If your bank rejected your request to waive overdraft charges, understanding your rights is essential. A Denial of Insufficient Funds Fee Reversal Request often occurs due to account history or internal policies, but you can still appeal the decision effectively. Learn how to persist and negotiate better outcomes with financial institutions. Below are some ready to use templates.

Image cover: Declining a Fee Waiver: Templates and Best Practices for Insufficient Funds Requests

Letter Samples List

- Insufficient Funds Fee Reversal Denial Letter

- Letter of Denial for Non-Sufficient Funds Fee Waiver

- Account Fee Reversal Request Rejection Letter

- Letter Declining Insufficient Funds Charge Reversal

- Banking Fee Appeal Denial Letter

- Letter of Refusal for Overdraft Penalty Refund

- Standard NSF Fee Reversal Denial Letter

- Letter Regarding Denial of Account Penalty Reversal

- Unsuccessful Insufficient Funds Fee Waiver Letter

- Letter Denying Courtesy Refund of NSF Fee

- Final Decision Letter on Insufficient Funds Appeal

- Letter of Notification for Fee Reversal Rejection

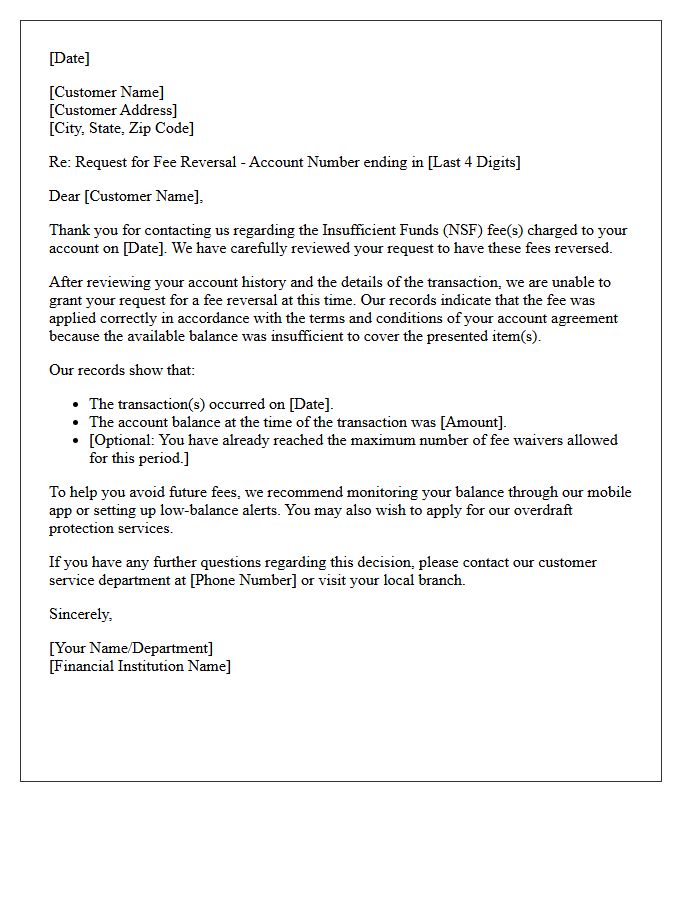

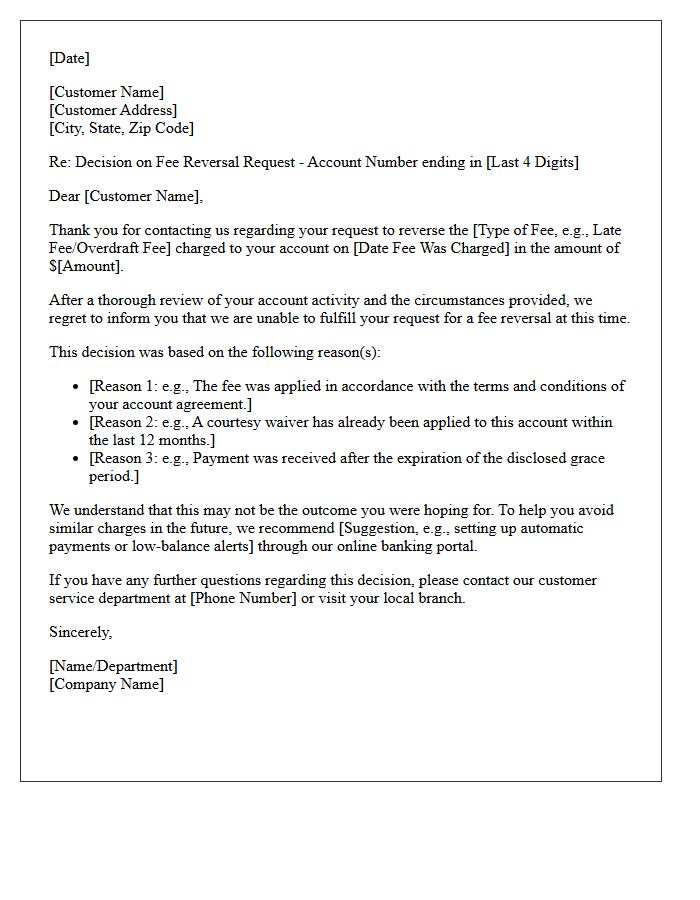

Insufficient Funds Fee Reversal Denial Letter

An Insufficient Funds Fee Reversal Denial Letter is a formal notice from a bank rejecting your request to waive overdraft charges. This document typically cites specific account policies, recurring patterns of overspending, or a previous history of granted waivers as reasons for the refusal. To contest a denial, review your account agreement for error-correction procedures and ensure your balance was accurately calculated at the time of the transaction. Understanding these banking regulations is essential for managing your financial health and preventing future penalties through effective balance monitoring.

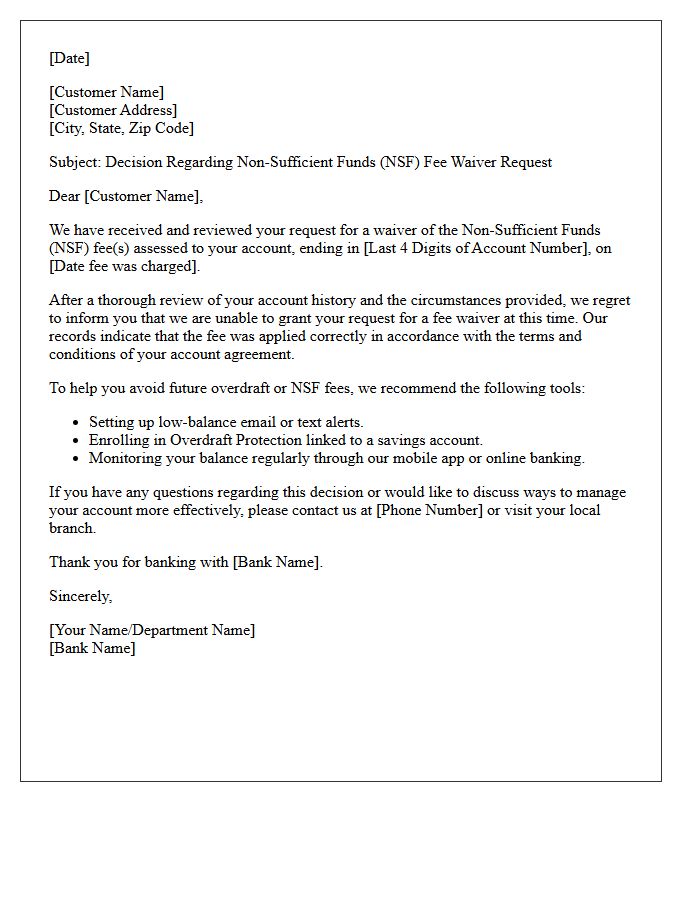

Letter of Denial for Non-Sufficient Funds Fee Waiver

A Letter of Denial for Non-Sufficient Funds Fee Waiver is a formal notification from a financial institution rejecting a customer's request to cancel overdraft charges. The document outlines specific reasons for the refusal, such as a history of frequent account deficits or exceeding the bank's annual waiver limit. Understanding these denial justifications is crucial for consumers seeking to improve their financial standing or appeal the decision. To prevent future penalties, account holders should monitor balances closely and consider linking a savings account for automatic overdraft protection.

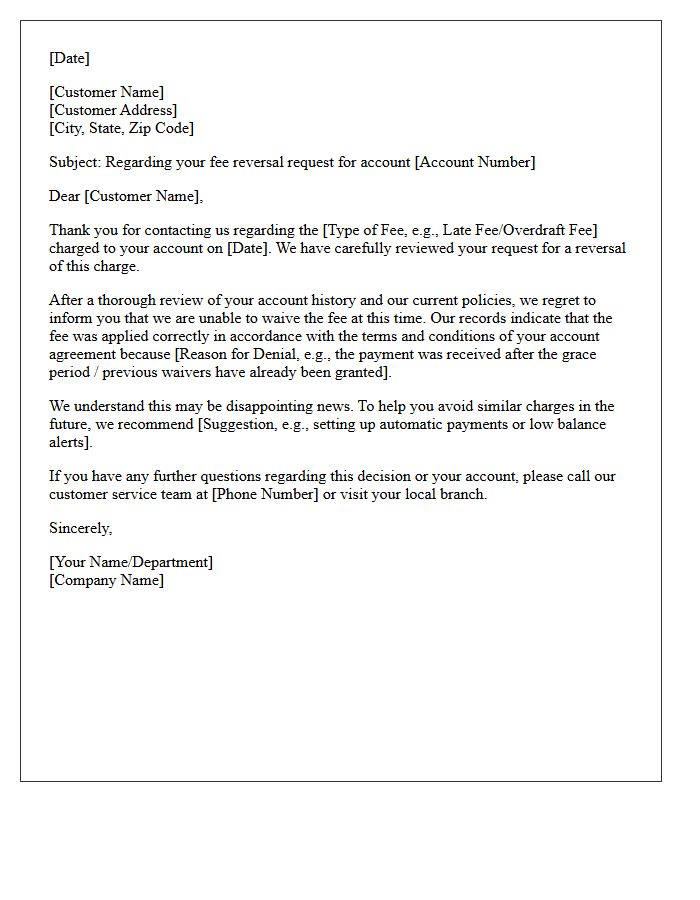

Account Fee Reversal Request Rejection Letter

An Account Fee Reversal Request Rejection Letter is a formal notice from a financial institution denying a customer's plea to waive specific charges. The document outlines the rationale for the decision, often citing account terms, previous courtesy waivers, or late submissions. Understanding the eligibility criteria is crucial, as banks typically require valid technical errors or extreme financial hardship to approve refunds. To contest a rejection, customers should provide supporting documentation or escalate the matter to a supervisor to demonstrate why the original fee application was unjust or incorrect based on their history.

Letter Declining Insufficient Funds Charge Reversal

When writing a letter declining an insufficient funds charge reversal, you must clearly state that the fee remains valid due to account terms. Briefly explain that the transaction exceeded the available balance and that prior courtesy waivers may limit further discretionary adjustments. Maintain a professional tone while highlighting the importance of overdraft protection or balance monitoring to prevent future occurrences. Ensuring the customer understands the contractual obligation helps maintain transparency and consistency in banking policies regarding non-sufficient funds (NSF) notifications.

Banking Fee Appeal Denial Letter

Receiving a banking fee appeal denial letter means the financial institution has formally rejected your request to waive a specific charge. This document typically cites specific account terms and conditions or historical patterns as the basis for the refusal. To contest this decision, review your monthly statements for errors and verify if the bank adhered to its own fee disclosure policies. If you believe the denial is unfair, you may escalate the issue to a formal grievance or contact a regulatory ombudsman for a secondary review of the transaction dispute.

Letter of Refusal for Overdraft Penalty Refund

A letter of refusal for an overdraft penalty refund is a formal document issued by a bank explaining why they will not reverse a service charge. To challenge this, you must review the Terms and Conditions to identify any potential breaches or errors in their assessment. Effective appeals often highlight financial hardship or demonstrate that the fees were disproportionate to the transaction. If the internal resolution fails, you should preserve all correspondence to escalate the dispute to the Financial Ombudsman for an independent review of the bank's decision.

Standard NSF Fee Reversal Denial Letter

A Standard NSF Fee Reversal Denial Letter is a formal notification from a financial institution rejecting a request to waive non-sufficient funds charges. Banks typically issue these denials when an account has a history of overdrafts or if the customer has already reached the maximum limit of courtesy refunds for the year. Understanding the specific reason for denial is crucial, as it may cite internal policies or repeated account mismanagement. To contest this, review your account agreement and provide evidence of bank errors or extreme financial hardship to support a potential appeal.

Letter Regarding Denial of Account Penalty Reversal

A Letter Regarding Denial of Account Penalty Reversal serves as a formal notification that your appeal was unsuccessful. This document outlines that the original disciplinary action remains final due to confirmed violations of the platform's terms of service. It is essential to review the specific evidence or policies cited to understand the permanent restrictions on your account. While receiving a rejection can be frustrating, these letters typically mark the conclusion of the internal review process, leaving legal counsel or external arbitration as the only remaining paths for dispute resolution.

Unsuccessful Insufficient Funds Fee Waiver Letter

When drafting an unsuccessful insufficient funds fee waiver letter, clarity and persistence are vital. Banks often deny initial requests, so you must emphasize your customer loyalty and any mitigating circumstances. Clearly state the specific transaction date and fee amount while requesting a one-time courtesy reversal. If the first attempt fails, ask for an escalation or provide documentation of financial hardship. Demonstrating a consistent history of positive balances increases your chances of success. Remember, a professional tone and a direct request for account reconciliation are the most effective strategies for recovery.

Letter Denying Courtesy Refund of NSF Fee

A letter denying a courtesy refund of an NSF fee formally notifies a customer that their request to waive a non-sufficient funds charge has been rejected. This decision is typically based on the account's transaction history or established banking policies. It is essential to understand that such waivers are discretionary, not mandatory. The notice serves as a final determination regarding the disputed charge, emphasizing the importance of maintaining a positive balance to avoid future penalties. Reviewing your account agreement can provide clarity on specific fee structures and waiver eligibility requirements.

Final Decision Letter on Insufficient Funds Appeal

The Final Decision Letter is the formal conclusion to your Insufficient Funds Appeal process. This document confirms whether the initial denial has been upheld or overturned after a secondary review. It is crucial to examine the reasoning provided, as this letter often marks the end of internal administrative options. If the appeal is denied, the letter will outline any remaining external rights, such as escalation to an ombudsman or legal action. Always verify the effective date and any specific instructions for fund recovery or account status adjustments.

Letter of Notification for Fee Reversal Rejection

A Letter of Notification for Fee Reversal Rejection is a formal document issued by a financial institution explaining why a requested refund was denied. This letter serves as a final decision regarding your dispute or claim. It typically outlines specific reasons, such as policy compliance, missed deadlines, or insufficient documentation. Understanding the stated grounds for denial is essential if you intend to initiate an appeals process or provide additional evidence to support your case. Always review the provided explanation to ensure your future transactions align with the institution's established terms and conditions.

Why was my request for an insufficient funds fee reversal denied?

Reversal requests are typically denied if the account has exceeded the maximum number of courtesy waivers allowed within a rolling 12-month period or if the account has a history of frequent overdrafts.

Can I appeal the decision if my fee waiver request was rejected?

Yes, you may request a secondary review by providing documentation of an administrative error or proof of an unexpected emergency, such as a delayed direct deposit or a verified bank technical glitch.

Does a denied fee reversal affect my credit score?

No, the denial of an internal bank fee reversal does not directly impact your credit score; however, leaving the account with a negative balance for an extended period may lead to collections reporting.

How many times can I request a reversal for insufficient funds fees?

While policies vary by institution, most banks limit fee waivers to one or two per calendar year, depending on your account standing and total years of membership.

What can I do to avoid future insufficient funds fees?

To prevent future fees, you can enroll in overdraft protection linked to a savings account, set up low-balance mobile alerts, or opt-out of overdraft coverage for point-of-sale debit transactions.

Comments