A Contingent Liability Audit Confirmation Letter is a formal request sent by auditors to a company's legal counsel. It identifies potential legal claims, pending litigation, or financial obligations that may impact financial statements. This ensures transparency and accuracy in corporate reporting by verifying undisclosed risks. To simplify your documentation process, below are some ready to use template.

Image cover: Professional Templates for Contingent Liability Audit Confirmation Letters

Letter Samples List

- Outstanding Commercial Letter of Credit Audit Confirmation Letter

- Financial Bank Guarantee Contingent Liability Audit Letter

- Pending Litigation and Legal Claims Bank Confirmation Letter

- Unfunded Loan Commitment Audit Confirmation Letter

- Derivative Instrument Contingent Liability Audit Letter

- Bankers Acceptance Liability Audit Confirmation Letter

- Trade Finance Contingent Liability Audit Letter

- Foreign Exchange Forward Contract Audit Letter

- Securitization Recourse Obligation Confirmation Letter

- Surety Bond and Indemnity Audit Confirmation Letter

- Syndicated Loan Contingency Audit Confirmation Letter

- Standby Letter of Credit Contingent Liability Audit Letter

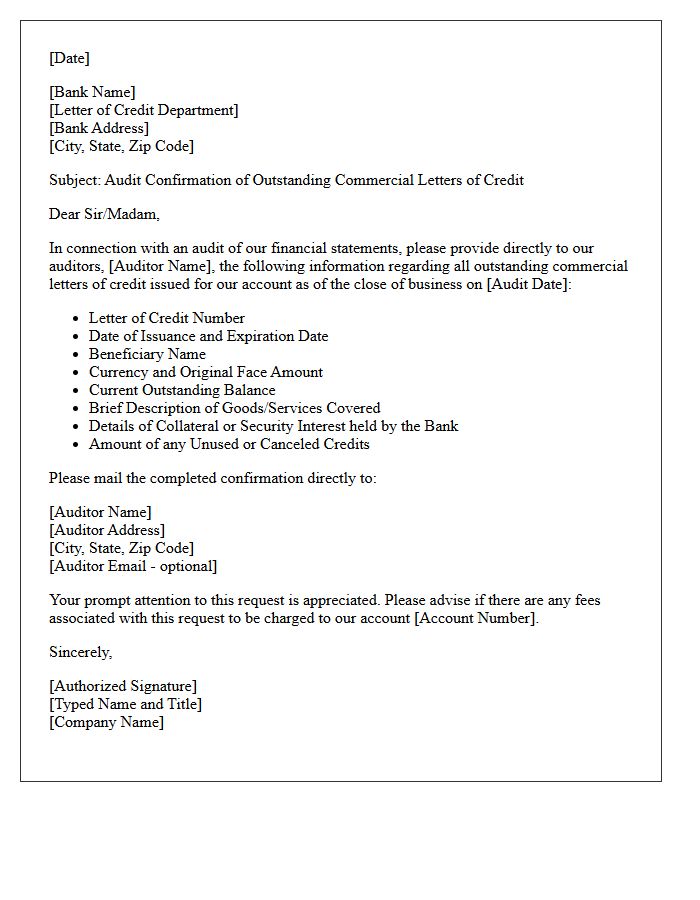

Outstanding Commercial Letter of Credit Audit Confirmation Letter

An Outstanding Commercial Letter of Credit Audit Confirmation Letter is a critical document used by auditors to verify a company's unpaid financial obligations. This request ensures that the bank and the client agree on the terms, balances, and expiration dates of active trade credits. It serves as primary evidence to confirm liability accuracy on financial statements, preventing unrecorded debts. By validating these trade instruments, auditors mitigate risks related to international trade financing and ensure the transparency of a business's contingent liabilities and current liquidity position during a fiscal year-end review.

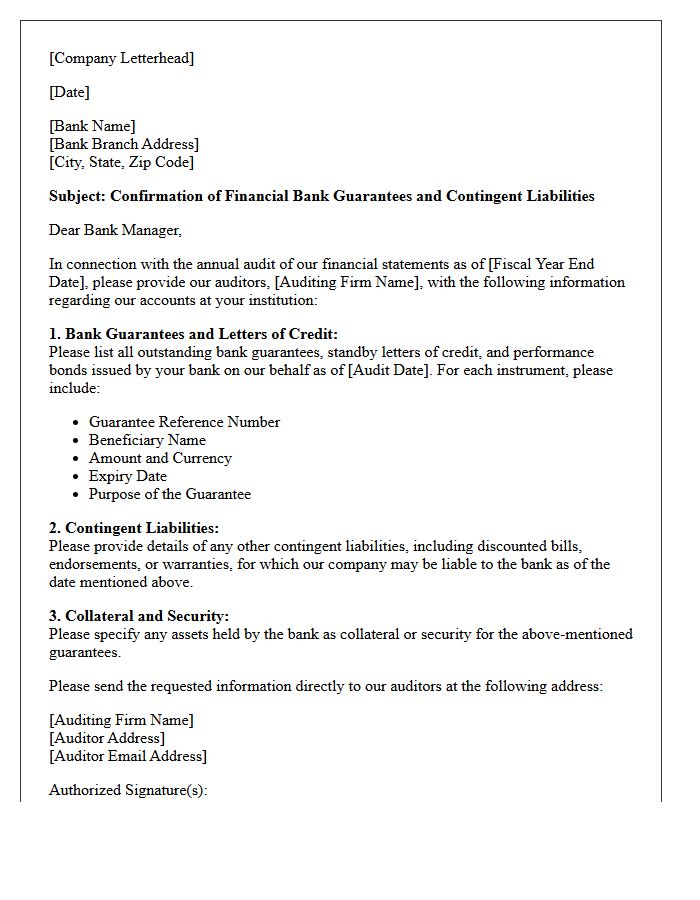

Financial Bank Guarantee Contingent Liability Audit Letter

A Financial Bank Guarantee is a significant contingent liability that must be disclosed during a corporate audit. An Audit Letter serves as official verification from a financial institution to auditors, confirming the existence, value, and terms of outstanding guarantees. This process ensures transparency in financial reporting, as these obligations represent potential debts if the applicant defaults. Auditors examine these letters to assess risk exposure and ensure compliance with accounting standards, preventing undisclosed off-balance sheet liabilities from misrepresenting a company's true fiscal health.

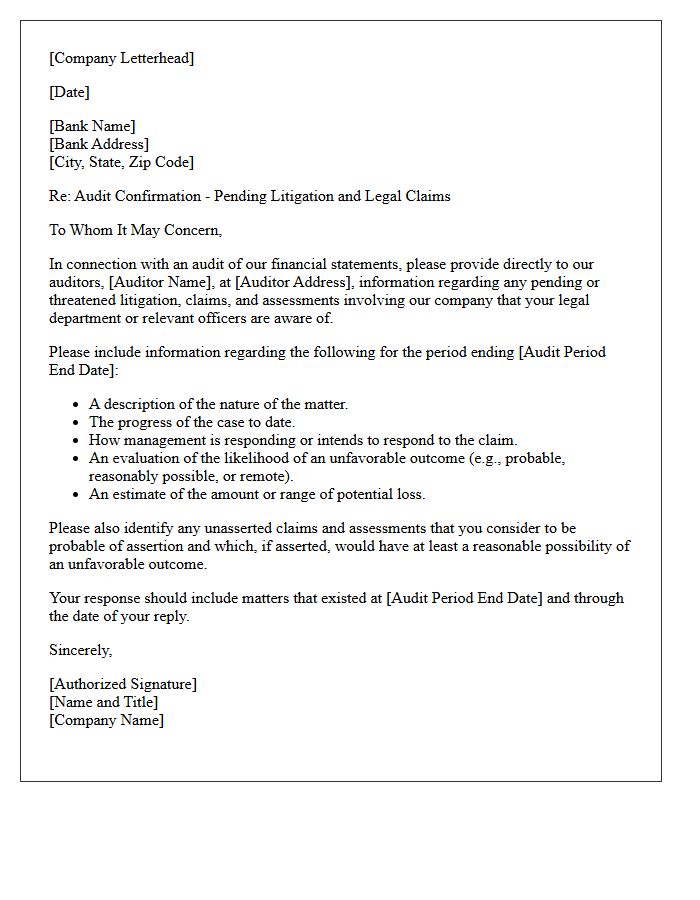

Pending Litigation and Legal Claims Bank Confirmation Letter

A bank confirmation letter regarding pending litigation is a formal inquiry sent by auditors to a financial institution. This document requests disclosure of any legal claims, judgments, or contingent liabilities that may impact a company's financial standing. It serves as critical audit evidence to ensure the completeness of financial statements and to identify potential risks not yet recorded. Accurate reporting of these claims is essential for regulatory compliance and provides stakeholders with transparency concerning the entity's actual financial obligations and legal exposure during the reporting period.

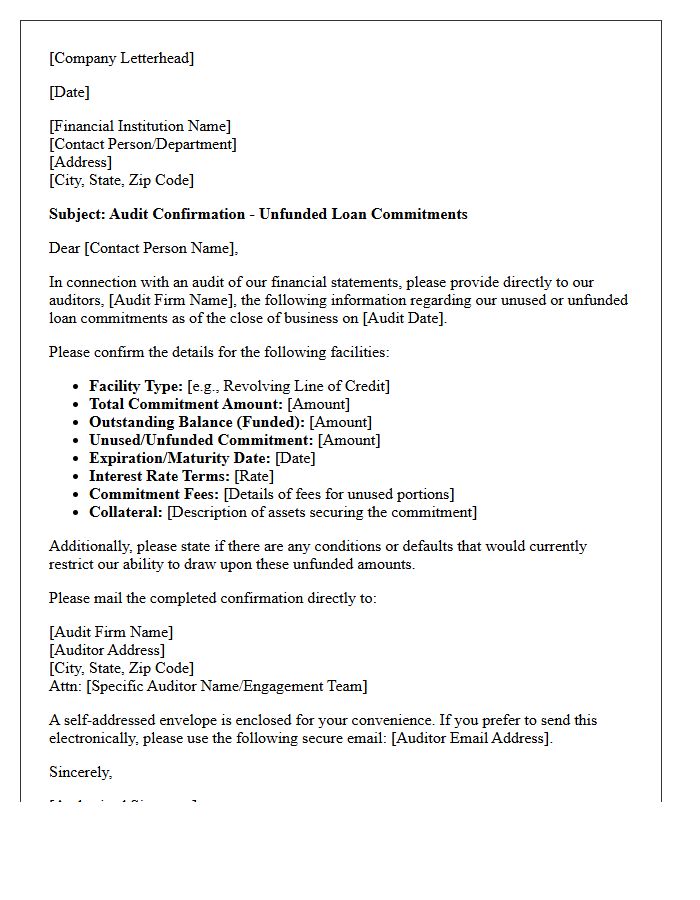

Unfunded Loan Commitment Audit Confirmation Letter

An Unfunded Loan Commitment Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify off-balance sheet obligations. It confirms the specific amount of credit a lender has promised but not yet disbursed to a borrower. This process is essential for ensuring financial statement accuracy and assessing potential liquidity risks. Companies must accurately report these commitments to provide a transparent view of their future borrowing capacity and contractual liabilities, helping stakeholders understand the entity's true financial position and potential debt exposure.

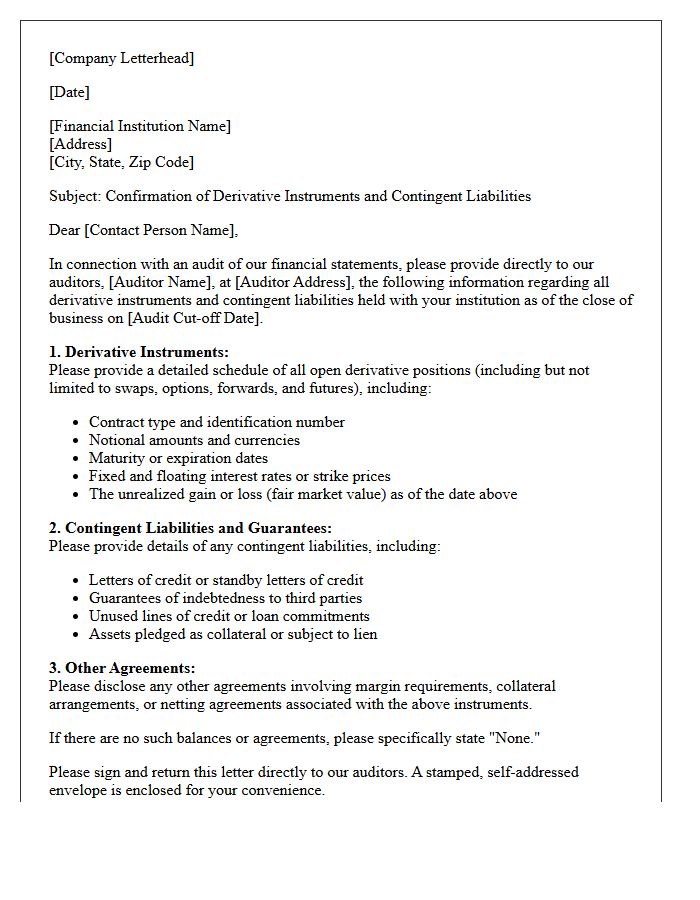

Derivative Instrument Contingent Liability Audit Letter

A Derivative Instrument Contingent Liability Audit Letter is a formal request sent to financial institutions to verify unrecorded obligations arising from complex financial contracts. This document is crucial for auditors to assess potential risks that may not appear on the balance sheet. It ensures the accuracy of a company's financial statements by confirming market values, collateral requirements, and contractual terms. Identifying these hidden liabilities is essential for maintaining transparency and evaluating the overall fiscal health of an organization during a comprehensive financial audit process.

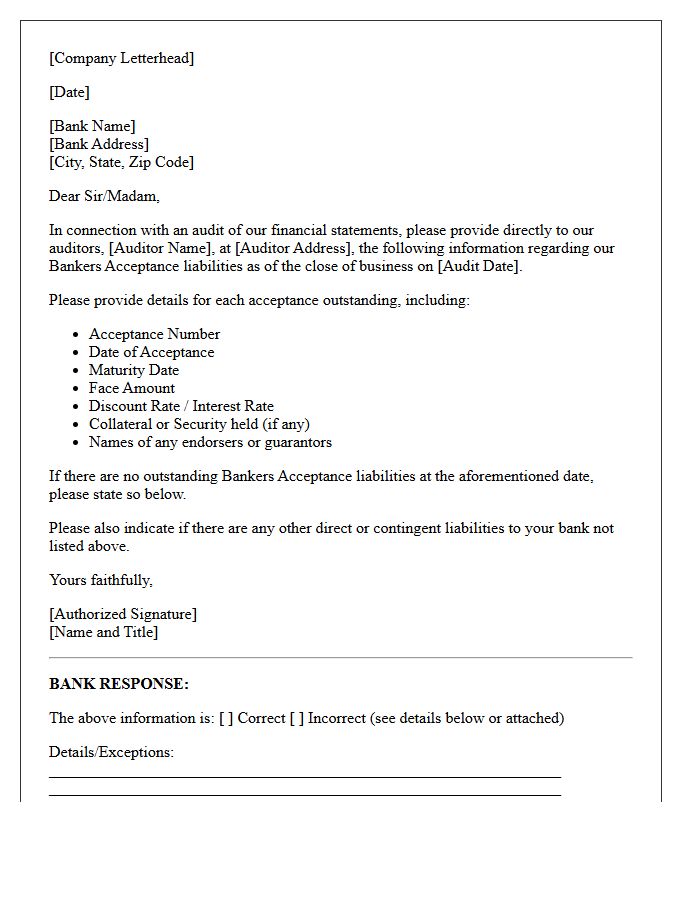

Bankers Acceptance Liability Audit Confirmation Letter

A Bankers Acceptance Liability Audit Confirmation Letter is a formal request sent by auditors to a financial institution to verify outstanding short-term debt obligations. This document ensures the accuracy of financial statements by confirming specific details like face value, maturity dates, and repayment terms. It serves as critical third-party evidence to prevent material misstatements regarding a company's credit liabilities. Understanding these confirmations is essential for validating liquidity positions and ensuring full transparency during the annual audit process.

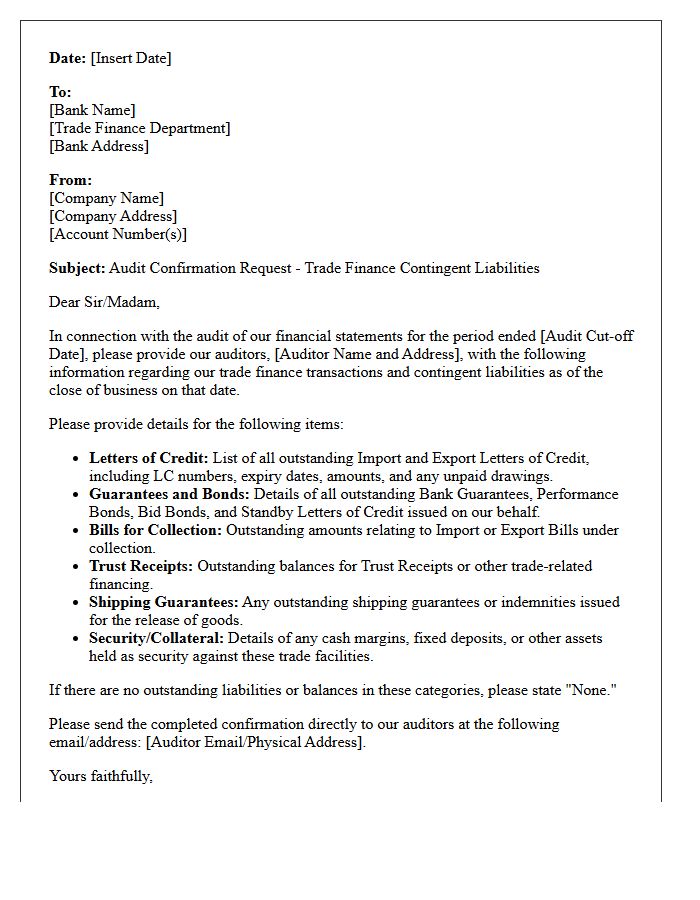

Trade Finance Contingent Liability Audit Letter

A Trade Finance Contingent Liability Audit Letter is a formal verification document used during financial examinations. It confirms an organization's potential obligations, such as letters of credit or guarantees, which are not yet realized on the balance sheet. Auditors utilize these letters to ensure transparency and accurate reporting of off-balance sheet risks. Understanding these contingent liabilities is essential for assessing a company's true financial exposure and ensuring compliance with global accounting standards. This process validates that all secondary obligations are documented to prevent unforeseen fiscal discrepancies.

Foreign Exchange Forward Contract Audit Letter

A Foreign Exchange Forward Contract Audit Letter is an essential confirmation document used to verify the existence and details of outstanding derivative transactions. During an audit, financial institutions provide these letters to validate strike prices, maturity dates, and notional amounts. This process ensures the accuracy of the company's financial statements by reconciling internal records with external bank data. It is a critical control for financial reporting, helping to mitigate risks related to valuation errors and ensuring compliance with international accounting standards for hedge accounting and liability disclosure.

Securitization Recourse Obligation Confirmation Letter

A Securitization Recourse Obligation Confirmation Letter is a critical legal document used in structured finance to verify a seller's liability. It explicitly confirms the recourse obligations retained by the originator if underlying assets, such as loans or receivables, underperform. This letter ensures transparency for investors and regulators by defining the financial risk retention and the specific conditions under which the seller must repurchase assets or provide additional collateral. It serves as essential proof of the contractual credit enhancement measures that protect the securitization structure's overall stability.

Surety Bond and Indemnity Audit Confirmation Letter

A Surety Bond and Indemnity Audit Confirmation Letter is a formal document sent to verify outstanding liabilities and bond obligations. It ensures financial transparency by confirming the penal sums, active dates, and any collateral held by the surety company. This process is essential for accurate corporate financial reporting and compliance during independent audits. It validates that all contingent liabilities under the indemnity agreement are correctly recorded, helping auditors assess the risk profile and overall solvency of the bonded entity effectively.

Syndicated Loan Contingency Audit Confirmation Letter

A Syndicated Loan Contingency Audit Confirmation Letter is a formal request sent to lenders to verify off-balance sheet liabilities and potential legal obligations. It ensures that any contingent liabilities, such as guarantees or pending litigation related to a multi-bank credit facility, are accurately disclosed in financial statements. This process is vital for financial transparency and helps auditors mitigate risks by confirming the scope of exposure across all participating institutions within the syndicate.

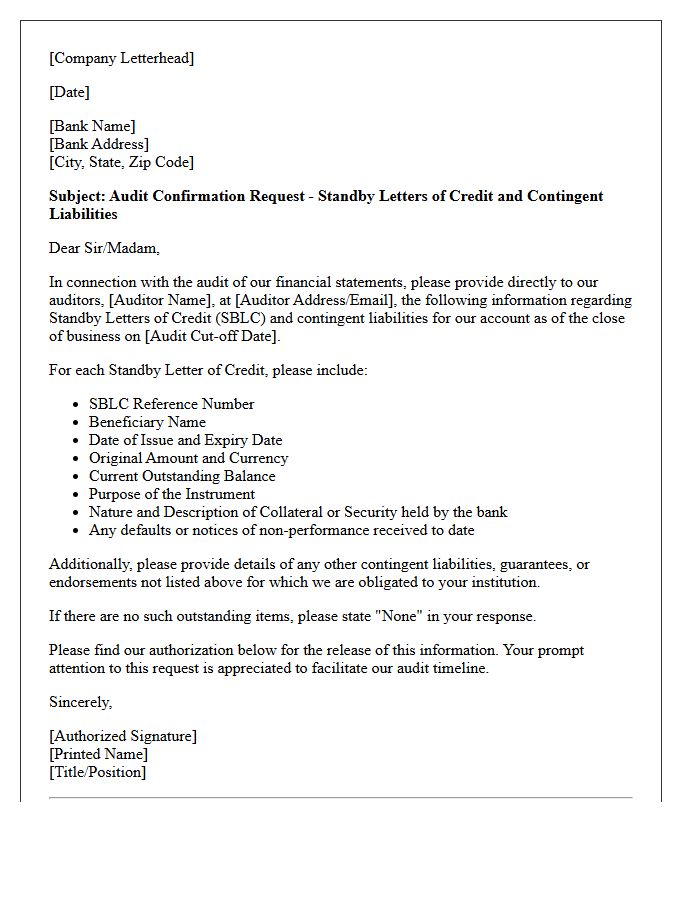

Standby Letter of Credit Contingent Liability Audit Letter

A Standby Letter of Credit represents a contingent liability that must be disclosed during a financial audit. Auditors use an audit letter to confirm the specific terms, expiration dates, and total exposure of these instruments directly with the issuing bank. This process ensures that potential payment obligations are accurately reported on balance sheets or within financial footnotes. Proper verification is crucial for maintaining transparency, as these credits only become active liabilities if the applicant defaults on their underlying contractual or financial obligations to the beneficiary.

What is a contingent liability audit confirmation letter?

A contingent liability audit confirmation letter is a formal request sent by a company's external auditors to its legal counsel to identify and verify any pending litigation, claims, or assessments that may impact the financial statements.

Why do auditors require a legal representation letter for contingent liabilities?

Auditors require this letter to obtain corroborative evidence regarding the existence, status, and potential financial exposure of legal matters, ensuring that all material liabilities are appropriately disclosed or accrued under accounting standards.

What key information is included in a contingent liability confirmation?

The letter typically includes a list of pending or threatened litigation, a description of the nature of the cases, the progress of proceedings, and the legal counsel's evaluation of the likelihood of an unfavorable outcome and estimated financial loss.

What is the difference between an asserted and an unasserted claim in an audit confirmation?

An asserted claim is an existing legal proceeding or formal demand already filed against the company, while an unasserted claim refers to potential legal actions that have not yet been filed but are probable and must be disclosed if a loss is reasonably possible.

How do auditors evaluate the responses received from legal counsel?

Auditors review the attorney's response for consistency with management's representations and financial records, focusing on "probable," "reasonably possible," or "remote" classifications to determine if a liability must be recorded on the balance sheet or disclosed in the footnotes.

Comments