Ensuring financial integrity in legal practice requires rigorous oversight. This guide explores essential Trust Account Reconciliation Practices to mitigate risks, maintain compliance with bar association standards, and safeguard client funds through meticulous internal controls. Effective management oversight prevents accounting errors and potential disciplinary actions. To help your firm implement these professional standards efficiently, below are some ready to use template.

Image cover: Strengthening Financial Integrity: Law Firm Trust Account Reconciliation Templates and Best Practices

Letter Samples List

- Management Letter on General Trust Account Reconciliation Practices

- Management Letter Regarding Unreconciled Client Trust Balances

- Management Letter on Segregation of Duties in Trust Accounting

- Management Letter Highlighting Trust Account Overdraft Risks

- Management Letter on Three-Way Reconciliation Deficiencies

- Management Letter Detailing Stale Dated Checks in Trust Accounts

- Management Letter on Commingling of Law Firm and Client Funds

- Management Letter Regarding Untimely Trust Account Bank Reconciliations

- Management Letter on Inadequate Trust Ledger Documentation

- Management Letter Addressing Electronic Fund Transfer Controls in Trust Accounts

- Management Letter on IOLTA Compliance and Interest Remittance Deficiencies

- Management Letter Noting Lack of Partner Oversight in Trust Reconciliation

- Management Letter Identifying Undistributed Trust Funds for Closed Matters

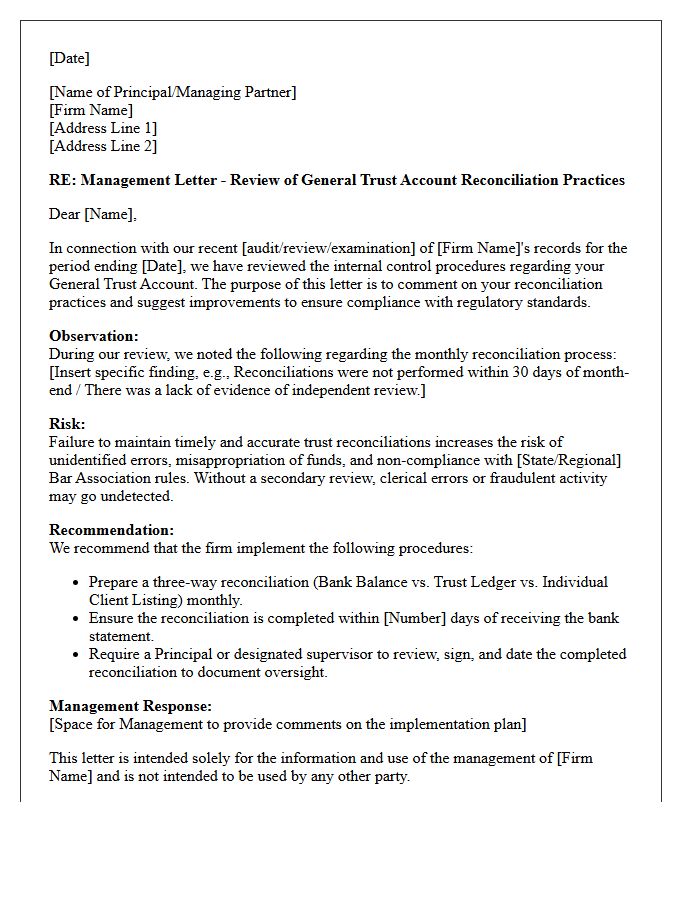

Management Letter on General Trust Account Reconciliation Practices

A management letter regarding general trust account reconciliation is a critical audit document highlighting internal control weaknesses. It identifies discrepancies between bank statements, ledgers, and individual client records. Ensuring fiduciary compliance is essential to prevent the commingling of funds and financial errors. Organizations must implement regular, documented reviews to mitigate risks of fraud or regulatory non-compliance. Addressing these recommendations promptly strengthens financial integrity and protects client assets, serving as a roadmap for improving accounting transparency and operational oversight within the firm's legal or financial framework.

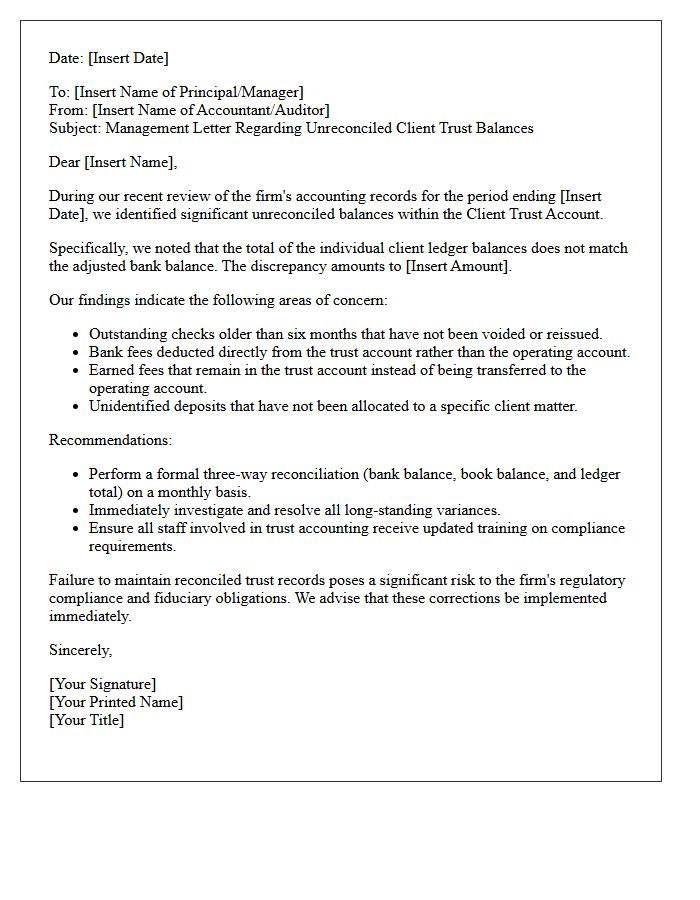

Management Letter Regarding Unreconciled Client Trust Balances

A management letter regarding unreconciled client trust balances is a critical formal notice highlighting internal control deficiencies. It warns that discrepancies between bank statements and sub-ledger records pose significant fiduciary risks and legal liabilities. Failure to resolve these variances can lead to accusations of commingling funds or misappropriation. To ensure compliance with professional standards, firms must implement immediate reconciliation procedures and robust oversight. Addressing these issues promptly is essential to protect client assets, maintain professional licensure, and ensure the financial integrity of the organization's trust accounting practices.

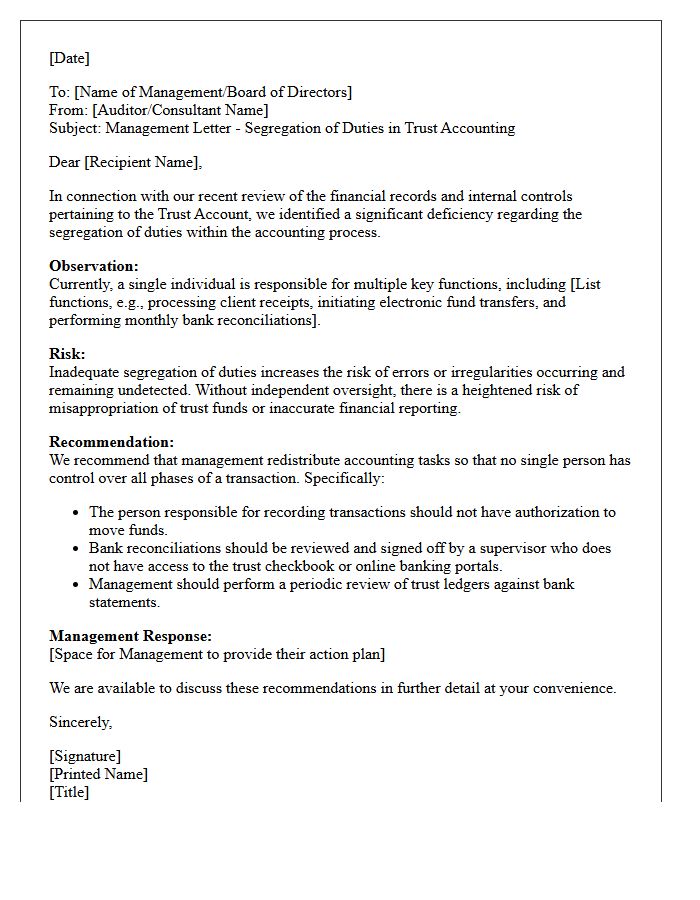

Management Letter on Segregation of Duties in Trust Accounting

A Management Letter serves as a formal communication identifying internal control deficiencies within trust accounting. The most critical observation often highlights a lack of segregation of duties, which occurs when a single individual handles authorization, recording, and custody of trust assets. This structural weakness significantly increases the risk of undetected errors or misappropriation of funds. Implementing independent reviews and dividing financial responsibilities are essential recommendations to ensure regulatory compliance, maintain fiduciary integrity, and protect client interests through robust oversight mechanisms.

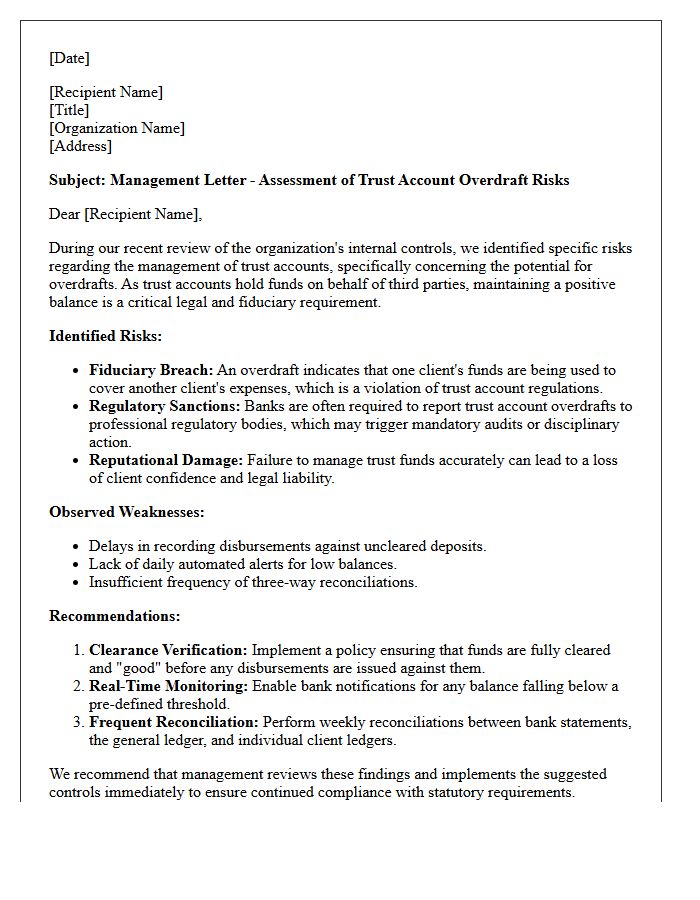

Management Letter Highlighting Trust Account Overdraft Risks

A management letter serves as a critical advisory tool for identifying Trust Account Overdraft Risks. To maintain financial integrity, firms must implement stringent oversight to prevent the misappropriation of client funds. Frequent causes include timing discrepancies, uncollected deposits, and administrative errors. Addressing these weaknesses through reconciliation protocols and internal controls is essential for regulatory compliance. Failure to mitigate these risks can lead to severe legal sanctions and loss of professional licensure. Proactive monitoring ensures that fiduciary duties are met while protecting the organization's reputation and long-term operational stability.

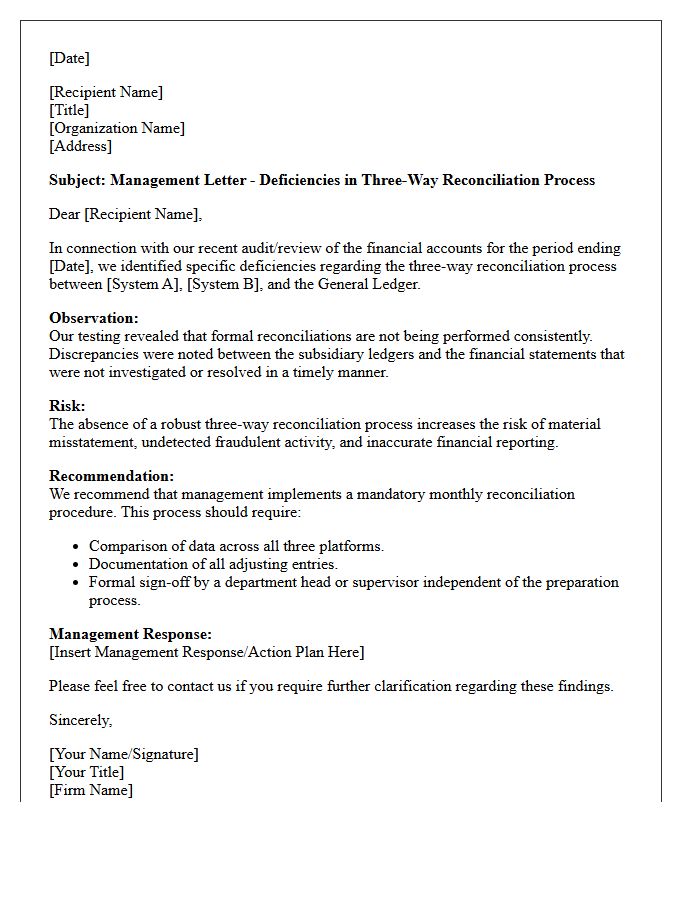

Management Letter on Three-Way Reconciliation Deficiencies

A management letter regarding three-way reconciliation deficiencies alerts leadership to critical gaps between bank statements, book balances, and individual ledger records. These internal control weaknesses increase the risk of undetected fraud, embezzlement, or accounting errors. Addressing these findings is essential to ensure financial accuracy and regulatory compliance. Organizations must implement timely corrective actions, such as formalizing review processes and enhancing documentation standards, to mitigate financial risks and strengthen overall oversight. Timely resolution of these identified discrepancies protects the entity's fiscal integrity and prevents significant year-end reporting issues.

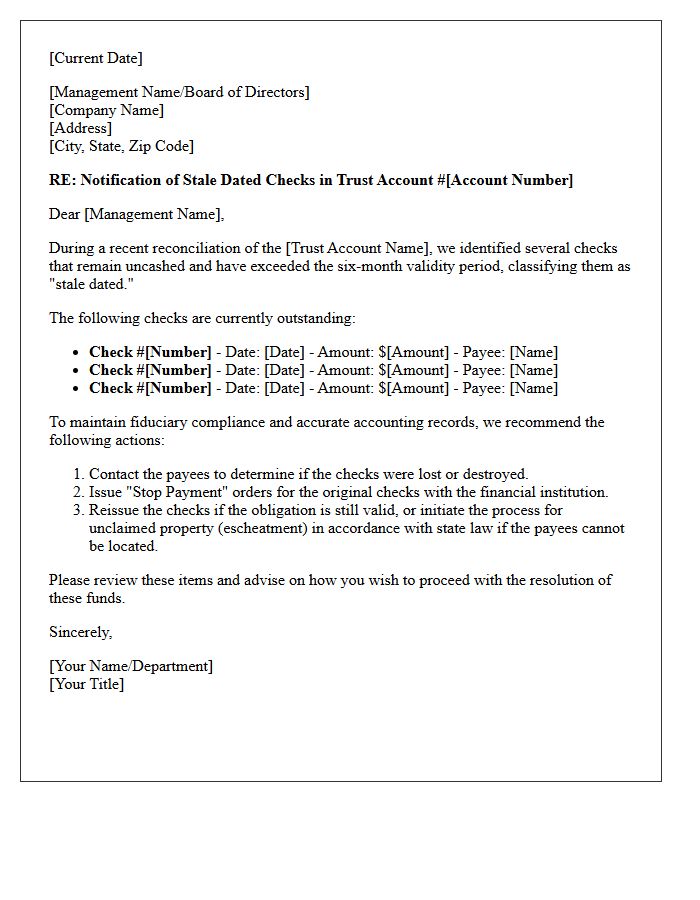

Management Letter Detailing Stale Dated Checks in Trust Accounts

A management letter regarding stale-dated checks in trust accounts is a critical compliance document. It identifies uncashed disbursements that have remained outstanding beyond a specific period, typically six months. These items pose significant fiduciary risks and audit concerns if left unresolved. To maintain accurate records, firms must perform regular bank reconciliations and follow escheatment laws to remit unclaimed funds to the state. Promptly investigating these checks prevents mismanagement of client funds and ensures the integrity of the legal or financial trust account remains intact and legally compliant.

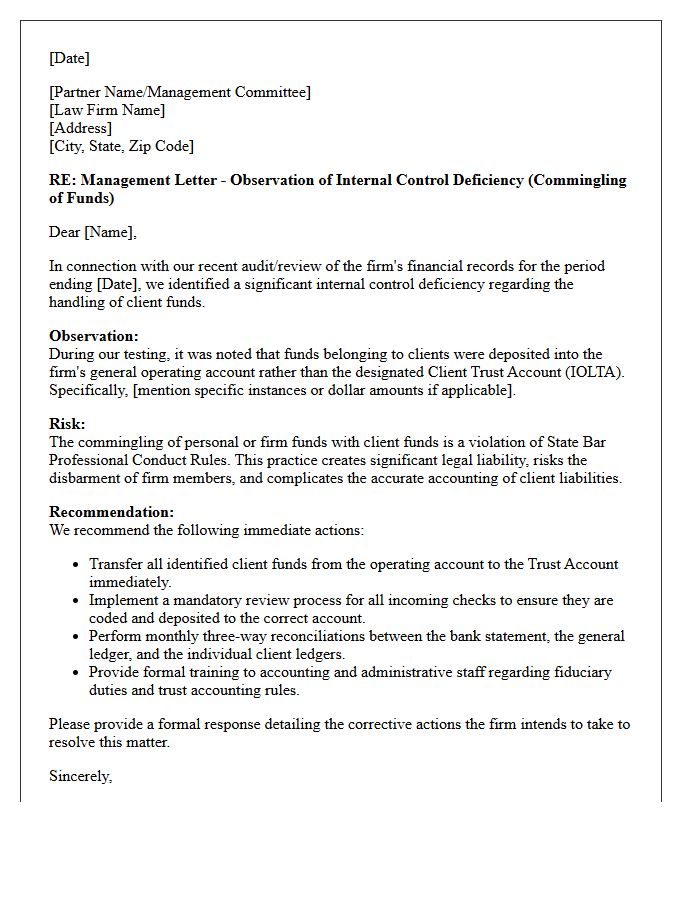

Management Letter on Commingling of Law Firm and Client Funds

A management letter regarding the commingling of funds serves as a critical warning for legal practices. It highlights the severe risks of mixing firm operating capital with client trust accounts. Maintaining strict separation is a core fiduciary duty required by bar associations to prevent ethical violations. The letter outlines necessary internal controls to ensure all settlements and retainers remain isolated, protecting the firm from disbarment or legal liability. Proper accounting protocols documented in this letter are essential for maintaining financial transparency and professional compliance within any law firm.

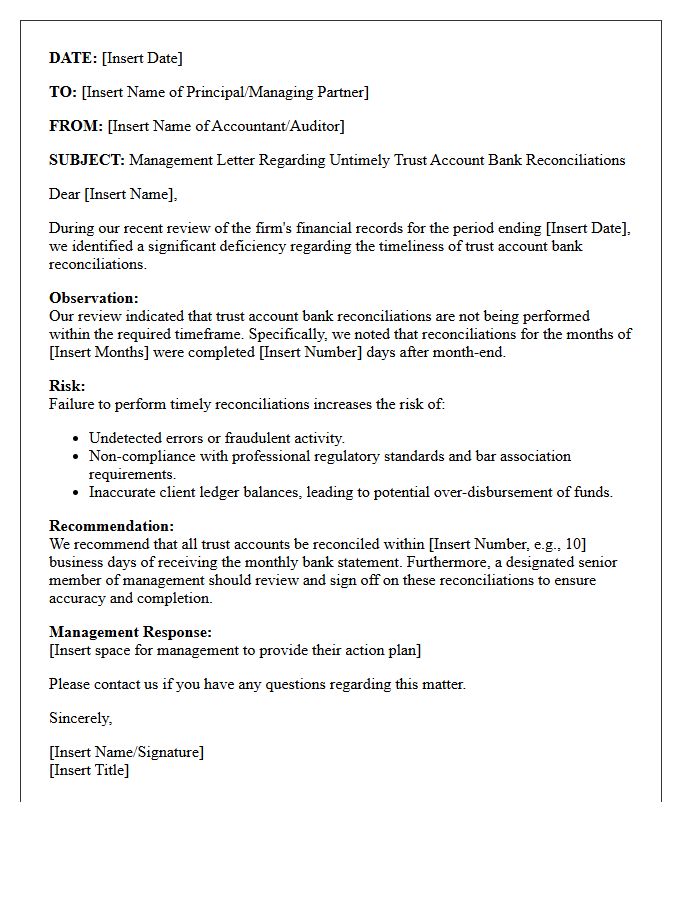

Management Letter Regarding Untimely Trust Account Bank Reconciliations

A management letter addressing untimely trust account bank reconciliations serves as a critical warning regarding fiduciary non-compliance. Regulatory standards require monthly reconciliations to ensure client funds are accurately safeguarded and to detect fraud or accounting errors immediately. Failing to perform these checks promptly creates significant financial risk and potential legal liability for the firm. Implementing a consistent oversight process is essential to maintain professional integrity, satisfy audit requirements, and protect the sanctity of the trust account from preventable mismanagement or misappropriation.

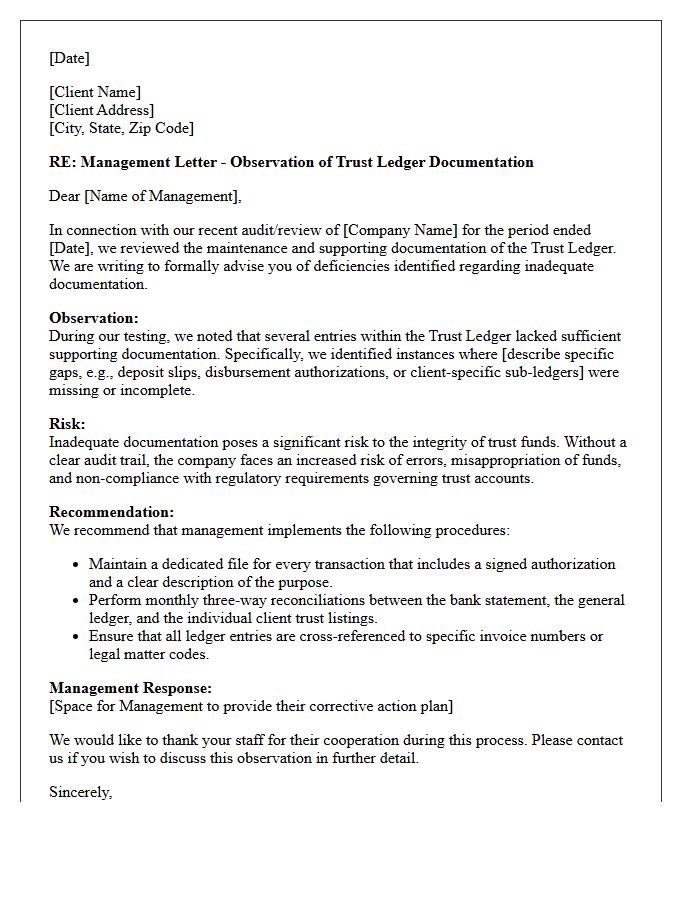

Management Letter on Inadequate Trust Ledger Documentation

A management letter regarding inadequate trust ledger documentation serves as a critical warning about systemic record-keeping failures. It highlights that the entity has failed to maintain detailed, reconciled records for client funds, creating significant risks of misappropriation or regulatory non-compliance. Auditors issue this notice to demand immediate corrective action, ensuring every transaction is transparent and traceable. Proper documentation is essential to safeguard fiduciary assets and maintain professional accountability. Addressing these deficiencies promptly is vital to prevent legal penalties and ensure the integrity of financial reporting within the organization.

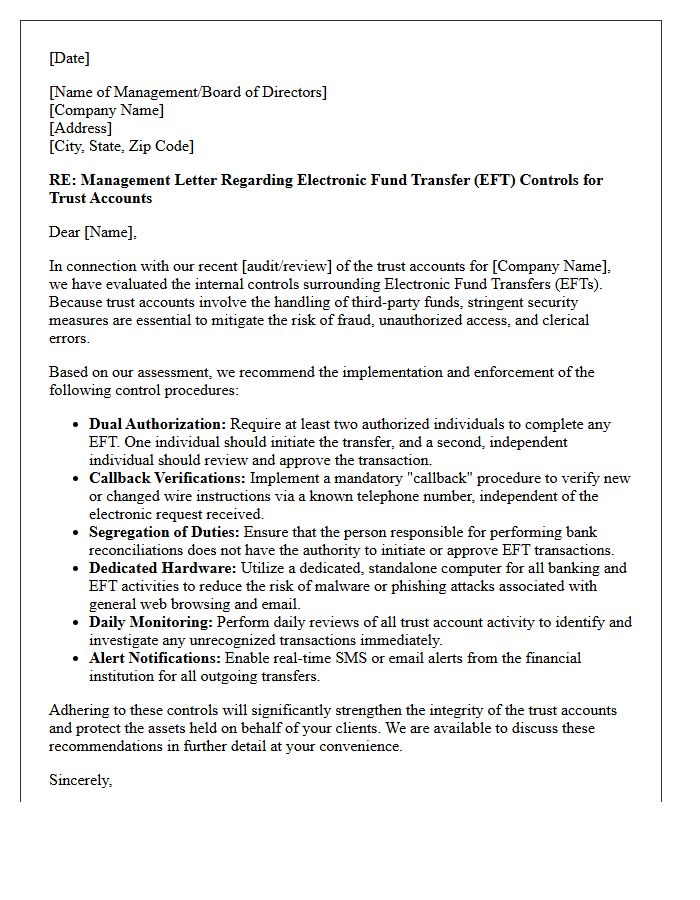

Management Letter Addressing Electronic Fund Transfer Controls in Trust Accounts

A management letter concerning trust accounts must prioritize Electronic Fund Transfer (EFT) controls to prevent unauthorized disbursements. Auditors evaluate the segregation of duties to ensure that no single individual can initiate and approve transfers. Strengthening multi-factor authentication and dual-authorization protocols is essential for mitigating fraud risks. Clear audit trails and regular reconciliations provide oversight, ensuring fiduciary responsibilities are met. Implementing robust internal controls protects client assets from cyber threats, maintaining the integrity of sensitive financial data within legal and professional standards.

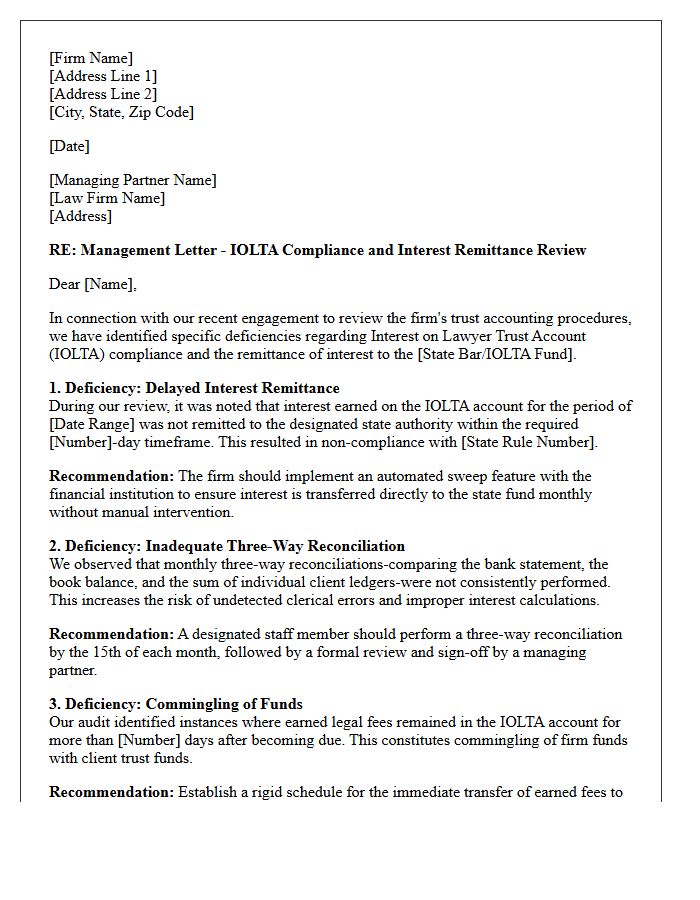

Management Letter on IOLTA Compliance and Interest Remittance Deficiencies

A Management Letter identifies critical internal control weaknesses regarding IOLTA accounts. It highlights compliance deficiencies such as improper record-keeping, failure to perform monthly three-way reconciliations, or interest remittance errors. These findings warn law firms of potential regulatory violations that could lead to disciplinary action. Addressing these gaps ensures the accurate transfer of earned interest to state justice funds while protecting client assets. Timely remediation of these documented issues is essential for maintaining professional fiduciary responsibilities and legal ethical standards.

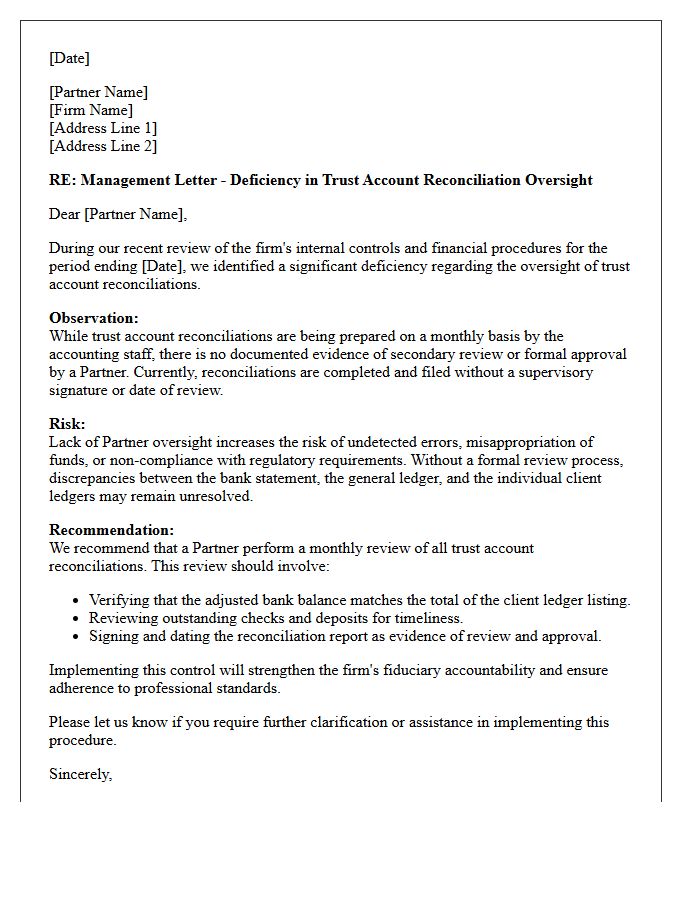

Management Letter Noting Lack of Partner Oversight in Trust Reconciliation

A management letter identifies a lack of partner oversight in trust account reconciliations as a critical internal control weakness. Without senior review, undiscovered errors or misappropriation of client funds may occur, increasing legal and financial risks. Effective governance requires regular partner supervision to verify that reconciliations are accurate, timely, and compliant with fiduciary standards. Implementing a formal review process ensures accountability, mitigates the risk of fraud, and maintains the integrity of the firm's financial reporting and professional reputation.

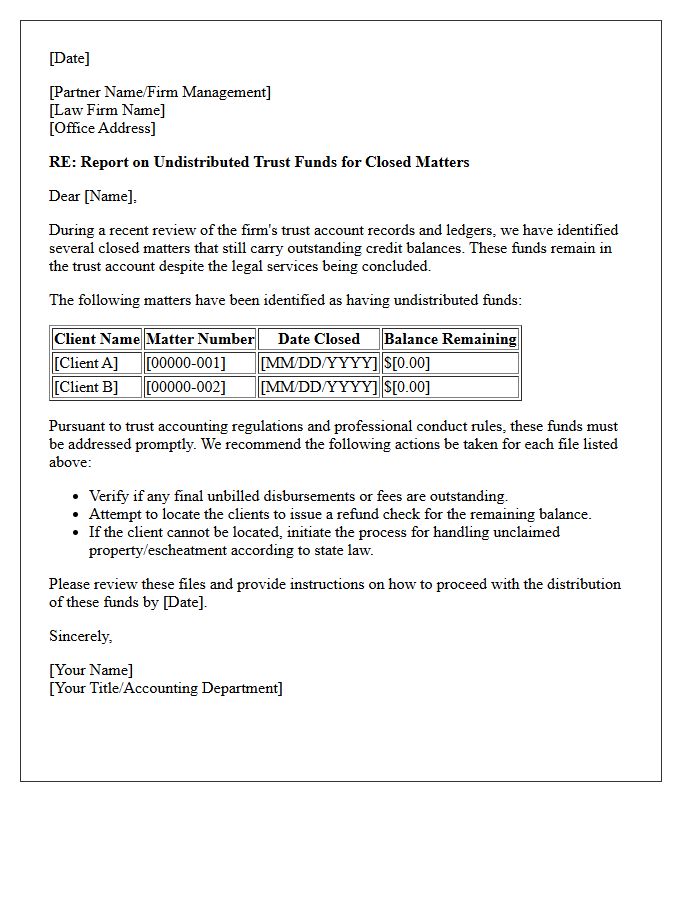

Management Letter Identifying Undistributed Trust Funds for Closed Matters

A management letter identifying undistributed trust funds for closed matters is a critical compliance tool for law firms. It highlights unclaimed client balances sitting in escrow after legal services have concluded. Failure to resolve these balances can lead to ethical violations or escheatment obligations to the state. Regular review of this report ensures accurate financial reconciliation and mitigates the risk of professional negligence. Firms must proactively return these funds to clients or follow statutory procedures for abandoned property to maintain trust account integrity and regulatory adherence.

What is a management letter regarding trust account reconciliation?

A management letter is a formal document issued by an auditor or consultant that identifies internal control weaknesses in a law firm's trust account reconciliation processes and provides actionable recommendations for improvement.

Why is a monthly three-way reconciliation essential for law firms?

A three-way reconciliation compares the book balance, the adjusted bank balance, and the total of individual client ledger balances to ensure all trust funds are accurately accounted for and to prevent commingling or misappropriation.

What are common deficiencies found in trust account management letters?

Common deficiencies include lack of timely reconciliations, failure to perform independent reviews, long-standing outstanding checks, and unidentified funds remaining in the trust account without proper documentation.

How does a formal review process improve trust account compliance?

Implementing a formal review process where a partner or senior manager signs off on monthly reconciliations ensures oversight, detects clerical errors early, and demonstrates the firm's commitment to state bar fiduciary standards.

What are the consequences of failing to address trust account reconciliation issues?

Failure to rectify reconciliation gaps can lead to financial discrepancies, severe ethical violations, potential disbarment, and increased vulnerability to internal fraud or external audits by regulatory bodies.

Comments