A Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify the accuracy of a client's cash holdings. This essential procedure ensures financial transparency and validates reported assets during an official audit. It helps prevent fraud and reconciles internal records with bank statements. To simplify your documentation process, below are some ready to use templates.

Image cover: Bank Confirmation Letter Guide: Audit Request Templates and Samples

Letter Samples List

- Standard Deposit Account Balance Audit Confirmation Letter

- Corporate Deposit Account Balance Audit Confirmation Letter

- Blank Deposit Account Balance Audit Confirmation Letter

- External Audit Deposit Account Balance Confirmation Letter

- Internal Audit Deposit Account Balance Confirmation Letter

- Fixed Deposit Account Balance Audit Confirmation Letter

- Savings Deposit Account Balance Audit Confirmation Letter

- Foreign Currency Deposit Account Balance Audit Confirmation Letter

- Year-End Deposit Account Balance Audit Confirmation Letter

- Interim Deposit Account Balance Audit Confirmation Letter

- Joint Deposit Account Balance Audit Confirmation Letter

- Escrow Deposit Account Balance Audit Confirmation Letter

- Trust Deposit Account Balance Audit Confirmation Letter

- Zero Balance Deposit Account Audit Confirmation Letter

- Closed Deposit Account Balance Audit Confirmation Letter

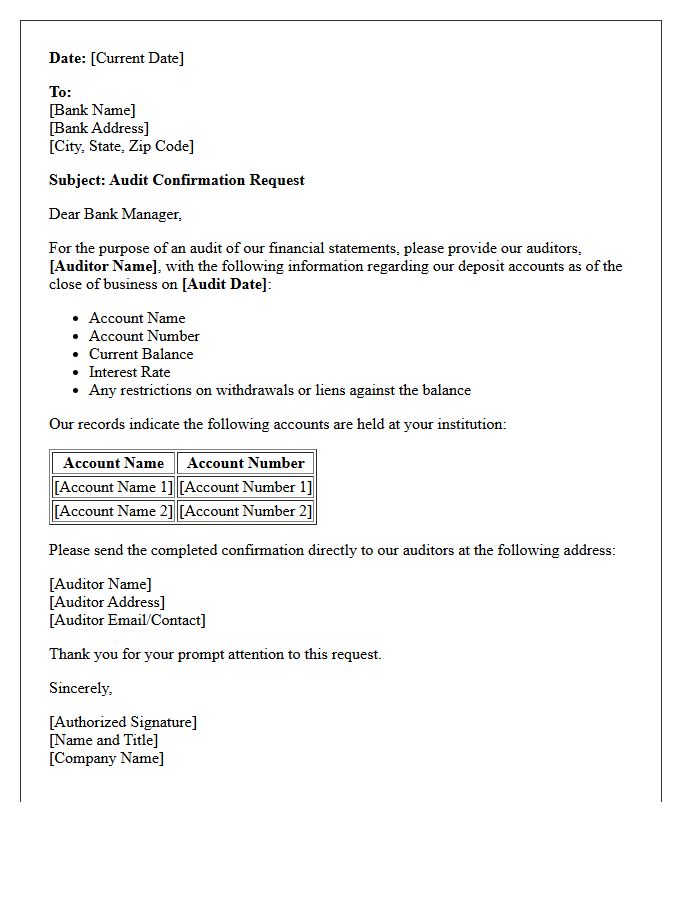

Standard Deposit Account Balance Audit Confirmation Letter

A Standard Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions. Its primary purpose is to verify the accuracy of a company's cash balances, loan obligations, and contingent liabilities as of a specific date. This document serves as independent evidence to prevent financial misstatement and detect potential fraud. By obtaining direct confirmation from the bank, auditors ensure that the financial records presented by management align perfectly with the bank's internal data, maintaining the integrity of the overall financial statement audit process.

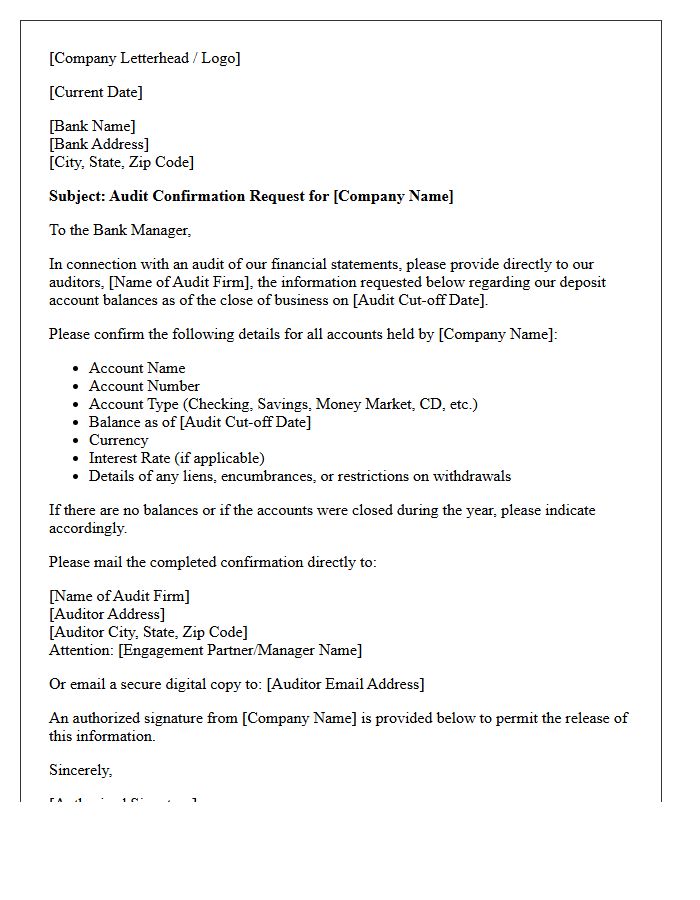

Corporate Deposit Account Balance Audit Confirmation Letter

A Corporate Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify the accuracy of a company's financial records. This document provides independent evidence regarding cash balances, loans, and contingent liabilities as of a specific date. It is a critical component of the financial audit process, ensuring transparency and preventing fraud. For the request to be fulfilled, the account holder must provide authorized signatures, allowing the bank to disclose sensitive fiscal data directly to the auditing firm for verification.

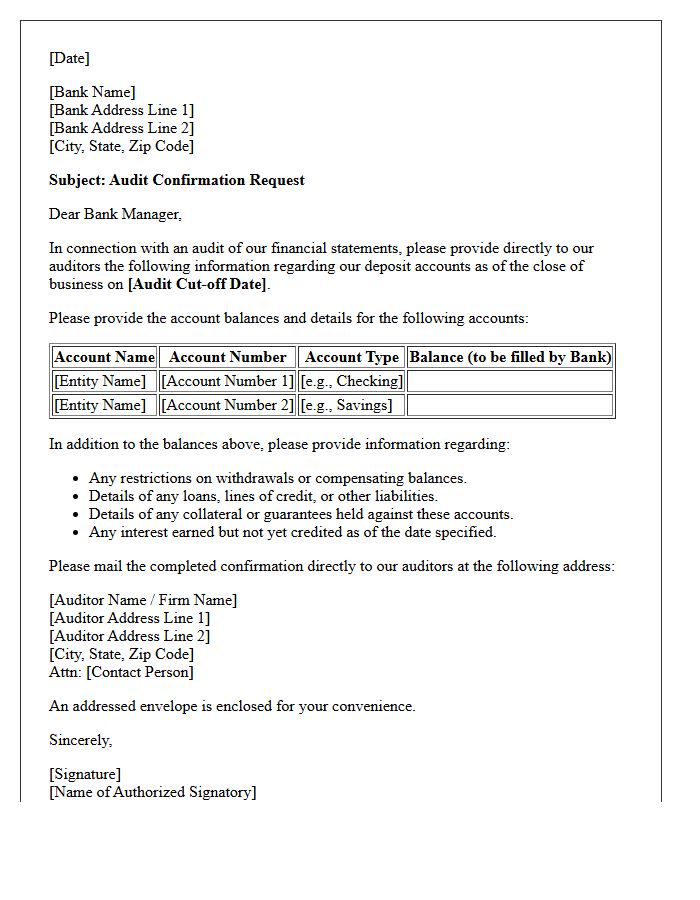

Blank Deposit Account Balance Audit Confirmation Letter

A Blank Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions. Its primary purpose is to verify the accuracy of a company's cash holdings independently. Unlike standard confirmations, this form leaves the balance field empty, requiring the bank to manually fill in the exact figures. This method reduces confirmation bias and ensures higher data reliability. It is a critical procedure for detecting financial statement misstatements and preventing fraud during the year-end auditing process.

External Audit Deposit Account Balance Confirmation Letter

An external audit deposit account balance confirmation letter is a verification document sent by auditors to financial institutions. It serves as independent evidence to confirm the accuracy of cash balances, interest rates, and liabilities reported on a company's financial statements. This procedure is critical for detecting financial statement fraud and ensuring internal controls are effective. To maintain integrity, the auditor must control the mailing process, and the bank must return the response directly to the auditor rather than through the client, preventing unauthorized alterations of sensitive financial data.

Internal Audit Deposit Account Balance Confirmation Letter

An Internal Audit Deposit Account Balance Confirmation Letter is a critical verification tool used to ensure financial reporting accuracy. It serves as independent validation of account balances directly between the bank and the auditor. This process helps detect unauthorized transactions, clerical errors, or potential fraud by reconciling internal records with external statements. Clients must sign and return these requests to maintain audit integrity and compliance with regulatory standards. Timely responses are essential for completing the audit cycle and confirming the existence and valuation of liquid assets held within the institution.

Fixed Deposit Account Balance Audit Confirmation Letter

A Fixed Deposit Account Balance Audit Confirmation Letter is a formal document sent by auditors to a financial institution to verify the accuracy of reported assets. This process ensures that the principal amount, accrued interest, and maturity dates match the company's financial statements. It serves as critical independent evidence to detect discrepancies or unauthorized transactions. By confirming the account status directly with the bank, auditors mitigate risks of material misstatement, providing stakeholders with assurance regarding the existence and valuation of invested funds during a statutory or internal audit.

Savings Deposit Account Balance Audit Confirmation Letter

A Savings Deposit Account Balance Audit Confirmation Letter is a verification document sent by auditors to financial institutions. Its primary purpose is to independently confirm the accuracy of reported cash balances and account details. This process ensures financial statements are transparent and free from material misstatement. As a bank client, you must provide authorized consent for the bank to disclose this sensitive information directly to the auditor. Timely responses are essential for completing the statutory audit and maintaining the integrity of corporate or personal financial records.

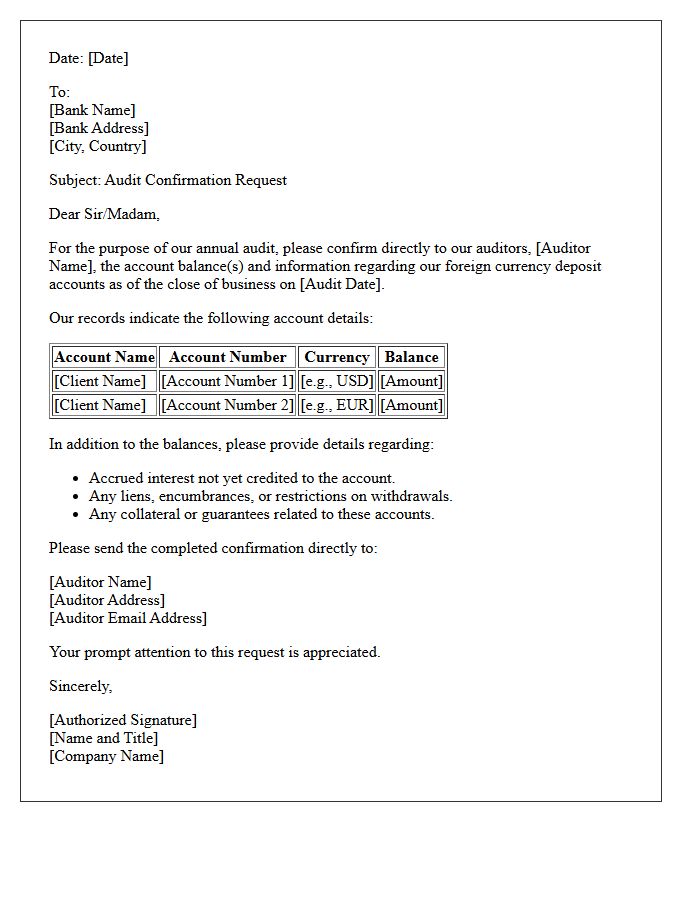

Foreign Currency Deposit Account Balance Audit Confirmation Letter

A Foreign Currency Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions. Its primary purpose is to verify the accuracy of account balances, interest rates, and loan obligations held in non-local denominations. This process ensures the financial statements reflect a true and fair view of the entity's liquidity and foreign exchange exposure. For organizations, timely responses are critical to complete the statutory audit process, mitigate risks of reporting errors, and confirm the existence of funds across international banking jurisdictions.

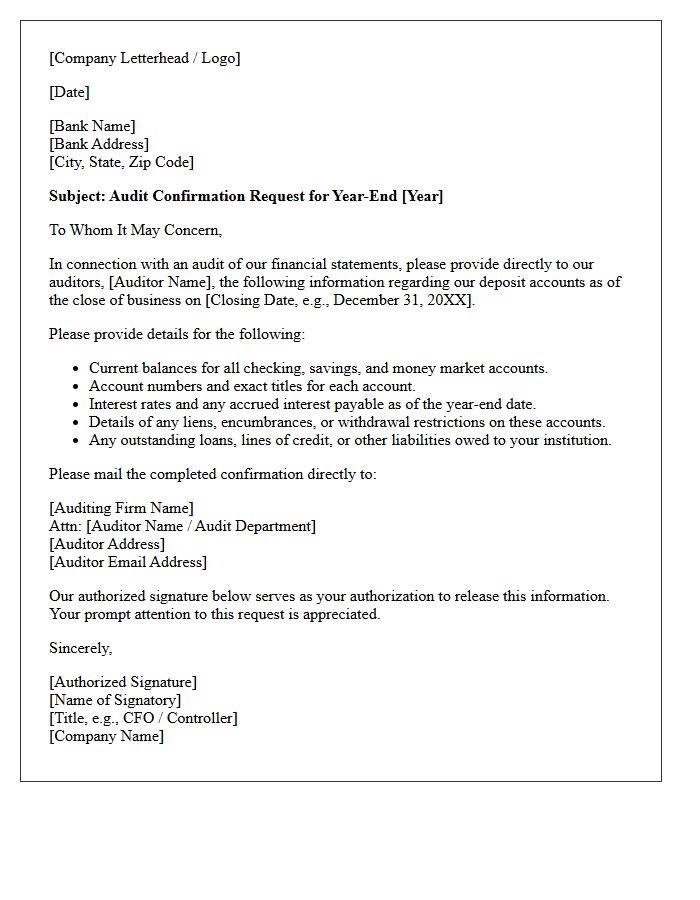

Year-End Deposit Account Balance Audit Confirmation Letter

A Year-End Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions. Its primary purpose is to verify the accuracy of a company's reported cash holdings. This document confirms account balances, interest rates, and any outstanding liabilities or contingent obligations. It serves as critical audit evidence to prevent financial misstatement and ensure transparency in year-end reporting. For businesses, timely response from banks is essential to complete the financial statement audit process efficiently and maintain regulatory compliance.

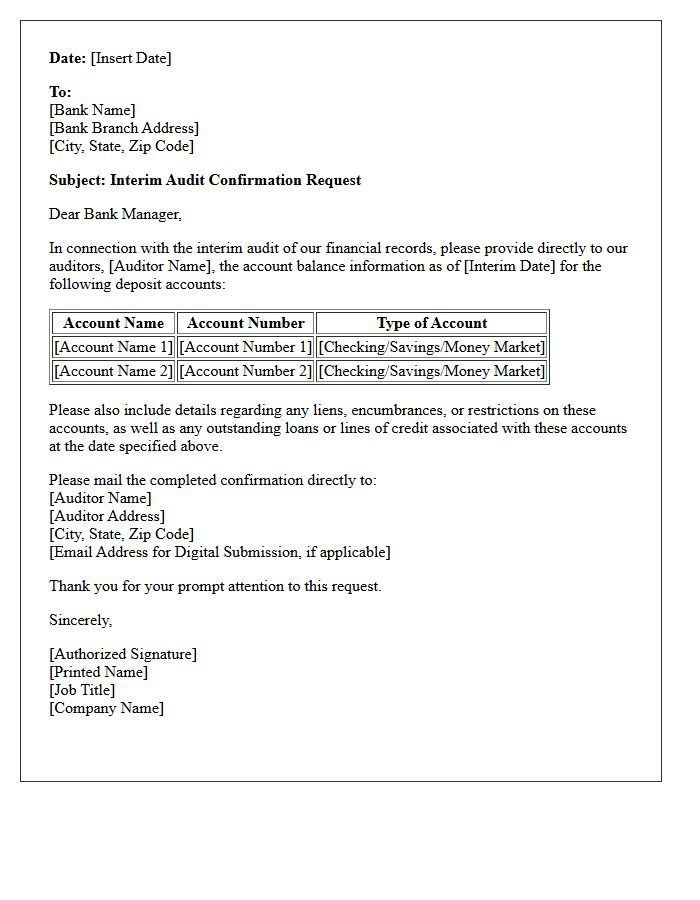

Interim Deposit Account Balance Audit Confirmation Letter

An Interim Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions. Its primary purpose is to verify the accuracy of cash balances and account details as of a specific interim date. This process ensures internal financial records align with third-party data, helping to detect discrepancies or unauthorized transactions before year-end reporting. It provides critical third-party evidence to support the integrity of a company's financial statements, ensuring transparency and regulatory compliance during the auditing cycle.

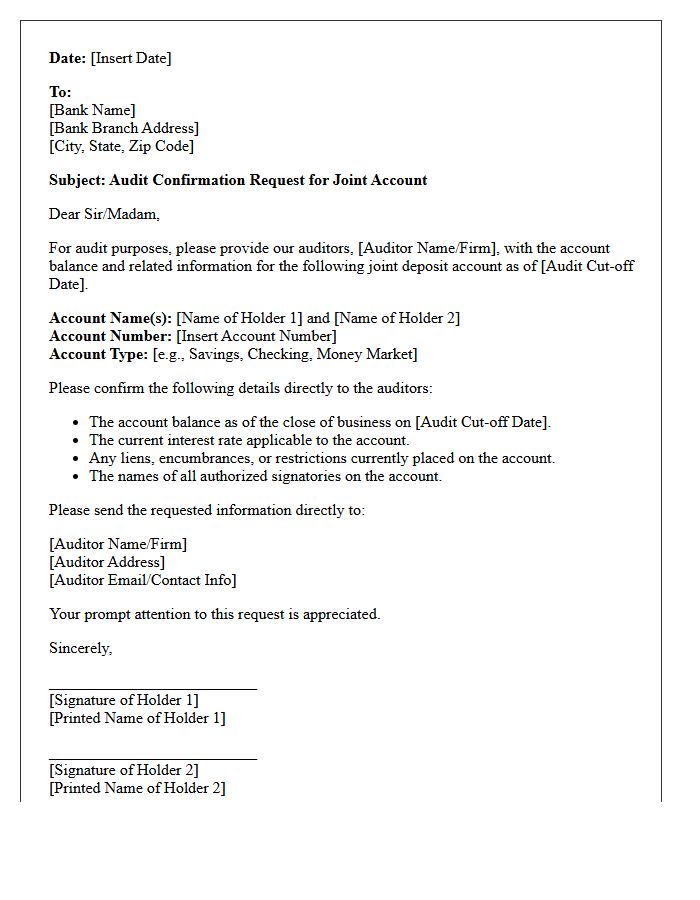

Joint Deposit Account Balance Audit Confirmation Letter

A Joint Deposit Account Balance Audit Confirmation Letter is a formal request used by auditors to verify the accuracy of financial records. It requires all account holders to confirm the reported account balance and interest details as of a specific date. This document is essential for ensuring transparency and preventing financial discrepancies or fraud. By cross-referencing bank data with internal ledgers, the process provides independent verification of assets held jointly, confirming that the stated funds legally exist and are correctly attributed to the owners.

Escrow Deposit Account Balance Audit Confirmation Letter

An Escrow Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify account accuracy. This document ensures that the reported funds held in trust match the bank's internal records. It serves as critical independent evidence to prevent fraud, detect mismanagement, and confirm legal compliance with fiduciary responsibilities. By validating the reconciled balance, auditors provide assurance that client deposits are properly safeguarded and accounted for during a specific reporting period, maintaining transparency in professional financial transactions.

Trust Deposit Account Balance Audit Confirmation Letter

A Trust Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify the accuracy of client funds held in trust. This essential document ensures regulatory compliance and prevents the misappropriation of assets. It confirms real-time balances, interest earned, and account status, providing independent evidence for financial statements. For legal and real estate professionals, these audits are critical to maintaining fiduciary integrity and passing mandatory state bar or industry inspections, confirming that trust records align perfectly with bank records.

Zero Balance Deposit Account Audit Confirmation Letter

A Zero Balance Deposit Account Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify that a specific account held a nil balance at the end of a reporting period. This process ensures the accuracy of financial statements and confirms no undisclosed liabilities or unauthorized transactions exist. It serves as independent verification, mitigating risks of fraud or accounting errors. Understanding this document is essential for maintaining transparent corporate governance and ensuring that closed or inactive accounts are correctly documented during a standard financial audit.

Closed Deposit Account Balance Audit Confirmation Letter

A Closed Deposit Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify zero balances on inactive accounts. This process ensures financial statement accuracy and detects potential unrecorded liabilities or fraud. The bank must confirm that the account was officially terminated and that no residual funds or outstanding obligations remain. For businesses, responding promptly to these verification requests is essential for maintaining transparent financial records and completing a successful independent audit cycle while ensuring all liquidated assets are properly documented.

What is a Deposit Account Balance Audit Confirmation Letter?

A Deposit Account Balance Audit Confirmation Letter is an official document sent by an external auditor to a financial institution to verify the accuracy of the cash balances, interest rates, and account details reported on a company's financial statements.

Why do auditors require a bank confirmation for deposit accounts?

Auditors require bank confirmations to obtain independent, third-party evidence that validates the existence, completeness, and ownership of the funds, ensuring there are no material misstatements or undisclosed liabilities.

What information is typically verified in a balance audit confirmation?

The letter typically verifies the account name, account number, current balance as of a specific date, currency type, interest earned, and whether the account is pledged as collateral for any loans.

How is the authorization process handled for bank audit confirmations?

The client must provide formal authorization, usually via a signed request or a secure digital platform like Confirmation.com, to permit the bank to disclose sensitive financial information to the independent auditing firm.

What is the difference between a positive and negative audit confirmation?

A positive confirmation requires the bank to respond regardless of whether the balance is correct, while a negative confirmation only requests a response if the bank disagrees with the balance stated in the letter.

Comments