An R&D Tax Credit Opinion Letter provides essential legal and technical documentation to substantiate your claims. It mitigates audit risks by evaluating qualified research activities and expenditures against IRS standards. Securing professional validation ensures compliance and strengthens your tax position during regulatory reviews. To streamline your documentation process, below are some ready to use template.

Image cover: R&D Tax Credit Opinion Letters: Expert Samples and Documentation Templates

Letter Samples List

- Draft Research and Development Tax Credit Opinion Letter

- Final Research and Development Tax Credit Opinion Letter

- Research and Development Tax Credit Feasibility Letter

- Research and Development Tax Credit Engagement Letter

- Research and Development Tax Credit Qualification Letter

- Research and Development Tax Credit Substantiation Letter

- Research and Development Tax Credit Nexus Opinion Letter

- Research and Development Tax Credit Management Representation Letter

- Internal Revenue Service Research and Development Tax Credit Response Letter

- State Apportionment Research and Development Tax Credit Opinion Letter

- Amended Return Research and Development Tax Credit Letter

- Research and Development Tax Credit Audit Defense Letter

- Research and Development Tax Credit Safe Harbor Letter

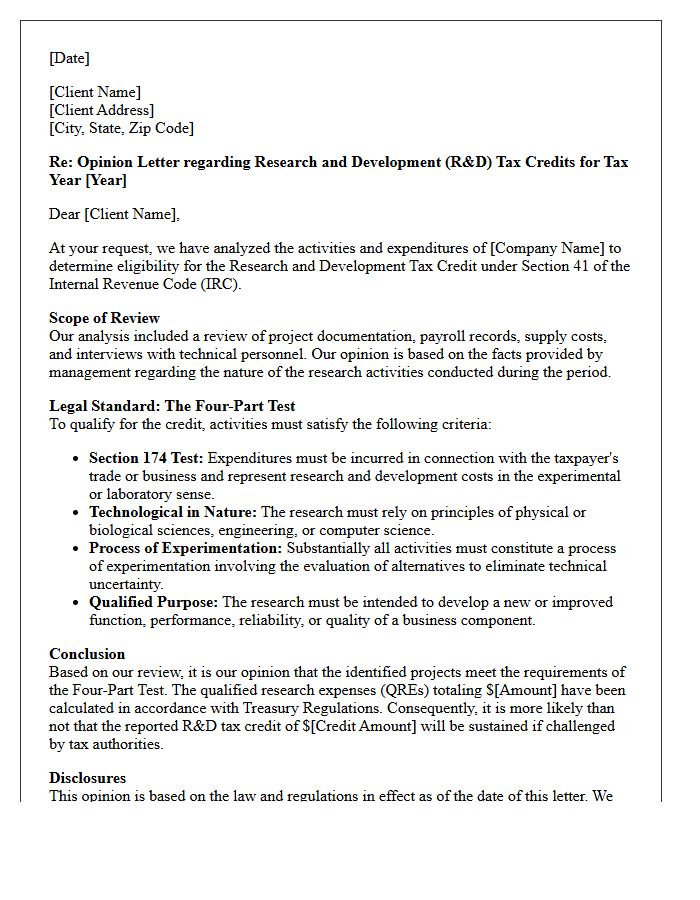

Draft Research and Development Tax Credit Opinion Letter

A Draft Research and Development Tax Credit Opinion Letter provides a legal framework to justify tax savings under Section 41. It must substantiate eligibility by detailing how specific activities meet the four-part test. This formal document serves as a defensive shield during IRS audits, establishing "reasonable cause" to avoid penalties. Key components include technical project descriptions, quantitative methodologies, and regulatory compliance analysis. Taxpayers rely on these professional opinions to mitigate financial risks while ensuring all qualified research expenses are accurately documented and legally defensible within the current tax landscape.

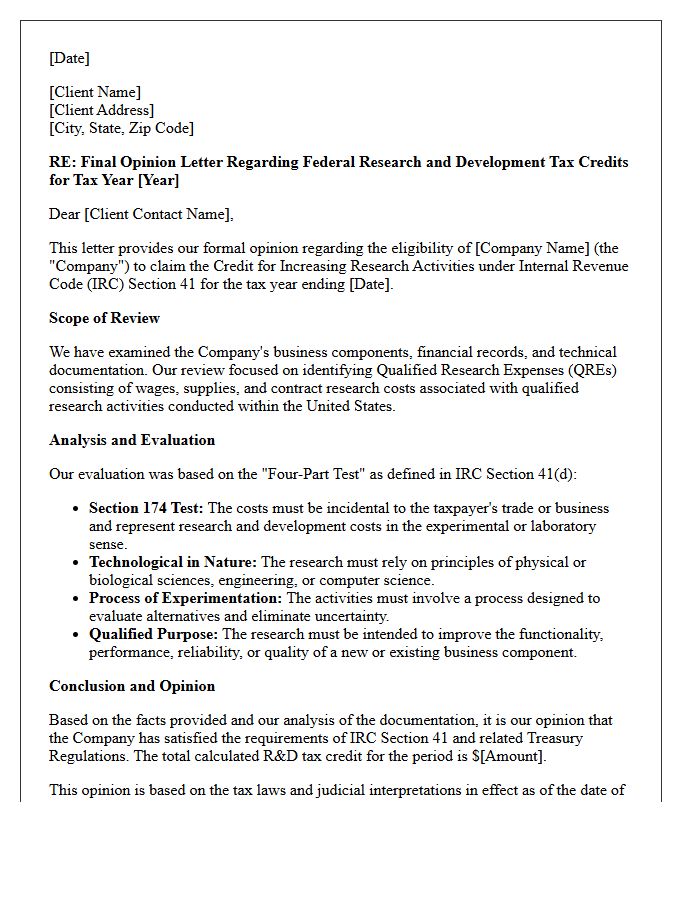

Final Research and Development Tax Credit Opinion Letter

A Final Research and Development Tax Credit Opinion Letter serves as a critical legal substantiation document provided by tax experts. It offers a formal evaluation of a company's qualified research activities and expenditures, ensuring compliance with IRS Section 41. This letter identifies qualified research expenses (QREs) and validates that projects meet the Four-Part Test. By documenting the methodology and technical nexus, the opinion letter provides a robust defense against potential audits, mitigating financial risk and confirming the technical eligibility of claims before filing tax returns.

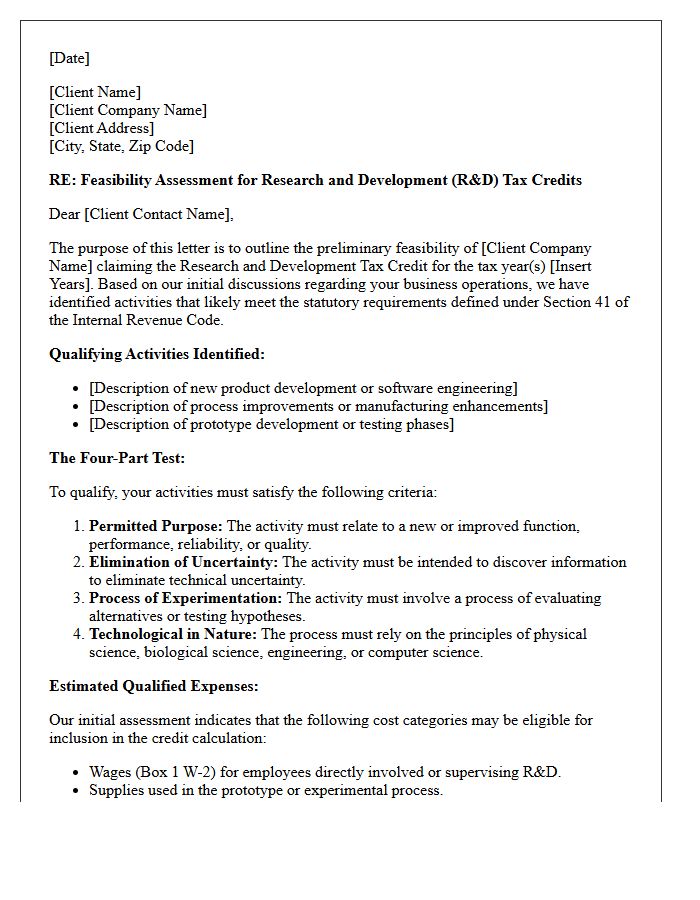

Research and Development Tax Credit Feasibility Letter

A Research and Development Tax Credit Feasibility Letter serves as a formal preliminary assessment to determine if a company's activities qualify for federal or state tax incentives. This document evaluates technical projects against the four-part test to estimate potential tax savings and identify eligible qualified research expenses. It acts as a strategic roadmap, outlining the methodology for a full study while highlighting financial benefits and documentation requirements. Securing this letter is an essential first step for businesses to validate their eligibility before investing in a comprehensive R&D tax credit claim.

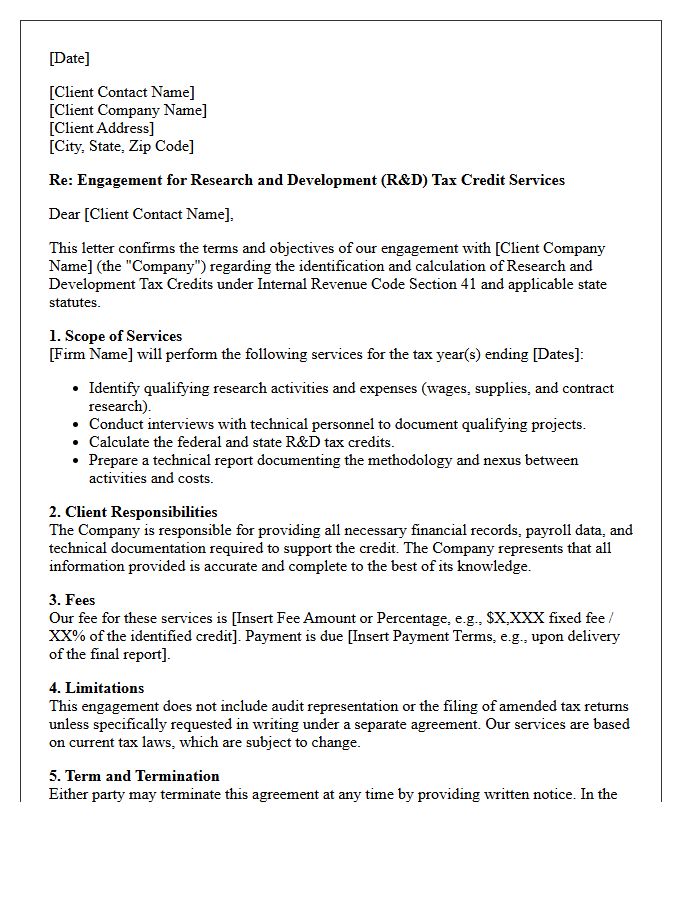

Research and Development Tax Credit Engagement Letter

A Research and Development Tax Credit Engagement Letter is a legally binding contract that defines the relationship between a client and a consultancy. It outlines the scope of services, fee structures, and responsibilities for documenting eligible innovation activities. This document ensures compliance with IRS guidelines by establishing clear expectations regarding claim methodologies and audit defense support. Before signing, businesses must verify terms related to contingency fees and data confidentiality to protect their financial interests during the tax credit recovery process.

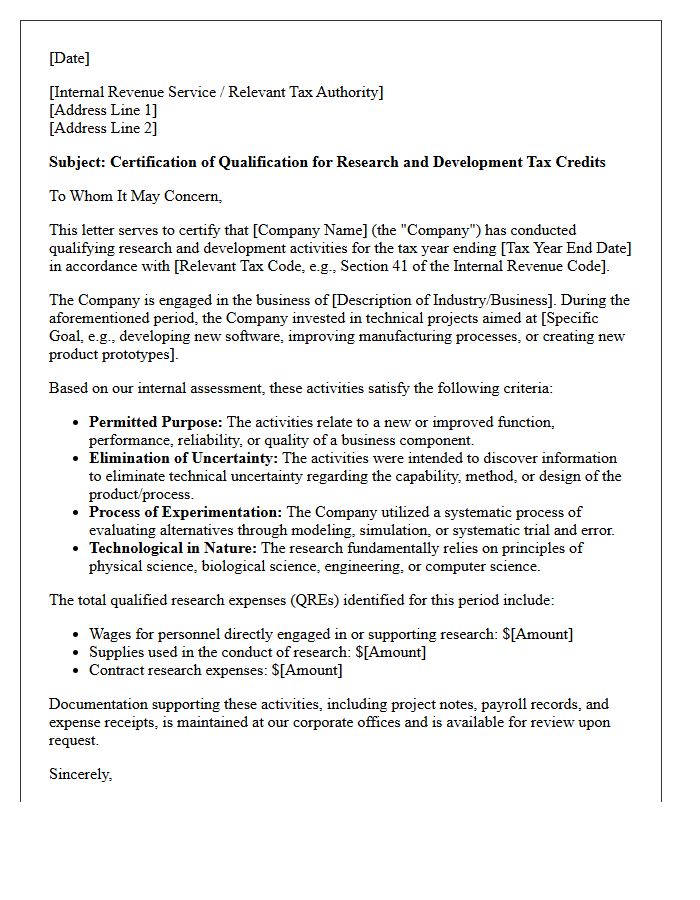

Research and Development Tax Credit Qualification Letter

A Research and Development Tax Credit Qualification Letter is a formal document substantiating that a company's activities meet specific IRS eligibility criteria. This letter serves as critical audit protection by documenting the technical nature of projects and their associated costs. It must detail how the work satisfies the Four-Part Test, focusing on innovation, technical uncertainty, and experimentation. Having this professional assessment ensures that businesses can confidently claim tax incentives while maintaining rigorous compliance standards during financial reviews or government inquiries.

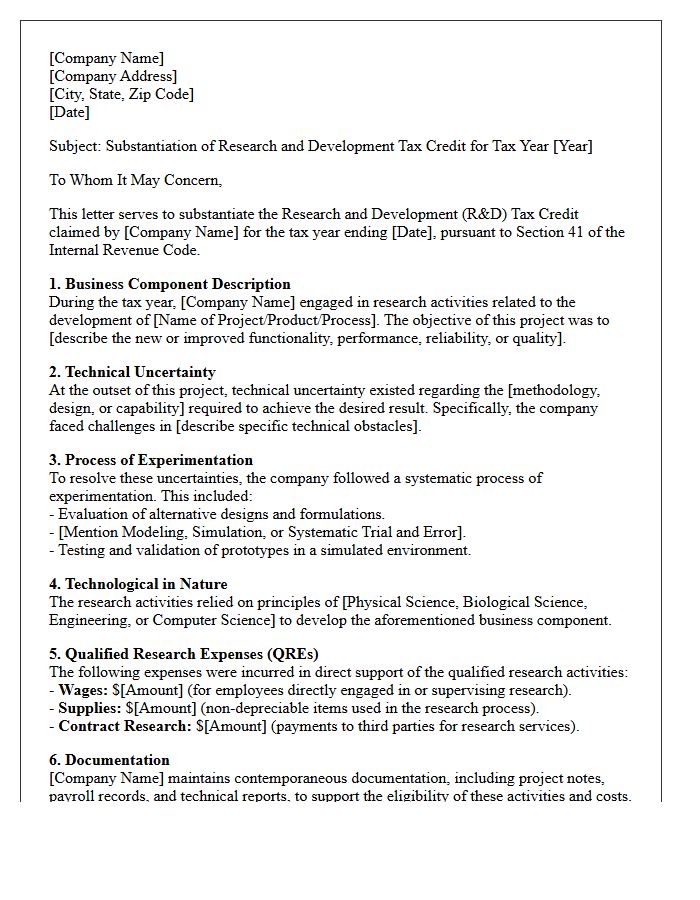

Research and Development Tax Credit Substantiation Letter

A Research and Development Tax Credit Substantiation Letter serves as critical contemporaneous documentation to validate your claim during an IRS audit. This formal document must detail how specific activities meet the four-part test, linking qualified research expenses directly to technical challenges. It provides a narrative bridge between financial data and engineering efforts, proving that projects involved technical uncertainty and a process of experimentation. Maintaining this evidence is essential to protect your tax savings and ensure full compliance with Section 41 regulations regarding eligibility and project nexus.

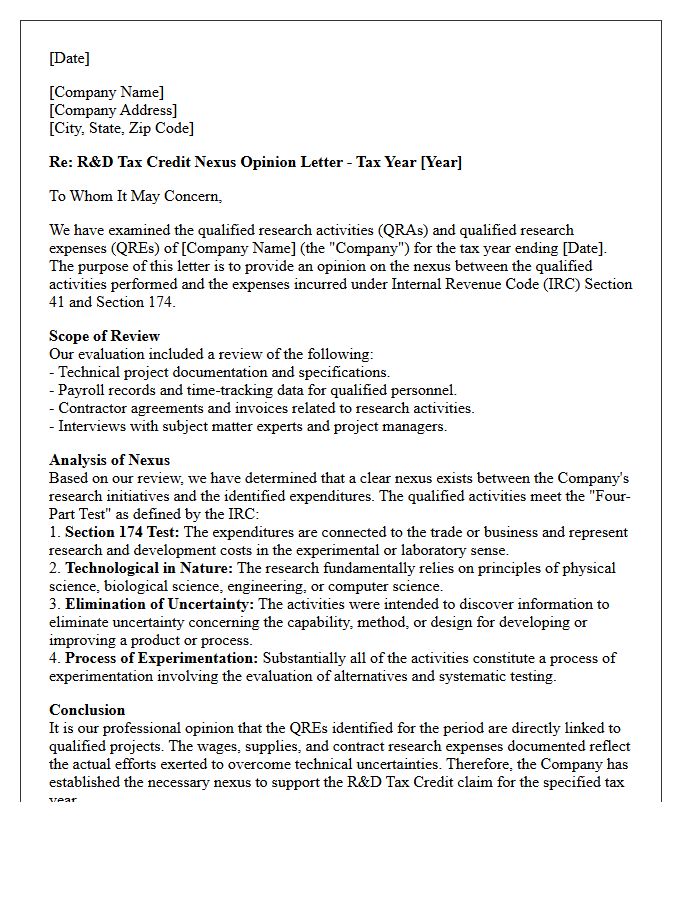

Research and Development Tax Credit Nexus Opinion Letter

A Research and Development Tax Credit Nexus Opinion Letter is a critical compliance document that establishes a direct link between qualified research activities and eligible expenses. It provides legal substantiation by detailing how specific employee roles and technical projects meet statutory requirements. This formal letter acts as a primary defense during audits, ensuring the tax credit is supported by technical facts rather than just financial data. By validating the nexus between innovation and investment, it protects the integrity of the claim and minimizes financial risk for the business.

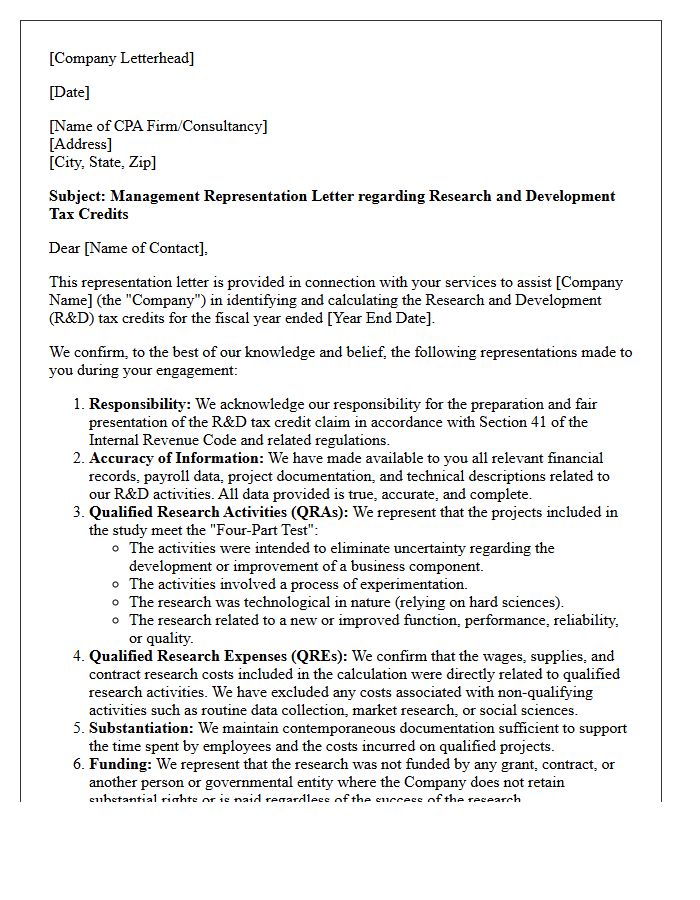

Research and Development Tax Credit Management Representation Letter

A Research and Development Tax Credit Management Representation Letter is a mandatory document signed by company executives during a tax study. It serves as official certification that all financial data, project descriptions, and employee wage allocations provided to advisors are accurate. By signing, management confirms they have supplied all relevant records and take full responsibility for the integrity of the R&D claim. This letter protects practitioners and fulfills IRS requirements, ensuring the tax credit reflects qualified research activities conducted by the business during the specified fiscal period.

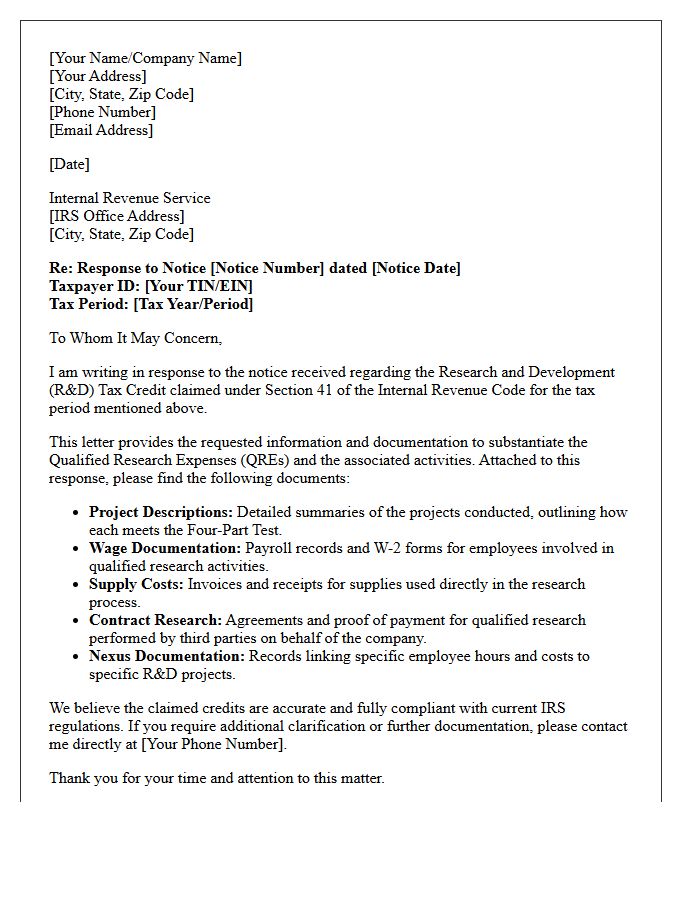

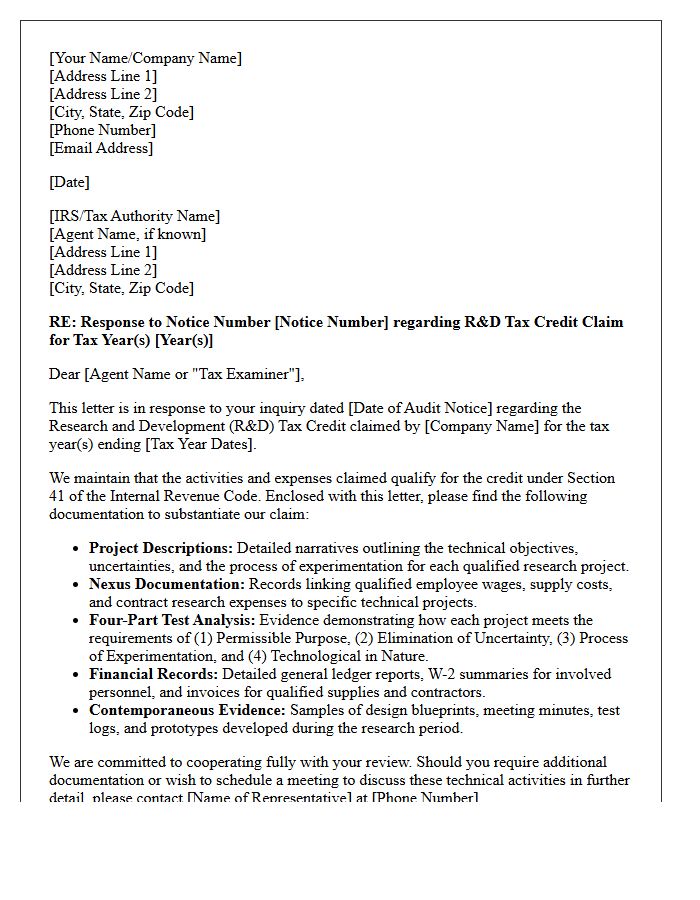

Internal Revenue Service Research and Development Tax Credit Response Letter

An Internal Revenue Service Research and Development Tax Credit Response Letter is a formal notification regarding your R&D claim. This document typically confirms receipt, requests additional documentation, or outlines a pre-refund examination to verify qualified expenses. It is crucial to respond promptly with detailed technical reports and financial records to substantiate your activities. Failure to provide contemporaneous documentation can lead to credit denial or penalties. Timely communication ensures the IRS can validate your innovation claims and process the tax offset or refund efficiently according to current federal regulations.

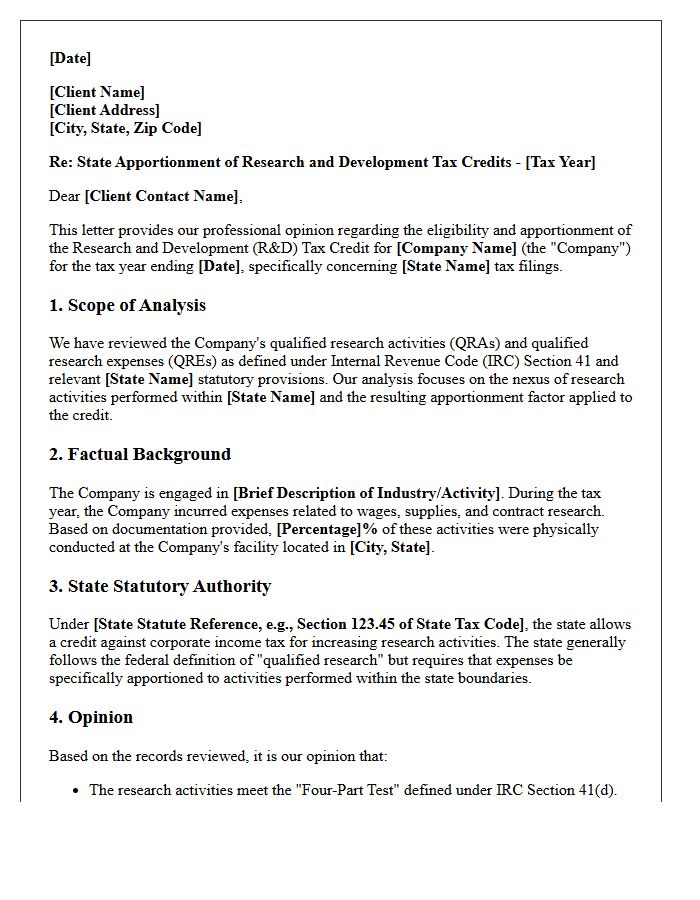

State Apportionment Research and Development Tax Credit Opinion Letter

A State Apportionment Research and Development Tax Credit Opinion Letter provides a legal framework for taxpayers to substantiate R&D claims across multiple jurisdictions. This formal document evaluates how qualified research expenses align with specific state statutes, ensuring compliance with complex nexus and apportionment rules. It serves as a vital defense during audits by providing a technical analysis of the taxpayer's methodology. Securing a professional opinion letter helps mitigate financial risk, optimizes state-level tax savings, and confirms that the allocation of credits accurately reflects regional business activities and statutory requirements.

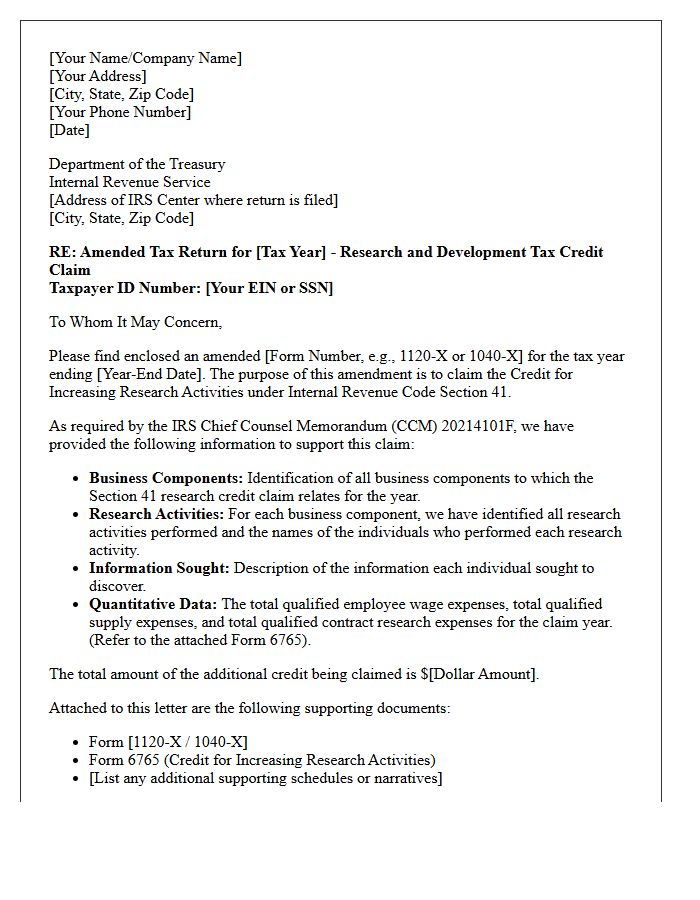

Amended Return Research and Development Tax Credit Letter

An Amended Return Research and Development Tax Credit Letter is a formal notification from the IRS regarding your claim for tax refunds related to qualifying business innovation. This letter often requests specific documentation to verify Qualified Research Expenses (QREs) and ensure compliance with Section 41. It is essential to provide detailed contemporaneous records and technical project descriptions to substantiate your activities. Timely and accurate responses are critical to successfully securing your R&D tax credits and avoiding potential audits or claim denials during the federal review process.

Research and Development Tax Credit Audit Defense Letter

A Research and Development Tax Credit Audit Defense Letter is a critical document used to justify qualified research activities during an IRS or state examination. It must provide detailed technical narratives and financial documentation that satisfy the Four-Part Test. A robust letter substantiates that your projects involved technological uncertainty and a process of experimentation. Proactively preparing this defense ensures compliance, protects your tax savings, and mitigates the risk of credit disallowance. Clear, evidence-based documentation is the strongest defense against audit challenges regarding your innovative investments.

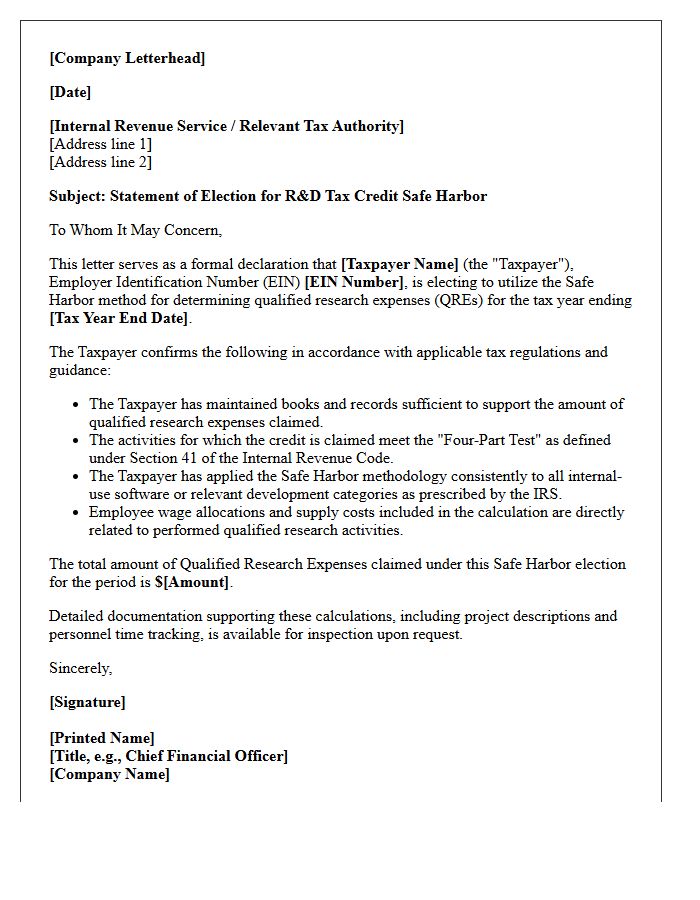

Research and Development Tax Credit Safe Harbor Letter

The Research and Development Tax Credit Safe Harbor Letter provides businesses with a crucial audit defense. This formal documentation establishes that a company's methodology for calculating QREs (Qualified Research Expenses) aligns with IRS standards. By securing this letter, taxpayers minimize the risk of credit disallowance and penalties during federal examinations. It serves as substantiation that research activities meet the four-part test, ensuring the tax benefits claimed are legally defensible and methodologically sound. Utilizing a safe harbor approach simplifies compliance and provides certainty in high-stakes tax positions.

What is a Research and Development (R&D) Tax Credit Opinion Letter?

An R&D Tax Credit Opinion Letter is a formal document issued by a tax professional or legal counsel that provides a legal evaluation and substantiation of a company's eligibility for tax credits under IRC Section 41. It serves as a defensive technical report that evaluates whether specific activities meet the IRS "Four-Part Test" and provides a professional conclusion on the sustainability of the tax position.

Why is an Opinion Letter important for R&D tax credit claims?

An Opinion Letter is critical for risk management as it establishes "reasonable cause" and "good faith," which can protect a taxpayer from accuracy-related penalties in the event of an IRS audit. It provides a structured legal framework that connects qualifying research activities (QRAs) and qualifying research expenses (QREs) to the statutory requirements of the Internal Revenue Code.

What are the core components of an R&D Tax Credit Opinion Letter?

A comprehensive Opinion Letter typically includes a detailed analysis of the taxpayer's business components, an evaluation of the research activities against the Four-Part Test, a breakdown of qualified costs (wages, supplies, and contract research), and a discussion of relevant judicial precedents and Treasury Regulations that support the credit calculation.

Who should draft an R&D Tax Credit Opinion Letter?

The letter should be drafted by qualified tax attorneys or specialized R&D tax consultants who possess both the technical expertise to understand the scientific processes and the legal expertise to interpret evolving tax laws. Having an independent third party draft the letter adds a layer of objectivity and professional authority to the tax filing.

Does an Opinion Letter guarantee that the IRS will approve the R&D credit?

No, an Opinion Letter does not guarantee IRS approval; however, it significantly strengthens the taxpayer's position by providing contemporaneous documentation and legal justification. It serves as the primary line of defense during an examination, demonstrating that the credit was claimed based on a thorough legal analysis rather than a mere estimation.

Comments