A Going Concern Opinion Letter is a formal statement issued by auditors expressing substantial doubt about a company's ability to continue operations for the next year. It highlights financial distress, liquidity issues, or negative cash flows discovered during an audit. Understanding this disclosure is vital for investors and stakeholders assessing corporate viability. To help you draft one, below are some ready to use template.

Image cover: Comprehensive Guide to Going Concern Opinion Letters and Professional Templates

Letter Samples List

- Unqualified Opinion Letter with Going Concern Emphasis

- Qualified Opinion Letter Due to Going Concern

- Disclaimer of Opinion Letter Regarding Going Concern

- Management Representation Letter for Going Concern

- Going Concern Assessment Communication Letter

- Substantial Doubt About Going Concern Letter

- Going Concern Mitigation Plan Evaluation Letter

- Adverse Opinion Letter Noting Going Concern

- Audit Committee Communication Letter on Going Concern

- Independent Auditor Going Concern Report Letter

- Going Concern Explanatory Paragraph Audit Letter

- Going Concern Resolution and Clearance Letter

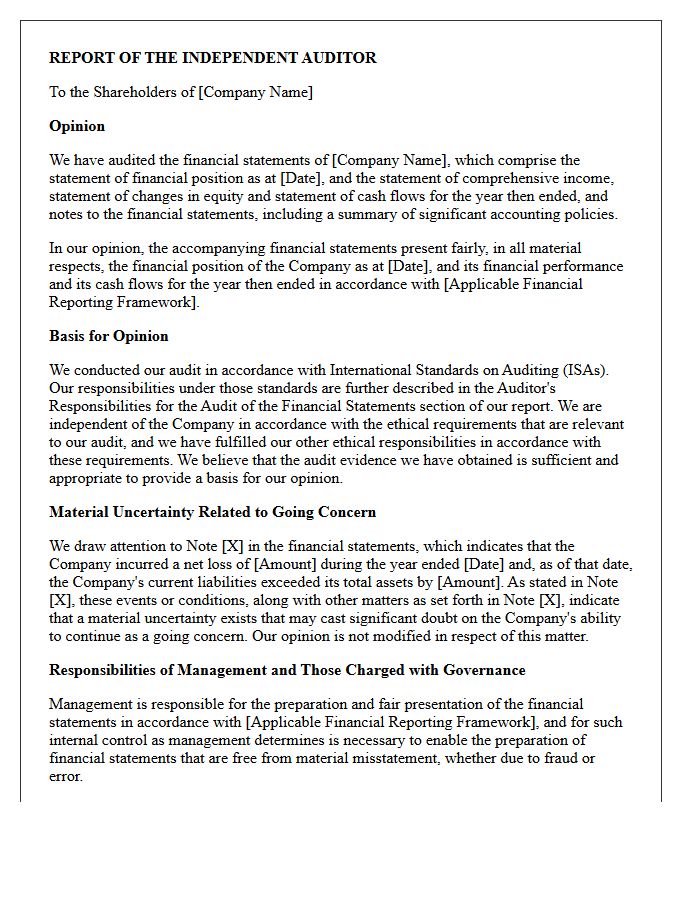

Unqualified Opinion Letter with Going Concern Emphasis

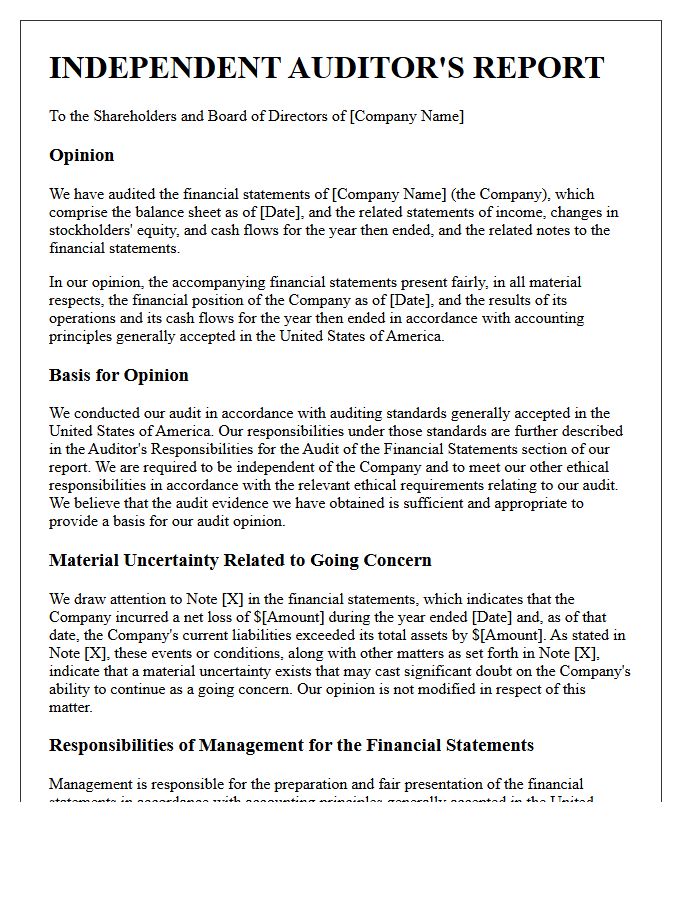

An Unqualified Opinion with Going Concern Emphasis confirms that a company's financial statements are fairly presented according to accounting standards. However, the auditor includes an explanatory paragraph highlighting substantial doubt about the entity's ability to continue operating for the next year. This emphasis of matter serves as a critical warning to investors that while the historical data is accurate, significant financial distress or liquidity issues threaten the firm's future survival. It bridges the gap between clean reporting and potential insolvency risks.

Qualified Opinion Letter Due to Going Concern

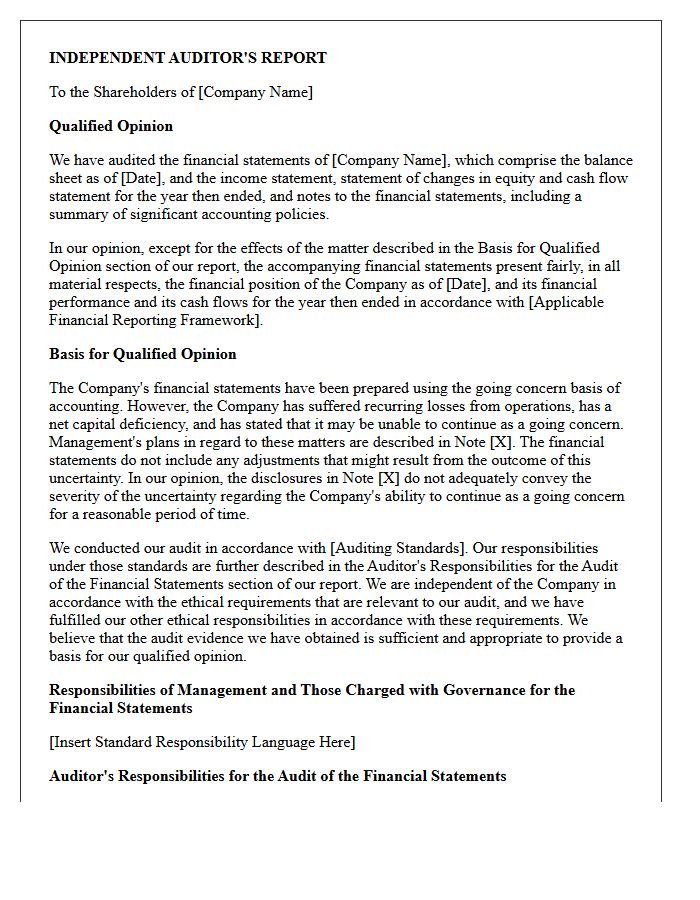

A Qualified Opinion Letter Due to Going Concern is a formal report issued by an external auditor when they harbor significant doubts about a company's ability to remain operational. This modified audit opinion indicates that while financial statements are generally accurate, there is substantial uncertainty regarding the entity's financial stability over the next twelve months. Investors view this as a critical warning sign of potential insolvency or bankruptcy. It highlights that the business may not meet its obligations, requiring stakeholders to exercise extreme caution before making investment or credit decisions.

Disclaimer of Opinion Letter Regarding Going Concern

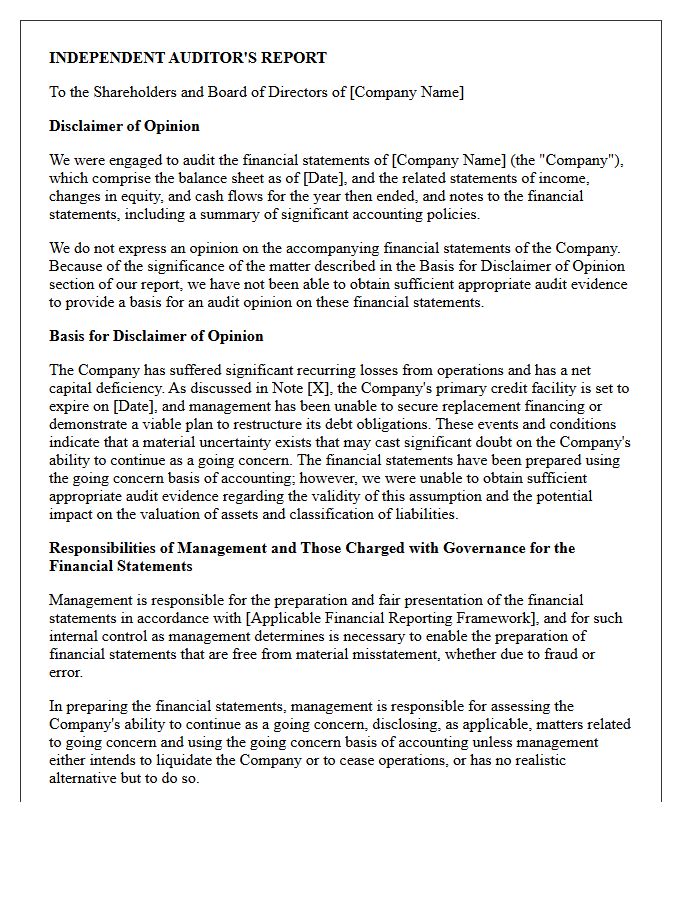

A Disclaimer of Opinion occurs when an auditor cannot gather sufficient evidence to provide a verdict on financial statements. In the context of a going concern, this suggests extreme uncertainty regarding a company's ability to remain operational over the next year. Unlike an adverse opinion, this letter signifies that the financial records or underlying conditions are so unstable or incomplete that the auditor refuses to vouch for the business's viability. Investors view this as a major red flag indicating potential insolvency or imminent corporate failure.

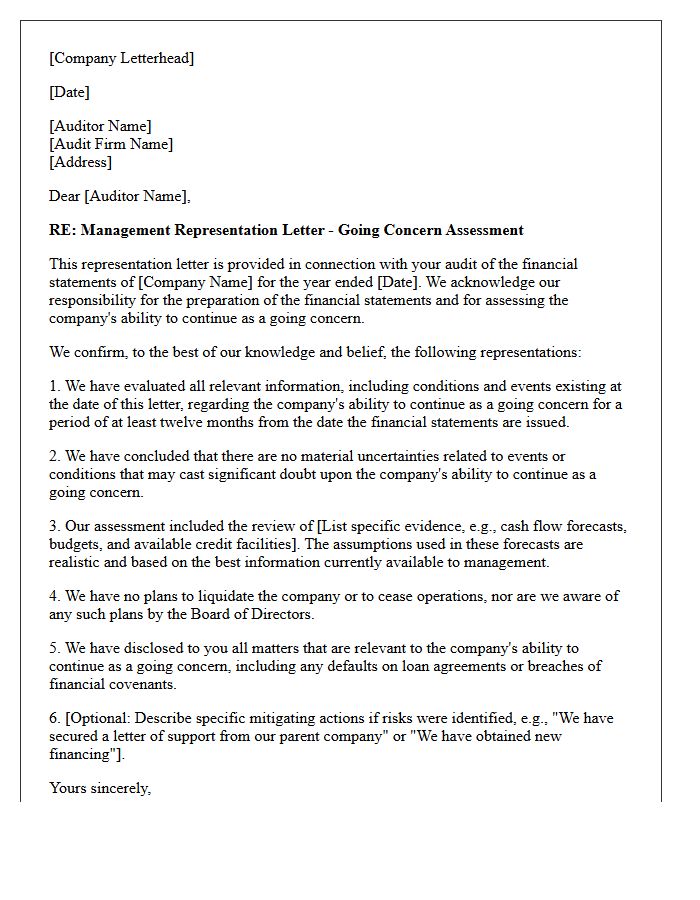

Management Representation Letter for Going Concern

A Management Representation Letter for going concern is a formal document where directors confirm the entity's ability to continue operations for the foreseeable future. It provides audit evidence regarding management's plans for liquidating assets, borrowing money, or restructuring debt to mitigate financial distress. This letter ensures accountability, as management must disclose all material uncertainties that could cast significant doubt on the company's viability. By signing, leadership acknowledges their responsibility for assessing financial sustainability and provides the auditors with necessary written assurances to support the final audit opinion.

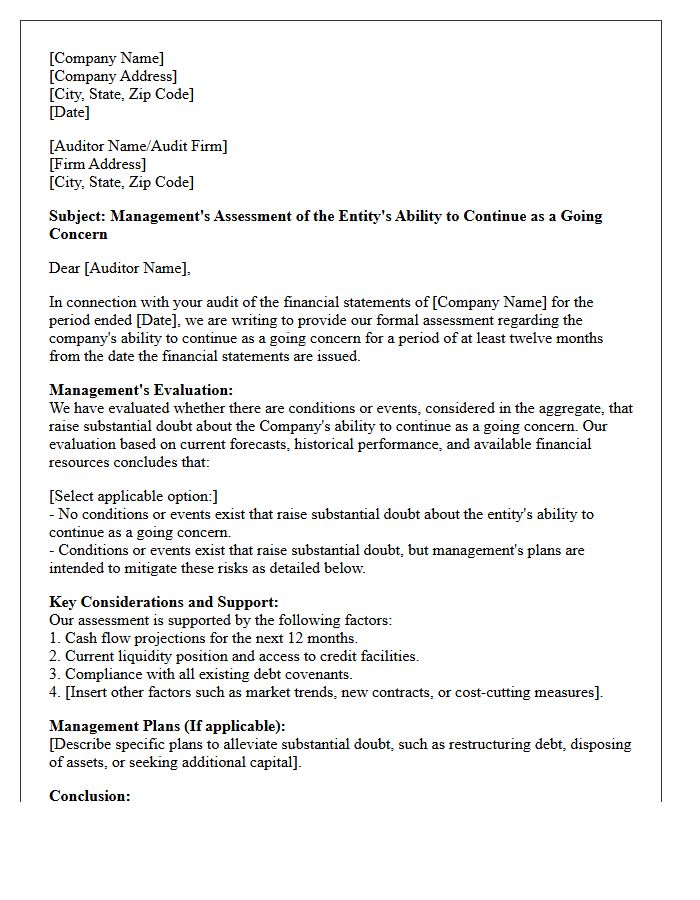

Going Concern Assessment Communication Letter

A Going Concern Assessment Communication Letter is a formal document from management to auditors evaluating the company's ability to continue operations for at least twelve months. It outlines financial viability, identifying potential risks like liquidity issues or debt defaults. If significant doubt exists, the letter must detail mitigation plans to resolve these uncertainties. Proper documentation ensures transparency, fulfills regulatory compliance, and supports the auditor's opinion regarding the entity's operational stability and future prospects in the financial statements.

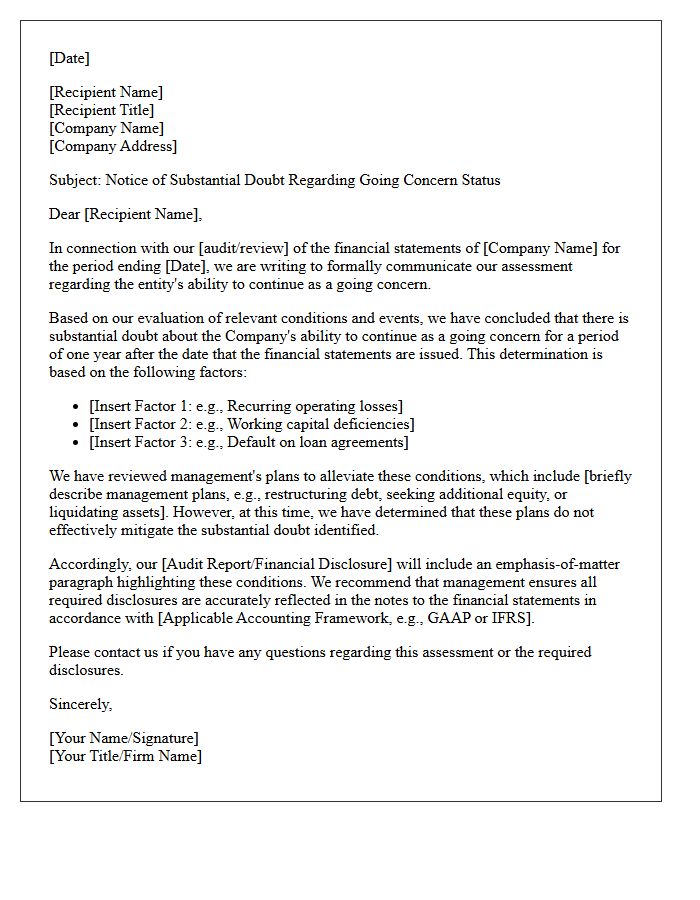

Substantial Doubt About Going Concern Letter

A substantial doubt about going concern letter is a formal notice issued by auditors when they believe a company may not survive the next twelve months. This audit opinion signals significant financial distress, such as negative cash flows or debt defaults. It warns investors and creditors that the business lacks the necessary resources to meet its upcoming obligations. If management cannot provide a viable mitigation plan to resolve these liquidity issues, the auditor must disclose this uncertainty to ensure transparency regarding the entity's long-term operational viability and potential risk of bankruptcy.

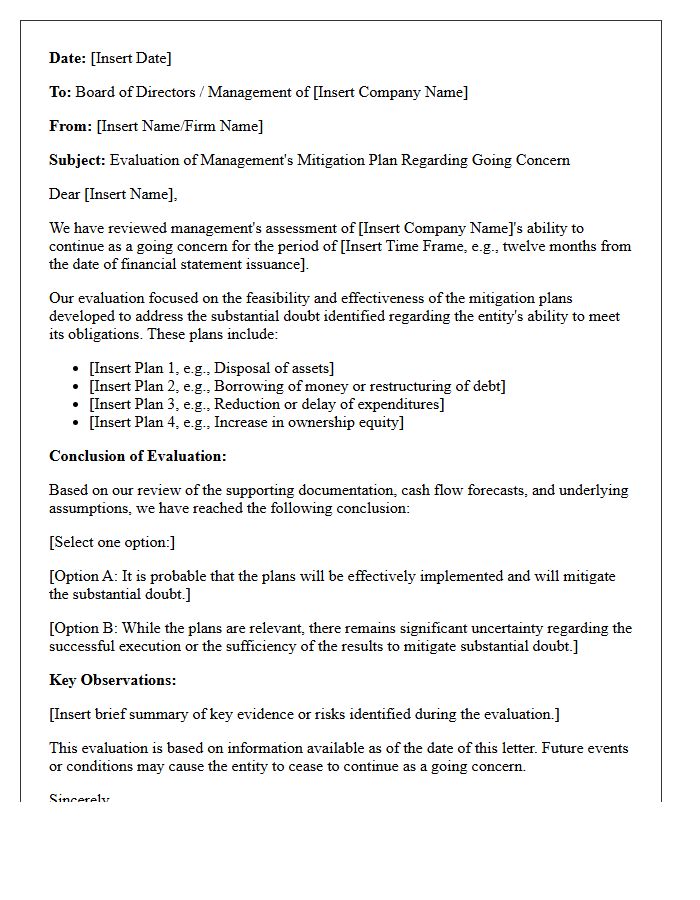

Going Concern Mitigation Plan Evaluation Letter

A Going Concern Mitigation Plan Evaluation Letter is a formal assessment issued by auditors to determine if a company's strategies can prevent insolvency. This document critically reviews management's projections, such as cost-cutting, asset sales, or securing new financing. The goal is to verify if these actions provide reasonable assurance that the business will remain operational for at least twelve months. Investors rely on this letter to gauge financial stability and the risk of total business failure. Accurate cash flow forecasting remains the most vital element for a successful evaluation outcome.

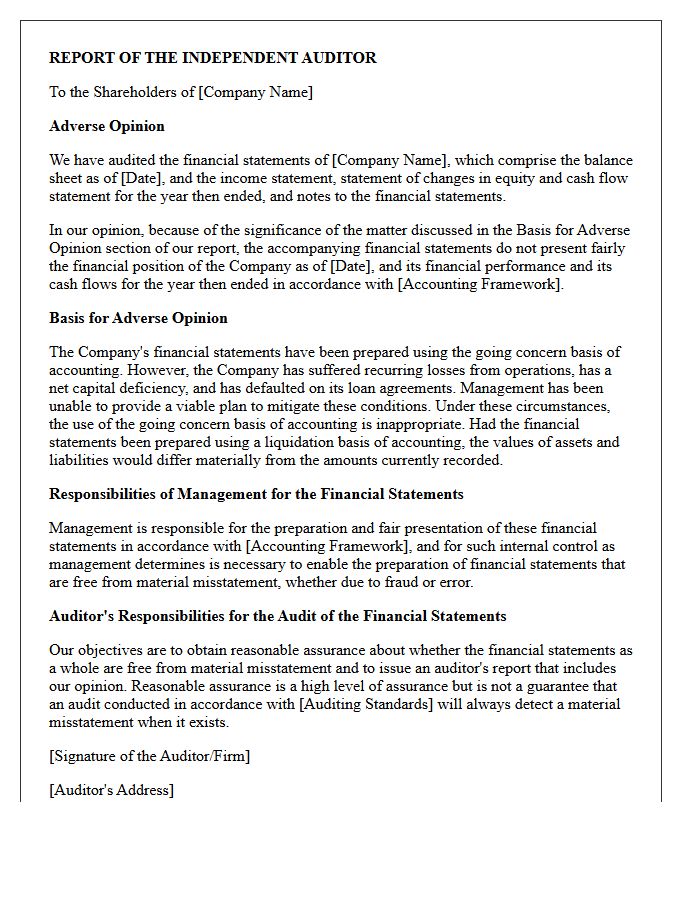

Adverse Opinion Letter Noting Going Concern

An adverse opinion is the most severe audit result, indicating that financial statements are materially misstated and do not fairly represent a company's health. When combined with a going concern qualification, it signals that the auditor has found pervasive reporting failures regarding the entity's ability to remain operational. This dual warning warns stakeholders that the company faces imminent insolvency and that its financial records are fundamentally unreliable, making it a critical red flag for potential business failure and total investment loss.

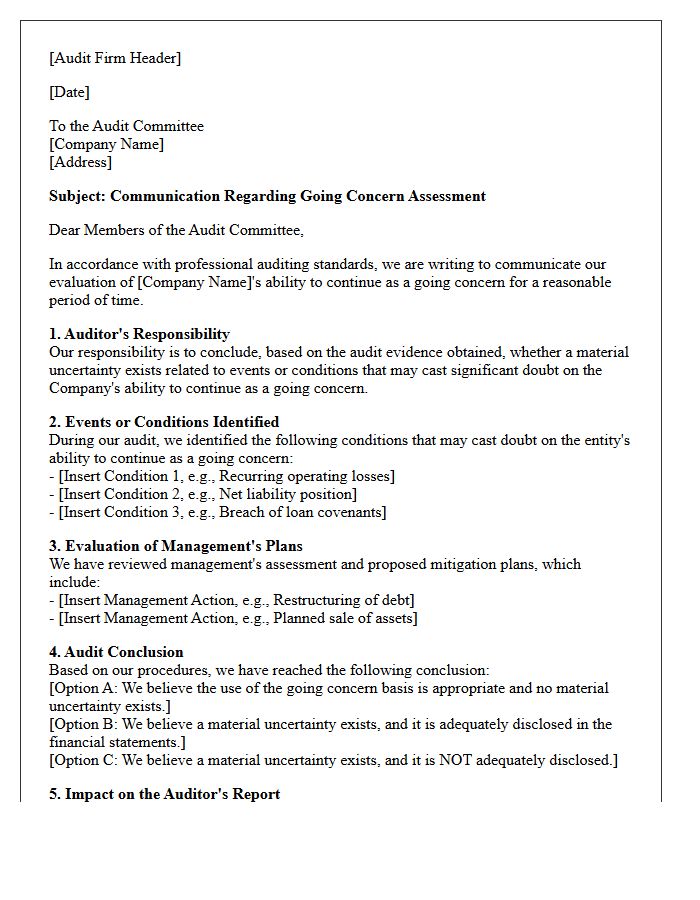

Audit Committee Communication Letter on Going Concern

An Audit Committee Communication Letter on Going Concern is a formal report from auditors to a company's oversight body. Its primary goal is to address substantial doubt about an organization's ability to continue operations for at least one year. Auditors must communicate identified events or conditions that threaten financial viability, such as severe liquidity issues or loan defaults. This letter ensures that governance members are informed of management's mitigation plans and any required disclosures in financial statements to maintain transparency for stakeholders and investors.

Independent Auditor Going Concern Report Letter

An Independent Auditor Going Concern Report Letter is a critical disclosure issued when a firm faces significant risk of insolvency within one year. It signals that the auditor has substantial doubt about the entity's ability to continue operations. This letter serves as a formal warning to investors and creditors, highlighting potential liquidity issues or operational failures. Understanding this report is vital for assessing financial stability and investment risk, as it indicates the company may not be able to meet its obligations or realize assets in the normal course of business.

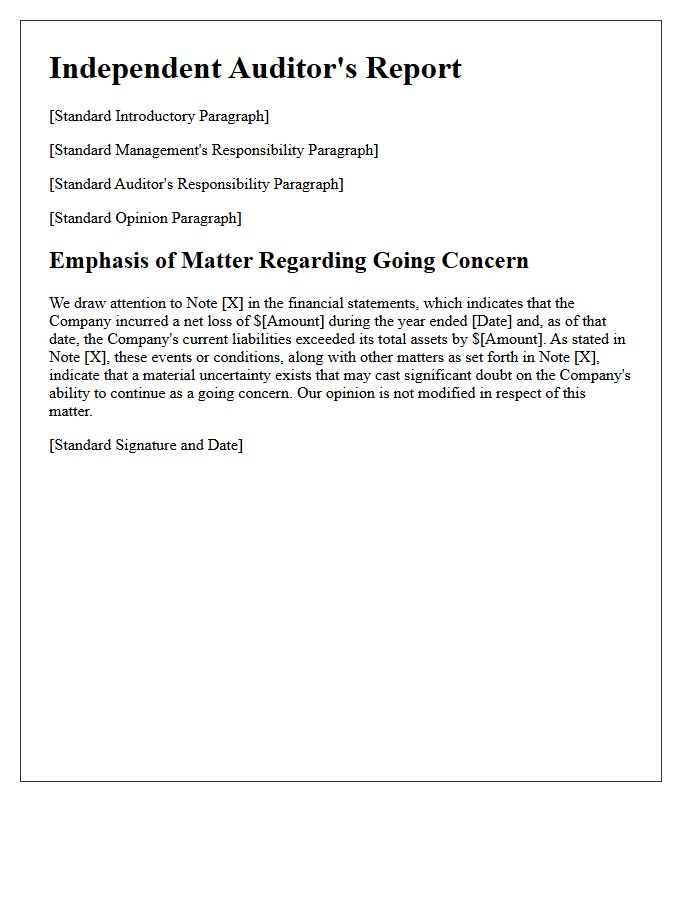

Going Concern Explanatory Paragraph Audit Letter

A Going Concern Explanatory Paragraph is a critical addition to an auditor's report when there is substantial doubt about a company's ability to continue operating for at least one year. While the financial statements may still be presented fairly, this section alerts investors to significant financial distress or liquidity issues. It highlights risks like recurring losses or loan defaults that could lead to business failure. Understanding this disclosure is essential for assessing the long-term viability and investment risk associated with the entity.

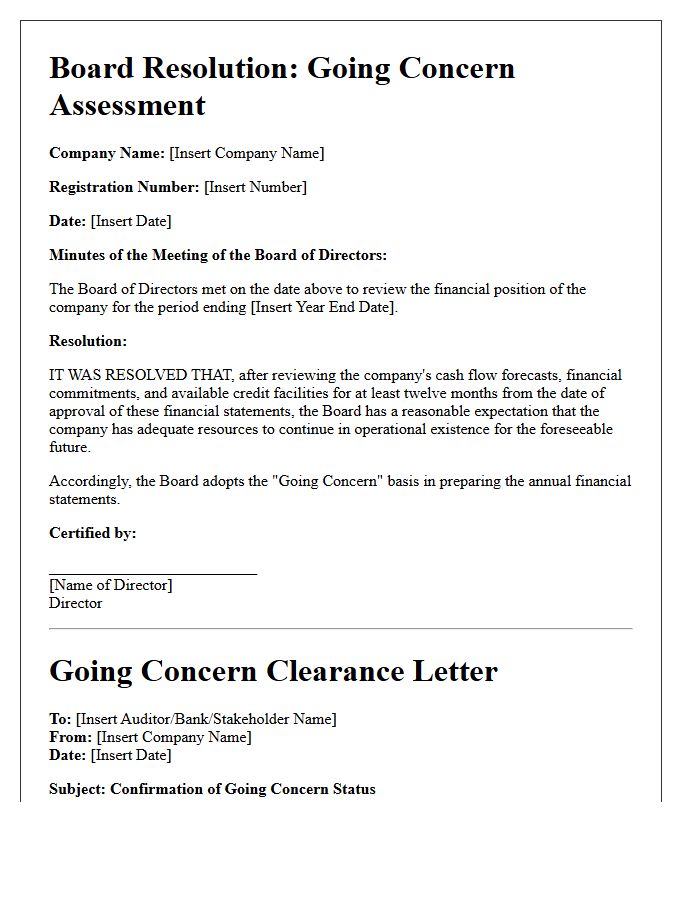

Going Concern Resolution and Clearance Letter

A Going Concern Resolution is a formal document passed by company directors to confirm the entity's ability to meet financial obligations for the foreseeable future. This is a critical requirement for year-end financial reporting and auditing. Conversely, a Clearance Letter is an official statement from tax authorities or creditors confirming that all liabilities are settled. This legal certification is essential during business liquidations, mergers, or ownership transfers to ensure the successor is not held liable for outstanding debts, providing a clean financial exit.

What is a Going Concern Opinion Letter?

A Going Concern Opinion Letter is a formal statement issued by an independent auditor expressing substantial doubt about a company's ability to continue its operations and meet financial obligations for a reasonable period, typically one year beyond the financial statement date.

What triggers a Going Concern modification in an audit report?

Auditors issue this opinion when negative trends, such as recurring operating losses, working capital deficiencies, loan defaults, or legal proceedings, suggest the entity may not be able to realize its assets and discharge its liabilities in the normal course of business.

How does a Going Concern Opinion affect a company's creditworthiness?

Receiving a Going Concern Letter can negatively impact credit ratings, make it difficult to secure new financing, and may trigger "default" clauses in existing loan agreements, potentially accelerating debt repayment schedules.

What is the difference between a Clean Opinion and a Going Concern Opinion?

A Clean (Unmodified) Opinion states that financial statements are presented fairly in all material respects. A Going Concern Opinion is an Unmodified Opinion that includes an additional "Emphasis of Matter" paragraph highlighting the uncertainty regarding the company's future viability.

Can a company recover after receiving a Going Concern Letter?

Yes, a company can remove this status by implementing a successful turnaround plan, which may include restructuring debt, securing new equity investments, selling non-core assets, or significantly improving operational cash flow to mitigate the auditor's concerns.

Comments