Drafting a professional Response to Request for Interest Rate Reduction is essential for maintaining client relationships while protecting financial margins. This guide outlines how to evaluate borrower creditworthiness, negotiate terms, and communicate decisions clearly and effectively. Whether approving or declining a rate adjustment, using structured language ensures compliance and professionalism. Below are some ready to use templates.

Image cover: Mastering Your Rate Reduction Request: Expert Templates and Response Guide

Letter Samples List

- Letter of Approval for Mortgage Interest Rate Reduction

- Letter of Denial for Credit Card Interest Rate Reduction Request

- Conditional Approval Letter for Personal Loan Interest Rate Reduction

- Letter Requesting Additional Documentation for Interest Rate Reduction

- Counter-Offer Letter for Business Loan Interest Rate Reduction

- Letter of Agreement for Temporary Interest Rate Reduction

- Final Decision Letter Regarding Auto Loan Interest Rate Reduction

- Policy Explanation Letter for Interest Rate Reduction Requests

- Letter Providing Alternative Repayment Options in Lieu of Rate Reduction

- Letter of Adjustment for Variable Loan Interest Rate Reduction

- Notice Letter of Interest Rate Reduction Denial Due to Credit Score

- Letter of Confirmation for Account Interest Rate Reduction

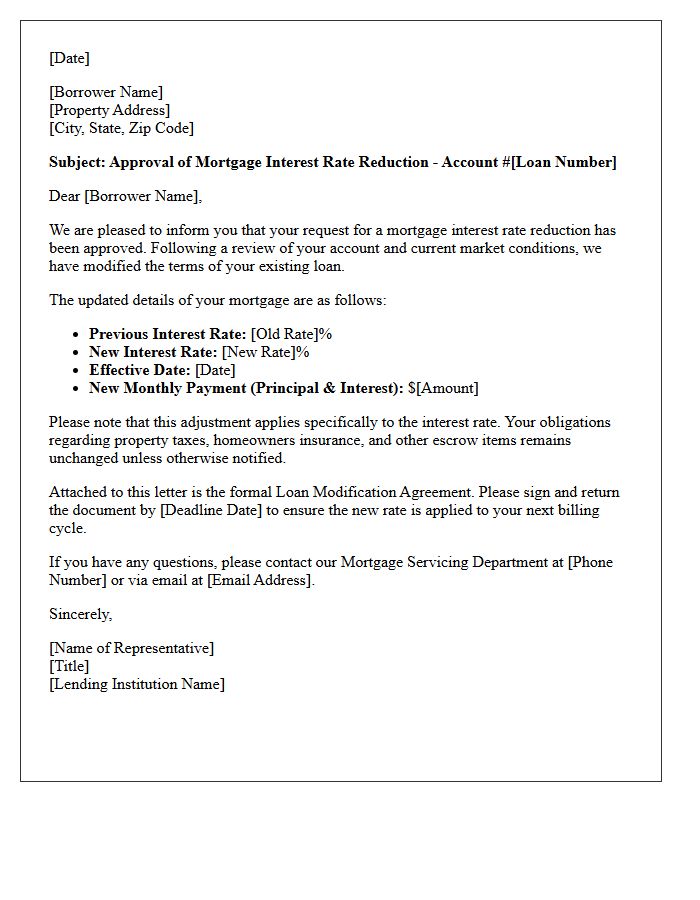

Letter of Approval for Mortgage Interest Rate Reduction

A Letter of Approval for a Mortgage Interest Rate Reduction serves as formal confirmation from your lender that they have agreed to lower your annual percentage rate. This document outlines your new monthly payments and the specific date the change takes effect. It is crucial to verify that all terms and conditions align with your negotiation. Keeping this official approval in your records ensures protection against future billing discrepancies while improving your long-term financial stability through reduced borrowing costs.

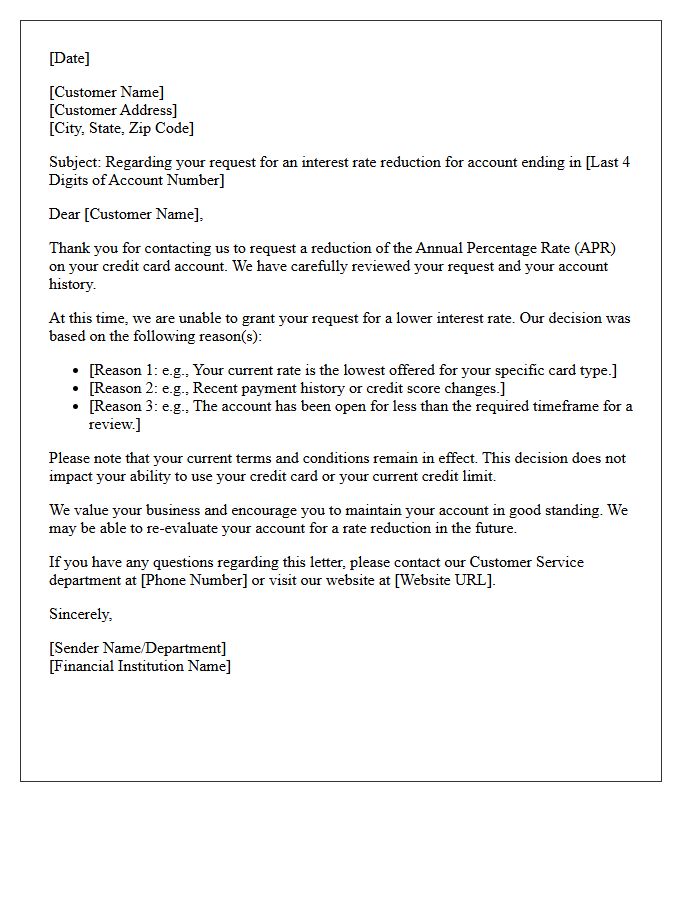

Letter of Denial for Credit Card Interest Rate Reduction Request

Receiving a Letter of Denial for a credit card interest rate reduction means the issuer declined your request to lower the APR. Common reasons include a low credit score, recent missed payments, or high debt-to-income ratios. This document is important because it often details the specific factors influencing the decision and lists the credit reporting agency used for the assessment. Reviewing these details helps you identify financial areas needing improvement. You can reapply after enhancing your creditworthiness by maintaining consistent, on-time payments and reducing outstanding balances over time.

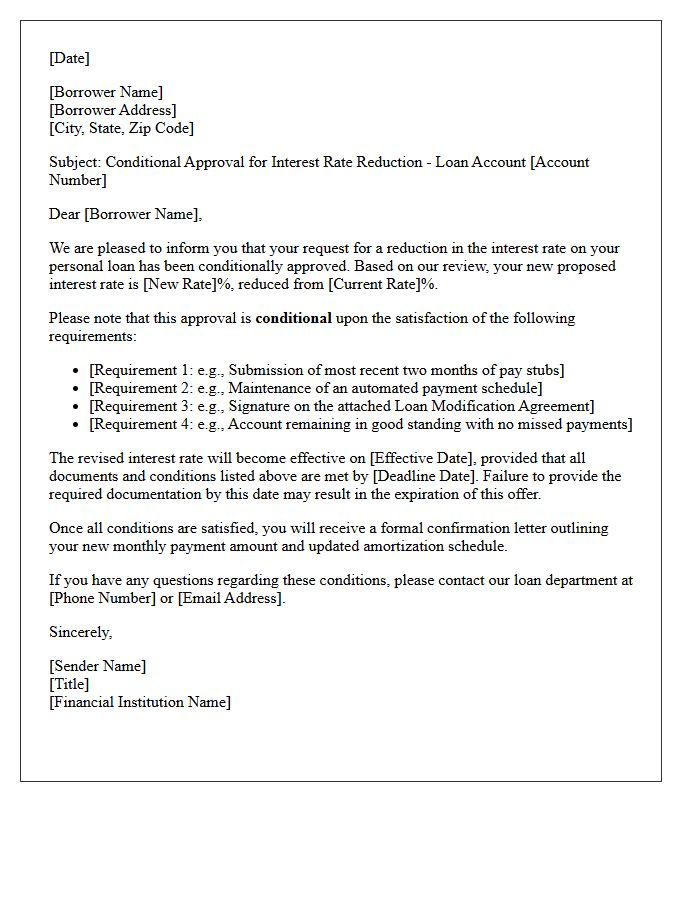

Conditional Approval Letter for Personal Loan Interest Rate Reduction

A Conditional Approval Letter signifies that a lender has pre-approved your personal loan request, often featuring a reduced interest rate based on your preliminary credit profile. To secure this lower rate, you must satisfy specific underwriting requirements, such as verifying income, employment, and debt obligations. This document is not a final guarantee; any discrepancies found during the verification process can lead to a denial or a rate adjustment. Always review the expiration date and listed stipulations to ensure you lock in the offered savings before the letter expires.

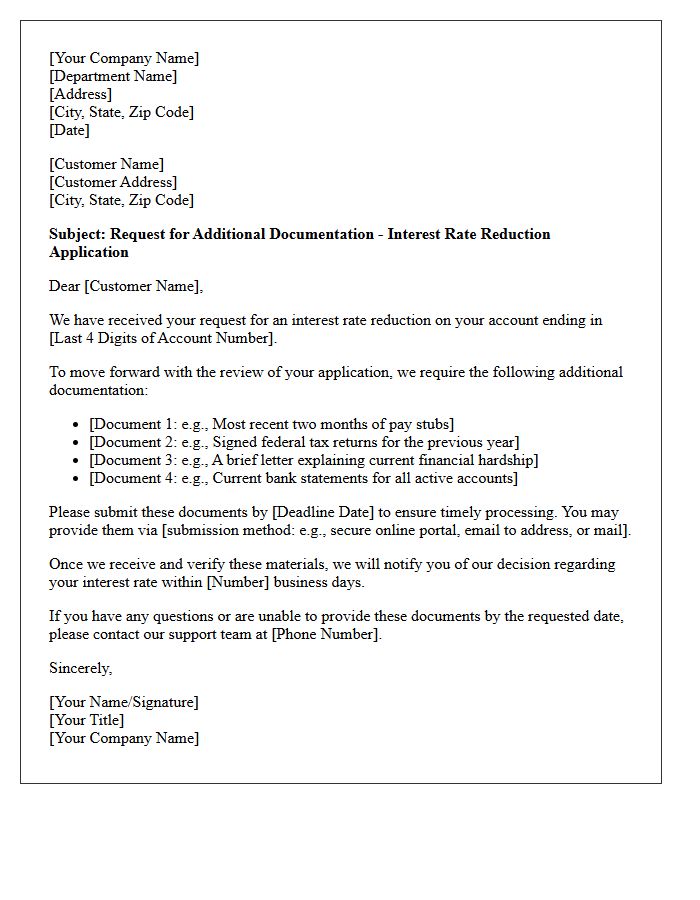

Letter Requesting Additional Documentation for Interest Rate Reduction

When drafting a letter requesting additional documentation for an interest rate reduction, clarity is essential. You must formally respond to the lender's inquiry by providing specific financial evidence, such as updated income statements, tax returns, or credit reports. Accurately submitting these supplementary records ensures the underwriting process continues without delays. Clearly reference your loan account number and list all enclosed supporting documents to demonstrate transparency. This professional communication is a vital step in securing a lower rate and improving your long-term financial stability through successful loan modification.

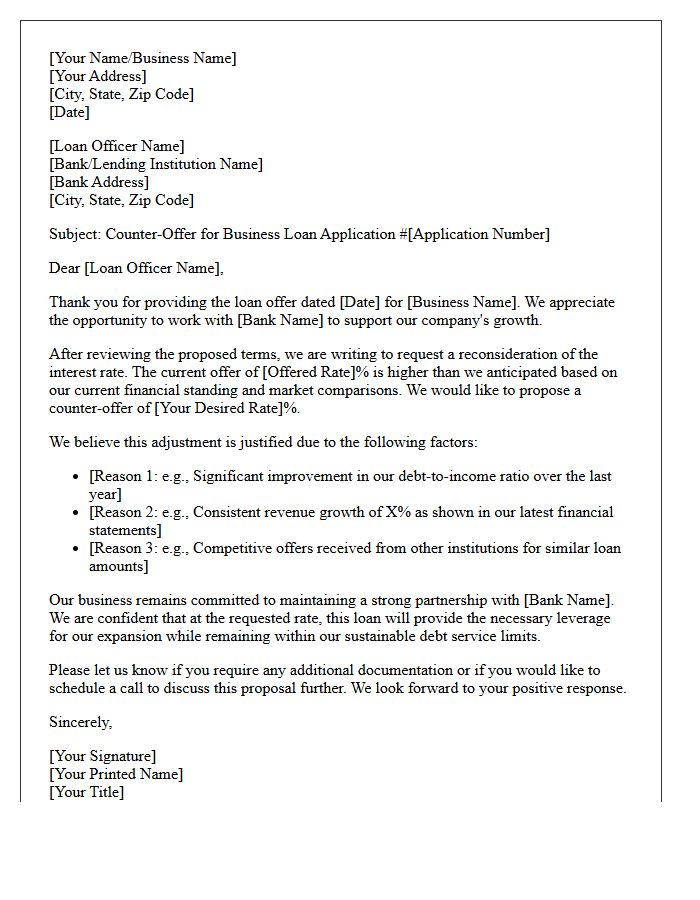

Counter-Offer Letter for Business Loan Interest Rate Reduction

A counter-offer letter is a strategic negotiation tool used to request a lower interest rate on a business loan. It should clearly outline your business's financial stability, improved credit score, or competitive offers from other lenders to justify the reduction. By presenting a data-driven argument, you demonstrate creditworthiness and professional leverage. Ensure the tone remains formal and includes a specific target rate to initiate a meaningful dialogue. Successfully negotiating these terms can significantly decrease your debt service costs and improve long-term cash flow for your company.

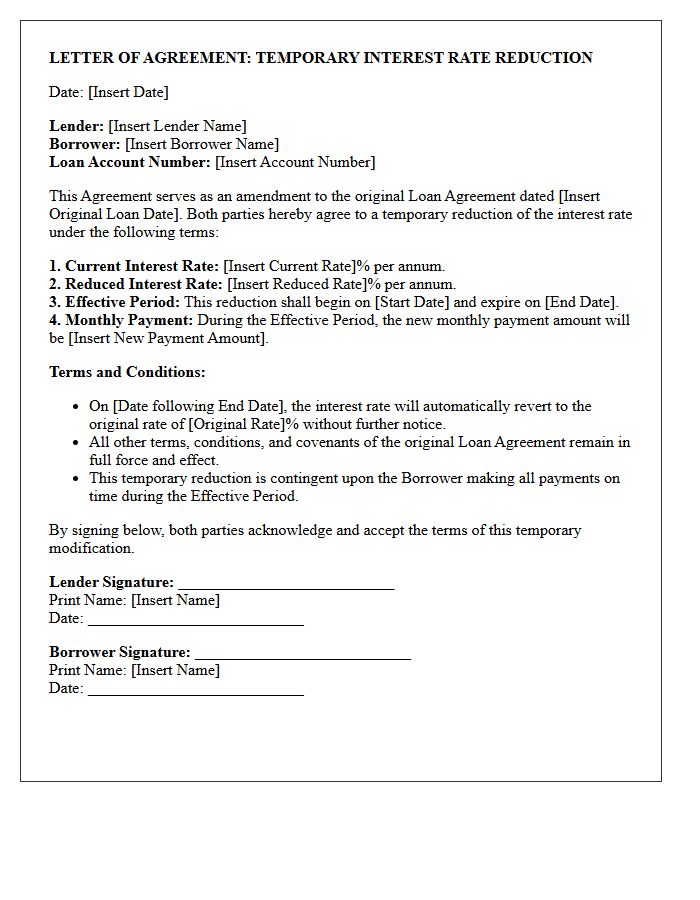

Letter of Agreement for Temporary Interest Rate Reduction

A Letter of Agreement for Temporary Interest Rate Reduction is a formal contract between a borrower and lender to lower monthly mortgage payments for a set period. This document outlines the temporary buydown terms, specifying how long the lower rate lasts and who funds the subsidy. It is essential for ensuring all parties understand the transition back to the original note rate. This arrangement provides immediate affordability, allowing homeowners to manage cash flow effectively during the initial years of their loan term while maintaining long-term financing stability.

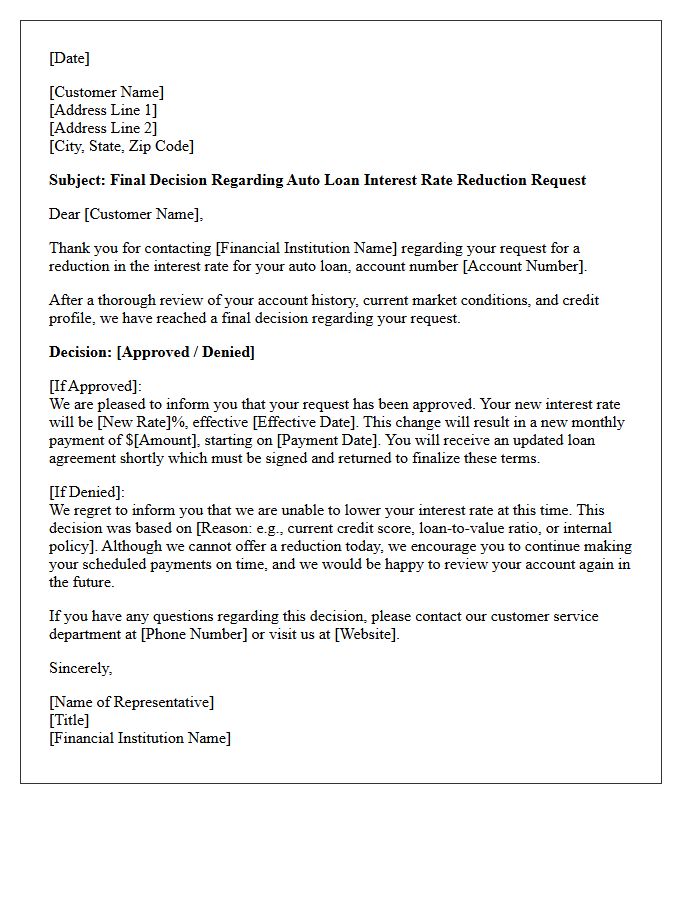

Final Decision Letter Regarding Auto Loan Interest Rate Reduction

A Final Decision Letter confirms the outcome of your request for an auto loan interest rate reduction. This formal notice specifies whether your APR has been lowered based on creditworthiness, payment history, or market conditions. If approved, it outlines your new monthly payments and updated amortization schedule. If denied, the letter must provide a specific reason for the refusal, such as a low credit score. Always review these documents immediately to ensure your lender has applied the correct terms to your account to save on long-term financing costs.

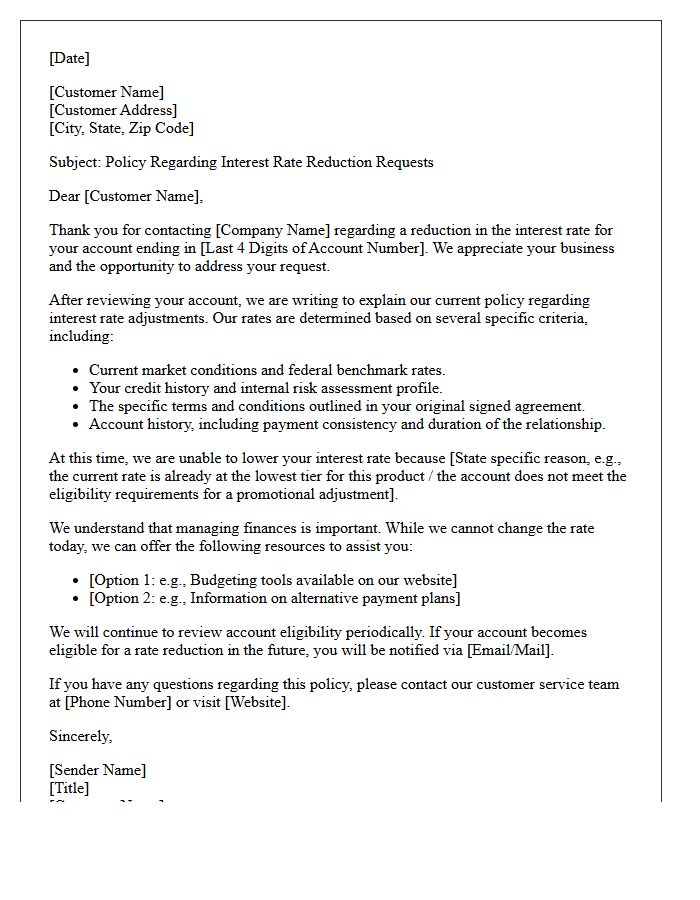

Policy Explanation Letter for Interest Rate Reduction Requests

A Policy Explanation Letter outlines the specific eligibility criteria and internal guidelines a lender follows when reviewing interest rate reduction requests. This document ensures transparency by detailing why a request was approved or denied based on financial risk, market conditions, or payment history. It serves as a formal justification for the decision, helping borrowers understand the compliance standards and regulatory policies involved. Providing this explanation is crucial for maintaining professional communication and ensuring all parties understand the contractual obligations and adjustments applied to the loan agreement.

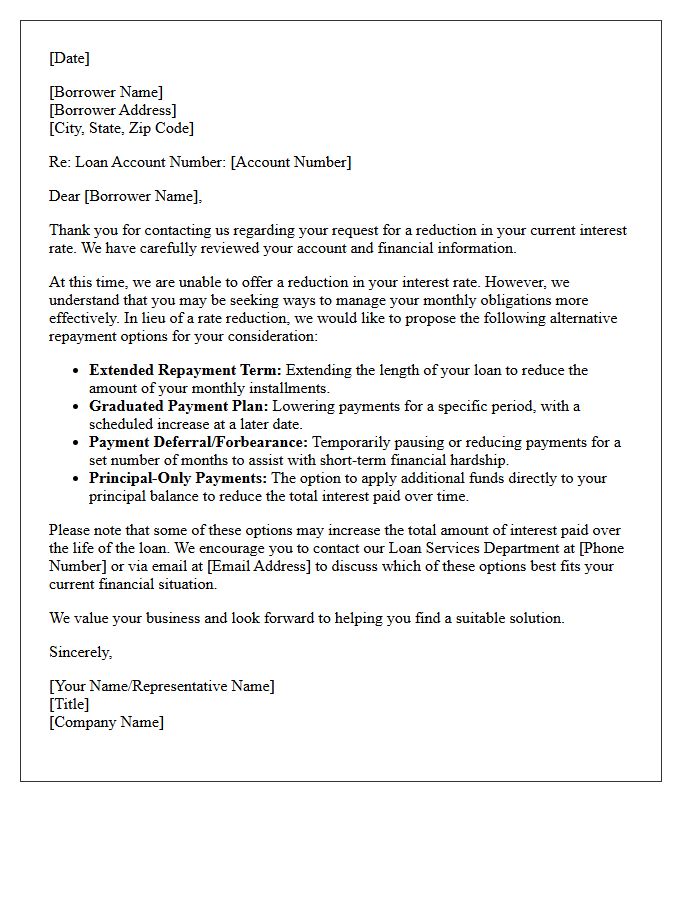

Letter Providing Alternative Repayment Options in Lieu of Rate Reduction

A letter providing alternative repayment options is an essential communication from lenders when a formal interest rate reduction is unavailable. It outlines flexible solutions such as extended loan terms, temporary payment deferrals, or graduated repayment plans to help borrowers manage debt effectively. Understanding these restructuring choices is crucial for maintaining financial stability and preventing default. This document serves as a formal notification of the loss mitigation strategies available to the borrower, ensuring they remain informed about manageable ways to fulfill their financial obligations without a permanent change to the base interest rate.

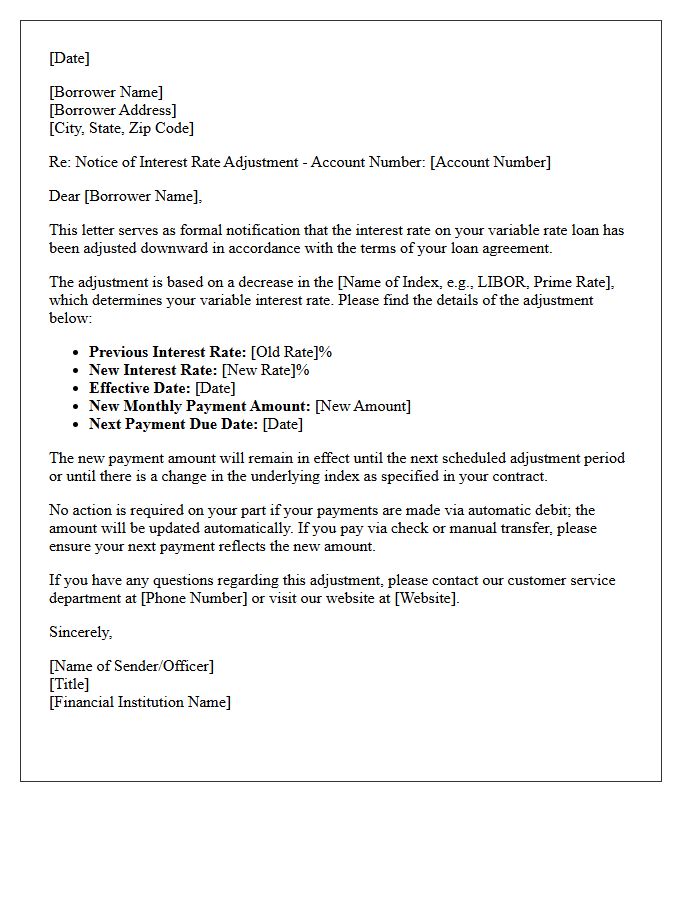

Letter of Adjustment for Variable Loan Interest Rate Reduction

A Letter of Adjustment serves as formal notification that your financial institution has approved a variable loan interest rate reduction. This document confirms the new, lower rate and specifies the effective date for your updated payment schedule. It is essential for verifying that your monthly obligations have decreased in alignment with current market trends or specific negotiations. Borrowers should retain this record to ensure billing accuracy and to monitor long-term savings on total interest costs over the remaining life of the loan.

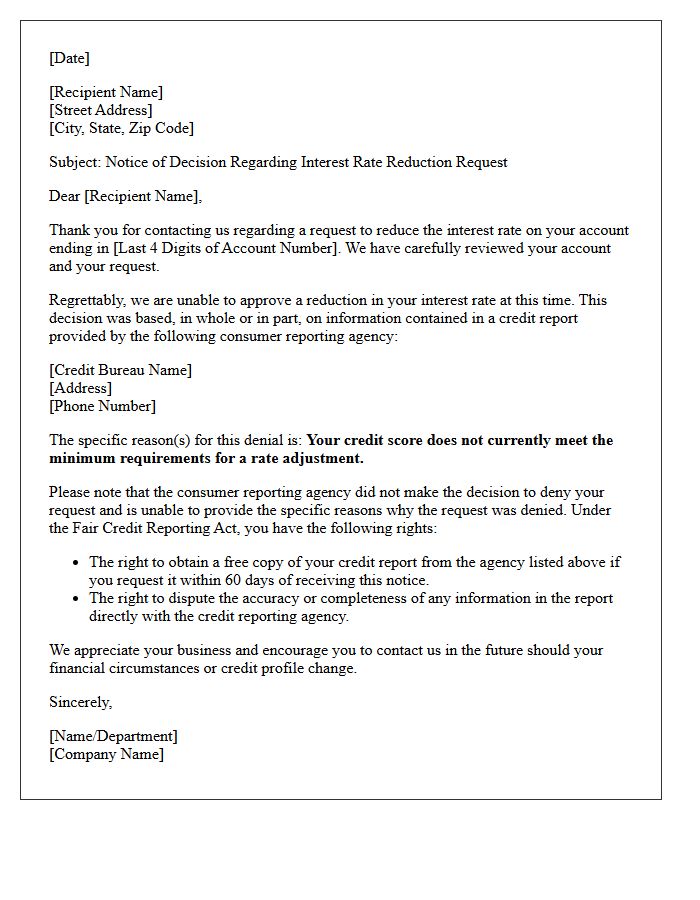

Notice Letter of Interest Rate Reduction Denial Due to Credit Score

A Notice of Interest Rate Reduction Denial occurs when a lender rejects your request for a lower APR based on your credit score. This adverse action notice must legally disclose the specific reasons for the decision and the credit reporting agency used. Factors like high credit utilization or late payments often trigger these denials. Reviewing this document is essential for identifying financial inaccuracies and understanding how to improve your creditworthiness to qualify for future rate reductions and lower borrowing costs.

Letter of Confirmation for Account Interest Rate Reduction

A Letter of Confirmation for Account Interest Rate Reduction serves as formal documentation that a financial institution has lowered your annual percentage rate. This written notice is essential for verifying new payment terms and ensuring accurate debt management. It typically outlines the specific effective date, the new interest percentage, and whether the change is permanent or a temporary promotional offer. Retaining this record is crucial for financial transparency and provides legal protection should any billing discrepancies arise regarding your adjusted repayment schedule.

How can I request a lower interest rate on my existing loan?

You can request an interest rate reduction by contacting your lender's customer service department to discuss a loan modification. It is helpful to provide evidence of improved credit scores, a consistent payment history, or competitive offers you have received from other financial institutions.

What factors do lenders consider when reviewing a rate reduction request?

Lenders typically evaluate your current creditworthiness, your history of on-time payments, the remaining balance of the loan, and prevailing market conditions. They may also consider your overall relationship with the bank, such as having other active accounts or investments.

Will requesting an interest rate reduction affect my credit score?

Simply asking for a lower rate or a "soft" inquiry for a modification does not usually impact your credit score. However, if the lender requires a formal re-application process involving a "hard" credit pull to verify your eligibility, you may see a temporary minor dip in your score.

What should I do if my request for an interest rate reduction is denied?

If your request is denied, ask the lender for the specific reasons behind the decision. You can then work on improving those areas, such as paying down other debts or increasing your credit score, before reapplying. Alternatively, you may consider refinancing with a different lender to secure a better rate.

How long does it take to receive a response to a rate reduction request?

The processing time for a response to a request for interest rate reduction typically ranges from 5 to 10 business days. This allows the lender to review your account details, evaluate your payment history, and determine if a lower rate can be approved under their current internal policies.

Comments