An Accountant Comfort Letter for private placements provides investors with professional assurance regarding a company's financial health and unaudited data. These documents are essential for due diligence and regulatory compliance during capital raises, bridging the gap between audited statements and the offering date. Understanding their scope helps mitigate financial risk for all stakeholders. Below are some ready to use templates.

Image cover: The Definitive Guide to Accountant Comfort Letters for Private Placements: Samples and Templates

Letter Samples List

- Standard Accountant Comfort Letter for Bank Private Placements

- Bring-Down Comfort Letter for Banking Securities Offerings

- Negative Assurance Letter for Interim Banking Financials

- Agreed-Upon Procedures Letter for Bank Loan Portfolios

- Pro Forma Financials Comfort Letter for Bank Mergers

- Subordinated Debt Private Placement Accountant Comfort Letter

- Regulatory Capital Ratios Verification Comfort Letter

- Asset Quality and Provisioning Accountant Letter

- Draft Accountant Comfort Letter for Placement Agents

- Final Rule 144A Offering Comfort Letter for Banks

- Net Interest Margin Financial Data Comfort Letter

- Tier One Capital Compliance Accountant Letter

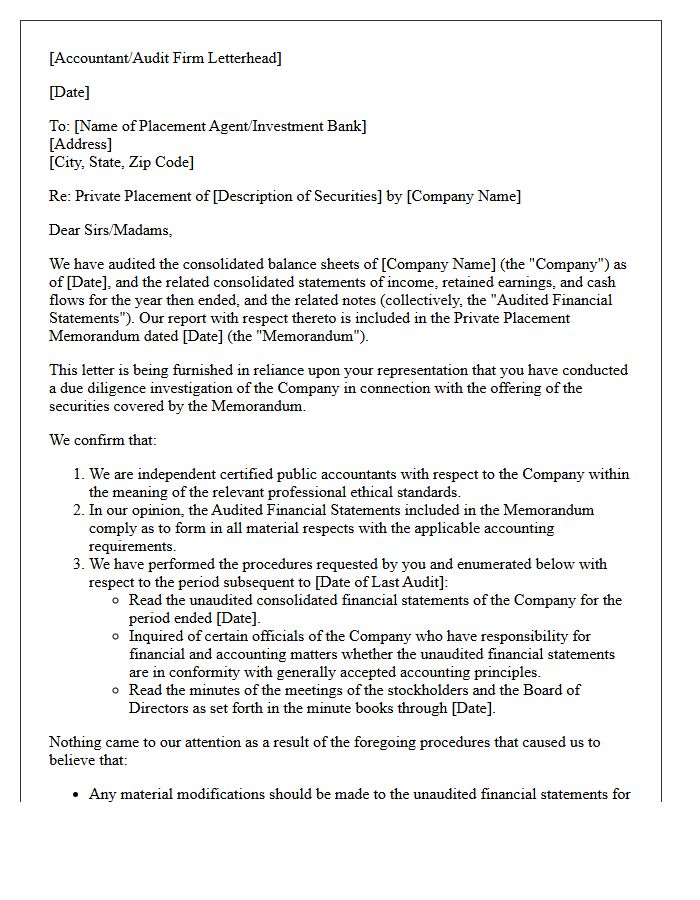

Standard Accountant Comfort Letter for Bank Private Placements

A Standard Accountant Comfort Letter provides negative assurance to underwriters regarding financial data in a private placement offering. It confirms that auditors performed specific procedures, ensuring the financial information aligns with audited statements. This document is crucial for the bank's due diligence process, helping mitigate legal risk under securities laws. It bridge the gap between the last audit and the closing date, verifying that no material adverse changes occurred. While not a guarantee, it offers essential verification for institutional investors participating in non-public debt or equity issuances.

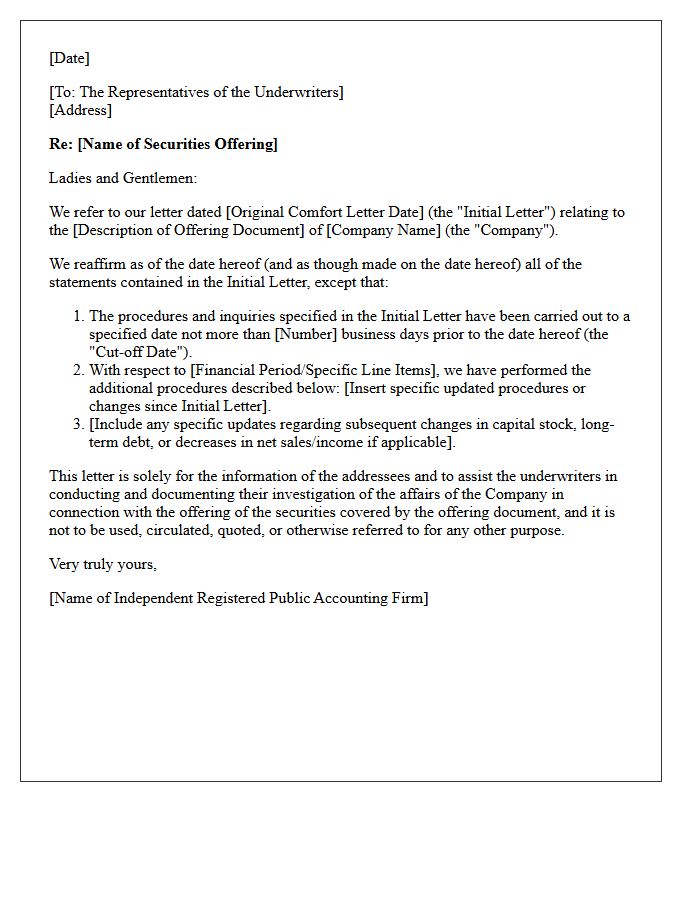

Bring-Down Comfort Letter for Banking Securities Offerings

A Bring-Down Comfort Letter is a critical document issued by external auditors to underwriters during a securities offering. It serves as an update to the initial comfort letter, typically delivered at the closing of the transaction. This letter confirms that no significant adverse financial changes have occurred between the initial audit and the closing date. By verifying the ongoing accuracy of financial data, it provides essential due diligence protection for investment banks, ensuring that all financial representations remain valid and reducing potential liability for material misstatements or omissions in offering documents.

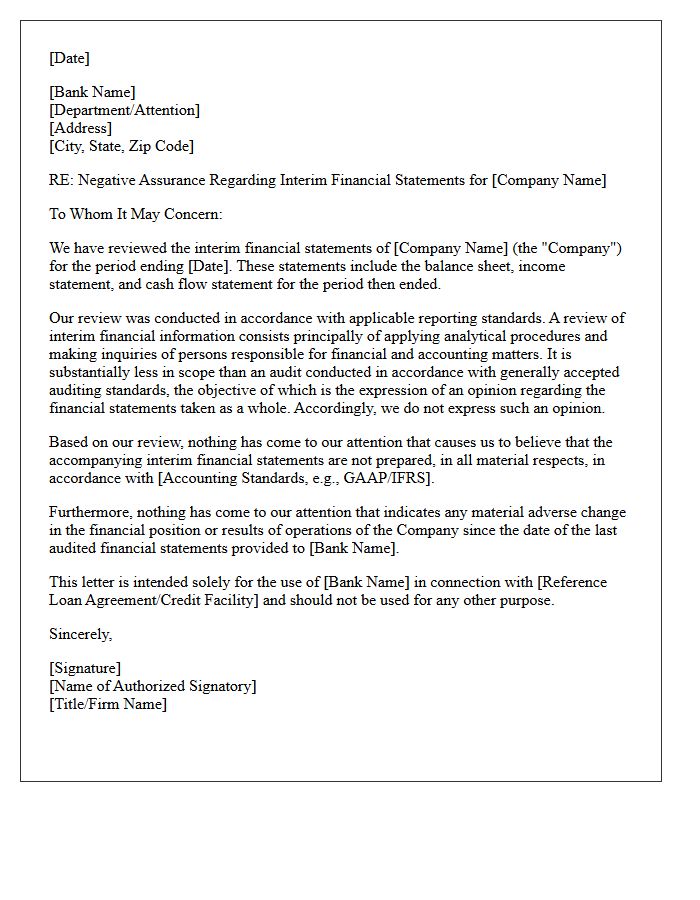

Negative Assurance Letter for Interim Banking Financials

A Negative Assurance Letter is a critical document provided by auditors regarding interim banking financials. It states that, based on a limited review, no material modifications are necessary for the financial statements to comply with reporting standards. Unlike a full audit, it offers limited assurance rather than a positive opinion. This process is essential for regulatory compliance and maintaining investor confidence during quarterly updates. It confirms that nothing has come to the auditor's attention suggesting the data is misstated, ensuring transparency in a bank's ongoing fiscal health.

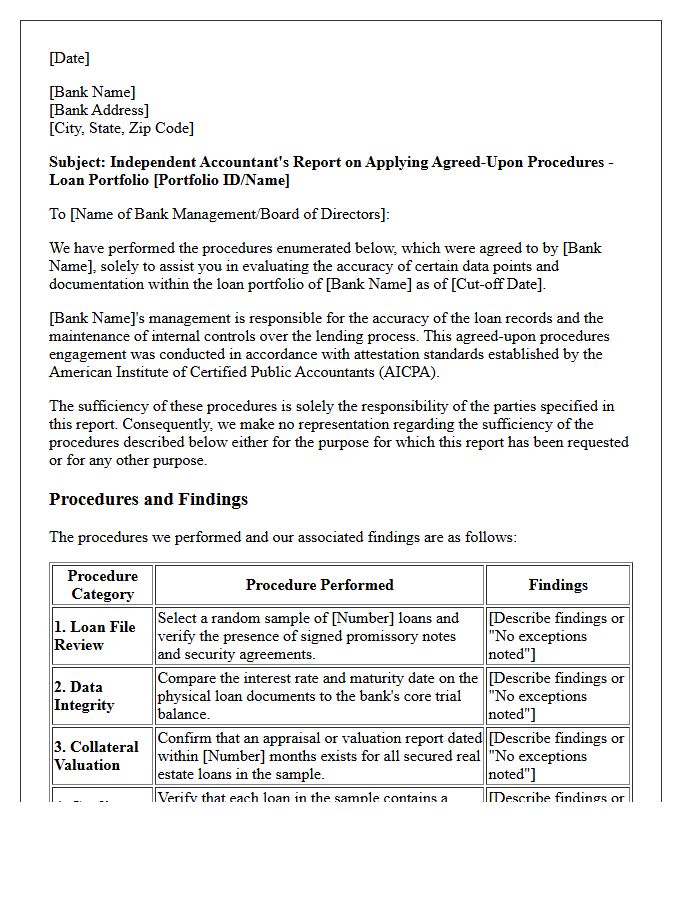

Agreed-Upon Procedures Letter for Bank Loan Portfolios

An Agreed-Upon Procedures (AUP) letter provides a specific, objective report on a bank's loan portfolio. Unlike a full audit, the practitioner performs customized tests defined by the lender or regulators to verify data accuracy, collateral documentation, and compliance with credit policies. This targeted verification enhances transparency for stakeholders by highlighting potential risks and exceptions within the asset pool. It serves as a vital tool for risk management and due diligence, ensuring that the reported quality of the loan portfolio aligns with actual performance and documentation standards.

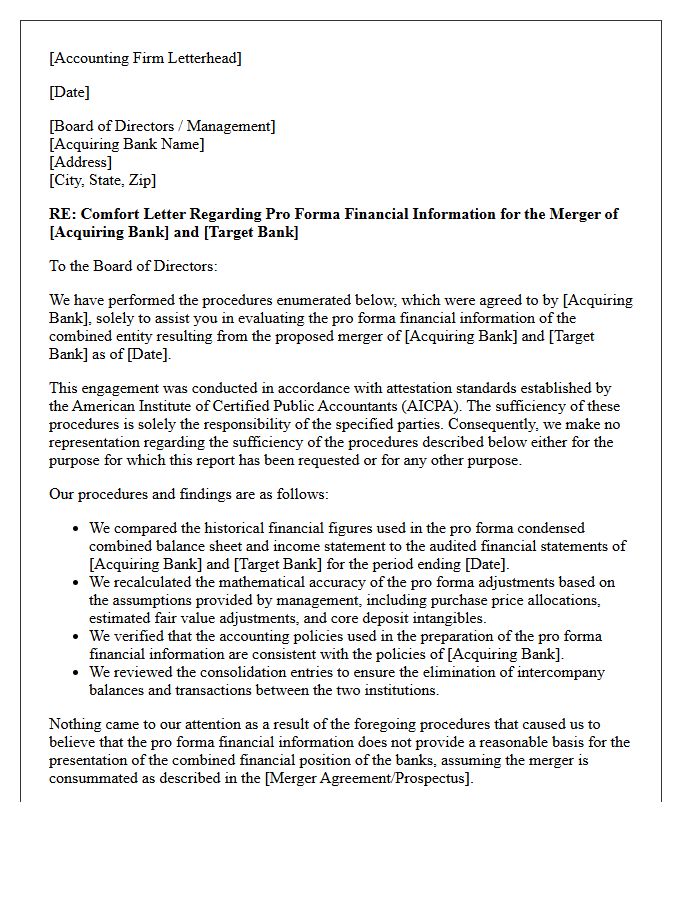

Pro Forma Financials Comfort Letter for Bank Mergers

A Pro Forma Financials Comfort Letter is a vital document issued by independent auditors during bank mergers to provide assurance on combined financial projections. It validates that pro forma adjustments comply with accounting standards, helping regulatory bodies and lenders assess the post-merger entity's stability. This letter confirms that the financial data reflects the transaction's impact accurately under Regulation S-X guidelines. For stakeholders, it serves as a critical due diligence tool to mitigate risks associated with capital adequacy and future earnings potential before finalizing the consolidation.

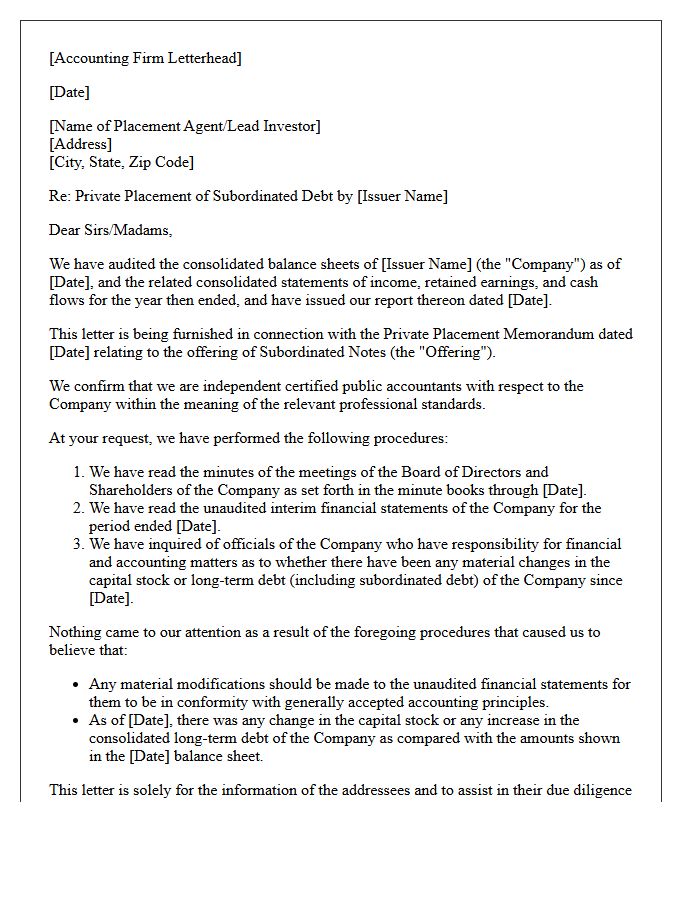

Subordinated Debt Private Placement Accountant Comfort Letter

A comfort letter is a critical document issued by an independent accountant during a subordinated debt private placement. It provides negative assurance to lenders and investors regarding the accuracy of financial data and subsequent changes not covered by audited statements. This letter mitigates due diligence risks by verifying that the issuer's financial information aligns with accounting standards. For private placements, it serves as a vital tool for establishing a "due diligence defense," ensuring all parties have verified the underlying fiscal health and debt structure before finalizing the investment agreement.

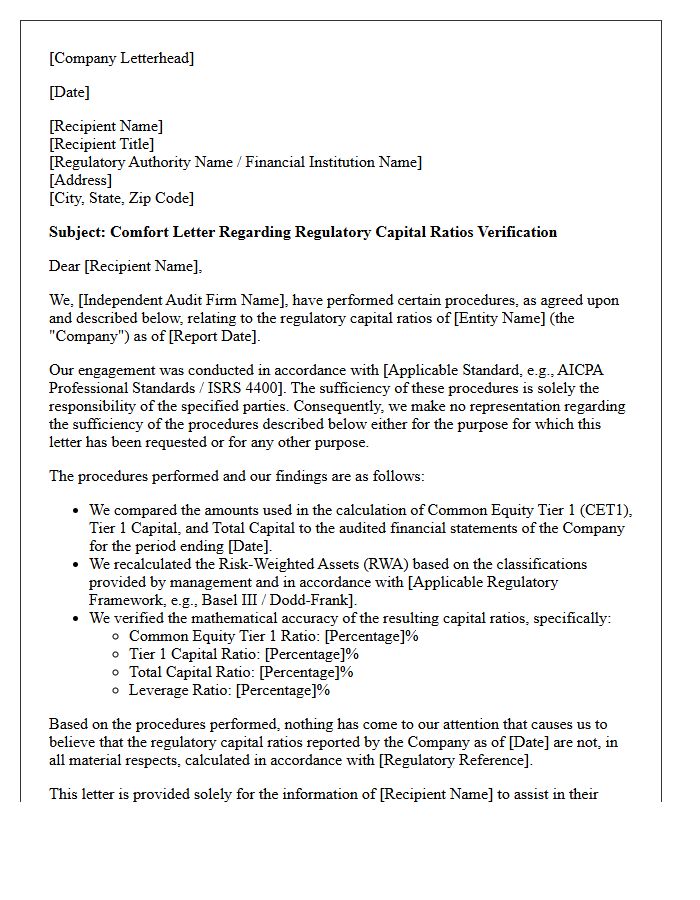

Regulatory Capital Ratios Verification Comfort Letter

A Regulatory Capital Ratios Verification Comfort Letter is a critical document issued by independent auditors to provide assurance on a financial institution's reported capital adequacy. It confirms that specific regulatory capital ratios, such as CET1 or Tier 1, are calculated in accordance with prevailing banking frameworks like Basel III. These letters are essential during securities offerings or debt issuances, offering third-party validation to investors and underwriters. By verifying mathematical accuracy and consistency with financial statements, the letter mitigates risk and ensures compliance with stringent transparency requirements set by financial regulators.

Asset Quality and Provisioning Accountant Letter

An Asset Quality and Provisioning Accountant Letter provides an independent professional assessment of a financial institution's loan portfolio health. It verifies that loan loss provisions accurately reflect potential credit risks and comply with accounting standards like IFRS 9 or CECL. This document ensures financial transparency by confirming that assets are valued correctly and that adequate capital is reserved for non-performing loans. Investors and regulators rely on this letter to evaluate the solvency and risk management effectiveness of the entity, ensuring the reported net asset value remains credible and reliable.

Draft Accountant Comfort Letter for Placement Agents

A Draft Accountant Comfort Letter is a critical document provided by auditors to placement agents during securities offerings. It offers negative assurance regarding the accuracy of financial statements and subsequent changes in financial position. By verifying that the data aligns with audited records, it helps placement agents establish a due diligence defense against potential liabilities. This letter bridges the gap between the last audit and the offering date, ensuring regulatory compliance and investor confidence in the issuer's financial disclosures before final execution.

Final Rule 144A Offering Comfort Letter for Banks

A Rule 144A Comfort Letter is a critical document issued by auditors to underwriters during private placements. It provides negative assurance regarding the accuracy of financial statements and subsequent changes in the issuer's financial position. For banks, this letter serves as a vital component of the due diligence defense under securities laws. By verifying that financial data in the offering circular aligns with audited records, it mitigates liability risks and ensures institutional investors receive reliable information before purchasing unregistered securities in the secondary market.

Net Interest Margin Financial Data Comfort Letter

A Net Interest Margin (NIM) comfort letter is a formal document issued by independent auditors to underwriters during a securities offering. It provides negative assurance regarding the accuracy of interest-related financial data not covered by audited statements. This process validates the yield on earning assets minus interest expenses, ensuring the financial disclosure remains consistent with accounting records. For issuers, it is a critical step in maintaining due diligence and investor confidence by verifying the profitability and interest spread metrics presented in the prospectus.

Tier One Capital Compliance Accountant Letter

A Tier One Capital Compliance Accountant Letter serves as formal verification of an individual's or entity's financial liquidity and net worth. Lenders and regulatory bodies require this document to confirm that the capital held meets specific solvency standards and is readily available as high-quality assets. Issued by a certified public accountant, the letter validates that the equity capital is sufficient to absorb potential losses, ensuring the investor possesses the fiscal capacity necessary for high-stakes transactions or regulatory licensing requirements without relying on external debt.

What is an accountant comfort letter in the context of private placements?

An accountant comfort letter is a document issued by an independent auditor to underwriters or placement agents during a private placement. It provides negative assurance that the financial statements have not materially changed since the last audit and that the financial data in the offering memorandum aligns with the company's accounting records.

Why do investors require a comfort letter for a private placement?

Investors and placement agents require a comfort letter to fulfill their "due diligence" obligations. It serves as professional verification that the financial information presented in the private placement memorandum (PPM) is accurate and has been reviewed by a qualified third party, thereby reducing the risk of material misstatements.

What specific procedures does an accountant perform for a comfort letter?

The accountant performs "agreed-upon procedures," which typically include comparing financial figures in the offering document to the general ledger, reviewing interim financial statements, and conducting inquiries with management regarding any significant financial changes since the most recent balance sheet date.

Does a comfort letter provide a guarantee of financial accuracy?

No, a comfort letter does not provide a guarantee or a high level of assurance like a full audit. It provides "negative assurance," stating that nothing came to the accountant's attention to indicate that the financial data is incorrect. It is intended for the internal use of the requesting parties and is not a legal opinion.

What is the difference between a standard audit report and a comfort letter?

A standard audit report provides a formal opinion on whether financial statements present a true and fair view, whereas a comfort letter is a non-public document focused on specific financial updates and verification of data points for a specific transaction. Comfort letters are governed by AICPA professional standards (AS 6101) specifically for securities offerings.

Comments