An Uncorrected Misstatements Representation Letter is a formal document where management confirms that unadjusted audit differences are immaterial to the financial statements. This letter is a critical component of audit documentation, ensuring accountability for financial reporting accuracy and compliance with auditing standards. To help you streamline your audit process, below are some ready to use template.

Image cover: Guide to Uncorrected Misstatements: Representation Letter Templates and Samples

Letter Samples List

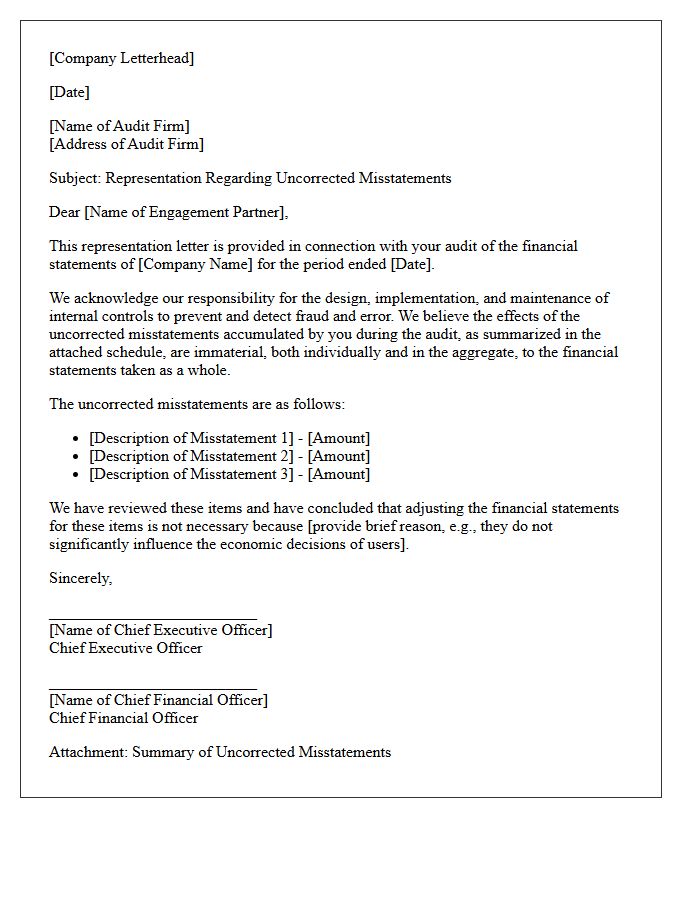

- Management Representation Letter For Uncorrected Misstatements

- Immaterial Unadjusted Differences Representation Letter

- Summary Of Uncorrected Misstatements Audit Letter

- Passed Adjustments Client Acknowledgment Letter

- Financial Statement Uncorrected Errors Representation Letter

- Aggregated Unadjusted Misstatements Evaluation Letter

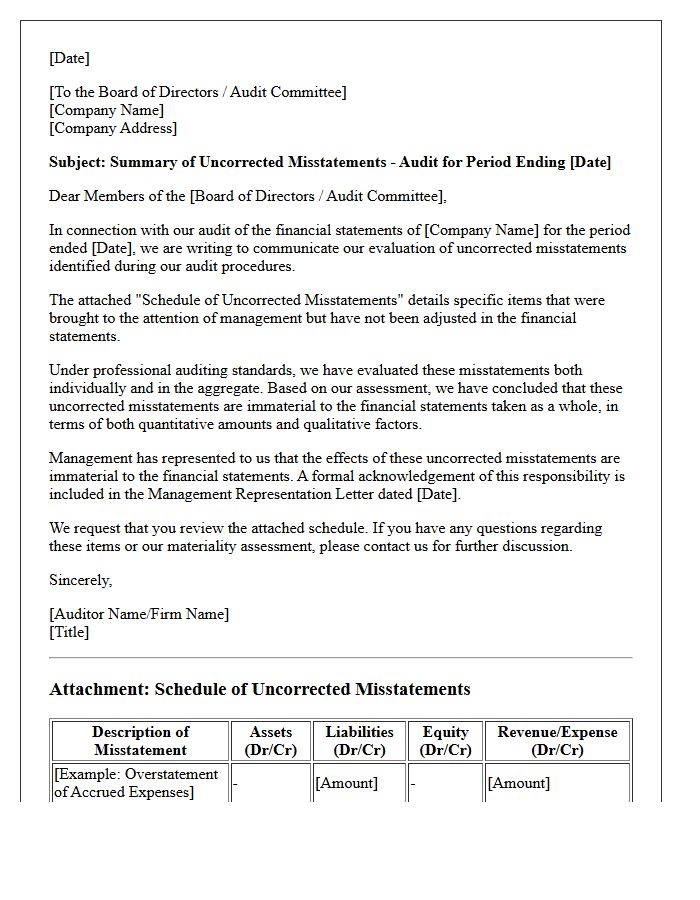

- Audit Committee Uncorrected Misstatements Communication Letter

- Schedule Of Uncorrected Audit Differences Representation Letter

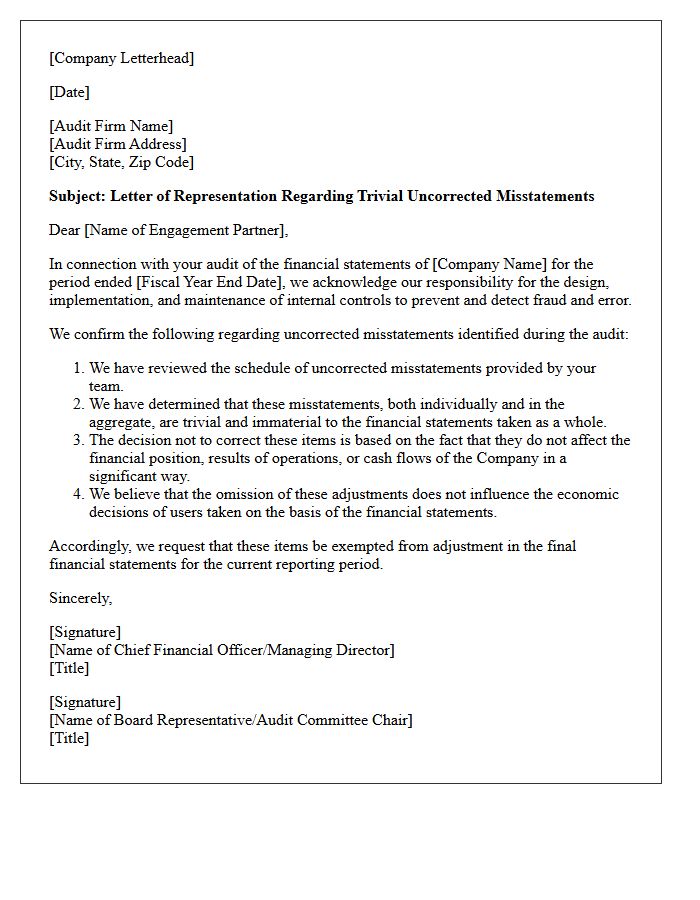

- Trivial Uncorrected Misstatements Exemption Letter

- Auditor Evaluation Of Uncorrected Misstatements Letter

- Accumulated Uncorrected Misstatements Representation Letter

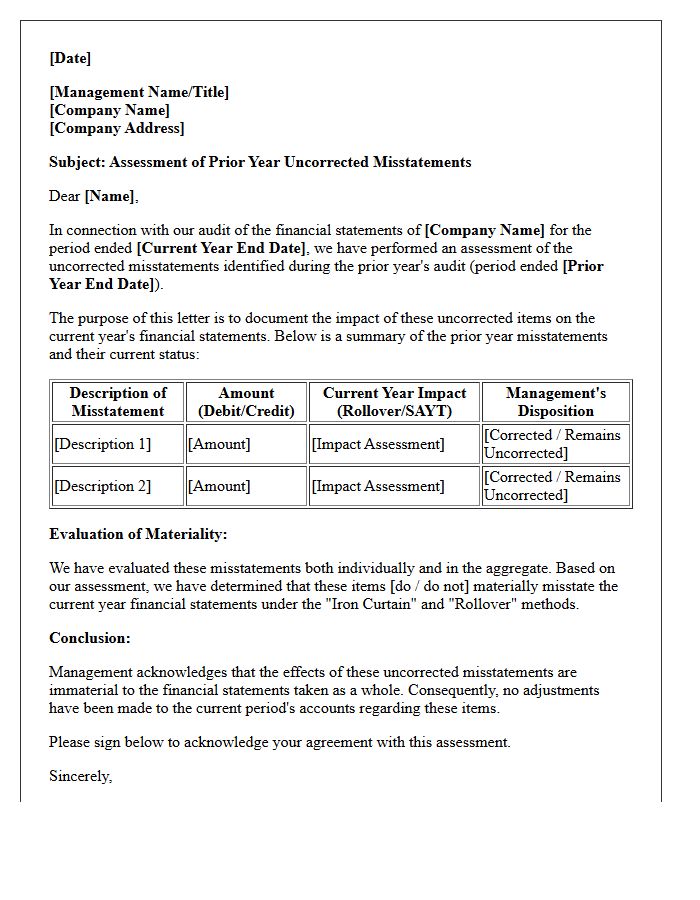

- Prior Year Uncorrected Misstatements Assessment Letter

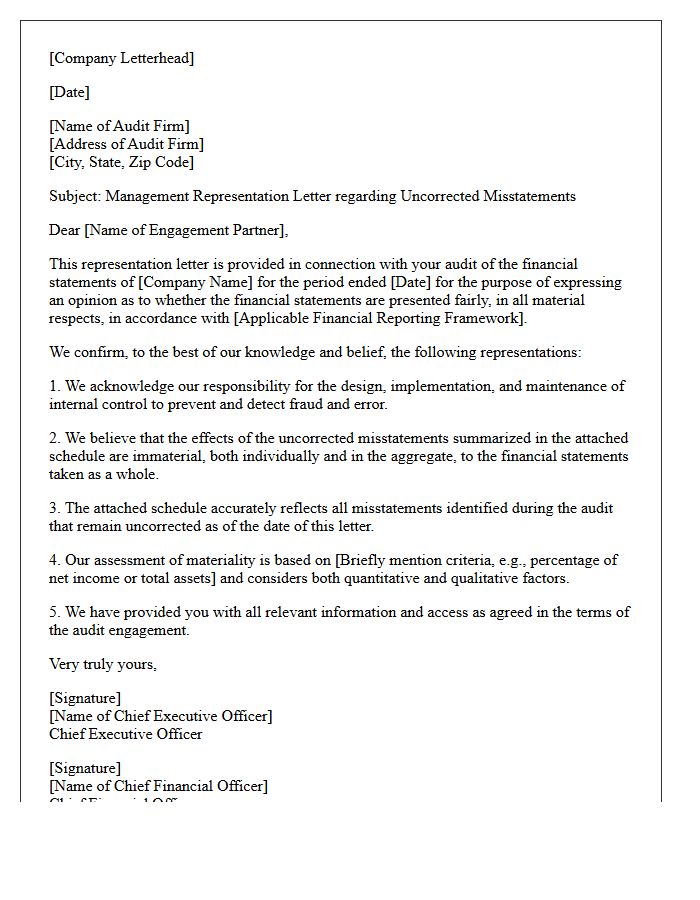

Management Representation Letter For Uncorrected Misstatements

A Management Representation Letter for uncorrected misstatements is a formal document where management confirms that the effects of unadjusted audit differences are immaterial to the financial statements as a whole. This letter serves as critical audit evidence, shifting the primary responsibility for financial accuracy to the entity's leadership. It ensures that those in charge have reviewed the summary of uncorrected misstatements and explicitly acknowledge that no further adjustments are necessary for a fair presentation, thereby protecting the auditor's opinion from potential future claims regarding omitted errors.

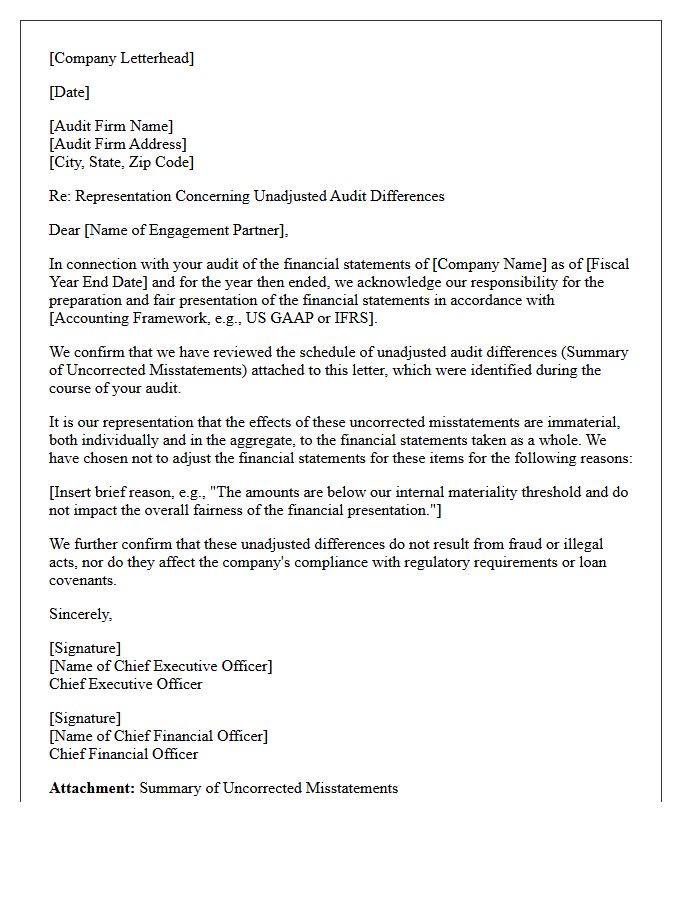

Immaterial Unadjusted Differences Representation Letter

An Immaterial Unadjusted Differences Representation Letter is a formal document where management confirms that uncorrected financial misstatements are immaterial to the overall financial statements. During an audit, if errors are discovered but not adjusted, management must provide this written representation to auditors. It ensures management accepts responsibility for the accuracy and integrity of the reported figures. This letter serves as critical audit evidence, documenting that any omissions or inaccuracies, individually or in aggregate, do not mislead stakeholders or significantly impact the company's financial position or performance outcomes.

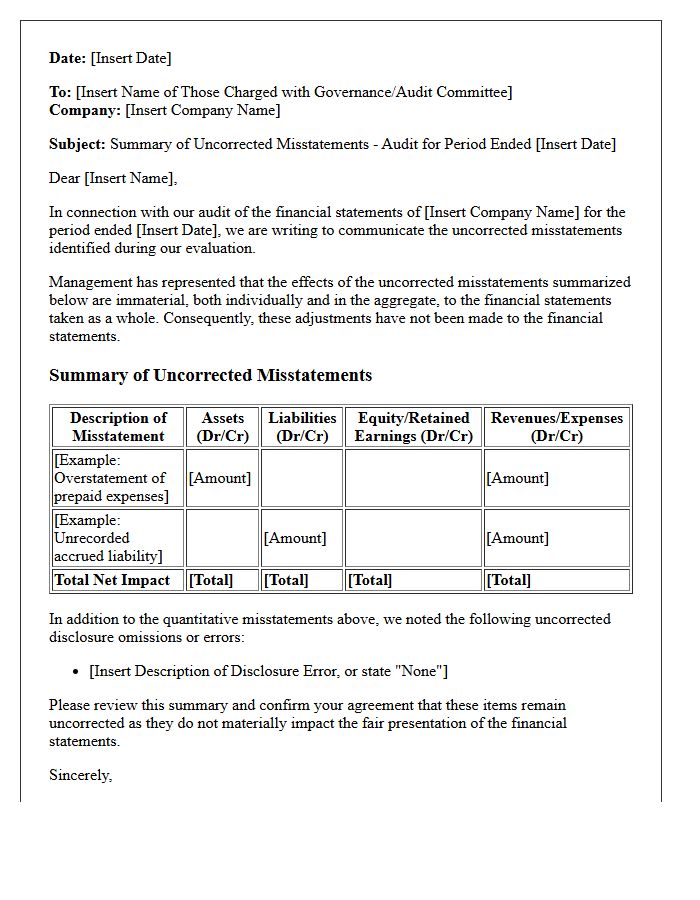

Summary Of Uncorrected Misstatements Audit Letter

A Summary of Uncorrected Misstatements is a critical audit document listing financial errors identified during an audit that management has declined to record. The auditor evaluates whether these aggregated misstatements are material, meaning they could influence the economic decisions of stakeholders. If the total uncorrected amount remains below the materiality threshold, the auditor may still issue a clean opinion. Management must provide a written representation confirming their belief that these effects are immaterial to the overall financial statements, ensuring transparency and accountability in reporting.

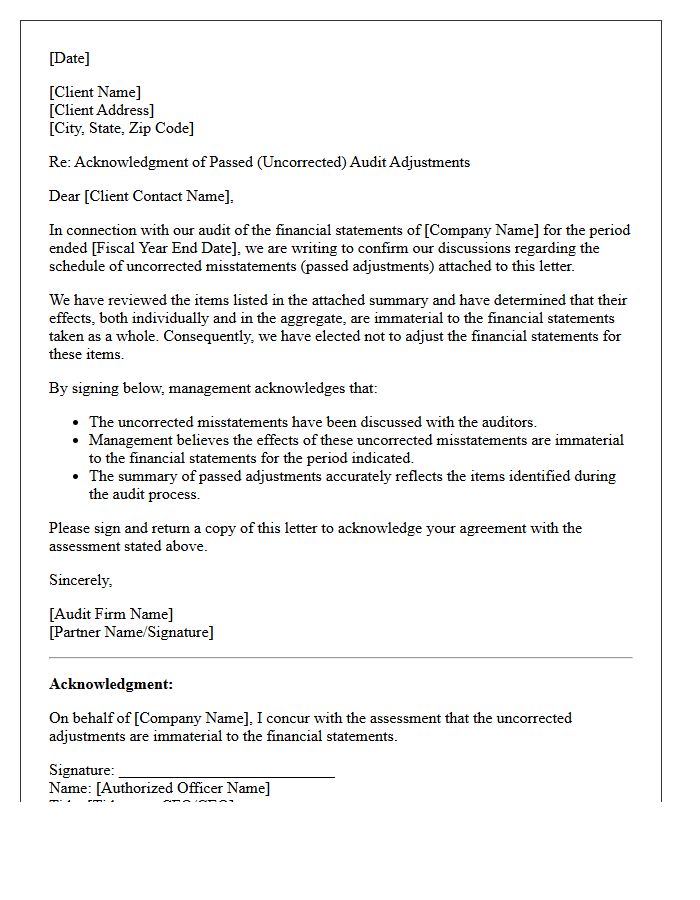

Passed Adjustments Client Acknowledgment Letter

A Passed Adjustments Client Acknowledgment Letter is a formal document where management confirms their decision not to record specific audit misstatements. This letter verifies that any immaterial financial discrepancies identified during an audit do not significantly distort the company's financial position. By signing, the client accepts responsibility for these uncorrected items, ensuring transparency and aligning expectations between the auditor and management. It serves as crucial audit evidence, protecting both parties by documenting that all identified adjustments were evaluated and deemed negligible for the overall financial reporting accuracy.

Financial Statement Uncorrected Errors Representation Letter

A Financial Statement Uncorrected Errors Representation Letter is a formal document where management confirms that uncorrected misstatements identified by auditors are immaterial to the overall financial health. This letter is crucial for audit compliance, as it shifts the responsibility for reported figures from the auditor to company leadership. By signing, management acknowledges that any passed adjustments do not significantly distort the fair presentation of the financial position. It serves as a vital safeguard, ensuring transparency and legal accountability regarding the accuracy of final disclosures within the annual report.

Aggregated Unadjusted Misstatements Evaluation Letter

An Aggregated Unadjusted Misstatements Evaluation Letter is a critical audit document summarizing uncorrected financial errors. It helps management and auditors assess whether the total cumulative effect of these discrepancies is material to the financial statements. Even if individual items seem minor, their combined impact could distort the company's true financial position. Management must formally acknowledge these immaterial misstatements and confirm that adjustments are unnecessary. This process ensures transparency, maintains reporting integrity, and provides a clear trail of professional judgment during the year-end audit conclusion phase.

Audit Committee Uncorrected Misstatements Communication Letter

The Audit Committee Uncorrected Misstatements Communication Letter is a formal report issued by external auditors to those charged with governance. It details identified financial errors that management has chosen not to adjust, as they are deemed immaterial to the overall financial statements. This communication ensures transparency, allowing the committee to evaluate the cumulative impact of these misstatements on financial integrity and internal controls. Understanding these uncorrected items is essential for fulfilling fiduciary oversight and ensuring the accuracy of financial reporting standards.

Schedule Of Uncorrected Audit Differences Representation Letter

The Schedule of Uncorrected Audit Differences (SUAD) is a critical component of the management representation letter. It lists identified misstatements that the auditor found but the company chose not to adjust. Management must formally acknowledge these items, explicitly declaring that any uncorrected errors are immaterial to the financial statements' overall integrity. This document ensures accountability and provides legal protection for auditors by confirming that management accepts responsibility for the final reported figures despite the noted discrepancies.

Trivial Uncorrected Misstatements Exemption Letter

The Trivial Uncorrected Misstatements Exemption Letter confirms that specific financial errors identified during an audit remain unadjusted. These items are considered immaterial, meaning their omission does not influence the economic decisions of stakeholders. Auditors establish a threshold below which misstatements are clearly trivial and do not require aggregation. Management must formally acknowledge these discrepancies in a representation letter, asserting that the financial statements still present a true and fair view. This process streamlines reporting by focusing solely on significant accounting inaccuracies that impact overall financial integrity.

Auditor Evaluation Of Uncorrected Misstatements Letter

The Auditor Evaluation of Uncorrected Misstatements Letter is a critical governance document that details identified financial errors that management has declined to adjust. Auditors assess whether these aggregated misstatements are material, either individually or in total, potentially impacting the reliability of financial statements. Management must provide a written representation confirming their belief that these uncorrected items are immaterial to the overall financial position. This process ensures transparency between auditors and those charged with governance, maintaining the integrity of reported financial data and ensuring compliance with professional auditing standards.

Accumulated Uncorrected Misstatements Representation Letter

The Accumulated Uncorrected Misstatements represent financial errors identified during an audit that management chooses not to adjust. A critical component of the Representation Letter is the formal acknowledgment by management that these uncorrected items are immaterial, both individually and in the aggregate, to the financial statements. This document serves as legal confirmation of management's responsibility for financial accuracy. Auditors must evaluate whether these omissions affect the overall audit opinion and ensure the Schedule of Uncorrected Misstatements is accurately attached and signed by authorized personnel.

Prior Year Uncorrected Misstatements Assessment Letter

A Prior Year Uncorrected Misstatements Assessment Letter is a critical audit document that evaluates the cumulative effect of past financial errors. It tracks immaterial discrepancies from previous periods to ensure they do not aggregate into a material misstatement in the current year. Auditors use this assessment to determine if historical inaccuracies now require adjusting entries to maintain financial integrity. Understanding these carryover effects is essential for accurate financial reporting and ensuring that the overall balance sheet reflects a true and fair view of the entity's current economic position.

What is an Uncorrected Misstatements Representation Letter?

An Uncorrected Misstatements Representation Letter is a formal document provided by management to external auditors confirming that any identified financial errors or omissions not adjusted in the books are considered immaterial, both individually and in the aggregate, to the financial statements taken as a whole.

Why do auditors require a management representation regarding uncorrected misstatements?

Auditors require this representation to fulfill professional auditing standards (such as ISA 450 or AS 2810), ensuring management acknowledges its responsibility for the financial statements and agrees that the excluded adjustments do not distort the company's true financial position.

What must be included in the schedule of uncorrected misstatements?

The schedule, often attached to the representation letter, must include a detailed list of all detected misstatements-other than those deemed clearly trivial-including their specific impact on assets, liabilities, equity, income, and expenses.

What happens if management refuses to sign the Uncorrected Misstatements Representation Letter?

If management refuses to sign the letter, it constitutes a scope limitation. The auditor may be unable to issue an unqualified opinion and may need to withdraw from the engagement or issue a qualified or disclaimer of opinion due to the lack of written evidence regarding management's accountability.

How does materiality influence the Uncorrected Misstatements Representation Letter?

Materiality is the threshold used to determine if a misstatement is significant enough to influence the decisions of stakeholders; the letter specifically addresses items that fall below this threshold but above the "clearly trivial" limit, documenting the justification for not adjusting them.

Comments