A Disclaimer of Opinion letter is issued by auditors when they are unable to obtain sufficient evidence to form a professional judgment on financial statements. This typically occurs due to severe scope limitations or significant uncertainties. Understanding this formal communication is vital for maintaining corporate transparency and regulatory compliance. To assist your reporting process, below are some ready to use template.

Image cover: Professional Disclaimer of Opinion Letter Samples and Templates

Letter Samples List

- Standard Audit Disclaimer of Opinion Letter

- Scope Limitation Disclaimer of Opinion Letter

- Insufficient Audit Evidence Disclaimer of Opinion Letter

- Inadequate Accounting Records Disclaimer of Opinion Letter

- Going Concern Uncertainty Disclaimer of Opinion Letter

- Missing Financial Documentation Disclaimer of Opinion Letter

- Impaired Auditor Independence Disclaimer of Opinion Letter

- Pending Legal Litigation Disclaimer of Opinion Letter

- Unaudited Subsidiary Financials Disclaimer of Opinion Letter

- Destroyed Financial Records Disclaimer of Opinion Letter

- Multiple Pervasive Uncertainties Disclaimer of Opinion Letter

- Initial Engagement Inventory Disclaimer of Opinion Letter

Standard Audit Disclaimer of Opinion Letter

A Disclaimer of Opinion is issued when an auditor cannot form a conclusion on financial statements. This typically occurs due to a limitation on scope or a lack of sufficient evidence. Unlike an adverse opinion, it signifies that the auditor does not express an opinion because of significant uncertainties or material data gaps. Stakeholders should view this as a major red flag, indicating that the entity's financial health and reporting integrity cannot be verified, often leading to legal or regulatory consequences for the organization involved.

Scope Limitation Disclaimer of Opinion Letter

A Scope Limitation Disclaimer of Opinion Letter is issued when auditors cannot obtain sufficient appropriate audit evidence to form a conclusion. This typically occurs due to restricted access to records, physical constraints, or management interference. Unlike a qualified opinion, this formal statement indicates that the financial statements' reliability remains unverified. It serves as a critical warning to stakeholders that significant uncertainties exist, preventing the auditor from expressing any opinion on the entity's overall financial health or compliance with reporting standards.

Insufficient Audit Evidence Disclaimer of Opinion Letter

An Insufficient Audit Evidence Disclaimer of Opinion occurs when auditors cannot obtain enough corroborative data to support financial statements. Unlike an adverse opinion, this letter signifies that scope limitations prevent the auditor from forming any conclusion. This typically results from missing records, restricted access, or internal control collapses. For stakeholders, this is a critical red flag indicating severe transparency issues and potential financial reporting failures. It effectively warns that the entity's financial health cannot be verified, often leading to immediate regulatory scrutiny and loss of investor confidence.

Inadequate Accounting Records Disclaimer of Opinion Letter

An Inadequate Accounting Records Disclaimer of Opinion Letter is issued when auditors cannot obtain sufficient evidence to verify financial accuracy. This formal statement occurs because the entity's documentation is missing, disorganized, or unreliable, preventing a clear audit trail. Consequently, the auditor explicitly states they do not express an opinion on the financial statements. This is a critical warning for investors and stakeholders, indicating a significant scope limitation and potential governance failures that obscure the organization's true financial health and legal compliance.

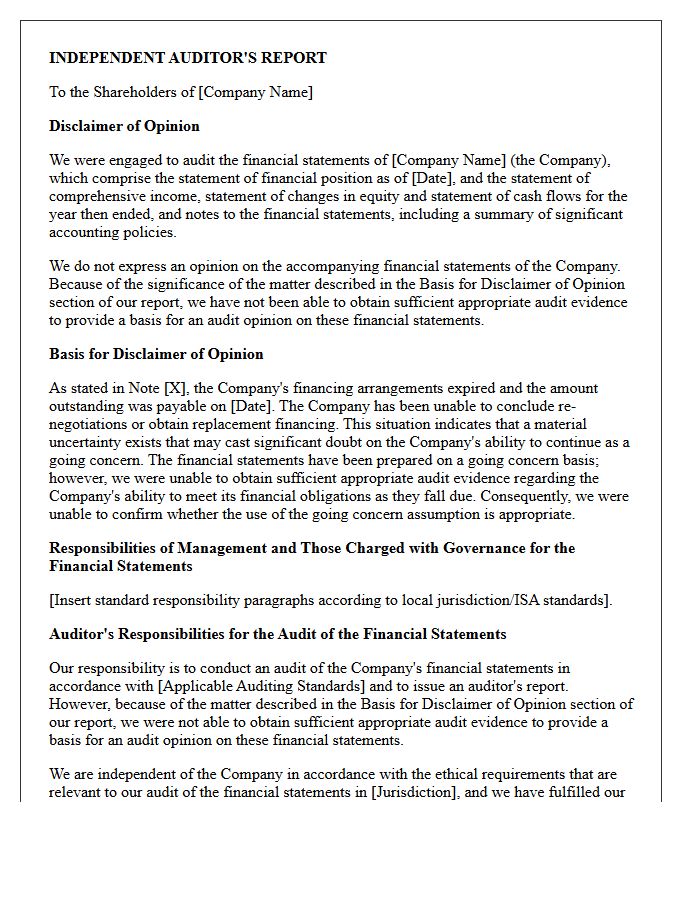

Going Concern Uncertainty Disclaimer of Opinion Letter

A Disclaimer of Opinion regarding going concern uncertainty is a critical audit report issued when an auditor cannot obtain sufficient evidence to verify a company's financial viability. Unlike a standard warning, this indicates extreme material uncertainty, preventing the auditor from expressing any opinion on the financial statements. This typically occurs when severe liquidity issues or imminent insolvency threats exist. For investors, this document serves as a high-level risk signal, suggesting the business model may fail within one year, potentially leading to total investment loss or corporate liquidation.

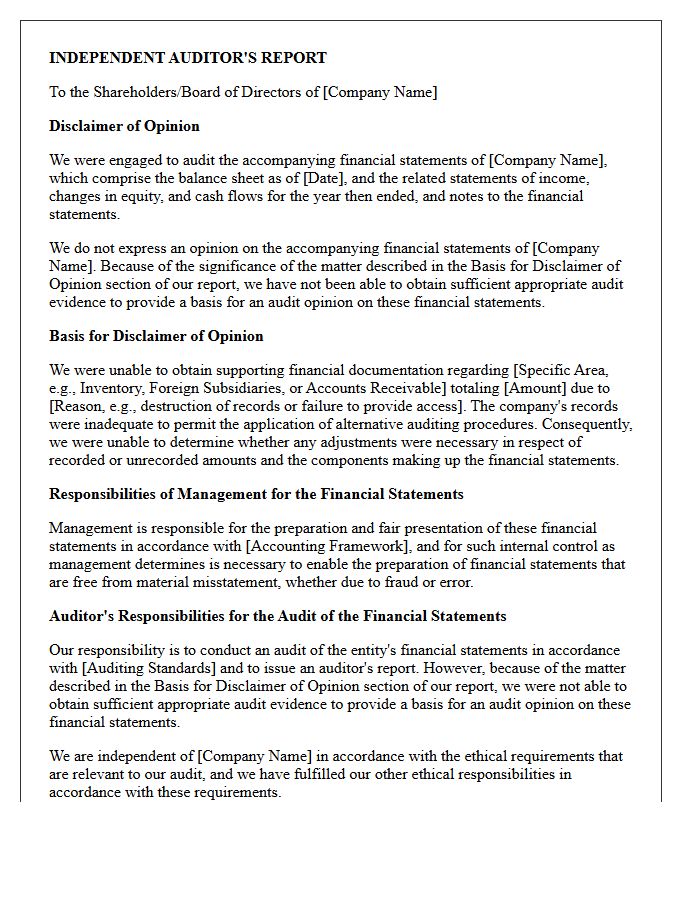

Missing Financial Documentation Disclaimer of Opinion Letter

A Disclaimer of Opinion is the most severe audit result issued when missing financial documentation prevents an auditor from forming a conclusion. This happens when a company fails to provide essential records, such as invoices, bank statements, or inventory logs. For stakeholders, this signal indicates a high level of financial uncertainty and potential risk, as the auditor cannot verify the accuracy or completeness of the financial statements. Resolving this requires implementing robust internal controls and maintaining organized data to ensure future transparency and auditability.

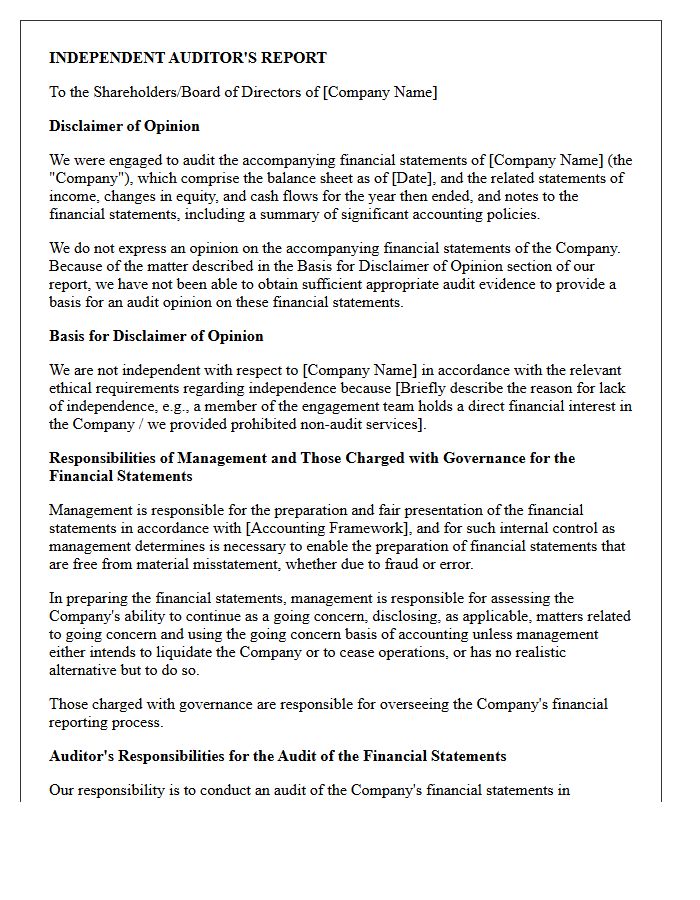

Impaired Auditor Independence Disclaimer of Opinion Letter

An Impaired Auditor Independence Disclaimer of Opinion Letter is issued when an auditor cannot remain objective due to financial, personal, or professional conflicts. Unlike a standard audit report, this formal statement declares that no opinion can be expressed on the financial statements. This occurs because independence is a mandatory ethical requirement under professional standards. Without it, the audit lacks credibility, and the auditor must explicitly disclaim their opinion to inform stakeholders that the audit integrity has been compromised by these underlying conflicts of interest.

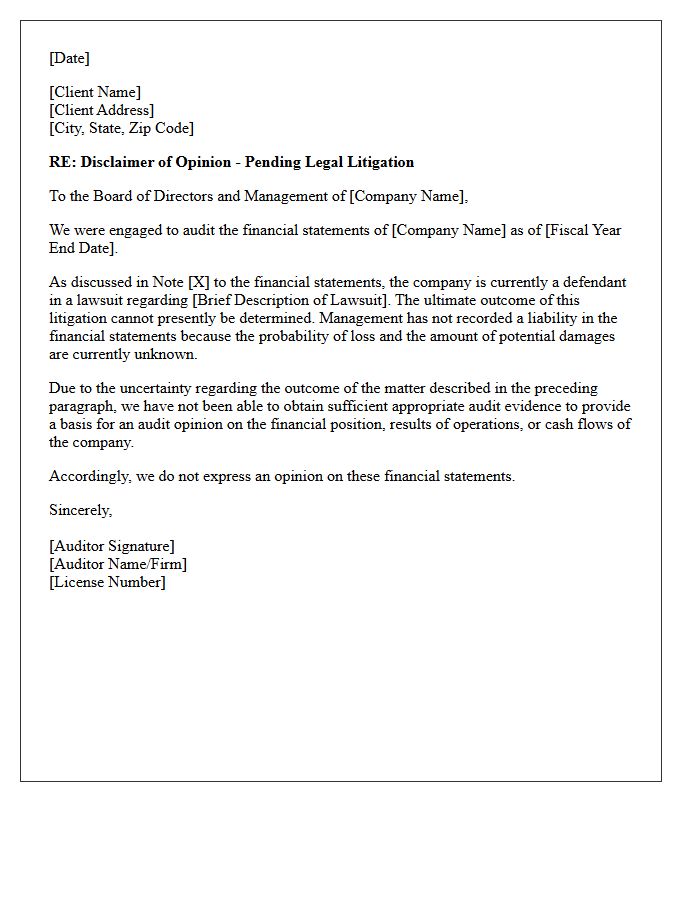

Pending Legal Litigation Disclaimer of Opinion Letter

A Pending Legal Litigation Disclaimer of Opinion Letter is a formal statement issued by an auditor when they cannot reach a conclusion on a company's financial health. This typically occurs due to uncertainties surrounding significant unresolved lawsuits. Since the potential financial impact of these legal battles is unpredictable, auditors protect themselves by refusing to provide a definitive opinion. For stakeholders, this disclaimer serves as a critical red flag, signaling that the organization faces substantial legal risks that could materially impair its future stability and overall valuation.

Unaudited Subsidiary Financials Disclaimer of Opinion Letter

An Unaudited Subsidiary Financials Disclaimer of Opinion Letter is a critical audit document issued when an auditor cannot verify the financial accuracy of a subsidiary entity. This occurs when the subsidiary's data is not audited, preventing the auditor from obtaining sufficient evidence to form a conclusion on the consolidated financial statements. Investors must recognize that this disclaimer indicates a material scope limitation, signaling potential hidden risks or inaccuracies within the parent company's overall financial reporting and internal control systems.

Destroyed Financial Records Disclaimer of Opinion Letter

A Disclaimer of Opinion is issued by auditors when destroyed financial records prevent them from gathering sufficient evidence to form a conclusion. This formal statement indicates that because critical documentation is missing, the auditor cannot verify the accuracy or completeness of the financial statements. For stakeholders, this represents a significant risk, as it suggests lack of transparency and potential non-compliance. Organizations must maintain robust backup systems to avoid this outcome, which often leads to adverse regulatory consequences and loss of investor confidence due to unverified fiscal health.

Multiple Pervasive Uncertainties Disclaimer of Opinion Letter

A Multiple Pervasive Uncertainties Disclaimer of Opinion Letter is issued when auditors encounter significant limitations or extreme instability within a company's financial records. Unlike a standard report, this document signifies that the auditor cannot express an opinion due to the cumulative effect of various unknowns. These factors, such as pending litigation or going concern doubts, are so pervasive that they compromise the financial statements' overall reliability. Investors should view this as a major red flag, indicating that the entity's true financial position remains unverified and potentially precarious.

Initial Engagement Inventory Disclaimer of Opinion Letter

An Initial Engagement Inventory Disclaimer of Opinion Letter is a formal notification issued when an auditor cannot verify opening balances. This typically occurs during a first-time audit if the auditor was not present for the physical inventory count or lacks sufficient evidence from prior periods. Since inventory significantly affects the cost of goods sold and net income, the auditor issues a disclaimer of opinion specifically regarding the financial performance and cash flows. It serves as a crucial regulatory disclosure, protecting the auditor while informing stakeholders about data limitations.

What is a Disclaimer of Opinion letter in auditing?

A Disclaimer of Opinion letter is a report issued by an external auditor stating that they are unable to form an opinion on a company's financial statements. This typically occurs when there is a significant limitation on the scope of the audit or if there is a lack of sufficient evidence to support the financial data provided.

What triggers a Disclaimer of Opinion?

Common triggers include a lack of independence by the auditor, severe restrictions on access to financial records, destruction of evidence, or significant uncertainties regarding the company's ability to continue as a "going concern" that cannot be adequately quantified.

How does a Disclaimer of Opinion differ from an Adverse Opinion?

An Adverse Opinion is issued when an auditor finds that financial statements are materially misstated or do not conform to GAAP. In contrast, a Disclaimer of Opinion is issued when the auditor cannot gather enough information to determine whether the statements are accurate or inaccurate in the first place.

What are the consequences of receiving a Disclaimer of Opinion letter?

Receiving this letter can lead to serious negative consequences, including a loss of investor confidence, a drop in stock price, potential delisting from stock exchanges, and difficulties in securing loans or credit due to the lack of verified financial transparency.

Can a company resolve a Disclaimer of Opinion in future audits?

Yes, a company can resolve a Disclaimer of Opinion by addressing the underlying issues, such as improving internal controls, granting full access to records, maintaining proper documentation, and ensuring auditor independence for the subsequent reporting period.

Comments