A Debt Settlement Offer Proposal is a formal written request sent to creditors to resolve outstanding balances for less than the total amount owed. This strategic negotiation can provide financial relief and help you avoid bankruptcy by securing a manageable lump-sum payment. Understanding how to structure your request is essential for success. Below are some ready to use template options to help you start.

Image cover: Proven Debt Settlement Offer Letters and Templates for Successful Negotiation

Letter Samples List

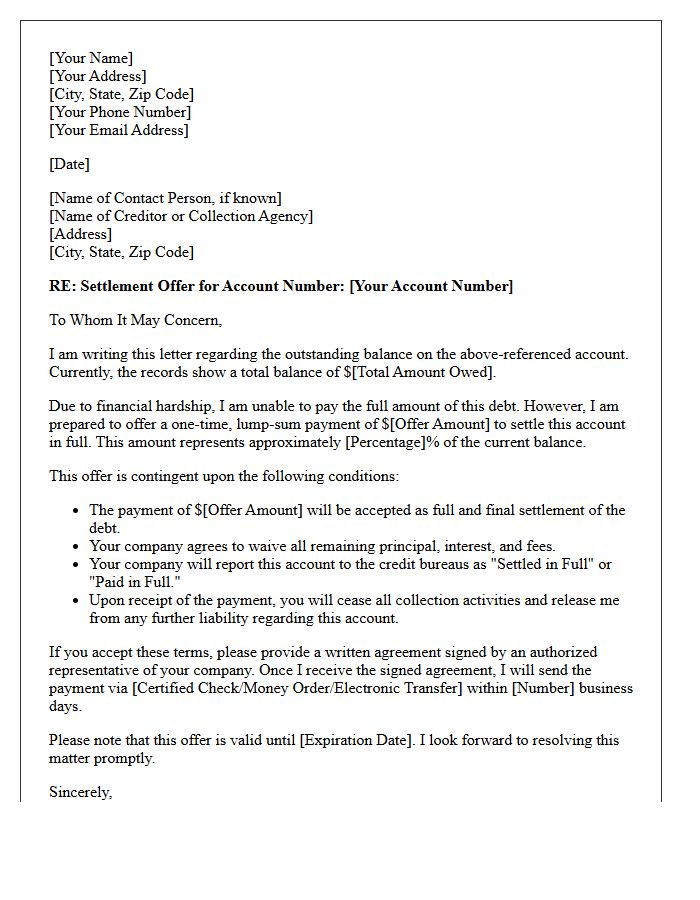

- Debt Settlement Offer Proposal Letter

- Lump Sum Debt Settlement Proposal Letter

- Financial Hardship Debt Settlement Offer Letter

- Installment Payment Debt Settlement Letter

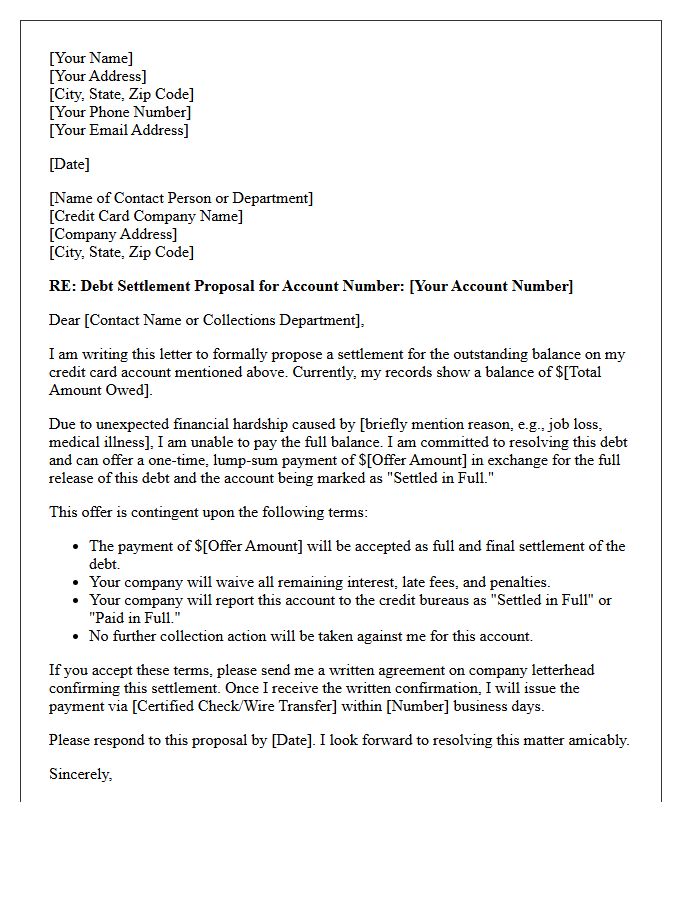

- Credit Card Debt Settlement Proposal Letter

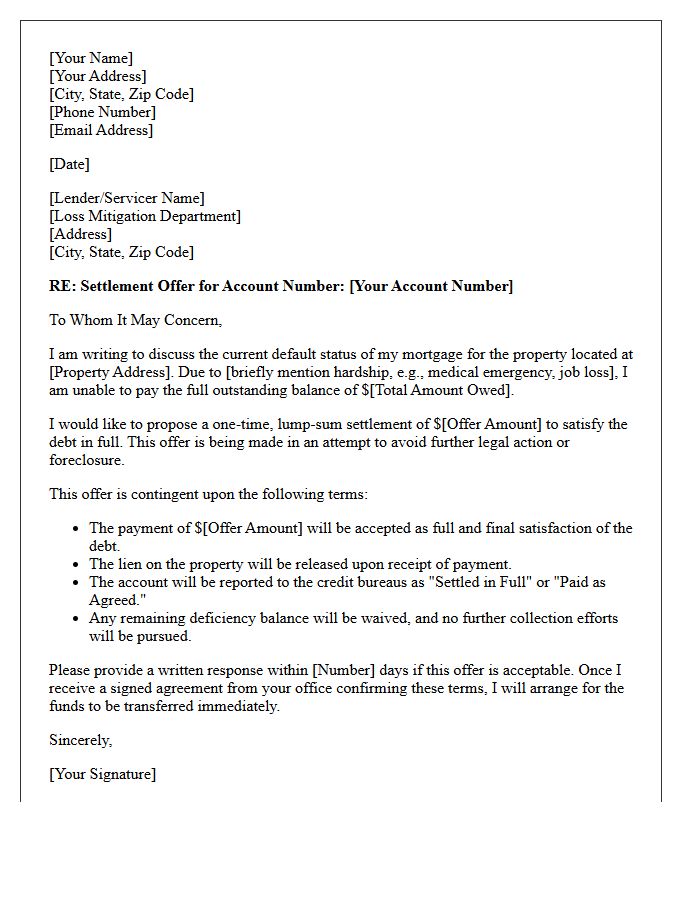

- Mortgage Default Debt Settlement Offer Letter

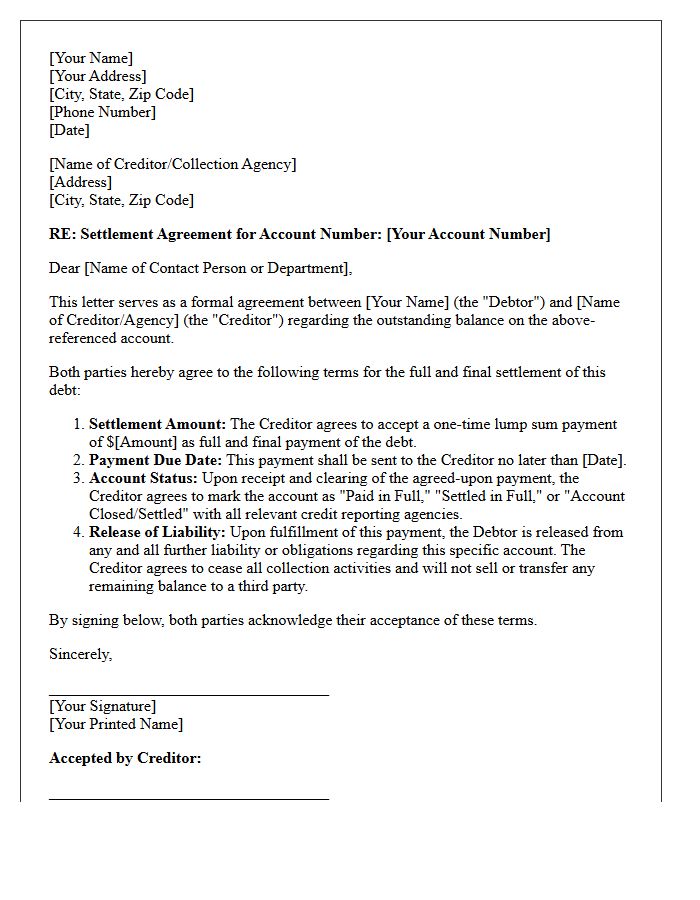

- Mutual Agreement Debt Settlement Letter

- Reduced Principal Debt Settlement Offer Letter

- Pre-Litigation Debt Settlement Proposal Letter

- Counter Offer Debt Settlement Letter

- Final Offer Debt Settlement Proposal Letter

- Account Charge-Off Debt Settlement Offer Letter

- Commercial Loan Debt Settlement Proposal Letter

Debt Settlement Offer Proposal Letter

A Debt Settlement Offer Proposal Letter is a formal document used to negotiate a reduced payment to satisfy a creditor. It is essential to clearly state your financial hardship and propose a specific lump-sum amount, typically lower than the total balance. Ensure the letter specifies that the payment serves as full and final settlement of the account. Always request a written acceptance before sending funds and keep copies for your records to protect your credit report from future disputes regarding the settled debt status.

Lump Sum Debt Settlement Proposal Letter

A Lump Sum Debt Settlement Proposal Letter is a formal written offer to pay a creditor a single, reduced payment to fully discharge a debt. This document is essential for legal protection, as it creates a paper trail of the negotiations. It should clearly state your account details, the specific settlement amount, and a request for a "settled in full" status on your credit report. Always ensure the creditor provides written acceptance before sending funds to prevent further collection efforts or future legal disputes regarding the remaining balance.

Financial Hardship Debt Settlement Offer Letter

A Financial Hardship Debt Settlement Offer Letter is a formal proposal sent to creditors to negotiate a reduced lump-sum payment. To be effective, the letter must clearly document insolvency or severe financial distress, such as medical crises or job loss. It acts as a legal record of your request to settle for less than the full balance. Always request that the agreement be put in writing and that the debt be marked as satisfied upon payment to protect your credit and prevent future collection efforts.

Installment Payment Debt Settlement Letter

An Installment Payment Debt Settlement Letter is a formal proposal to resolve outstanding balances through a structured repayment plan. It is crucial to negotiate a reduced total amount while ensuring the creditor agrees to stop further collection actions or interest accrual. This written agreement should clearly outline the payment schedule, amounts, and a confirmation that the debt will be marked as "satisfied" upon completion. Always obtain a signed copy before sending funds to legally protect your financial status and prevent future disputes over the remaining balance.

Credit Card Debt Settlement Proposal Letter

A credit card debt settlement proposal letter is a formal document used to negotiate a reduced lump-sum payment to resolve outstanding balances. To be effective, clearly state your hardship and specify the exact percentage of the total debt you can afford to pay. Request that the creditor marks the account as "settled in full" on credit reports. Always send this proposal via certified mail to ensure a paper trail. Securing a written agreement before sending funds is the most critical step in protecting your legal and financial interests.

Mortgage Default Debt Settlement Offer Letter

A Mortgage Default Debt Settlement Offer Letter is a formal proposal sent to lenders to resolve delinquent balances for less than the total amount owed. This document is a critical tool for deficiency waiver negotiations, potentially preventing foreclosure or legal judgments. To be effective, the letter must clearly outline your financial hardship, provide a specific lump-sum offer, and request a written agreement that the debt is considered fully satisfied. Ensuring the lender reports the account as settled in full is essential for protecting your long-term credit recovery and financial stability.

Mutual Agreement Debt Settlement Letter

A Mutual Agreement Debt Settlement Letter is a formal legal document used to finalize terms between a debtor and creditor. It confirms that the creditor accepts a reduced lump-sum payment as full satisfaction of the balance. Key elements include the settled amount, payment deadlines, and a written guarantee to update credit reports as "settled in full." This agreement protects you from future collection efforts or legal action by providing written proof that the debt is legally discharged, ensuring both parties are bound by the negotiated resolution.

Reduced Principal Debt Settlement Offer Letter

A Reduced Principal Debt Settlement Offer Letter is a formal proposal sent to creditors to resolve an outstanding balance for a single, lump-sum payment that is less than the total amount owed. This document serves as a critical legal record of the negotiation process. It must clearly outline the offered amount, payment terms, and a request for a full release of liability. Once accepted, it prevents future collection efforts and ensures the remaining deficiency is forgiven, helping consumers achieve financial recovery and stop compounding interest or late fees.

Pre-Litigation Debt Settlement Proposal Letter

A Pre-Litigation Debt Settlement Proposal Letter is a formal offer sent to creditors to resolve outstanding balances before legal action commences. This document serves as a strategic negotiation tool, aiming to reach a mutual agreement for a reduced lump-sum payment or a structured installment plan. By clearly outlining financial hardship and proposing a realistic settlement amount, debtors can potentially avoid costly courtroom proceedings and legal judgments. It is essential to request that the agreement be recorded in writing and that the debt be marked as "satisfied" to protect your credit profile.

Counter Offer Debt Settlement Letter

A Counter Offer Debt Settlement Letter is a formal proposal sent to creditors to negotiate a lower payoff amount. It serves as a legal record of your willingness to pay a specific lump sum while requesting the remaining balance be forgiven. To protect your credit, ensure the agreement includes a "paid in full" status and get all terms in writing before sending funds. This strategic communication is essential for debt reduction and achieving financial stability without paying the original total owed.

Final Offer Debt Settlement Proposal Letter

A Final Offer Debt Settlement Proposal Letter is a formal document sent to creditors to resolve outstanding balances for a reduced lump-sum payment. This legally binding negotiation tool clearly states your financial hardship and outlines a specific expiration date for the offer. It is crucial to demand a written agreement confirming that the payment settles the debt in full before sending any funds. This process helps prevent further collection actions and protects your future credit rating by ensuring the account is marked as settled rather than remaining in default.

Account Charge-Off Debt Settlement Offer Letter

An Account Charge-Off Debt Settlement Offer Letter is a formal proposal sent to creditors to resolve delinquent debt for less than the total balance. Once an account is "charged off," the creditor deems it uncollectible, providing a final opportunity to negotiate a lump-sum payment. It is crucial to ensure the agreement is in writing, explicitly stating that the payment will satisfy the debt in full. This process can stop collection efforts and prevent further legal action, though it may impact your credit score depending on the reported status.

Commercial Loan Debt Settlement Proposal Letter

A Commercial Loan Debt Settlement Proposal Letter is a formal document used to negotiate a reduced payoff for business obligations. It must clearly outline your financial hardship, the specific settlement amount offered, and a request for a "full and final release" from liability. Creditors review these proposals to assess if accepting a lump-sum payment is more viable than pursuing lengthy legal action or bankruptcy. Crafting a persuasive, professional letter is essential to demonstrate transparency and secure a mutually beneficial agreement that protects your company's remaining assets.

What should be included in a formal debt settlement offer proposal?

A formal debt settlement proposal should include your account number, a clear statement of your financial hardship, a specific lump-sum offer amount (typically 25% to 50% of the total balance), a deadline for the creditor's response, and a request that the remaining debt be forgiven and reported as "settled in full" to credit bureaus.

How much should I offer for a debt settlement lump-sum payment?

Most experts recommend starting your initial offer at roughly 25% to 30% of the outstanding balance. Creditors often counter-offer, with most final settlements landing between 40% and 60%. The final percentage depends on the age of the debt and the specific policies of the collection agency or original creditor.

Does a debt settlement offer proposal stop collection calls and lawsuits?

Submitting a proposal does not legally obligate a creditor to stop collection efforts or dismiss a pending lawsuit. However, many creditors will pause aggressive collection tactics while actively negotiating a settlement. Protection from legal action is only guaranteed once a written settlement agreement is signed by both parties and the payment is made.

What are the tax implications of a successful debt settlement?

If a creditor forgives $600 or more of a debt, the IRS considers the canceled amount as taxable income. You will likely receive a Form 1099-C at the end of the year. You must report this amount on your federal tax return, though you may be exempt if you can prove you were legally insolvent at the time of the settlement.

Should I get a debt settlement agreement in writing before paying?

Yes, you should never send a payment until you have a signed written agreement from the creditor. This document must explicitly state the agreed-upon amount, confirm that the payment satisfies the entire debt, and outline how the account will be reported to credit agencies. Verbal promises over the phone are not legally binding and provide no protection against future collections.

Comments