An Interbank Placement and Borrowing Audit Confirmation Letter is a formal document used to verify outstanding balances and interest rates between financial institutions. This process ensures financial accuracy and regulatory compliance during the auditing cycle. It serves as crucial third-party evidence for verifying liquidity and interbank transactions. To streamline your verification process, below are some ready to use template.

Image cover: The Auditor's Toolkit: Essential Interbank Placement and Borrowing Confirmation Templates

Letter Samples List

- Standard Interbank Placement Audit Confirmation Letter

- Standard Interbank Borrowing Audit Confirmation Letter

- Foreign Currency Interbank Placement Audit Confirmation Letter

- Domestic Interbank Borrowing Audit Confirmation Letter

- Overnight Interbank Placement Audit Confirmation Letter

- Term Interbank Borrowing Audit Confirmation Letter

- Cross-Border Interbank Placement Audit Confirmation Letter

- Islamic Interbank Placement Audit Confirmation Letter

- Interbank Money Market Borrowing Audit Confirmation Letter

- Central Bank Interbank Placement Audit Confirmation Letter

- Interbank Repurchase Agreement Borrowing Audit Confirmation Letter

- Outstanding Interbank Placement Balance Audit Confirmation Letter

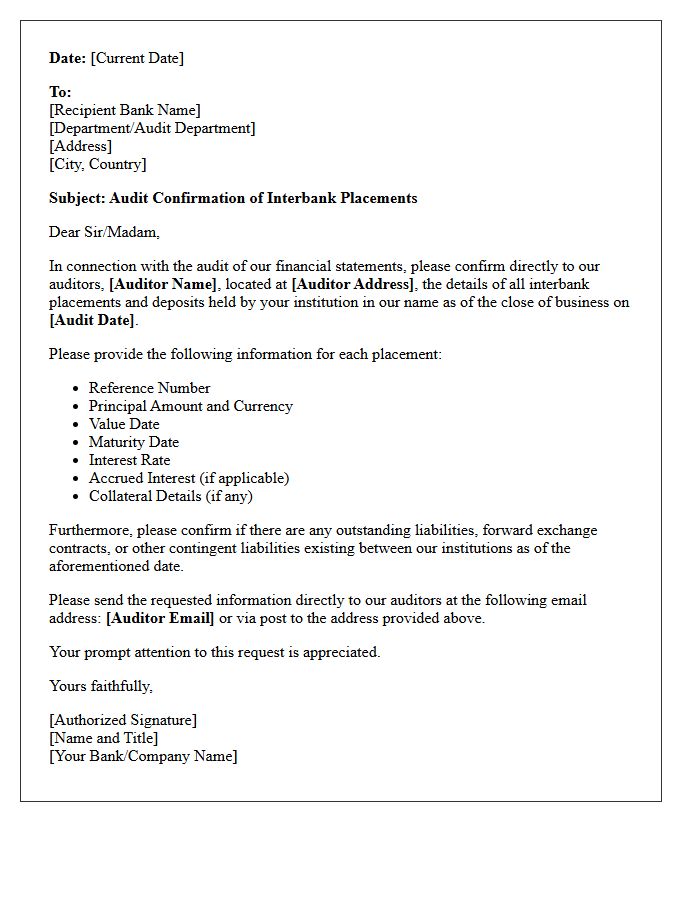

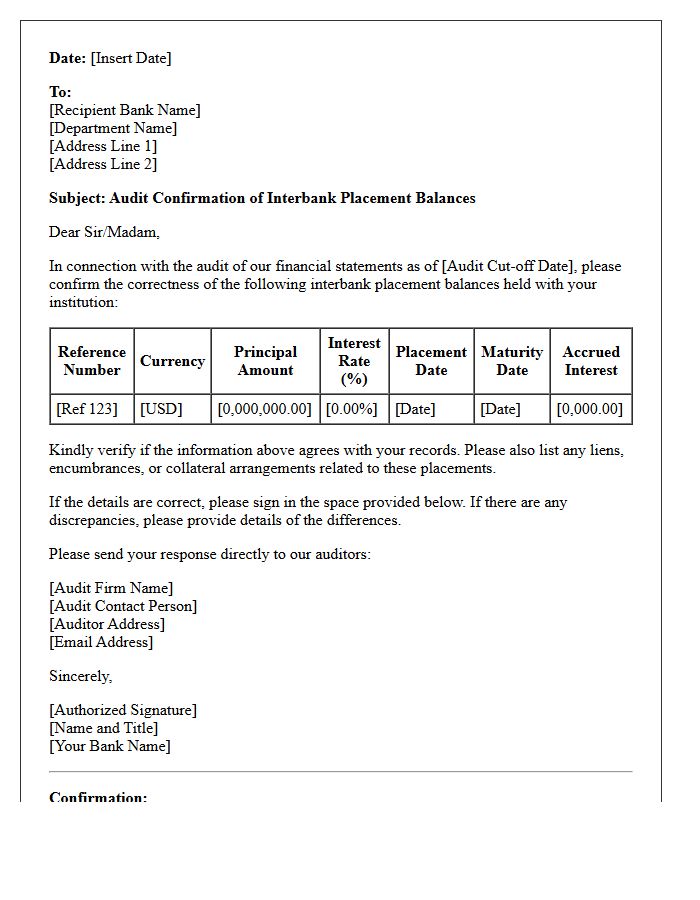

Standard Interbank Placement Audit Confirmation Letter

A Standard Interbank Placement Audit Confirmation Letter is a formal document used by auditors to verify the existence and terms of cash deposits between financial institutions. It ensures liquidity accuracy by confirming principal amounts, interest rates, and maturity dates directly with the counterparty. This process mitigates risk, prevents financial misstatement, and provides third-party evidence for regulatory compliance. Accurate confirmations are essential for validating a bank's balance sheet and maintaining transparency within global monetary markets during annual financial examinations.

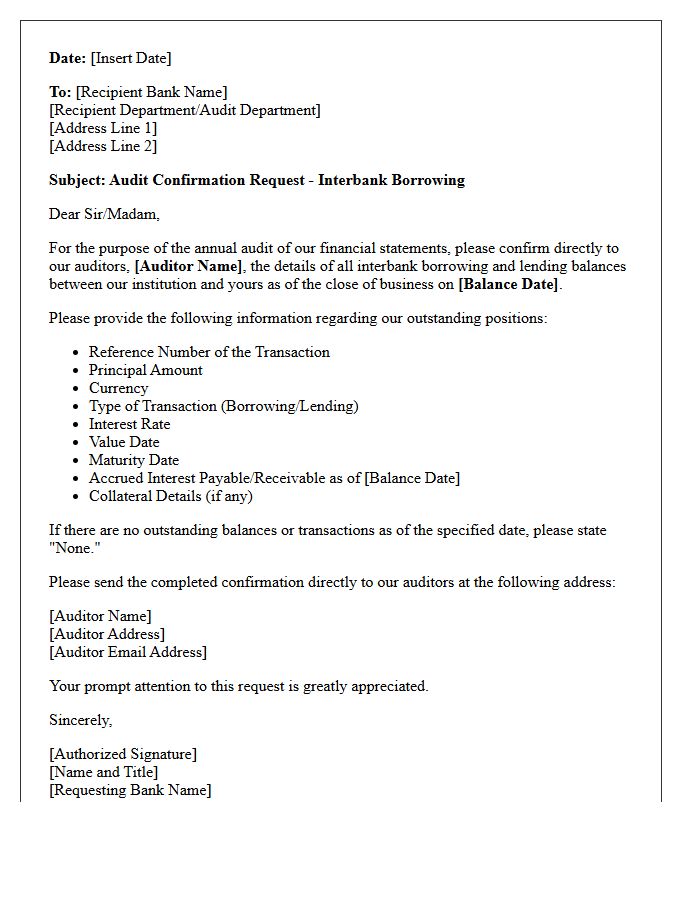

Standard Interbank Borrowing Audit Confirmation Letter

A Standard Interbank Borrowing Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify outstanding loan balances and interest rates. This document ensures the accuracy of a bank's financial statements by confirming interbank liabilities and asset values directly with the counterparty. It serves as crucial third-party evidence to detect reporting discrepancies, mitigate fraud risks, and validate liquidity positions. Accurate completion of these letters is essential for regulatory compliance and maintaining the integrity of the global banking audit process.

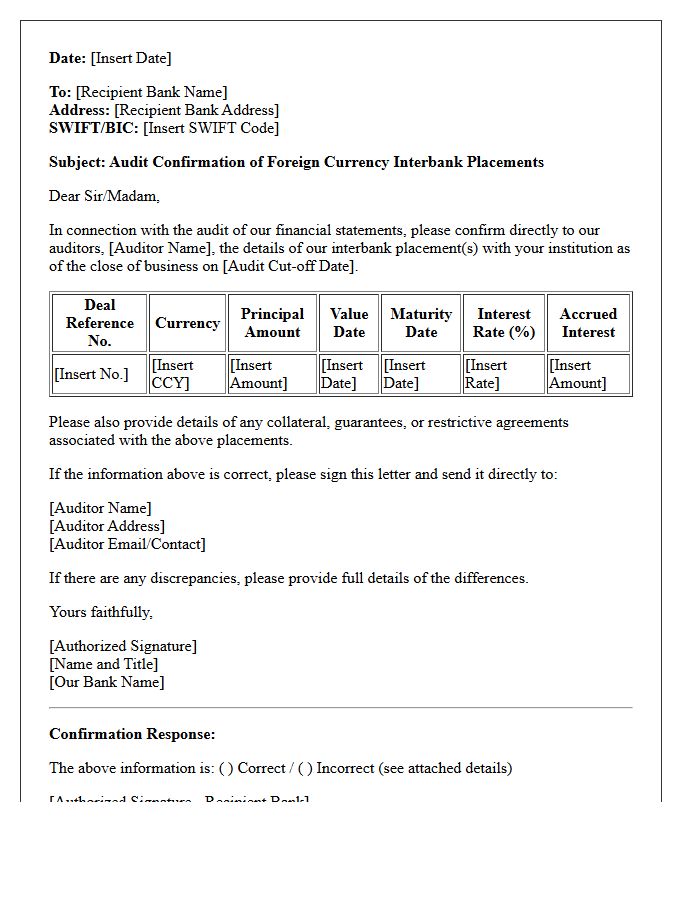

Foreign Currency Interbank Placement Audit Confirmation Letter

A Foreign Currency Interbank Placement Audit Confirmation Letter is a critical verification document used during financial audits to validate balances held between banks. It serves as direct evidence of outstanding deposits, interest rates, and maturity dates for foreign exchange transactions. By confirming these details directly with the counterparty, auditors ensure the accuracy of the bank's financial statements and mitigate risks related to misstatement or fraud. This process maintains transparency in the global interbank market and ensures regulatory compliance across different currency jurisdictions.

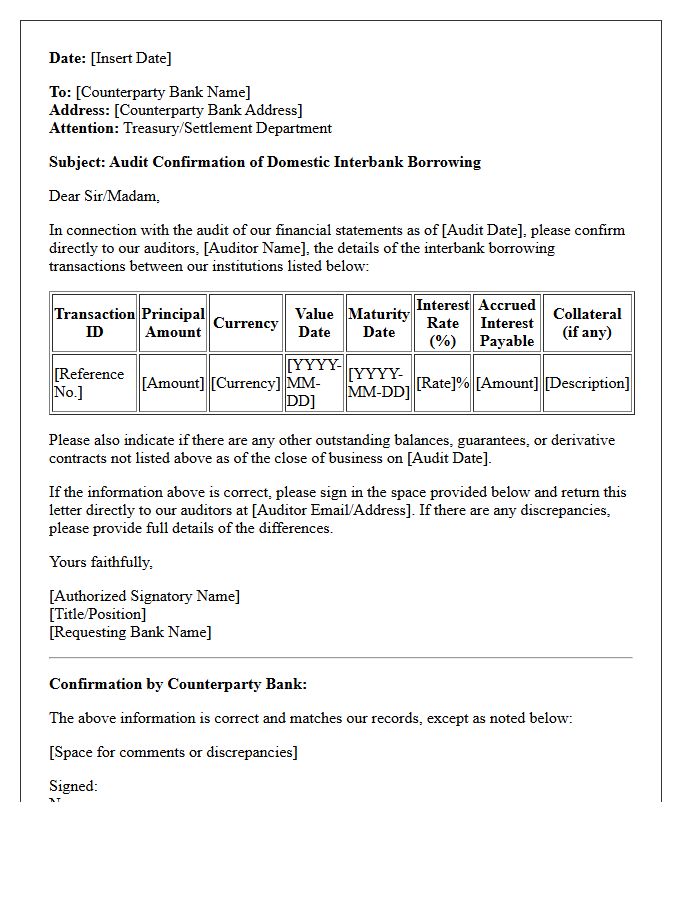

Domestic Interbank Borrowing Audit Confirmation Letter

A Domestic Interbank Borrowing Audit Confirmation Letter is a formal document used by auditors to verify the accuracy of interbank transactions and outstanding balances between financial institutions. It serves as critical third-party evidence to confirm recorded liabilities, interest rates, and maturity dates. This process ensures financial transparency and helps detect reporting discrepancies or unauthorized lending activities. By validating these interbank placements, auditors can confirm the institution's liquidity position and compliance with regulatory standards, providing essential assurance for the integrity of a bank's financial statements during the annual audit cycle.

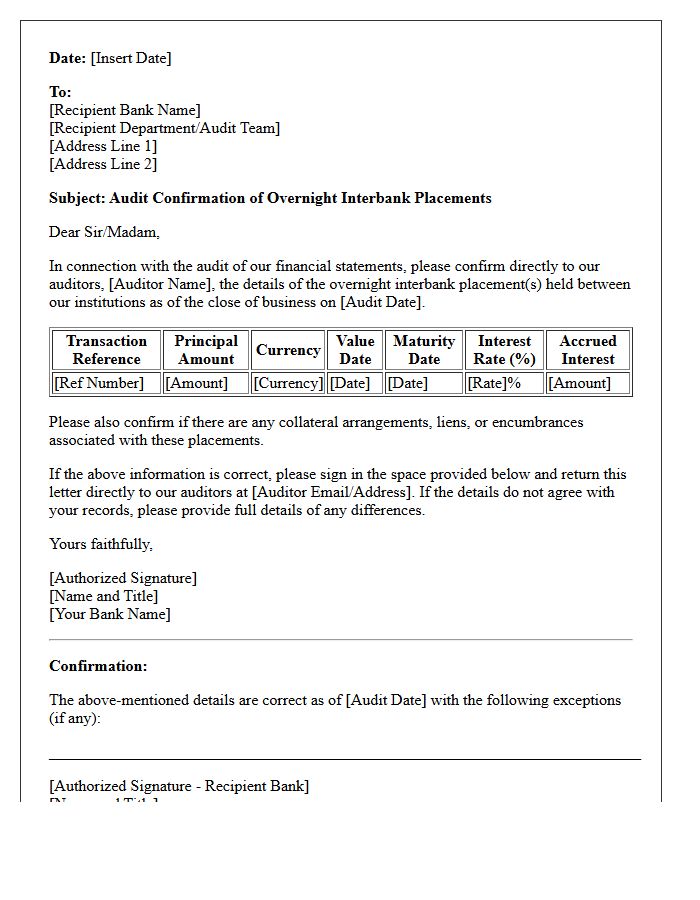

Overnight Interbank Placement Audit Confirmation Letter

An Overnight Interbank Placement Audit Confirmation Letter is a formal document used to verify short-term lending transactions between financial institutions. It serves as independent evidence for auditors to reconcile year-end balances and interest income. This letter ensures that the principal amount and maturity terms recorded in the bank's ledger match the counterparty's records. Accurate confirmations are essential for maintaining financial transparency, mitigating operational risks, and ensuring compliance with international accounting standards during the annual statutory audit process.

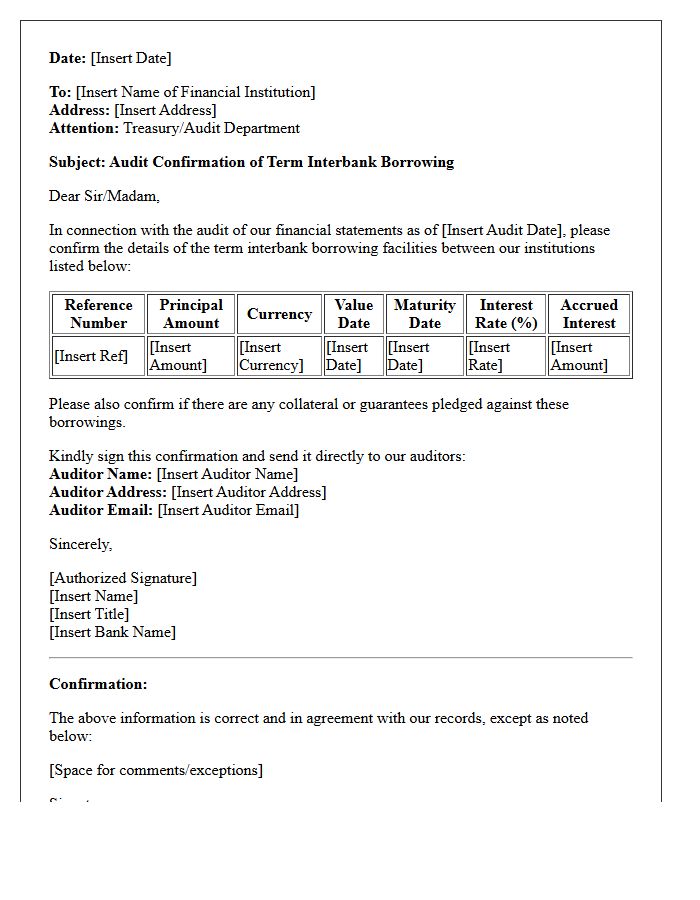

Term Interbank Borrowing Audit Confirmation Letter

An Interbank Borrowing Audit Confirmation Letter is a formal document sent by auditors to verify the accuracy of balances and terms reported between financial institutions. It ensures that outstanding liabilities, interest rates, and maturity dates match the records of both the borrowing and lending banks. This process is critical for verifying liquidity, preventing financial misstatements, and ensuring regulatory compliance. By validating these high-value transactions directly with third parties, auditors can mitigate risks related to fraud and reporting errors in a bank's financial statements.

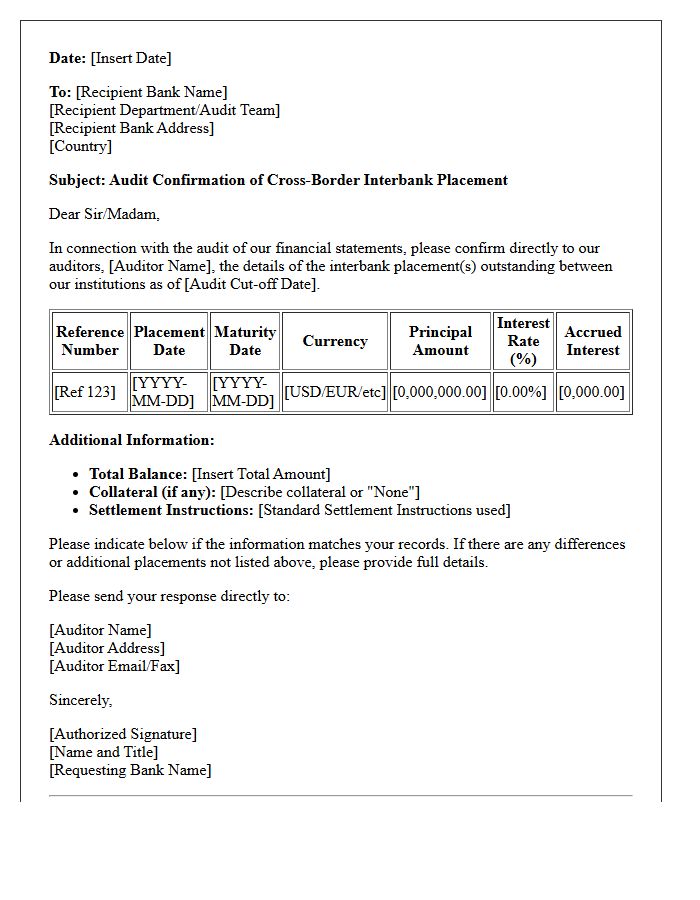

Cross-Border Interbank Placement Audit Confirmation Letter

A Cross-Border Interbank Placement Audit Confirmation Letter is a vital control document used to verify balances between international financial institutions. It ensures that liquidity placements and interest terms recorded in one bank's ledger match the corresponding counterparty records. This independent verification process is essential for financial reporting accuracy, mitigating operational risk, and detecting potential fraud. During annual audits, these letters provide primary evidence of legal ownership and the existence of foreign currency assets, ensuring compliance with global banking regulations and IFRS standards for transparent interbank transactions.

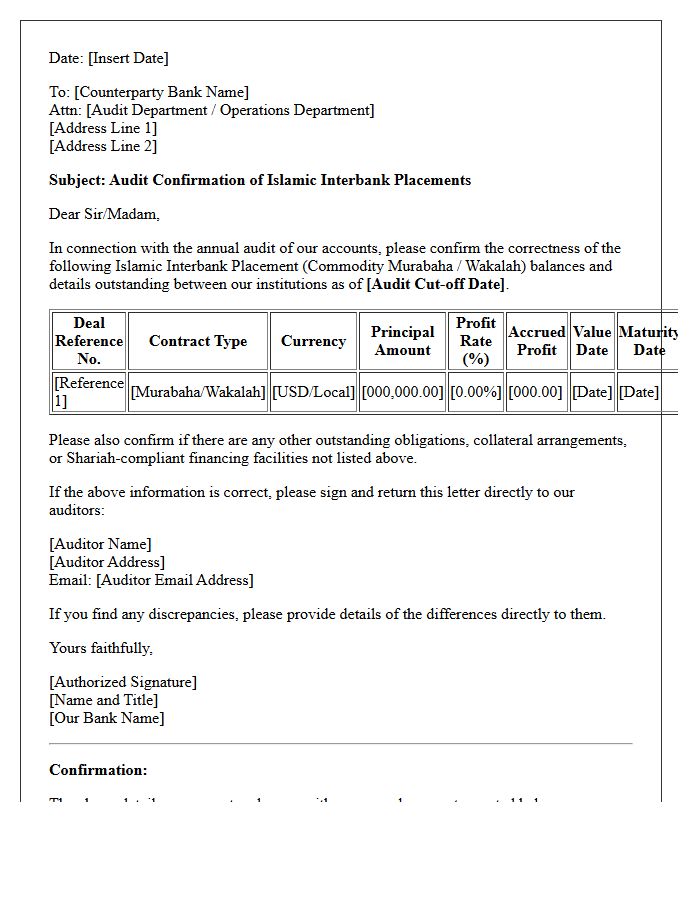

Islamic Interbank Placement Audit Confirmation Letter

An Islamic Interbank Placement Audit Confirmation Letter is a formal document used to verify Sharia-compliant investment balances between financial institutions. It serves as independent evidence for auditors to validate the accuracy of commodity murabaha or wakala transactions reported on the balance sheet. This process ensures transparency, confirms profit rates, and mitigates operational risks within the Islamic money market. Timely reconciliation of these placements is essential for maintaining regulatory compliance and ensuring that all interbank activities adhere strictly to ethical financing principles and accounting standards.

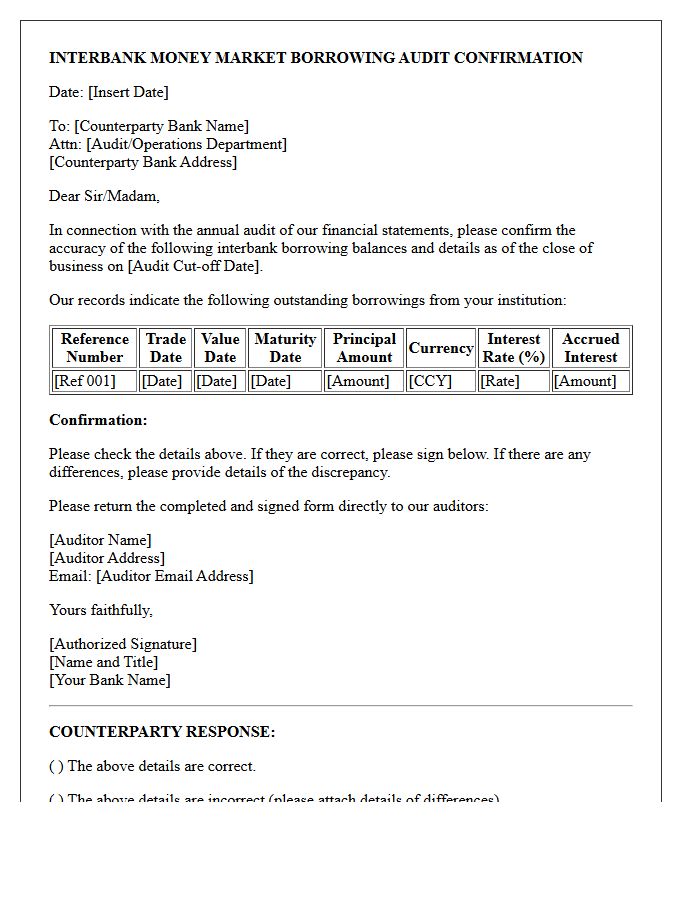

Interbank Money Market Borrowing Audit Confirmation Letter

An Interbank Money Market Borrowing Audit Confirmation Letter is a formal request sent by auditors to verify outstanding loan balances between financial institutions. It serves as independent evidence to validate the accuracy of reported liabilities, interest rates, and maturity dates on a bank's balance sheet. This process is crucial for ensuring financial transparency and regulatory compliance. By confirming these high-value transactions directly with the counterparty, auditors can effectively mitigate risks related to material misstatements or unauthorized borrowing activities during the annual audit cycle.

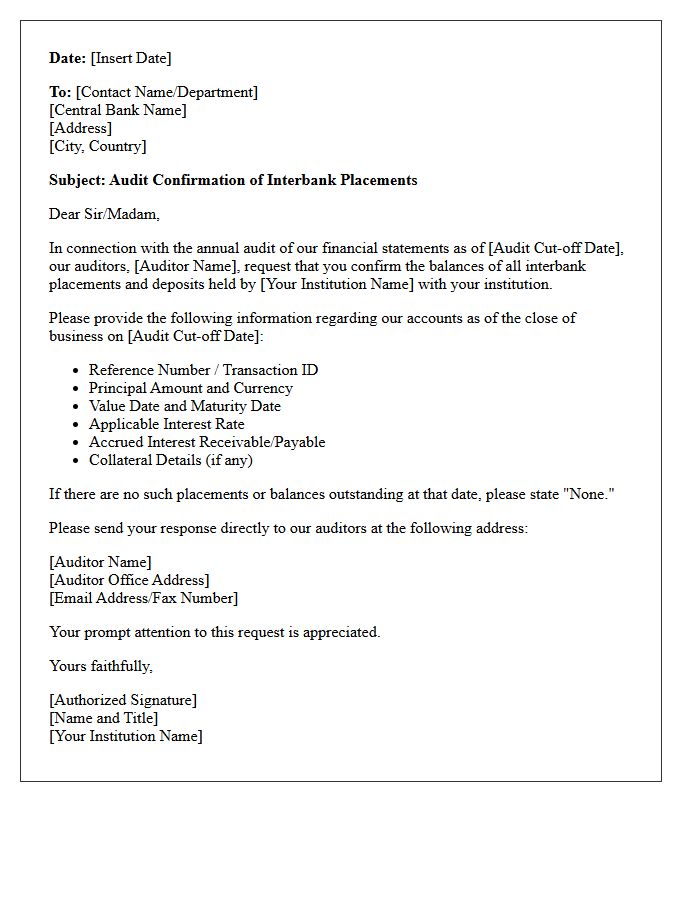

Central Bank Interbank Placement Audit Confirmation Letter

A Central Bank Interbank Placement Audit Confirmation Letter is a critical document used to verify the existence and accuracy of funds held at a monetary authority. During an external audit, this formal request ensures that recorded balances, interest rates, and maturity dates match the central bank's official records. This process is essential for maintaining financial transparency and validating liquidity positions. It serves as primary audit evidence to detect reporting discrepancies, mitigate fraud risks, and ensure compliance with regulatory standards within the global banking system.

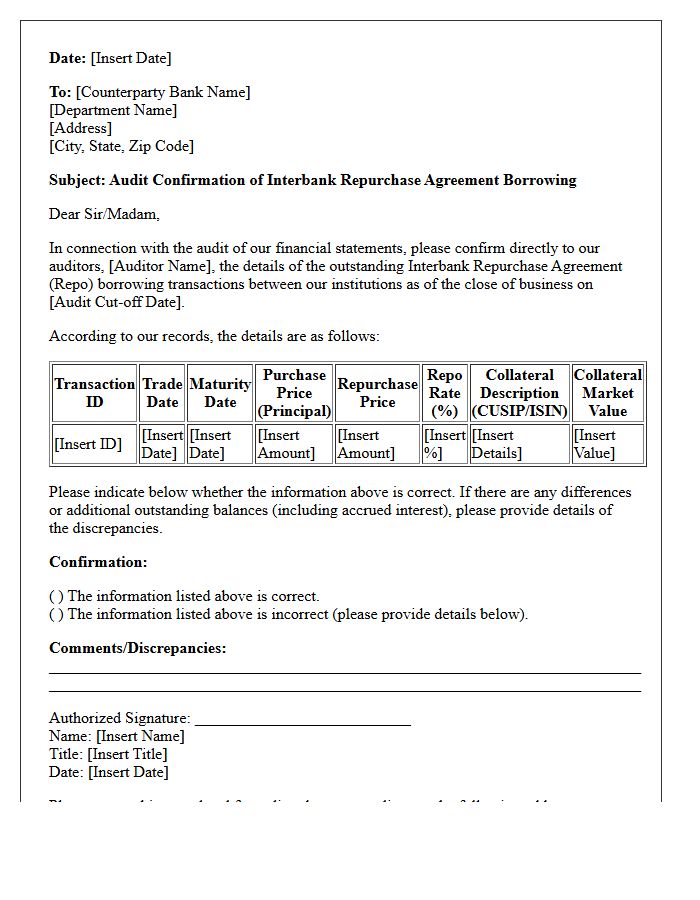

Interbank Repurchase Agreement Borrowing Audit Confirmation Letter

An Interbank Repurchase Agreement Borrowing Audit Confirmation Letter is a critical document used to verify repurchase agreements (repos) between financial institutions. It serves as independent evidence for auditors to validate the outstanding principal balance, interest rates, and collateral details at a specific reporting date. This process ensures the accuracy of financial statements and confirms the existence of legal obligations. Accurate reconciliation of these letters is essential for mitigating operational risk and ensuring transparency in high-volume liquidity exchanges within the interbank market.

Outstanding Interbank Placement Balance Audit Confirmation Letter

An Outstanding Interbank Placement Balance Audit Confirmation Letter is a critical verification document used during financial audits to validate the accuracy of funds held between banking institutions. It ensures that the recorded principal amounts, interest rates, and maturity dates align perfectly between the lending and borrowing parties. This process is essential for maintaining financial transparency, mitigating reporting errors, and preventing fraudulent activities. By confirming these balances independently, auditors gain reliable evidence regarding a bank's liquidity position and overall balance sheet integrity.

What is an Interbank Placement and Borrowing Audit Confirmation Letter?

An Interbank Placement and Borrowing Audit Confirmation Letter is a formal document sent by auditors to financial institutions to verify the accuracy of reported balances, interest rates, and maturity dates of short-term loans and deposits held between banks as of a specific reporting date.

Why is external confirmation necessary for interbank borrowing and placement activities?

External confirmation is necessary to provide independent evidence of the existence, rights and obligations, and valuation of interbank transactions. It helps auditors detect unrecorded liabilities, verify collateral arrangements, and ensure that the financial statements reflect the true liquidity position of the bank.

What key data points are verified in an interbank audit confirmation?

The confirmation typically verifies the principal amount outstanding, the agreed-upon interest rate, accrued interest receivable or payable, the value and nature of any pledged collateral, and the specific value dates and maturity dates of the placements or borrowings.

How does an audit confirmation letter help in detecting "window dressing" in interbank markets?

By reconciling the confirmation response directly from the counterparty bank with the internal ledger, auditors can identify temporary or circular transactions designed to artificially inflate liquidity ratios or improve the appearance of the balance sheet at the end of a reporting period.

What is the standard procedure if a discrepancy is found in an interbank confirmation response?

If a discrepancy is identified, auditors must perform follow-up procedures, which include reviewing trade tickets, checking swift messages (MT300/MT320), inspecting board approvals, and communicating with the counterparty's middle office to determine whether the difference arises from timing issues or reporting errors.

Comments