Receiving an Unsecured Personal Loan Default Notice indicates that you have breached your repayment agreement. This formal document outlines the outstanding balance, the grace period for rectification, and potential legal consequences. Addressing this notice immediately is crucial to protect your credit score and avoid further collection actions. Below are some ready to use templates to help you respond effectively.

Image cover: Navigating the Unsecured Personal Loan Default Notice: Templates and Expert Samples

Letter Samples List

- Initial Unsecured Personal Loan Default Notice Letter

- First Warning Loan Default Notification Letter

- Second Notice of Unsecured Loan Default Letter

- Final Demand for Payment Default Letter

- Pre-Legal Action Loan Default Warning Letter

- Unsecured Loan Acceleration Notice Letter

- Breach of Loan Agreement Default Letter

- Delinquent Personal Loan Account Notification Letter

- Debt Collection Agency Transfer Notification Letter

- Unsecured Loan Charge-Off Advisory Letter

- Credit Bureau Reporting Default Warning Letter

- Notice of Default and Final Demand Letter

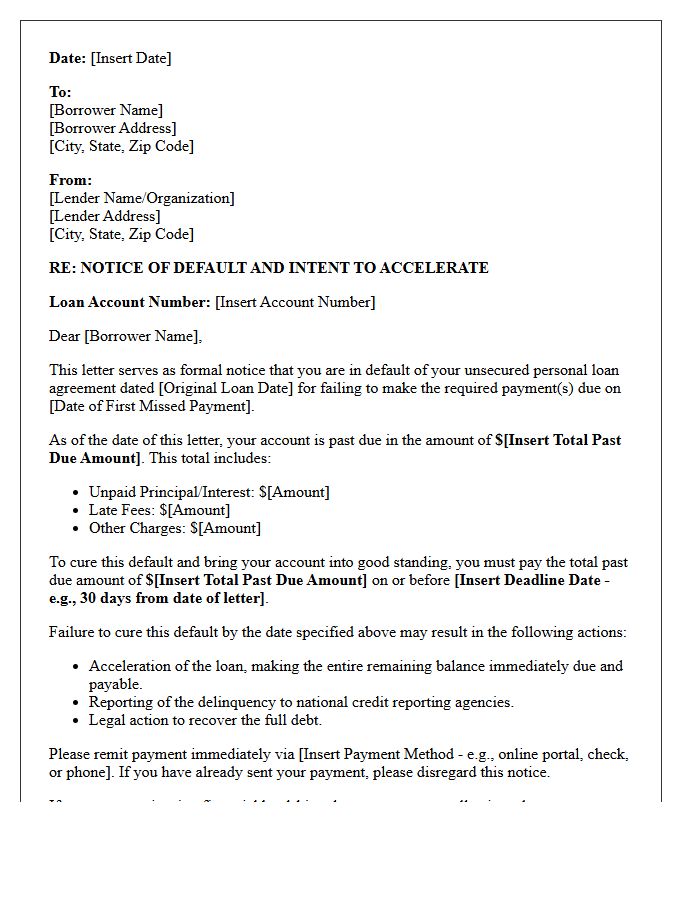

Initial Unsecured Personal Loan Default Notice Letter

An Initial Unsecured Personal Loan Default Notice Letter is a formal legal notification issued when a borrower misses a payment. This document officially states that the loan agreement has been breached and outlines the overdue balance required to rectify the account. It serves as a final opportunity to settle the debt before the lender initiates acceleration, demand for full repayment, or reports the delinquency to credit bureaus. Receiving this letter is critical because it marks the beginning of potential legal action and significant credit score damage if the default is not resolved immediately.

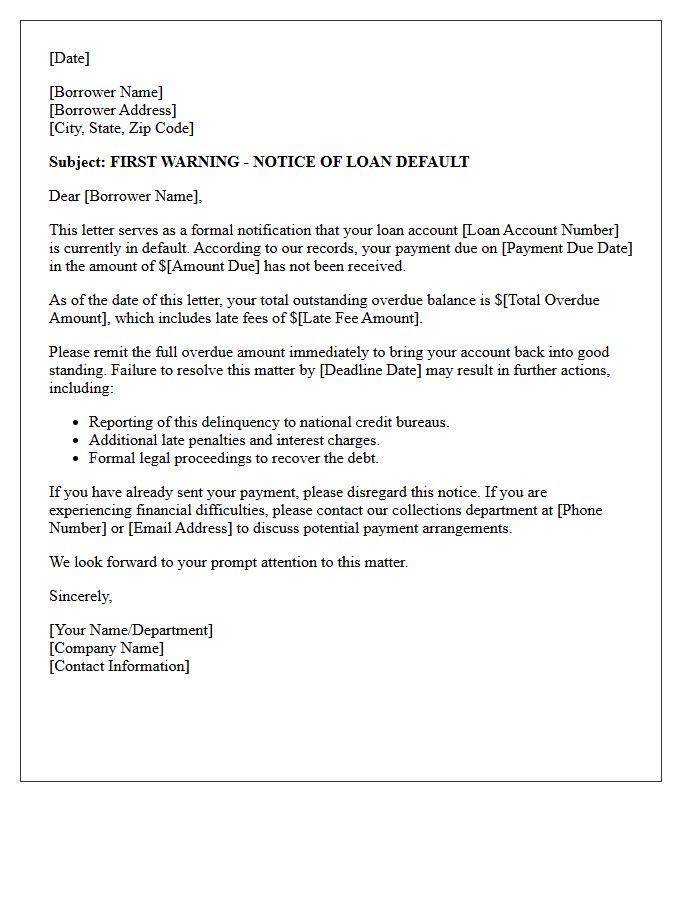

First Warning Loan Default Notification Letter

A First Warning Loan Default Notification Letter serves as a formal alert that you have missed a scheduled payment. Receiving this document is a critical compliance step, indicating your account is at risk of formal default. It outlines the total arrears, late fees, and a specific deadline to rectify the balance. Addressing this notice immediately is essential to protect your credit score and prevent further legal actions or asset repossession. Open communication with your lender can often lead to repayment arrangements before the situation escalates.

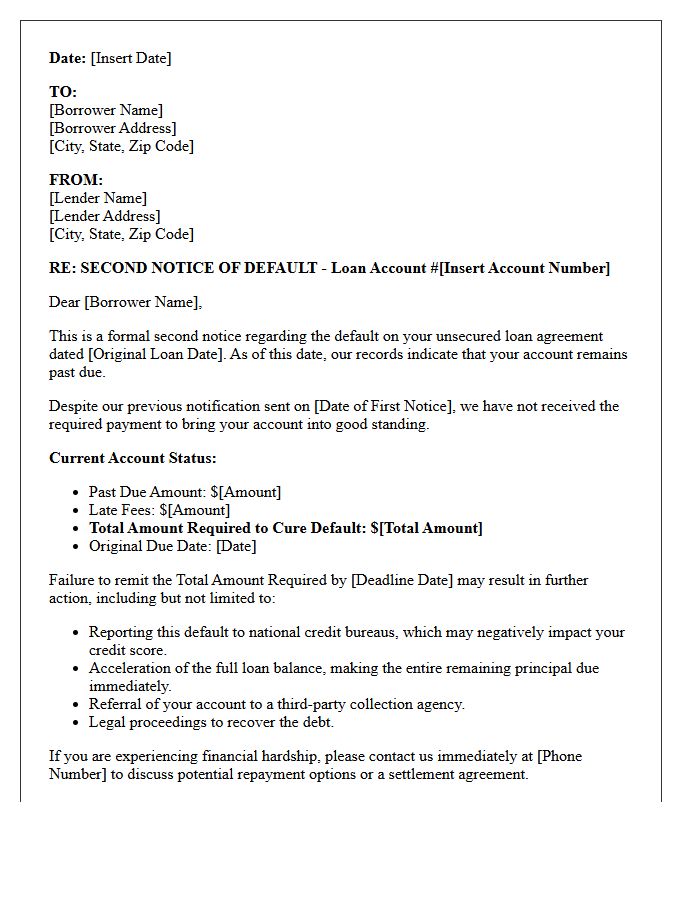

Second Notice of Unsecured Loan Default Letter

A Second Notice of Unsecured Loan Default is a critical formal warning indicating that your debt remains unpaid after initial contact. This letter serves as a final opportunity to rectify the breach before the lender pursues aggressive legal action or debt collection. Ignoring this document often leads to severe credit score damage and potential lawsuits. It is essential to contact the creditor immediately to negotiate a repayment plan or settlement to avoid further financial penalties and the permanent escalation of the recovery process.

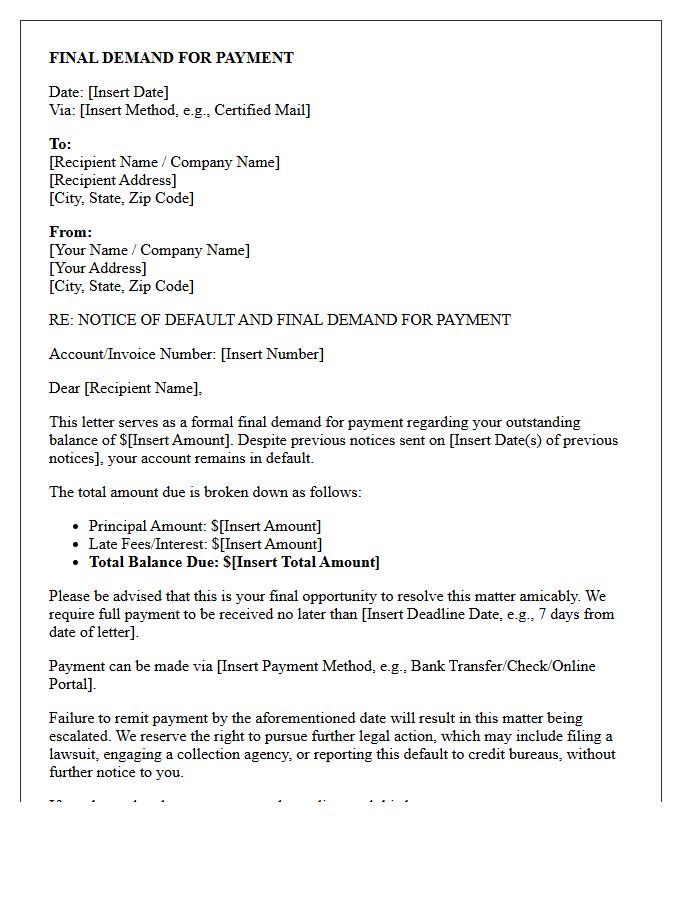

Final Demand for Payment Default Letter

A Final Demand for Payment Default Letter serves as a critical formal notice sent to a debtor before initiating legal action. It outlines the specific amount owed, the original due date, and a final deadline for settlement. This document provides clear evidence of a debt collection attempt, which is often a mandatory procedural requirement for court proceedings. By clearly stating the intent to pursue litigation or credit reporting, the letter encourages immediate resolution while establishing a legal paper trail to protect the creditor's rights during recovery efforts.

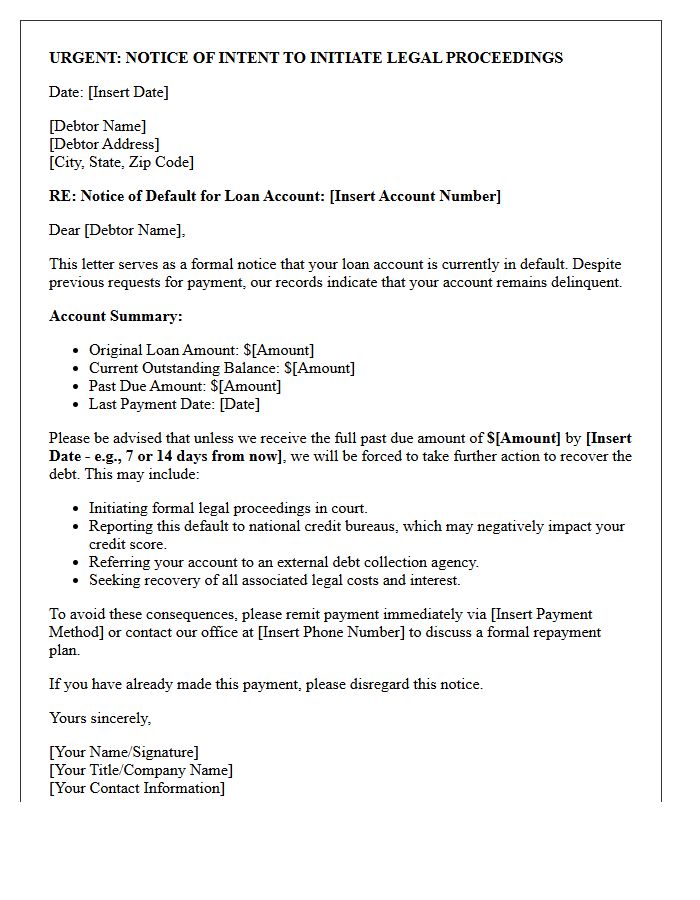

Pre-Legal Action Loan Default Warning Letter

A Pre-Legal Action Loan Default Warning Letter is a formal notice sent to borrowers who have breached their repayment agreement. This critical document serves as a final opportunity to settle outstanding debts before a creditor initiates formal litigation. It outlines the specific amount owed, the deadline for payment, and the potential consequences of inaction, such as court summons or negative impacts on credit scores. Receiving this letter indicates that the lender is preparing for legal recovery, making it essential for the recipient to respond immediately to avoid further costs or judgments.

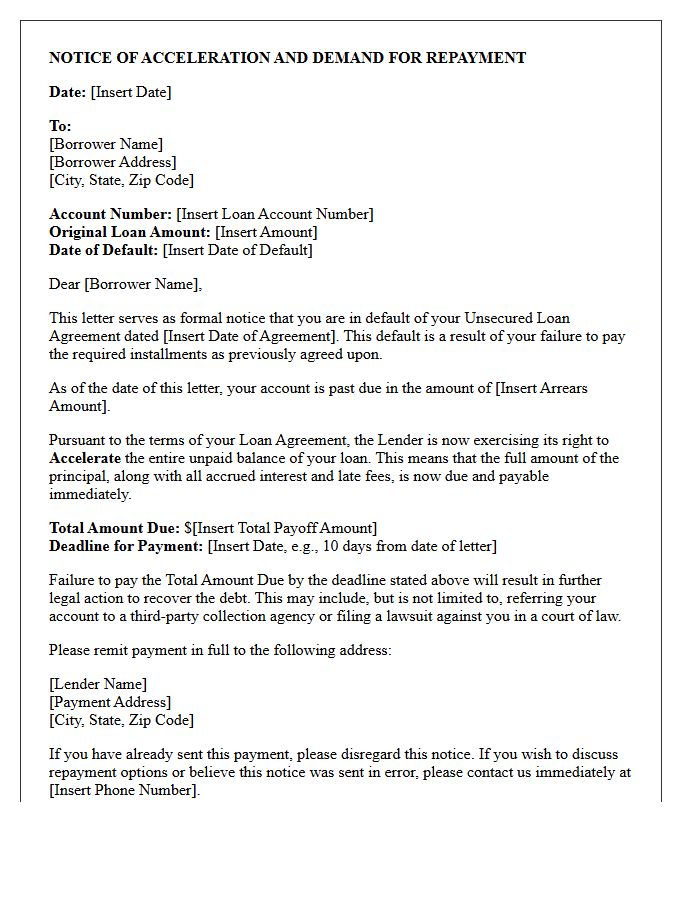

Unsecured Loan Acceleration Notice Letter

An Unsecured Loan Acceleration Notice Letter is a formal legal demand issued by a lender when a borrower defaults. This document serves as formal notification that the entire outstanding balance, including interest and fees, is now due immediately. Since the debt is unsecured, no collateral is at risk, but failure to pay often leads to aggressive debt collection, lawsuits, or significant credit score damage. Receiving this letter is a critical warning to negotiate a repayment plan or seek legal advice before the lender initiates formal court proceedings to recover the funds.

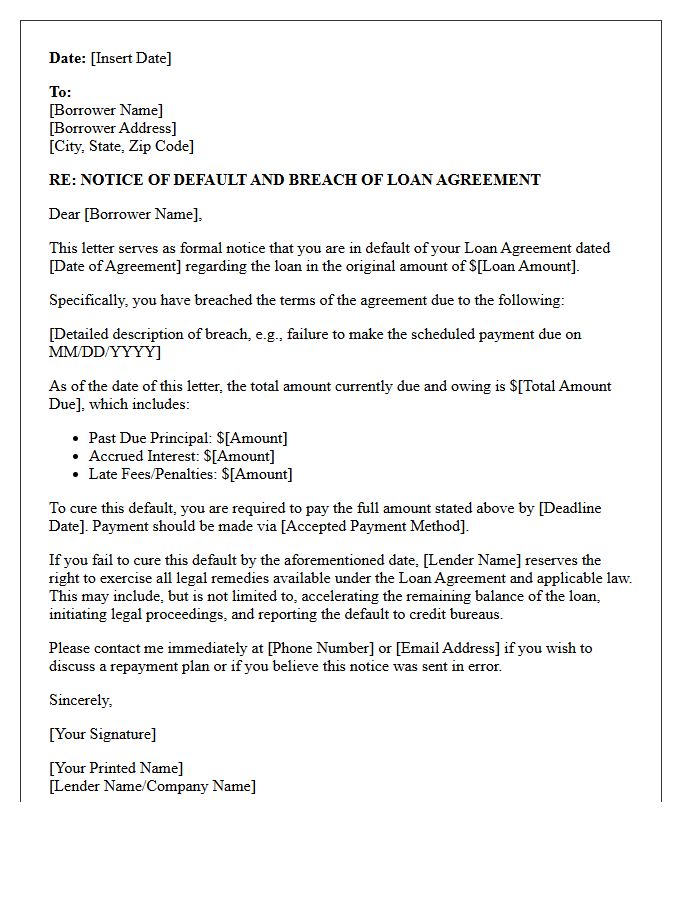

Breach of Loan Agreement Default Letter

A Breach of Loan Agreement Default Letter serves as a formal notification that a borrower has failed to meet specific contractual obligations. This document identifies the event of default, such as missed payments or covenant violations, and outlines the required remedial actions to avoid legal consequences. It typically includes a grace period for the borrower to rectify the breach. Receiving this letter is a critical legal step that precedes loan acceleration or debt collection, making it essential for parties to respond promptly to mitigate further financial or legal risk.

Delinquent Personal Loan Account Notification Letter

A Delinquent Personal Loan Account Notification Letter is a formal warning issued by lenders when payments are overdue. This document serves as a final opportunity to settle the balance before the debt is transferred to collections. Receiving this notice indicates that your credit score may be negatively impacted and legal action could follow. It is essential to contact the financial institution immediately to discuss repayment options, such as a deferment or a settlement plan, to avoid further penalties and long-term financial damage to your credit history.

Debt Collection Agency Transfer Notification Letter

A Debt Collection Agency Transfer Notification Letter is a formal document informing a consumer that their account has been moved to a third-party collector. Legally, this notice must specify the total balance owed and the name of the new agency. It is essential to verify the debt within thirty days of receipt to protect your consumer rights under the FDCPA. Always keep a copy for your records to ensure accurate credit reporting and to prevent potential harassment or double-payment errors during the transition between creditors.

Unsecured Loan Charge-Off Advisory Letter

An Unsecured Loan Charge-Off Advisory Letter is a formal notice indicating that a creditor has written off your debt as a loss due to extended non-payment. While this stops immediate internal collections, you remain legally obligated to repay the balance. This status severely damages your credit score and may lead to the debt being sold to a third-party collection agency or resulting in legal action. Receiving this letter is a critical warning to seek debt settlement or financial counseling to mitigate long-term financial consequences and potential litigation.

Credit Bureau Reporting Default Warning Letter

A Credit Bureau Reporting Default Warning Letter is a formal notice sent by creditors before reporting negative payment history to agencies like Equifax or Experian. Receiving this Default Warning signifies that your account is significantly overdue and risk formal legal default status. To protect your financial reputation, you must settle the outstanding balance or arrange a payment plan within the specified timeframe. Ignoring this letter will lead to a negative credit entry, severely lowering your credit score and hindering your ability to secure future loans, mortgages, or favorable interest rates.

Notice of Default and Final Demand Letter

A Notice of Default is a formal legal notification sent when a borrower fails to meet loan obligations. It serves as the final warning before foreclosure or legal action begins. This document outlines the specific amount overdue, any applicable late fees, and the deadline to cure the delinquency. Receiving a Final Demand Letter signifies that the grace period has ended and the lender intends to accelerate the debt. To protect your property and credit, you must respond immediately or settle the outstanding balance to prevent further litigation.

What is an unsecured personal loan default notice?

An unsecured personal loan default notice is a formal legal letter sent by a lender when a borrower has missed consecutive payments, officially notifying them that they have breached the loan agreement and must rectify the arrears to avoid further legal action.

What happens after I receive a notice of default on a personal loan?

Once a default notice is issued, you are typically given a specific timeframe-usually 14 to 30 days-to pay the overdue amount. Failure to comply allows the lender to "accelerate" the debt, demanding the full remaining balance immediately, and may lead to the debt being sold to a collection agency.

Will an unsecured personal loan default affect my credit score?

Yes, receiving a default notice and failing to resolve it will result in a default being recorded on your credit report. This negative mark remains visible to potential lenders for up to six years, significantly lowering your credit score and making it difficult to obtain future financing.

Can a lender take my assets if I default on an unsecured loan?

Because the loan is unsecured, the lender cannot seize specific assets like your home or car without a court order. However, if they successfully sue you and obtain a County Court Judgment (CCJ) or similar legal ruling, they may then apply for enforcement actions such as wage garnishment or a charging order.

How can I resolve a default notice to prevent further legal action?

The most effective way to resolve a default notice is to pay the specified arrears before the deadline. If you cannot afford the full amount, contact your lender immediately to negotiate a repayment plan or a settlement offer, as proactive communication can often halt the litigation process.

Comments