuring transparency and financial integrity. It confirms that all salaries, bonuses, and benefits paid to executive leadership are accurately recorded and compliant with reporting standards. These disclosures are essential for stakeholders to assess organizational governance and potential conflicts of interest. Auditors use this formal communication to verify that remuneration align with regulatory requirements, providing assurance that the board's financial decisions regarding top-tier management are fully documented and ethically sound within the annual financial report.

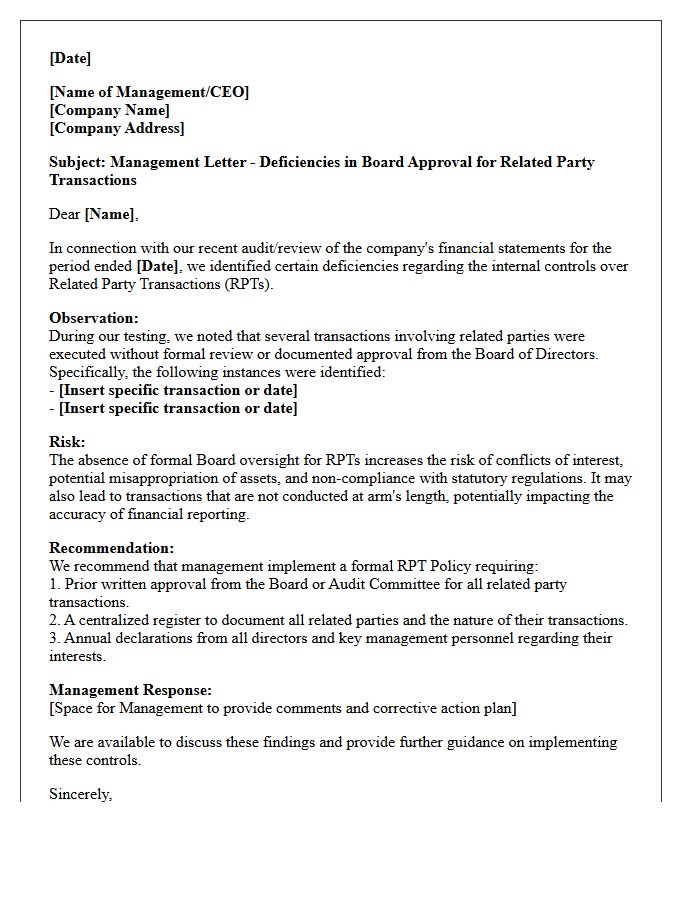

Management Letter on Board Approval Deficiencies for Related Party Transactions

A management letter addressing Board Approval Deficiencies highlights critical failures in the oversight of Related Party Transactions (RPTs). It alerts leadership that transactions with insiders occurred without formal authorization, increasing risks of conflicts of interest and financial misstatement. To ensure regulatory compliance and robust corporate governance, the board must implement rigorous review protocols and document all approvals in meeting minutes. Remedying these weaknesses is essential to protect shareholder interests and maintain the integrity of financial reporting processes.

What is a Management Letter regarding related party transactions?

A Management Letter is a formal communication issued by auditors to entity management that identifies internal control weaknesses and provides recommendations for improving the identification, authorization, and disclosure of transactions with related parties.

What are the primary disclosure requirements for related party transactions under accounting standards?

Entities must disclose the nature of the relationship, a description of the transactions, the dollar amounts involved, outstanding balances, and any terms or conditions to ensure financial statements provide a true and fair view of the entity's financial position.

How does a Management Letter address the completeness of related party disclosures?

The letter evaluates whether management has implemented robust systems to capture all affiliate dealings and highlights any omissions where transactions were not properly recorded or disclosed in accordance with framework requirements like ASC 850 or IAS 24.

What internal control recommendations are typically found in a Management Letter for related parties?

Auditors often recommend maintaining a central registry of related parties, implementing formal conflict-of-interest policies, and requiring board-level approval for significant non-routine transactions to mitigate the risk of self-dealing.

Why is the "arm's length" principle significant in Management Letter reporting?

The Management Letter often flags instances where related party transactions were not conducted at arm's length, as these require specific disclosure to prevent users of financial statements from being misled about the entity's independent operating performance.

Comments