Receiving an insufficient funds notice for a post-dated check can lead to unexpected bank fees and legal complications. It is essential to communicate promptly with the recipient to resolve the payment issue and maintain professional credibility. Understanding your rights and responsibilities helps mitigate financial damage effectively. To assist you in drafting a formal response, below are some ready to use template.

Image cover: Professional Templates for Insufficient Funds Notices on Post-Dated Checks

Letter Samples List

- First Notice Letter for Post-Dated Check Insufficient Funds

- Final Warning Letter Regarding Unfunded Post-Dated Check

- Retail Banking Letter for Returned Post-Dated Check

- Commercial Account Letter for Post-Dated Check Insufficient Balance

- Bank Penalty Fee Letter for Bounced Post-Dated Check

- Official Dishonor Letter for Post-Dated Check Insufficient Funds

- Account Overdraft Alert Letter Due to Post-Dated Check

- Legal Action Warning Letter for Post-Dated Check Insufficient Funds

- Grace Period Notification Letter for Unfunded Post-Dated Check

- Corporate Banking Letter Regarding Post-Dated Check Insufficient Funds

- Customer Advisory Letter for Post-Dated Check Clearance Failure

- Returned Item Advice Letter for Post-Dated Check Insufficient Funds

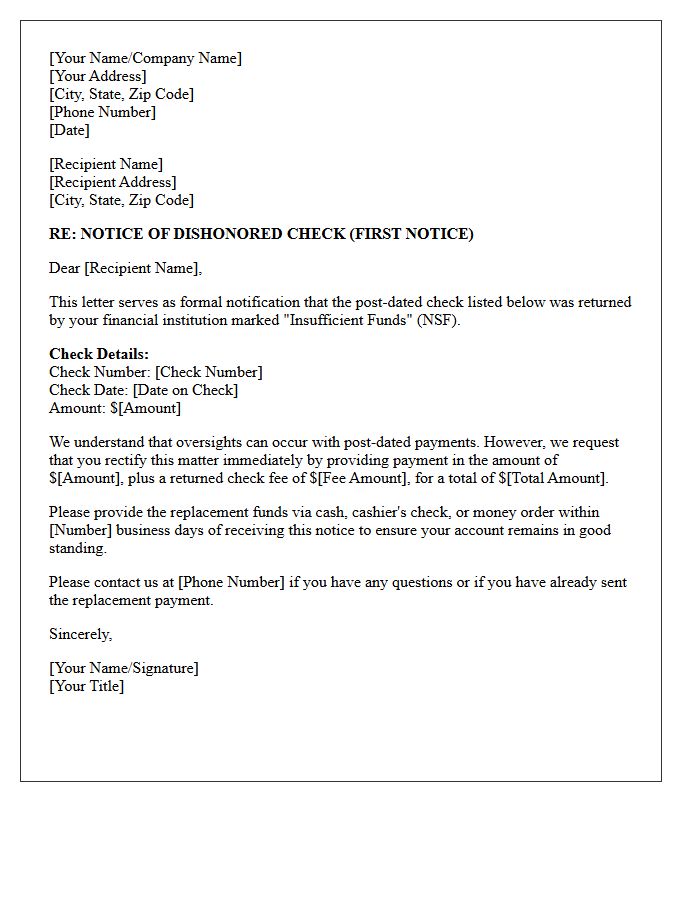

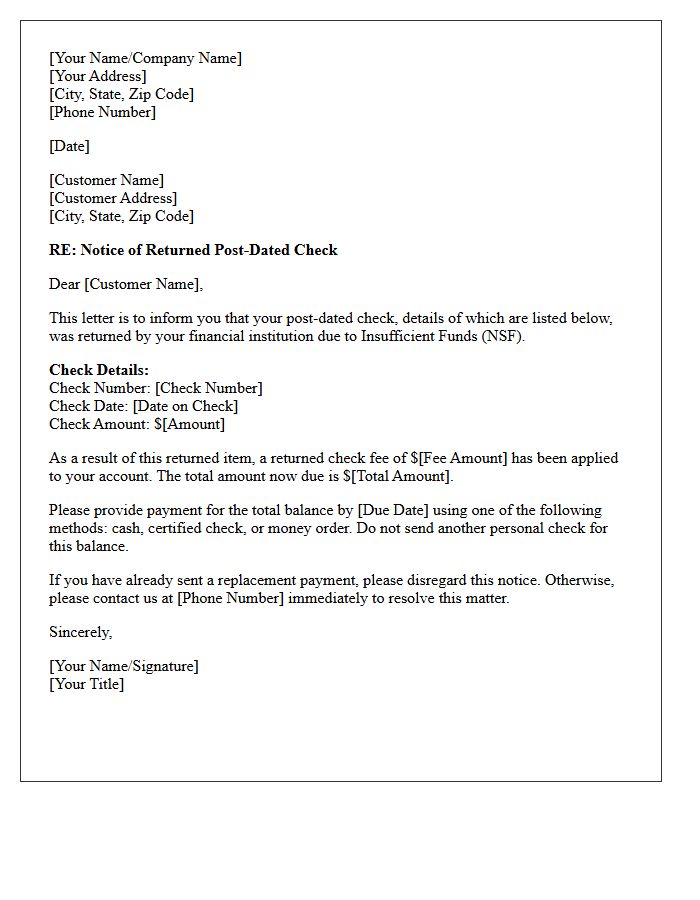

First Notice Letter for Post-Dated Check Insufficient Funds

A First Notice Letter serves as a formal legal demand after a post-dated check is dishonored due to insufficient funds. It officially notifies the issuer of the payment failure, providing a specific grace period to settle the debt plus applicable penalties. This document is a critical prerequisite for pursuing criminal prosecution or civil litigation under bouncing check laws. Receiving this notice requires immediate action to rectify the balance and avoid potential legal consequences or damage to your credit standing.

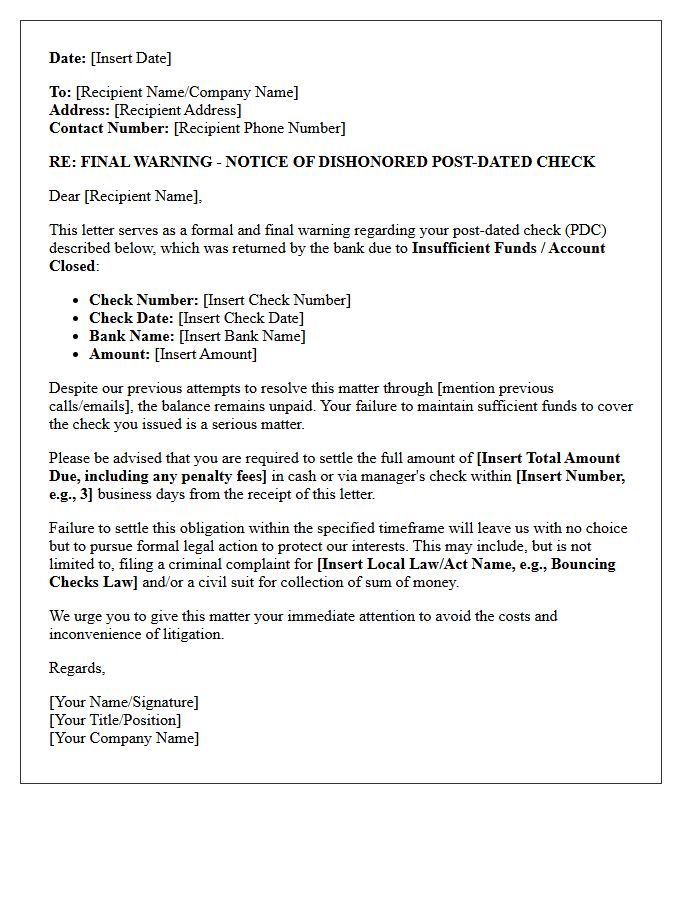

Final Warning Letter Regarding Unfunded Post-Dated Check

A final warning letter regarding an unfunded post-dated check serves as a formal notice before initiating legal action. It informs the issuer that their payment was returned due to insufficient funds, creating a serious financial default. To avoid criminal prosecution or civil litigation under debt recovery laws, the recipient must settle the outstanding balance immediately. This document acts as crucial evidence of a formal demand for payment, giving the debtor a final opportunity to rectify the breach of contract and maintain financial credibility before the matter escalates to court.

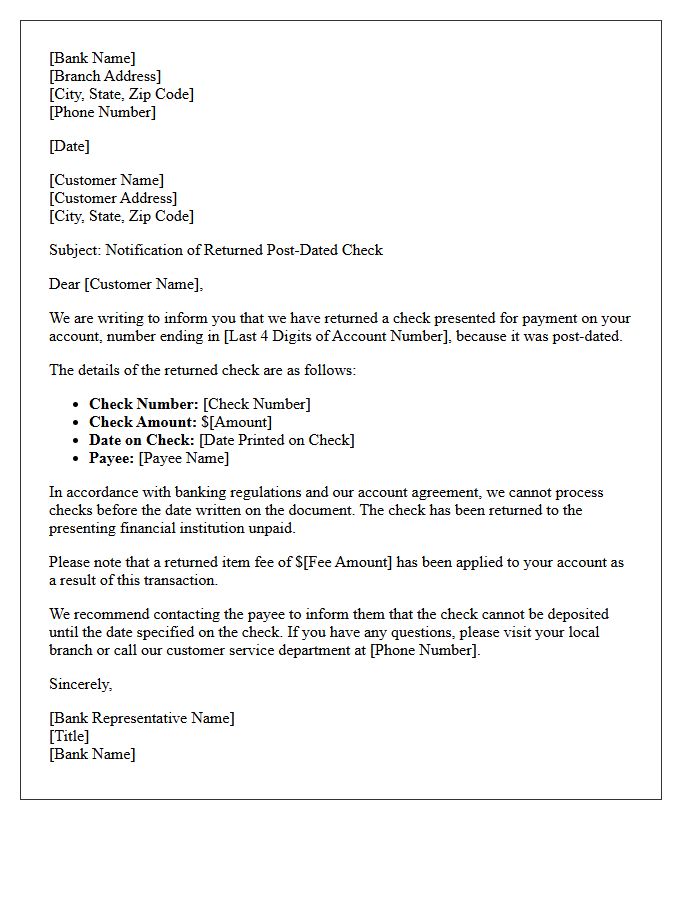

Retail Banking Letter for Returned Post-Dated Check

A retail banking letter for a returned post-dated check notifies the issuer that a payment was processed before its effective date or rejected due to insufficient funds. It is crucial to understand that banks may inadvertently process checks early unless a formal stop payment order is active. This notification serves as legal documentation of the dishonored instrument, potentially leading to administrative fees. Customers should immediately verify their account balance and contact the payee to resolve the outstanding debt and avoid negative impacts on their credit standing.

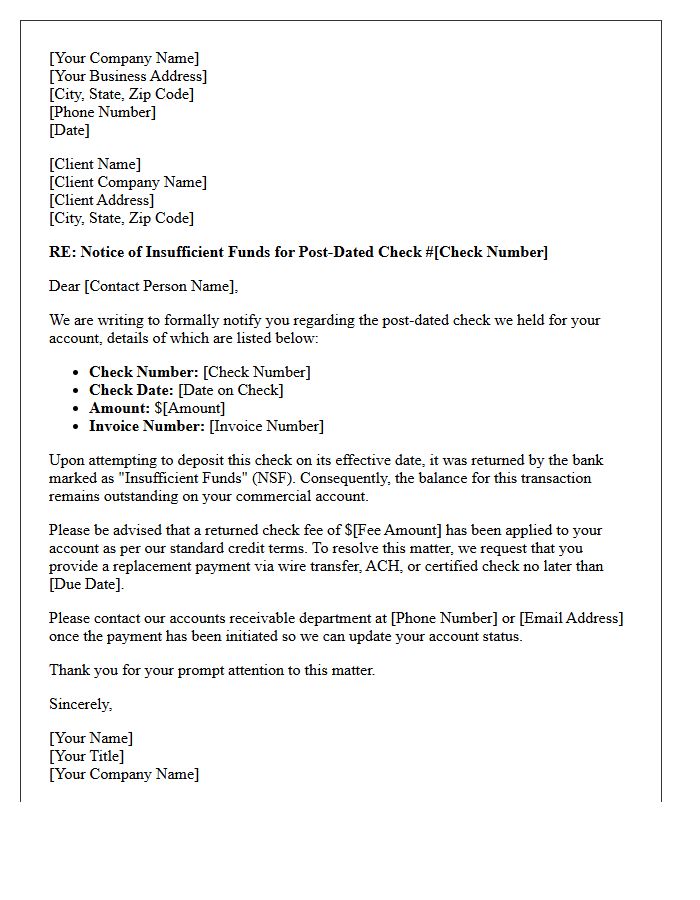

Commercial Account Letter for Post-Dated Check Insufficient Balance

A Commercial Account Letter for a post-dated check with an insufficient balance serves as formal notification that a scheduled payment cannot be honored. This document protects the issuer by proactively informing the payee of a liquidity issue before the deposit date. It helps maintain professional credibility and may prevent costly overdraft fees or legal complications. The letter should clearly request a payment extension or propose an alternative settlement date to preserve a stable business relationship and ensure future financial transparency between both parties.

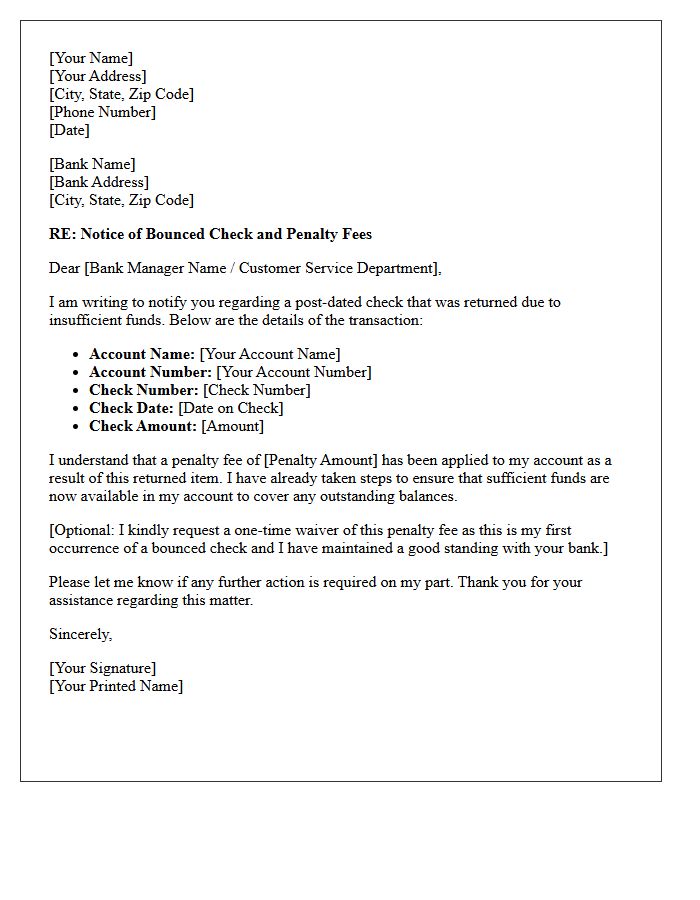

Bank Penalty Fee Letter for Bounced Post-Dated Check

A bank penalty fee letter informs you of charges incurred due to a bounced post-dated check. This occurs when an account has insufficient funds to cover a payment on its specified date. The notice details the specific penalty amount and the reason for the failed transaction. To avoid additional legal complications or negative impacts on your credit score, you must settle the outstanding balance and the associated service fees immediately. Always ensure your account is adequately funded before the check's maturity date to prevent these costly financial penalties.

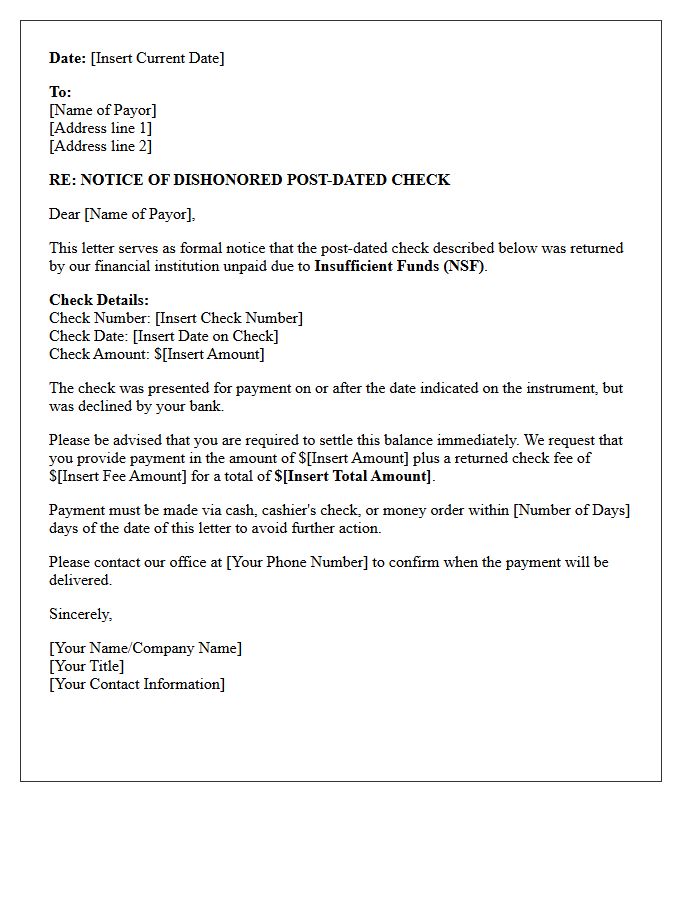

Official Dishonor Letter for Post-Dated Check Insufficient Funds

An official dishonor letter serves as a formal legal notice when a post-dated check is returned for insufficient funds. This document informs the issuer that their payment failed, demanding immediate restitution to avoid potential litigation. Under many jurisdictions, sending this notice is a mandatory step before pursuing civil penalties or criminal charges for bad checks. It must clearly state the check details, the reason for dishonor, and a specific deadline for payment to ensure the recipient is held legally accountable for the outstanding debt.

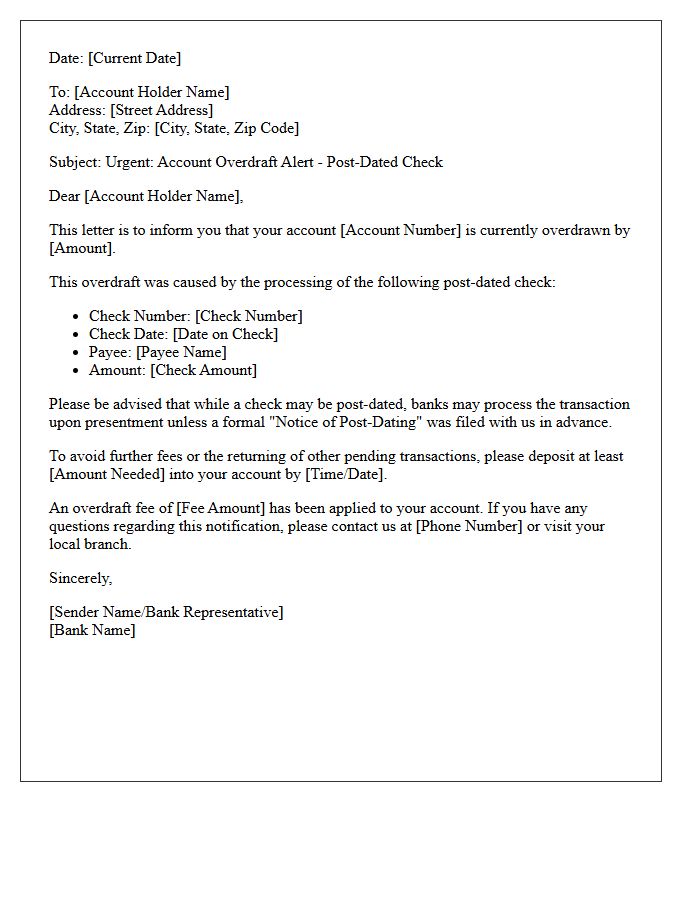

Account Overdraft Alert Letter Due to Post-Dated Check

Receiving an account overdraft alert letter indicates that a post-dated check was presented for payment before its scheduled date. Banks often process checks when received, regardless of the date written, which can lead to insufficient funds and costly penalties. To protect your finances, ensure your balance covers all outstanding checks immediately. Contact your financial institution to discuss fee reversals and consider overdraft protection to prevent future transaction failures. Always monitor your statements closely to maintain a positive account standing and avoid negative credit implications.

Legal Action Warning Letter for Post-Dated Check Insufficient Funds

A legal action warning letter for a post-dated check with insufficient funds serves as a formal notice before initiating litigation. It informs the issuer that their payment defaulted, demanding immediate settlement to avoid prosecution under financial crime statutes. Recipients are typically given a strict deadline to provide valid funds plus administrative fees. Ignoring this notice can lead to civil lawsuits or criminal charges, depending on local jurisdiction. To protect your rights, always send this formal demand via certified mail to maintain a documented paper trail for potential court proceedings.

Grace Period Notification Letter for Unfunded Post-Dated Check

A Grace Period Notification Letter informs clients that an unfunded post-dated check has been presented, offering a specific timeframe to settle the balance before legal actions or penalties occur. This formal notice serves as a final opportunity to rectify the payment default and maintain a positive credit standing. Timely communication is essential to avoid dishonored check charges or potential litigation under financial regulations. Ensure the account is funded immediately to prevent contractual termination or formal reporting to credit bureaus during this critical restitution period.

Corporate Banking Letter Regarding Post-Dated Check Insufficient Funds

Receiving a Corporate Banking Letter regarding a post-dated check with insufficient funds (NSF) is a critical legal and financial alert. This formal notice indicates that a future-dated payment was processed prematurely or lacked adequate coverage upon the specified date. To avoid account suspension or penalties, businesses must immediately rectify the balance. Maintaining liquidity management is essential, as repeated occurrences can damage your credit profile and lead to legal repercussions under banking regulations. Prompt communication with your relationship manager is necessary to resolve discrepancies and prevent service interruptions.

Customer Advisory Letter for Post-Dated Check Clearance Failure

A Customer Advisory Letter serves as a formal notification when a post-dated check (PDC) fails to clear due to insufficient funds or technical errors. It is crucial for maintaining clear communication and avoiding legal complications under financial regulations. Recipients must immediately address the payment default to prevent service disruptions or negative impacts on their credit standing. This document outlines the reason for dishonor and specifies the necessary steps for repayment or check replacement to ensure continued account compliance and professional trust between both parties.

Returned Item Advice Letter for Post-Dated Check Insufficient Funds

A Returned Item Advice Letter for a post-dated check with insufficient funds serves as formal notification that a payment was declined. It is crucial to resolve the balance immediately to avoid additional NSF fees or legal repercussions. Recipients should contact the issuing bank to verify account standing and coordinate with the payee for alternative payment methods. Maintaining accurate records of these notices is essential for financial tracking and protecting your credit reputation. Prompt action prevents service interruptions and potential collection efforts resulting from the failed transaction.

What should I do if I receive an "Insufficient Funds" notice for a post-dated check?

You should immediately contact the recipient to explain the situation and arrange an alternative payment method or request that they re-deposit the check at a later date once funds are available. It is also important to check your bank statement for any overdraft or returned item fees.

Can a bank process a post-dated check before the date written on it?

Yes, in many jurisdictions, banks can legally cash or deposit a post-dated check before the date on the instrument unless you have provided a formal "Notice of Post-Dating" to your financial institution. Without this specific legal notice, you risk an insufficient funds (NSF) notification if the money is withdrawn early.

What are the penalties for having a post-dated check returned for insufficient funds?

Common penalties include non-sufficient funds (NSF) fees charged by your bank, late payment fees from the merchant or creditor, and potential negative impacts on your ChexSystems report. In some cases, repeated occurrences may lead to the closure of your checking account.

How can I prevent insufficient funds issues with post-dated checks?

The most effective way to prevent these issues is to maintain a buffer in your account or set up overdraft protection. Additionally, you should notify your bank in writing about any post-dated checks you have issued to ensure they are not processed prematurely.

Is it illegal to write a post-dated check if I don't have the funds yet?

Writing a post-dated check is generally legal if done in good faith with the expectation that funds will be available by the date on the check. However, intentionally writing checks that you know will not clear can be considered "check kiting" or fraud, depending on local laws and the intent to deceive.

Comments