Managing an overdrawn checking account requires clear communication with your financial institution or employer to resolve a negative balance. Whether you are seeking emergency assistance or a salary advance, a formal request for funds is essential to avoid excessive overdraft fees and maintain financial stability. To help you draft a professional message quickly, below are some ready to use template.

Image cover: Professional Funds Request Templates for Overdrawn Checking Accounts

Letter Samples List

- First Notice of Overdrawn Checking Account Letter

- Urgent Request for Funds on Overdrawn Account Letter

- Standard Checking Account Overdraft Notice Letter

- Friendly Reminder of Negative Balance Resolution Letter

- Immediate Action Required for Overdrawn Account Letter

- Overdraft Fee Assessment and Funds Request Letter

- Grace Period Expiration on Overdrawn Account Letter

- Second Notice of Overdrawn Checking Account Letter

- Account Suspension Warning for Overdraft Letter

- Overdrawn Account Repayment Arrangement Letter

- Final Warning Before Account Closure Overdraft Letter

- Pre-Collections Notice for Overdrawn Account Letter

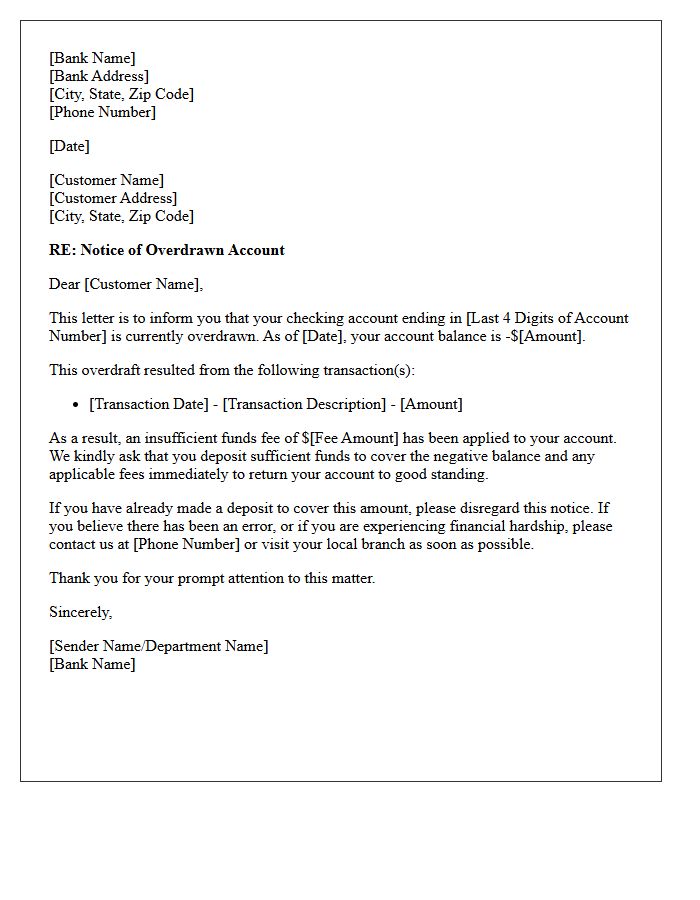

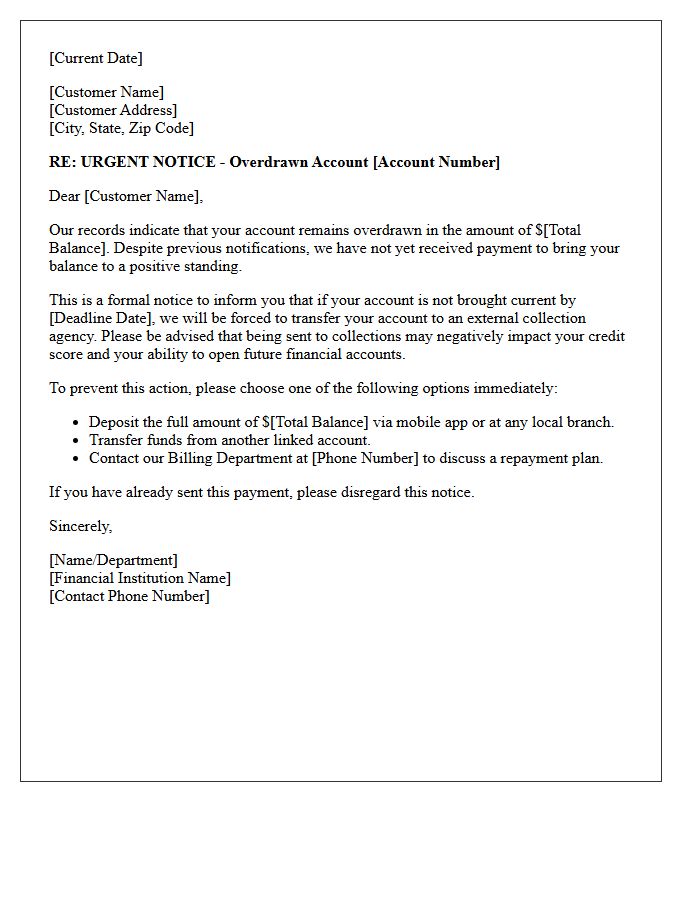

First Notice of Overdrawn Checking Account Letter

A First Notice of Overdrawn Checking Account is a formal notification from your bank indicating a negative balance. It is crucial to deposit funds immediately to cover the deficit and avoid escalating penalties. This letter typically outlines the specific overdraft fees charged per transaction. Promptly addressing this notice prevents the bank from reporting delinquency to credit bureaus or closing your account. Always review your recent transaction history for errors and contact your financial institution to discuss repayment options or potential fee waivers to protect your financial standing.

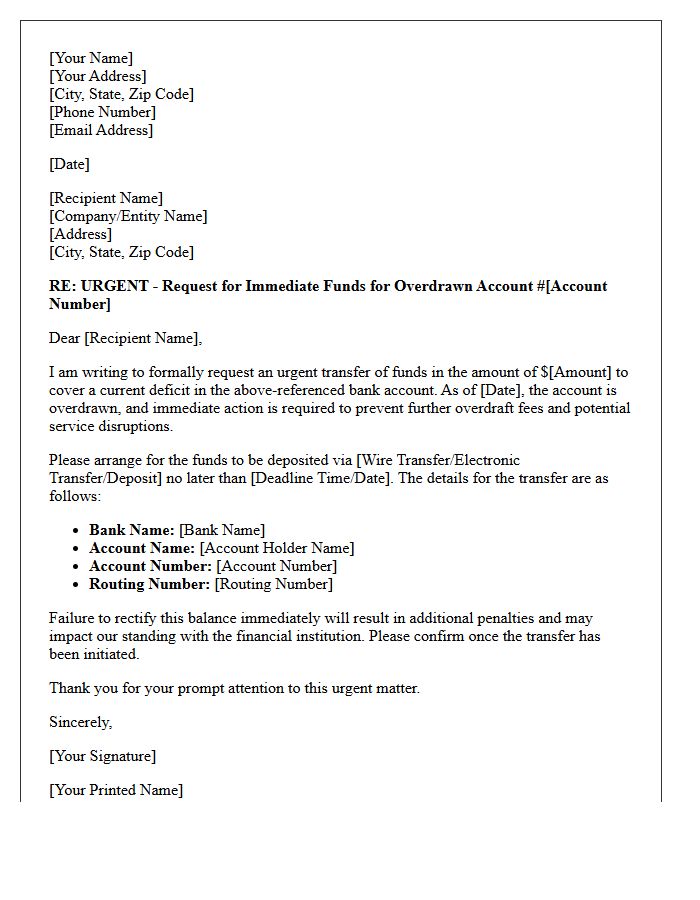

Urgent Request for Funds on Overdrawn Account Letter

An overdrawn account letter serves as a formal notification that your balance has fallen below zero. This urgent request requires immediate action to avoid mounting overdraft fees and potential account suspension. To resolve the deficit, you must deposit sufficient funds to cover the negative balance and any associated penalties. Timely communication with your bank is essential to negotiate fee waivers or establish a repayment plan. Ignoring this notice can severely damage your credit score and limit your future access to essential banking services and financial products.

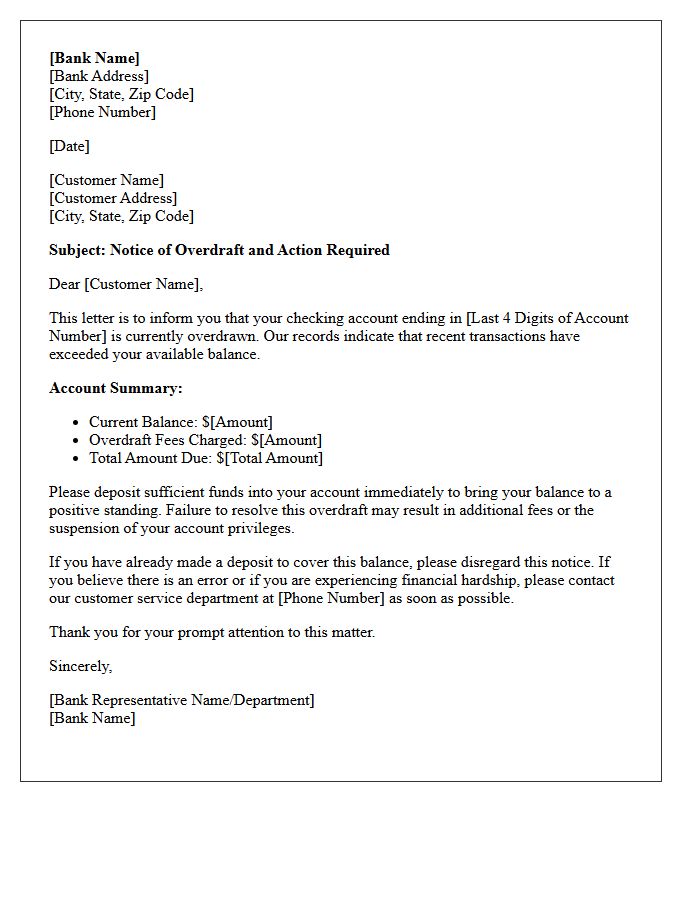

Standard Checking Account Overdraft Notice Letter

A Standard Checking Account Overdraft Notice Letter informs you when your balance falls below zero. It typically details the transaction amount, the resulting deficit, and any overdraft fees applied by the bank. Understanding this notice is crucial because it outlines your repayment obligations and the timeframe to restore a positive balance. Reviewing these letters helps you track spending habits and avoid consecutive penalties. Some banks also include options to opt-out of coverage or link a savings account to prevent future financial penalties and ensure account stability.

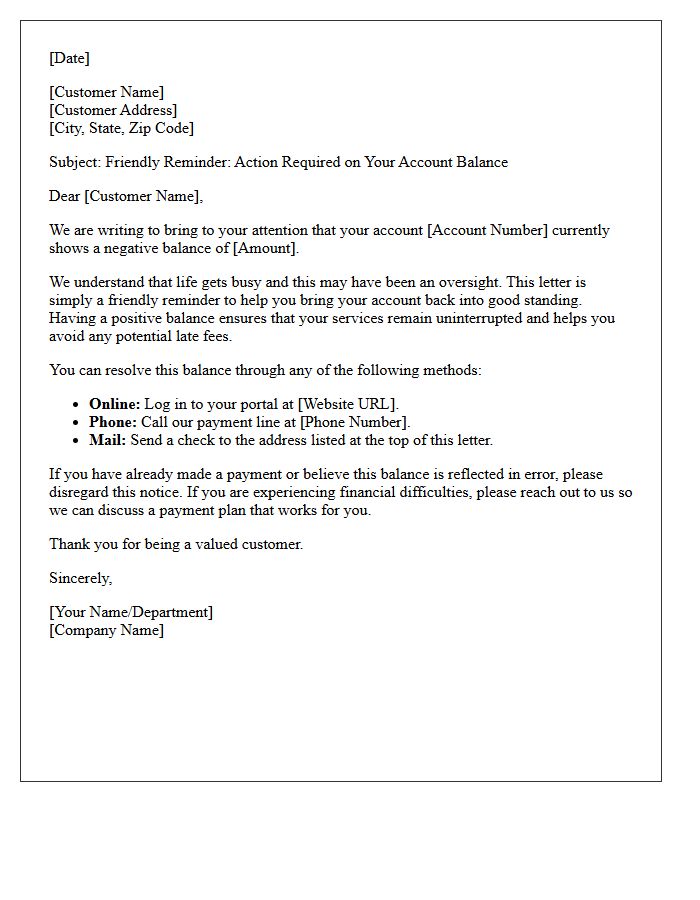

Friendly Reminder of Negative Balance Resolution Letter

A negative balance resolution letter is a formal notice requesting the immediate settlement of an outstanding overdrawn account. It is crucial to address this repayment obligation promptly to avoid additional service fees or potential account closure. Taking swift action protects your credit standing and ensures continued access to banking features. If you cannot pay the full amount, contacting the institution to discuss a payment arrangement is highly recommended. Resolving this discrepancy quickly demonstrates financial responsibility and maintains a positive relationship with your financial provider.

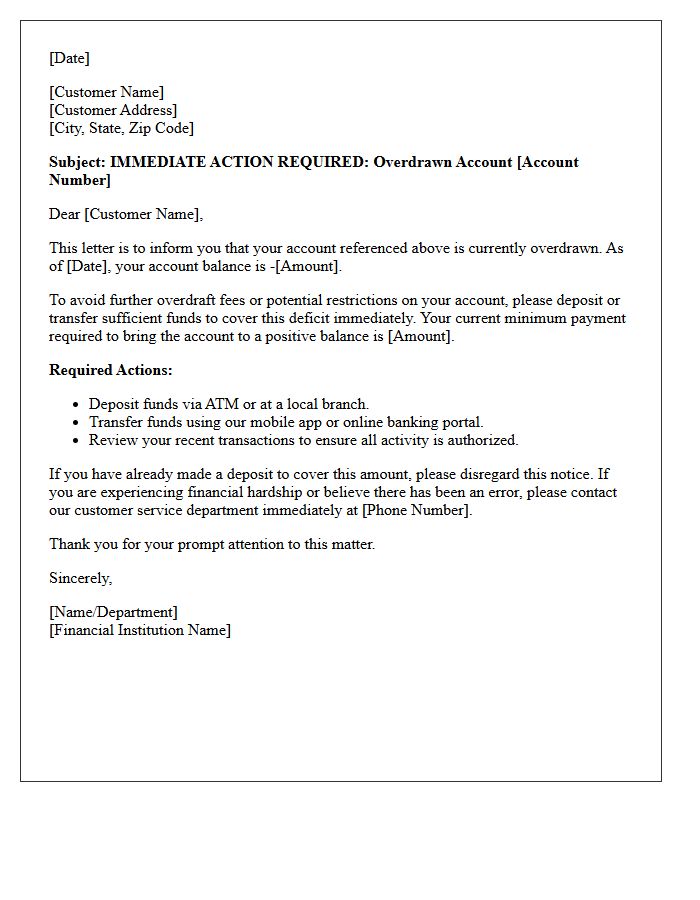

Immediate Action Required for Overdrawn Account Letter

Receiving an immediate action required notice for an overdrawn account means your balance is negative. You must deposit funds instantly to resolve the deficit and avoid escalating overdraft fees. Failure to act quickly can result in account closure, negative reports to credit bureaus, or collection activities. Contact your financial institution immediately to discuss repayment options or fee waivers. Maintaining a positive balance is essential to protect your financial standing and ensure continued access to banking services. Prioritize this notification to prevent further financial penalties or long-term banking restrictions.

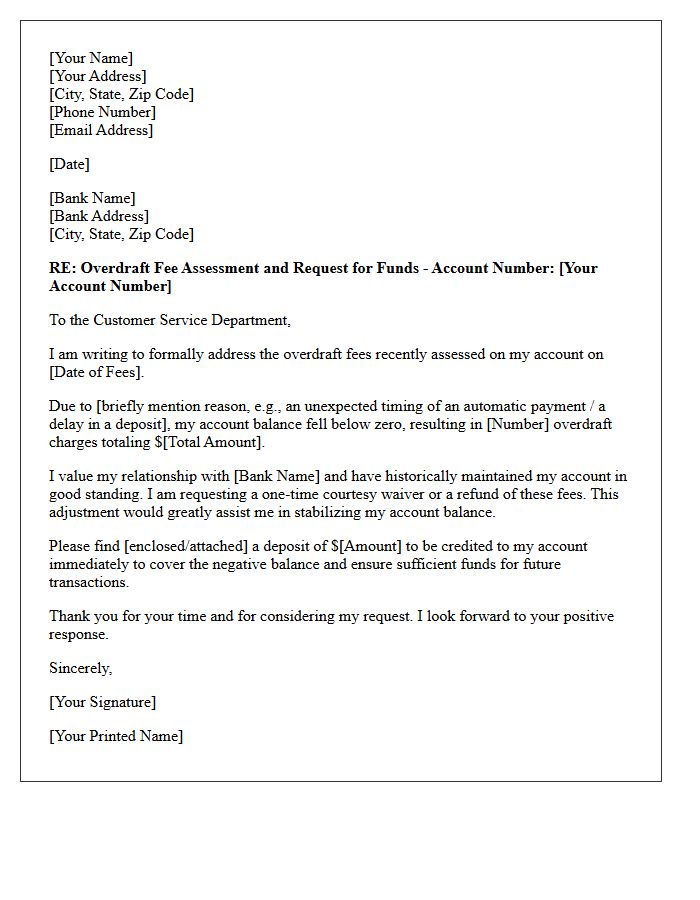

Overdraft Fee Assessment and Funds Request Letter

An Overdraft Fee Assessment occurs when a bank processes a transaction exceeding your available balance, resulting in high penalties. To mitigate financial loss, you can submit a Funds Request Letter to your financial institution. This formal document serves to request a fee waiver or a reversal of charges, often citing financial hardship or an isolated banking error. Providing a clear explanation and demonstrating a history of responsible account management increases your chances of a refund. Timely communication is essential to maintain a positive account standing and avoid escalating debt.

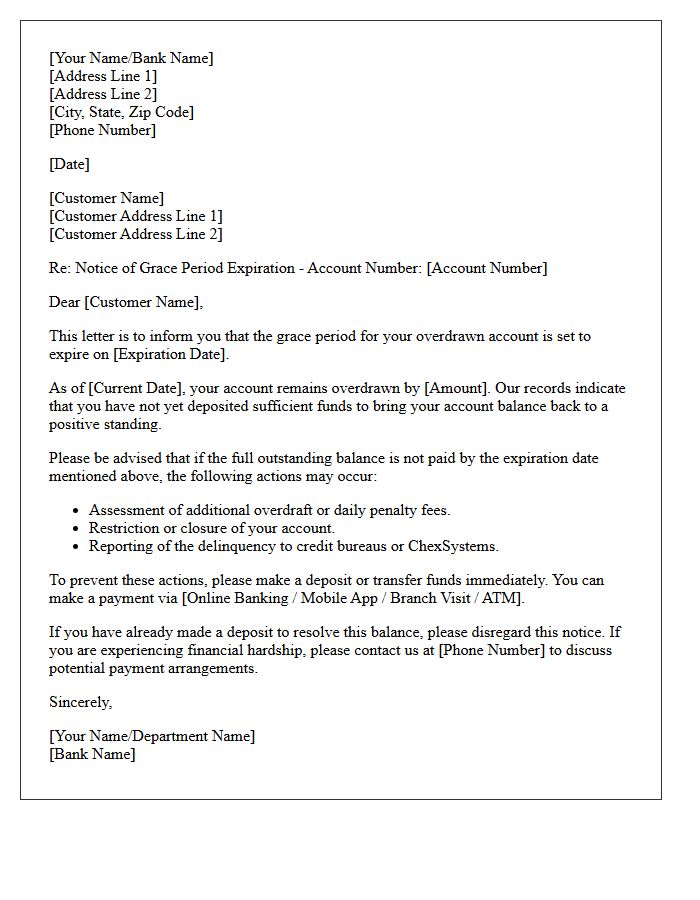

Grace Period Expiration on Overdrawn Account Letter

Receiving a Grace Period Expiration letter signifies that the temporary window to rectify a negative balance is ending. To avoid account closure and potential reporting to credit bureaus, you must deposit funds immediately. Failure to act results in overdraft fees and loss of banking privileges. If you cannot cover the deficit, contact your bank's hardship department to discuss repayment options before the deadline passes. Prompt action protects your financial reputation and prevents long-term legal collection efforts associated with unpaid overdrawn accounts.

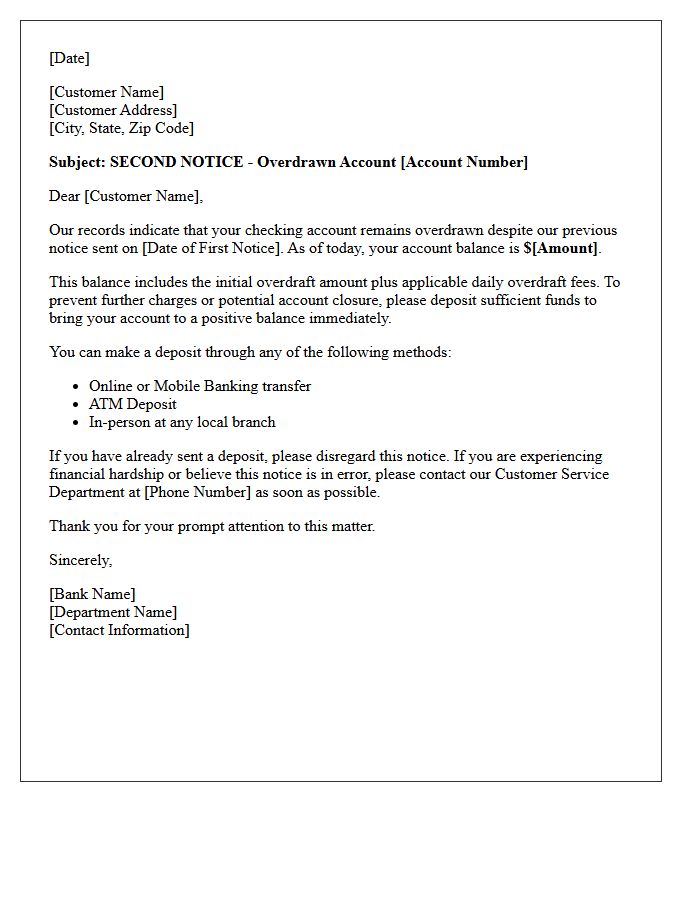

Second Notice of Overdrawn Checking Account Letter

A Second Notice of Overdrawn Checking Account is a critical formal warning indicating your balance remains negative. Receiving this letter means previous notifications were ignored, and you must repay the deficit immediately to avoid severe consequences. Failure to act often results in account closure, overdraft fees, and negative reporting to agencies like ChexSystems. This status can damage your financial reputation and hinder your ability to open future bank accounts. Contact your bank instantly to discuss repayment options or dispute errors before the debt is sent to a collection agency.

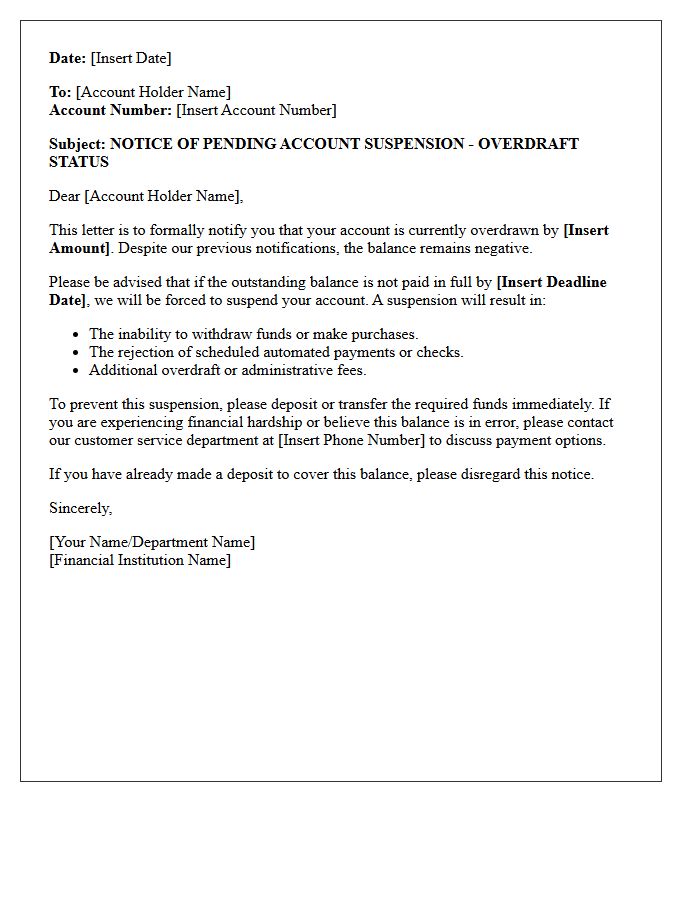

Account Suspension Warning for Overdraft Letter

Receiving an Account Suspension Warning indicates your bank account has remained in a negative balance for too long. This notice serves as a final overdraft alert before the financial institution restricts your access or closes the account entirely. To prevent long-term damage to your credit score and placement on banking blacklists like ChexSystems, you must immediately deposit funds to cover the deficit and any associated fees. Prompt action ensures your banking privileges remain intact and helps you avoid legal collections processes or involuntary account termination.

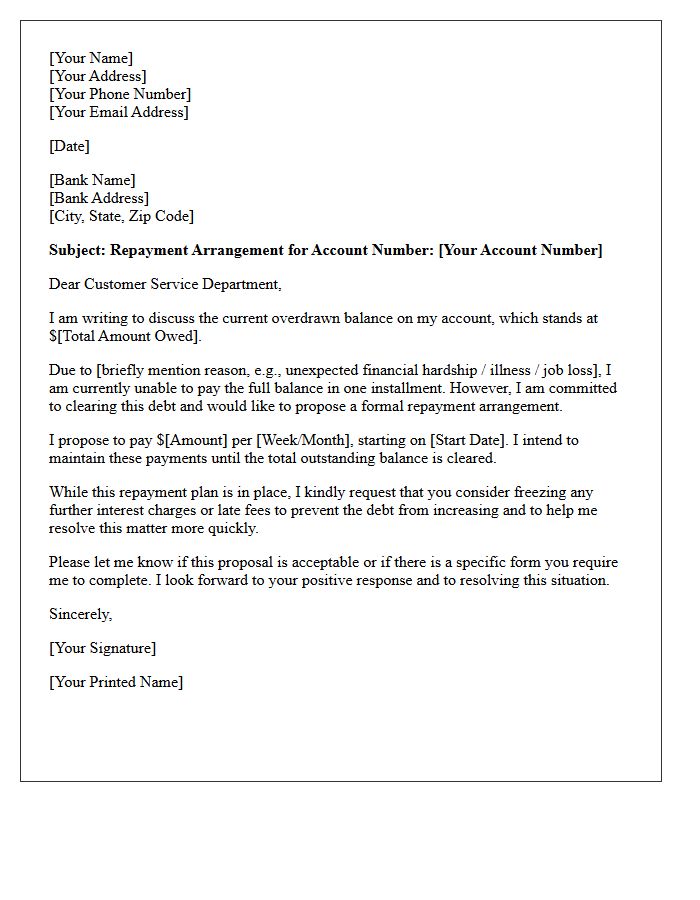

Overdrawn Account Repayment Arrangement Letter

An Overdrawn Account Repayment Arrangement Letter is a formal proposal sent to a bank to manage debt recovery. It outlines a structured plan to repay a negative balance through affordable monthly installments. This document is essential for financial recovery, as it helps prevent further penalty charges, protects your credit score, and demonstrates a proactive commitment to resolving arrears. Including a detailed income and expenditure summary ensures the proposal is realistic, increasing the likelihood that the lender will accept the terms and freeze ongoing interest.

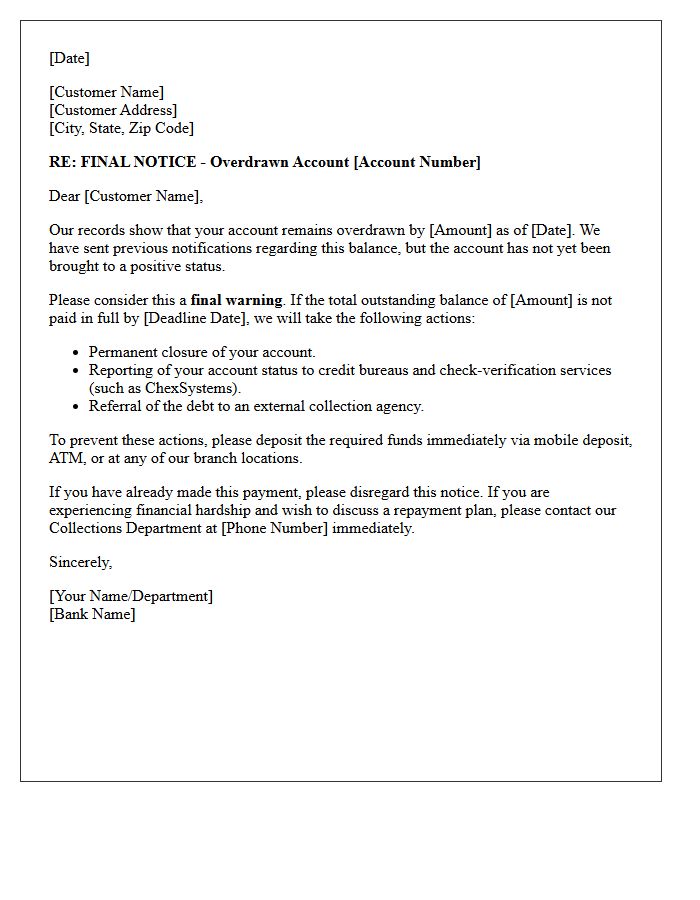

Final Warning Before Account Closure Overdraft Letter

Receiving a Final Warning Before Account Closure regarding an overdraft is a critical legal notice. It signifies that your bank will permanently terminate your banking relationship unless the outstanding balance is repaid immediately. This action can severely damage your credit score and prevent you from opening new accounts elsewhere. To avoid being reported to collection agencies or ChexSystems, you must contact your financial institution to settle the debt or establish a formal repayment plan before the specified deadline. Prompt action is essential to protect your financial standing.

Pre-Collections Notice for Overdrawn Account Letter

A Pre-Collections Notice is a final formal warning sent to account holders with a negative balance. This document serves as a last opportunity to settle the debt before the financial institution transfers the file to a third-party agency. It outlines the total amount owed, payment deadlines, and potential consequences, such as credit score damage or restricted banking access. Promptly addressing this notice is essential to prevent legal action and maintain financial standing. Always verify the debt details immediately to ensure accuracy and avoid unnecessary collection proceedings.

How can I request a fund transfer to cover an overdrawn checking account?

You can request funds by logging into your online banking portal, navigating to the "Transfers" section, and selecting a linked savings account or line of credit as the source to move money into your overdrawn checking account.

What should I include in a formal request for funds to resolve a negative balance?

A formal request should include your full name, account number, the specific dollar amount needed to clear the deficit, and the identified source of the incoming funds to ensure the overdrawn status is corrected immediately.

Are there automatic options to fund an overdrawn account?

Yes, most financial institutions offer Overdraft Protection services that automatically request and transfer funds from a backup savings account or credit card whenever your checking account balance falls below zero.

Can I request a fee waiver when adding funds to my overdrawn account?

If you deposit or transfer funds to correct the balance promptly, you can contact customer service to request a one-time courtesy refund of any non-sufficient funds (NSF) or overdraft fees associated with the transaction.

How long does it take for requested funds to reflect in an overdrawn account?

Internal transfers between accounts at the same bank typically reflect instantly, while requests for funds from external banks or wire transfers may take 1 to 3 business days to clear and resolve the negative balance.

Comments