A Pending Litigation and Claims Representation Letter is a formal document sent by legal counsel to auditors. It confirms ongoing lawsuits or potential liabilities that could impact a company's financial statements. Ensuring accurate reporting of legal risks is vital for corporate transparency and compliance during annual audits. To simplify your documentation process, below are some ready to use template.

Image cover: Professional Response Templates for Pending Litigation and Claims Representation Letters

Letter Samples List

- Audit Inquiry Letter Regarding Pending Litigation

- Legal Counsel Representation Letter for Claims

- Client Attorney Litigation Assessment Letter

- Management Representation Letter for Pending Claims

- Unasserted Claims and Assessments Attorney Letter

- Pending Litigation and Contingencies Confirmation Letter

- Lawyer Response Letter to Audit Inquiry

- General Counsel Litigation Update Letter

- External Legal Counsel Pending Claims Letter

- Accounting Firm Legal Representation Letter

- Auditor Request Letter for Litigation Status

- Pending Legal Action and Claims Inquiry Letter

- Contingent Liabilities and Litigation Attorney Letter

- Corporate Counsel Claims Representation Letter

- Financial Statement Pending Litigation Disclosure Letter

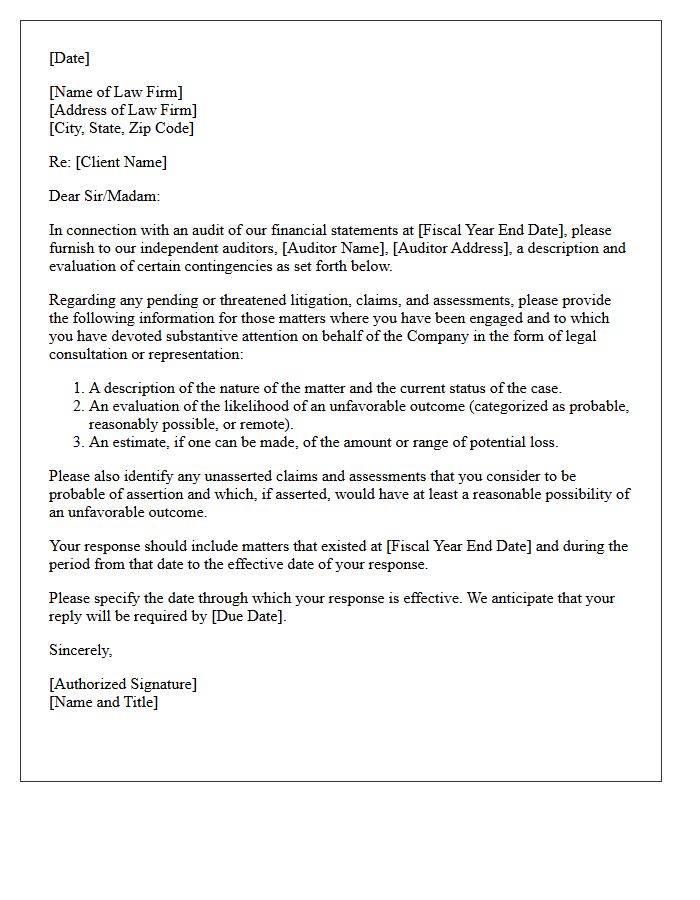

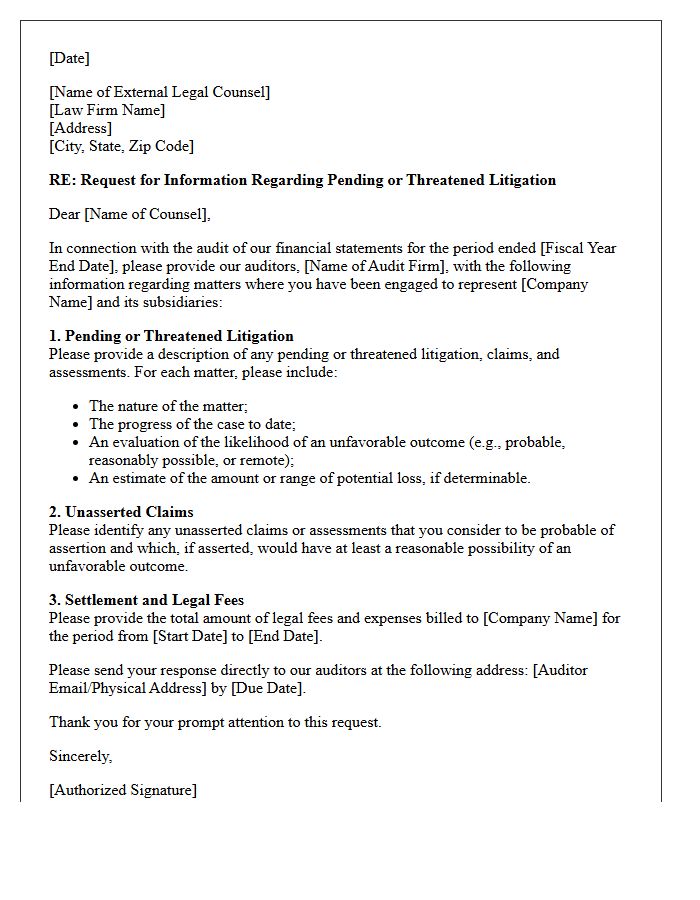

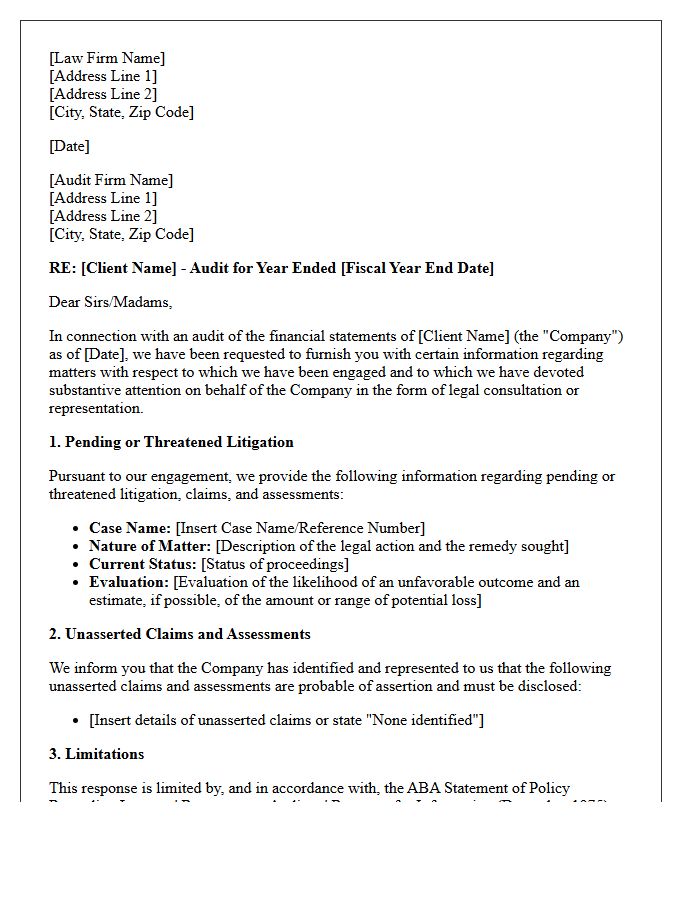

Audit Inquiry Letter Regarding Pending Litigation

An Audit Inquiry Letter is a formal request sent by a company to its legal counsel to confirm information about pending litigation. This document is essential for financial reporting, ensuring that potential liabilities and legal risks are accurately disclosed to auditors. It helps verify the status of lawsuits, the probability of unfavorable outcomes, and estimated financial impacts. Timely and precise responses from attorneys are critical to maintaining audit integrity and complying with accounting standards regarding loss contingencies and corporate transparency.

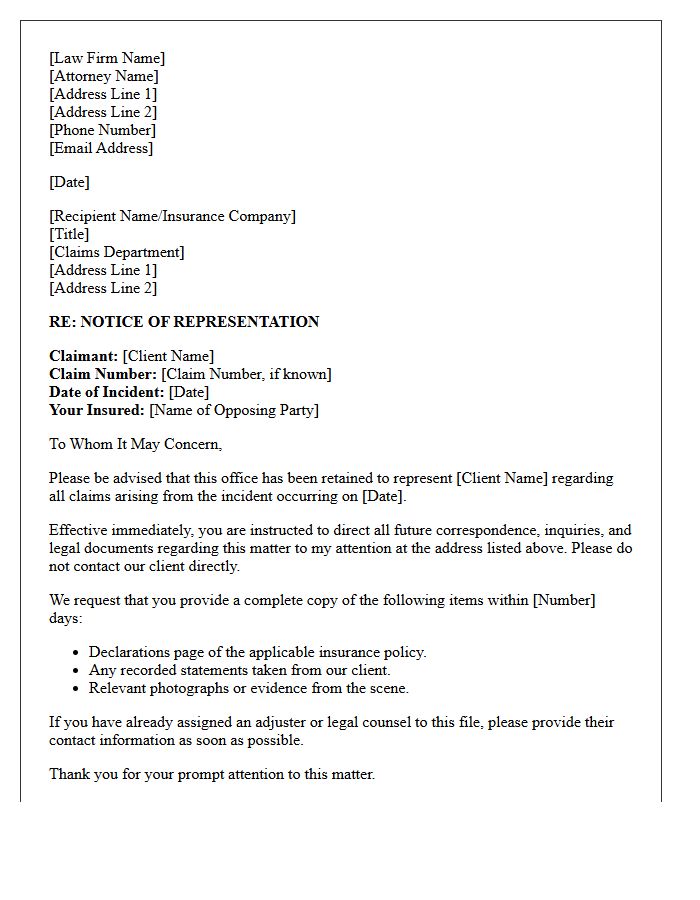

Legal Counsel Representation Letter for Claims

A Legal Counsel Representation Letter is a formal notice informing insurance companies or opposing parties that an attorney is handling your claim. This document is crucial because it legally mandates that all future communication must go through your legal representative, preventing adjusters from contacting you directly. It establishes professional oversight, protects your legal rights, and ensures that statements are managed by experts. Providing this letter is the first step in formalizing a personal injury or liability claim to secure fair compensation while avoiding self-incrimination during the settlement process.

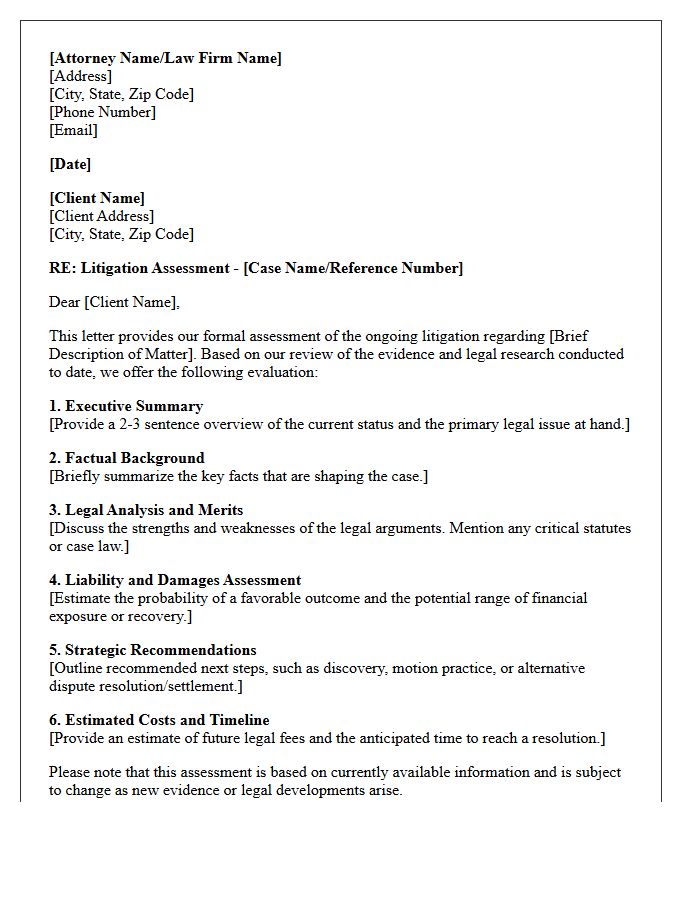

Client Attorney Litigation Assessment Letter

A Client Attorney Litigation Assessment Letter is a formal document evaluating the strengths, weaknesses, and potential outcomes of a legal dispute. It provides a strategic roadmap for decision-makers by estimating financial exposure, probability of success, and projected legal costs. This assessment ensures transparency between counsel and client, helping organizations manage risk and allocate resources effectively. By documenting the merits of the case early on, it serves as a critical tool for settlement negotiations or trial preparation, facilitating informed choices throughout the litigation lifecycle.

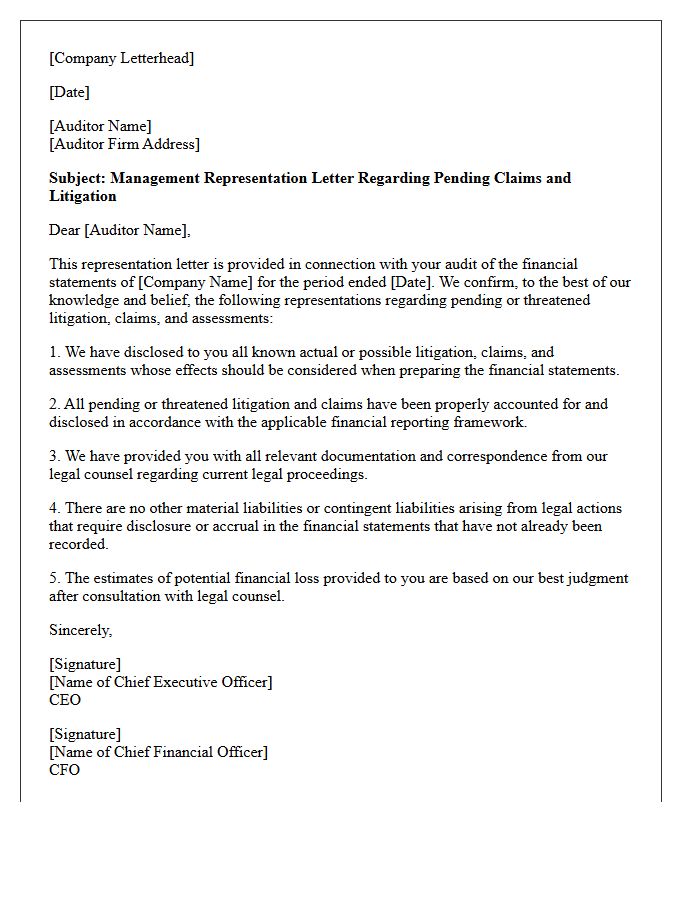

Management Representation Letter for Pending Claims

A Management Representation Letter for pending claims is a formal document provided by company leadership to external auditors. It confirms that all potential legal liabilities and outstanding litigation have been fully disclosed in the financial statements. This letter protects auditors by shifting the responsibility for the completeness of information to management. It ensures that any contingent losses that could materially impact the company's financial health are accurately recorded or noted, maintaining transparency for stakeholders and ensuring compliance with accounting standards regarding legal risks and uncertainties.

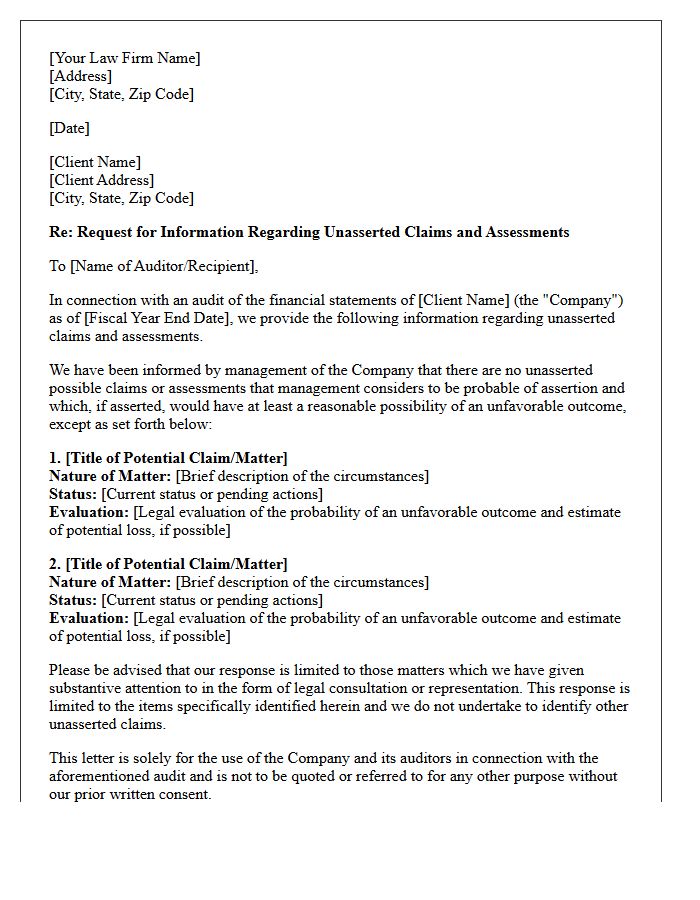

Unasserted Claims and Assessments Attorney Letter

An Unasserted Claims and Assessments Attorney Letter is a critical audit document used to identify potential legal liabilities. During financial audits, companies request their legal counsel to disclose pending litigation or probable claims that have not yet been formally filed. This process ensures transparency in financial reporting by evaluating the likelihood of unfavorable outcomes and estimating potential losses. Attorneys must carefully balance disclosure requirements with attorney-client privilege to provide auditors with an accurate assessment of a firm's contingent liabilities and overall fiscal health.

Pending Litigation and Contingencies Confirmation Letter

A Pending Litigation and Contingencies Confirmation Letter is a formal request sent by a client to their legal counsel during a financial audit. It requires attorneys to disclose potential liabilities, outstanding lawsuits, and unasserted claims that could materially impact the company's financial standing. Auditors use this document to ensure financial statement accuracy by evaluating the probability of loss and estimating potential costs. Timely and precise responses are essential to maintain compliance with accounting standards and provide transparency regarding contingent risks facing the organization.

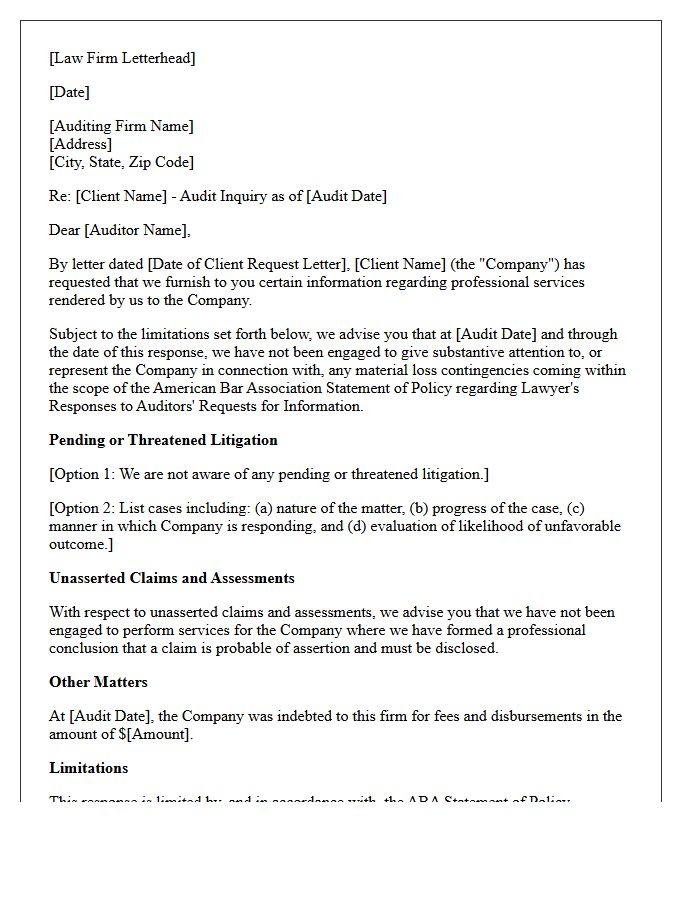

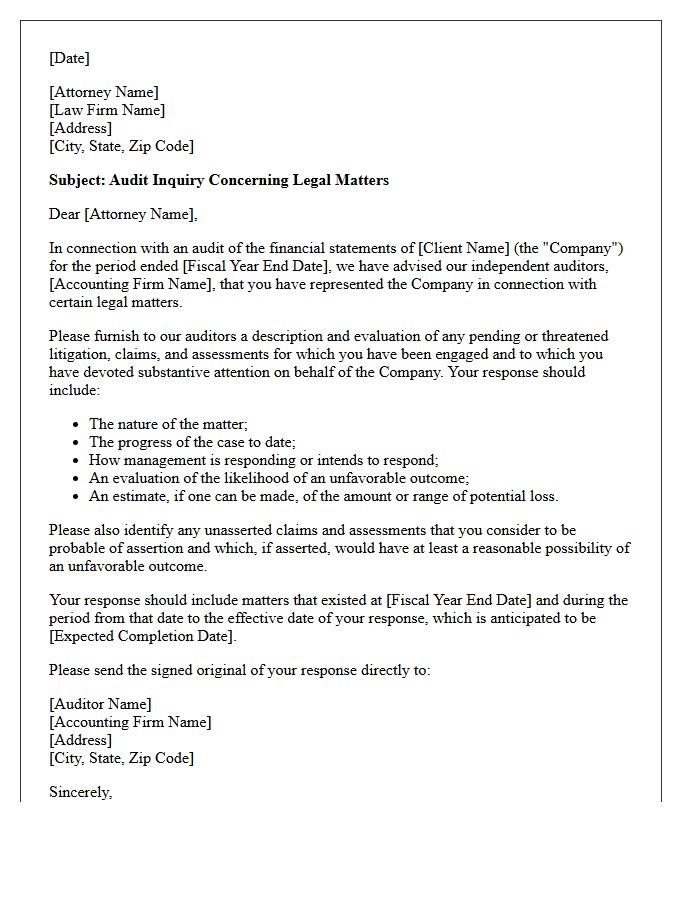

Lawyer Response Letter to Audit Inquiry

A lawyer response letter to an audit inquiry is a formal document provided to external auditors regarding a client's pending or threatened litigation. This communication is essential for evaluating a company's financial health and potential liabilities. Legal counsel discloses loss contingencies while maintaining attorney-client privilege. The response must adhere to the ABA Statement of Policy to ensure accuracy and professional compliance. Stakeholders rely on these evaluations to confirm that financial statements reflect realistic legal risks and potential settlement costs, making precise language and timely disclosure critical for corporate transparency.

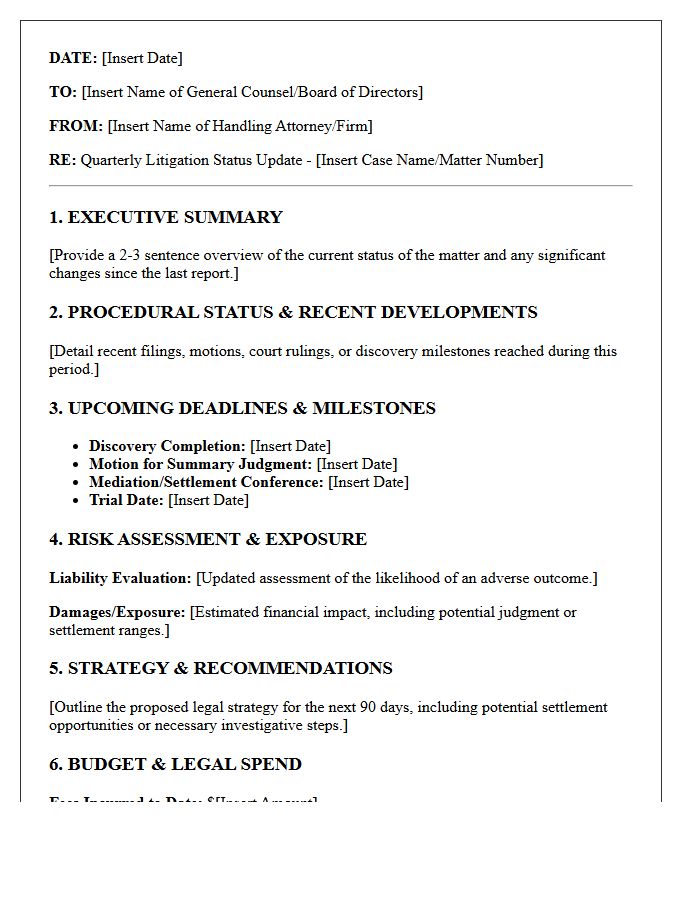

General Counsel Litigation Update Letter

A General Counsel Litigation Update Letter is a critical communication tool used to inform executive leadership about legal risks and ongoing court proceedings. It provides a strategic overview of pending lawsuits, potential financial exposure, and settlement prospects. By offering a concise summary of legal developments, these letters enable informed decision-making and ensure alignment between the legal department and corporate goals. They are essential for risk management, regulatory compliance, and maintaining transparency regarding significant liabilities that could impact the company's bottom line or reputation.

External Legal Counsel Pending Claims Letter

An External Legal Counsel Pending Claims Letter is a formal inquiry sent by auditors to a company's outside attorneys during an annual audit. This document confirms contingent liabilities by requesting details on active litigation, potential claims, and estimated financial exposure. It ensures that the financial statements accurately reflect legal risks. Management must authorize the request, but the counsel responds directly to auditors to maintain objectivity. Understanding this process is vital for regulatory compliance and transparent financial reporting regarding outstanding legal disputes.

Accounting Firm Legal Representation Letter

An accounting firm legal representation letter is a critical audit procedure used to corroborate information about pending litigation and potential liabilities. Auditors request the client's management to authorize their external legal counsel to disclose any claims or assessments that could materially impact financial statements. This document ensures audit evidence is complete regarding loss contingencies. It helps bridge the information gap between a company's legal risks and its financial reporting accuracy, protecting stakeholders by ensuring all significant legal threats are appropriately disclosed or accrued in the annual report.

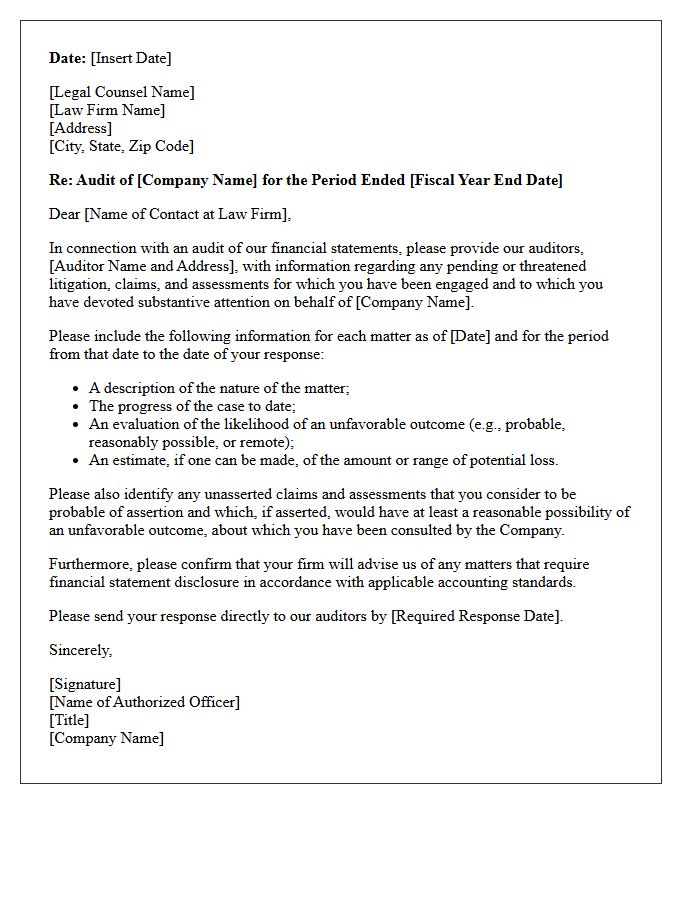

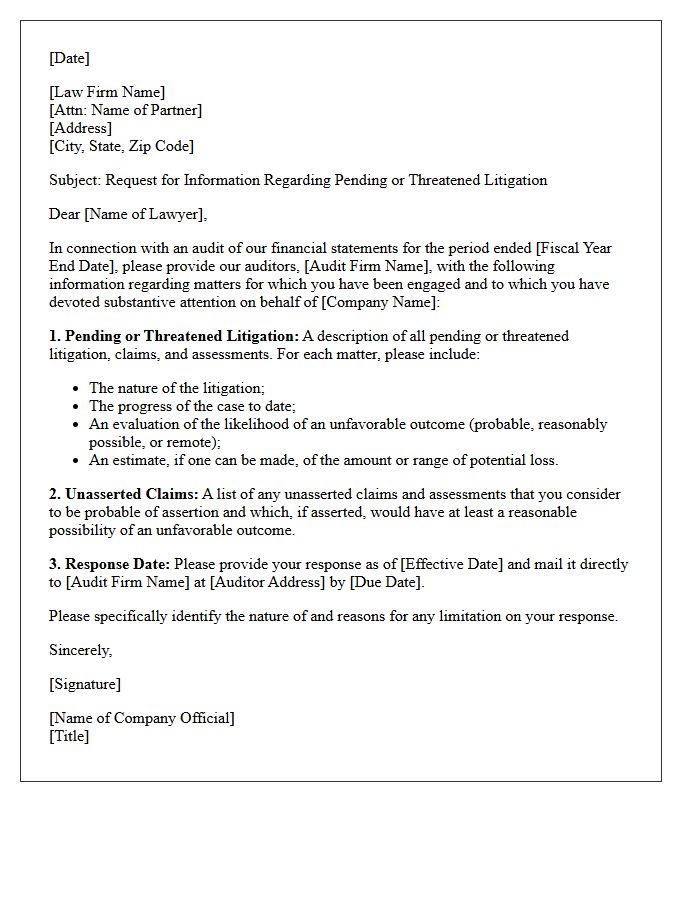

Auditor Request Letter for Litigation Status

An Auditor Request Letter for litigation status is a formal inquiry sent by a company to its legal counsel. It asks attorneys to disclose pending or threatened legal claims that could materially impact the organization's financial statements. This process is essential for financial reporting accuracy and compliance with auditing standards. The letter requires lawyers to evaluate the probability of an unfavorable outcome and estimate potential financial losses. Providing this information ensures transparency for stakeholders and helps auditors verify that all significant liabilities are appropriately recognized or disclosed in the year-end report.

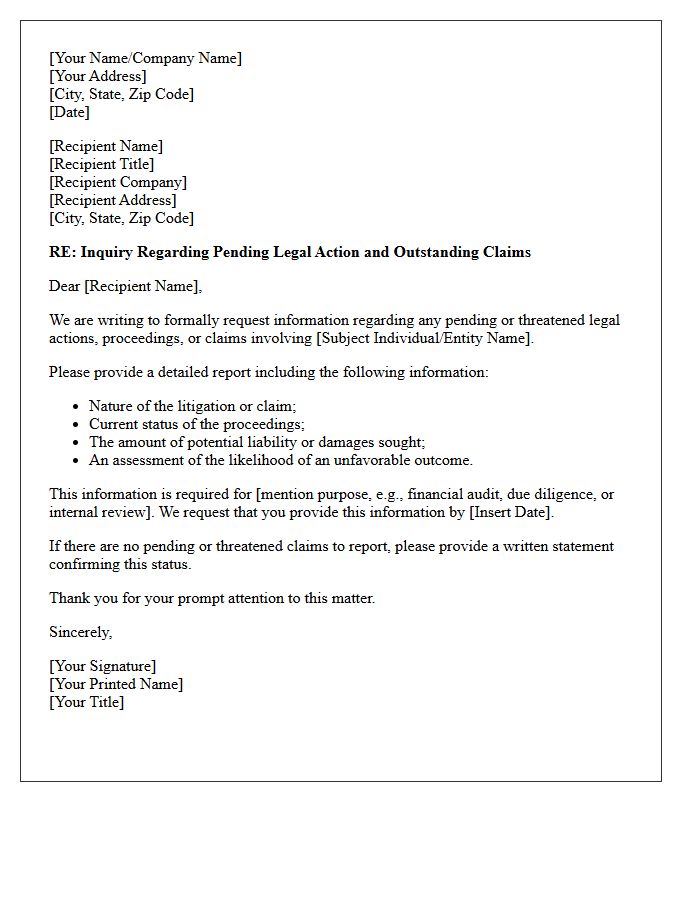

Pending Legal Action and Claims Inquiry Letter

A Pending Legal Action and Claims Inquiry Letter is a formal document used during financial audits to confirm potential liabilities. It requests legal counsel to disclose any unasserted claims, active lawsuits, or assessments that could financially impact a company. This letter is crucial for ensuring financial statement accuracy and transparency. Auditors rely on these responses to evaluate contingent liabilities, ensuring all significant legal risks are properly documented. Timely and precise communication between management, auditors, and legal representatives is essential to maintain regulatory compliance and stakeholder trust.

Contingent Liabilities and Litigation Attorney Letter

A contingent liability is a potential financial obligation depending on the outcome of future events, such as lawsuits. To ensure accurate financial reporting, auditors request a litigation attorney letter. This formal inquiry requires legal counsel to evaluate pending claims, estimate potential losses, and determine the probability of an unfavorable ruling. This process is essential for transparency, as it helps stakeholders understand legal risks that could materially impact a company's balance sheet or overall fiscal health.

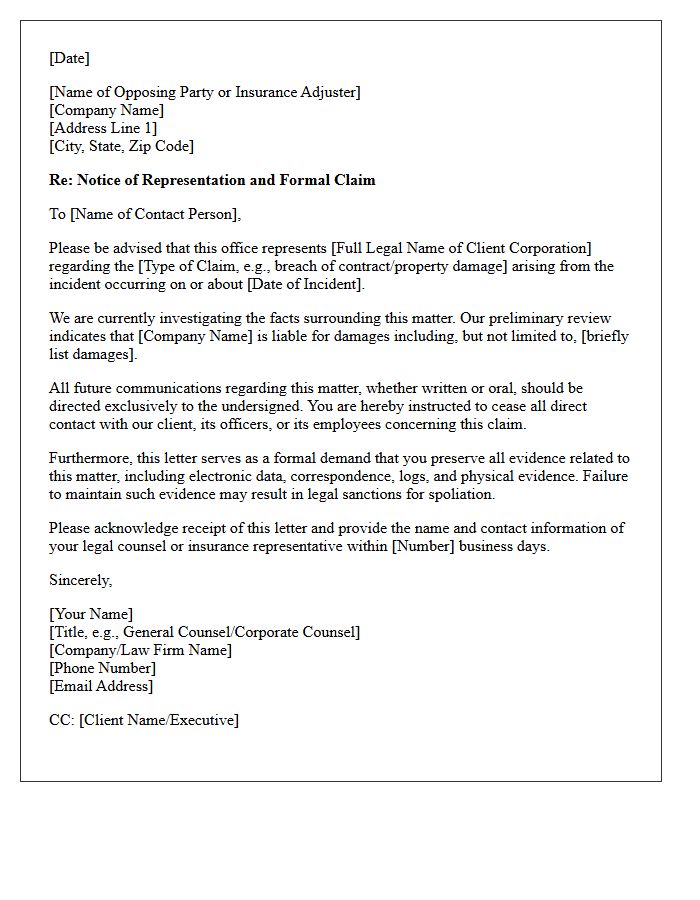

Corporate Counsel Claims Representation Letter

A Corporate Counsel Claims Representation Letter is a formal legal document issued to confirm that an attorney represents a business entity in a specific legal matter. This letter serves as official notice to opposing parties or insurance carriers, directing all future communications through legal counsel to protect the organization's rights. It establishes a clear chain of command, ensures attorney-client privilege is maintained, and prevents direct contact with company employees. Providing this notice is a critical step in managing corporate liability and streamlining the claims resolution process effectively.

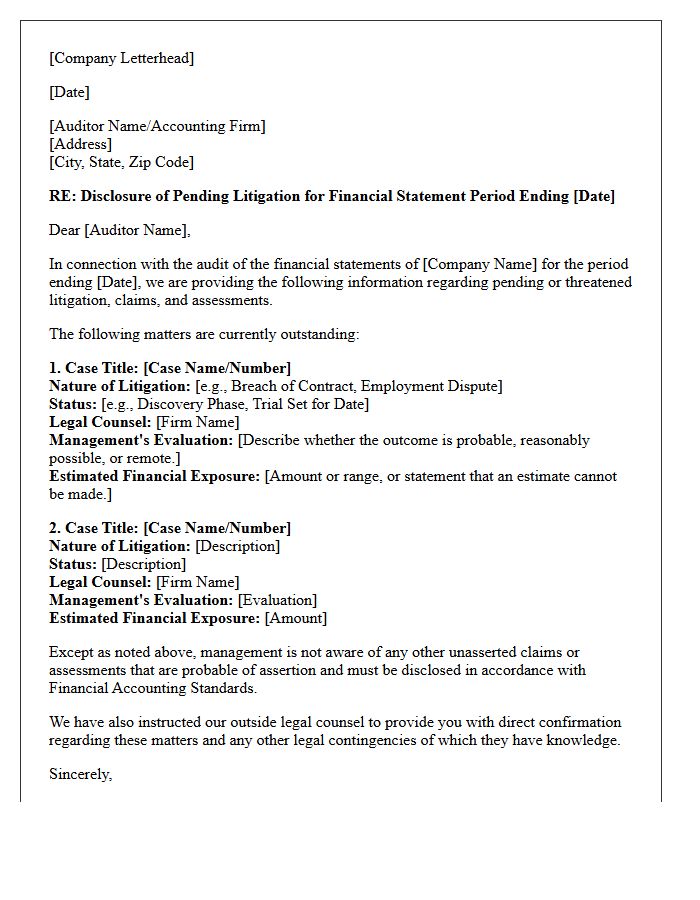

Financial Statement Pending Litigation Disclosure Letter

A financial statement pending litigation disclosure letter is a formal document provided by legal counsel to auditors. It assesses contingent liabilities arising from ongoing or threatened lawsuits. This letter is crucial for financial transparency, as it helps determine if potential legal losses must be accrued or disclosed in the footnotes. By evaluating the probability of an unfavorable outcome and estimating potential costs, the document ensures that the company's financial health is accurately represented to investors and regulatory bodies according to accounting standards.

What is a Pending Litigation and Claims Representation Letter?

A Pending Litigation and Claims Representation Letter is a formal document sent by a company's management to its legal counsel, requesting that the attorney provide information directly to the company's external auditors regarding existing or potential legal liabilities.

What is the primary purpose of a legal representation letter in an audit?

The primary purpose is to provide independent audit evidence regarding the completeness and accuracy of management's assertions concerning litigation, claims, and assessments that may materially impact the company's financial statements.

What information is typically included in a litigation representation letter?

The letter typically includes a list of pending or threatened litigation, a description of the nature of each case, the progress of the proceedings, and the attorney's evaluation of the likelihood of an unfavorable outcome and an estimate of potential loss.

Why do auditors require a direct response from a company's legal counsel?

Auditors require a direct response to satisfy professional auditing standards (such as AU-C Section 501), ensuring that information about legal risks is corroborated by a knowledgeable third party rather than relying solely on internal management representations.

What happens if a lawyer refuses to provide a representation letter?

If a lawyer refuses to furnish the requested information, it is considered a limitation on the scope of the audit. This may lead the auditor to modify their audit opinion, potentially resulting in a qualified opinion or a disclaimer of opinion.

Comments