An escrow shortage occurs when your property taxes or insurance premiums increase beyond the funds collected. If your annual analysis reveals a deficit, your mortgage servicer will issue a notification detailing required payment adjustments to cover the balance. Understanding these changes helps you manage your monthly budget effectively. To simplify your communication, below are some ready to use templates.

Image cover: Managing Your Escrow Shortage: Official Notification Templates and Samples

Letter Samples List

- Standard Escrow Shortage Adjustment Notification Letter

- Annual Escrow Account Shortage Adjustment Letter

- Mortgage Escrow Shortage Payment Option Letter

- Banking Escrow Deficiency and Shortage Notice Letter

- Escrow Shortage Adjustment Lump Sum Payment Letter

- Escrow Account Shortage Monthly Installment Adjustment Letter

- Revised Escrow Shortage Adjustment Disclosure Letter

- Escrow Analysis Shortage Adjustment Informational Letter

- Final Notice Escrow Shortage Adjustment Letter

- Escrow Shortage Adjustment Account Review Letter

- Automated Escrow Shortage Adjustment Banking Letter

- Supplemental Escrow Shortage Adjustment Letter

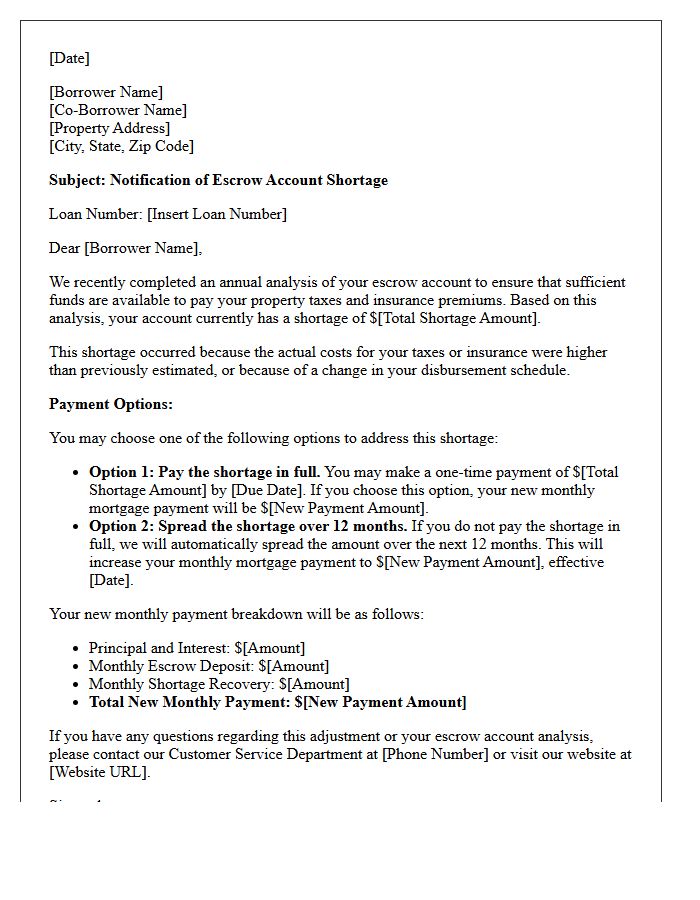

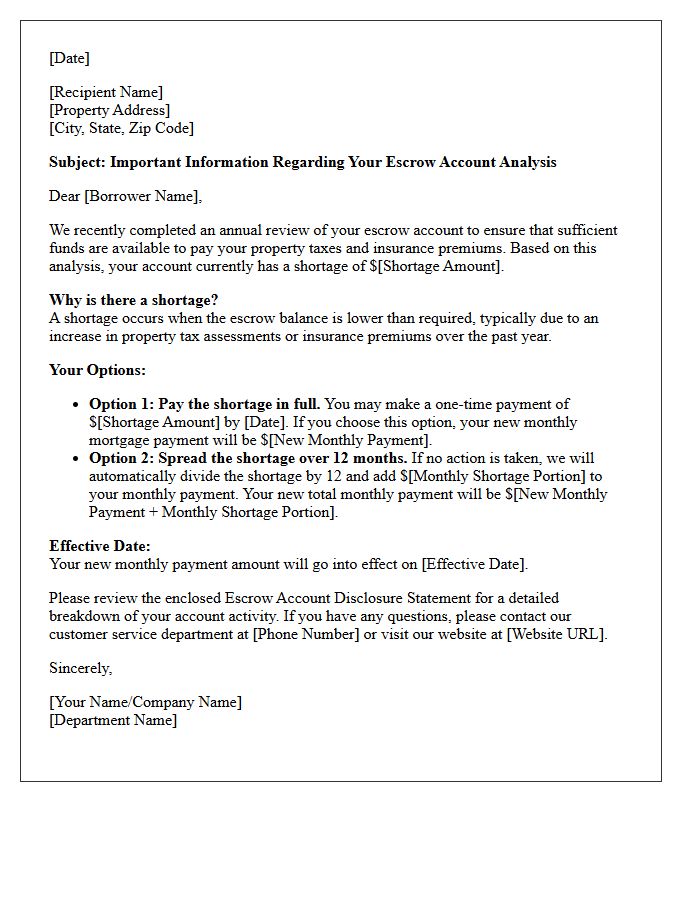

Standard Escrow Shortage Adjustment Notification Letter

A Standard Escrow Shortage Adjustment Notification Letter informs homeowners of a deficit in their impound account. This occurs when property taxes or insurance premiums increase beyond initial estimates. The notice outlines payment options, typically allowing for a one-time lump sum or spreading the balance over twelve months through an increased monthly mortgage statement. It is a critical document for financial planning, ensuring the lender maintains sufficient funds to cover legally required property obligations while preventing future account deficiencies and potential payment shocks.

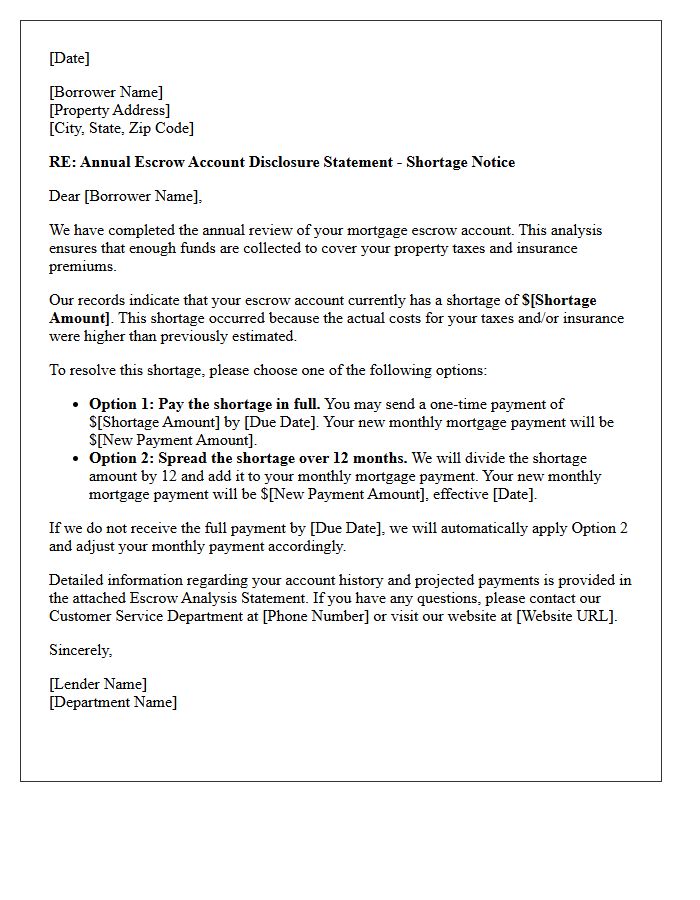

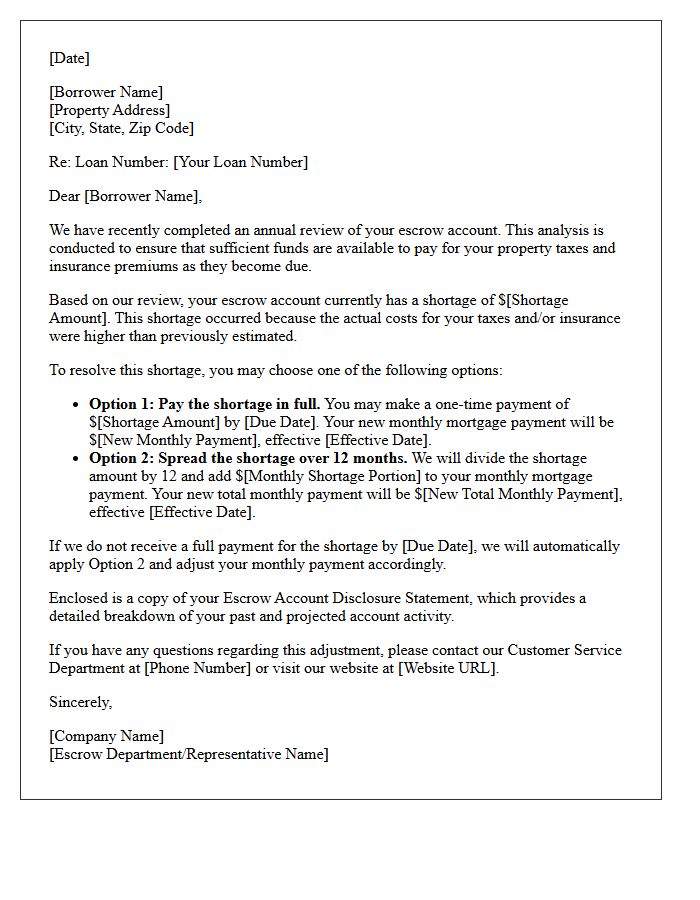

Annual Escrow Account Shortage Adjustment Letter

An Annual Escrow Account Shortage Adjustment Letter notifies homeowners when their property taxes or insurance premiums increase beyond previous estimates. This document outlines the deficiency in your escrow balance and details how your monthly mortgage payment will rise to cover the gap. You typically have the option to pay the shortage in a single lump sum or spread the cost over the next year. Reviewing this statement is essential for maintaining accurate financial planning and ensuring your housing expenses remain fully funded through your lender.

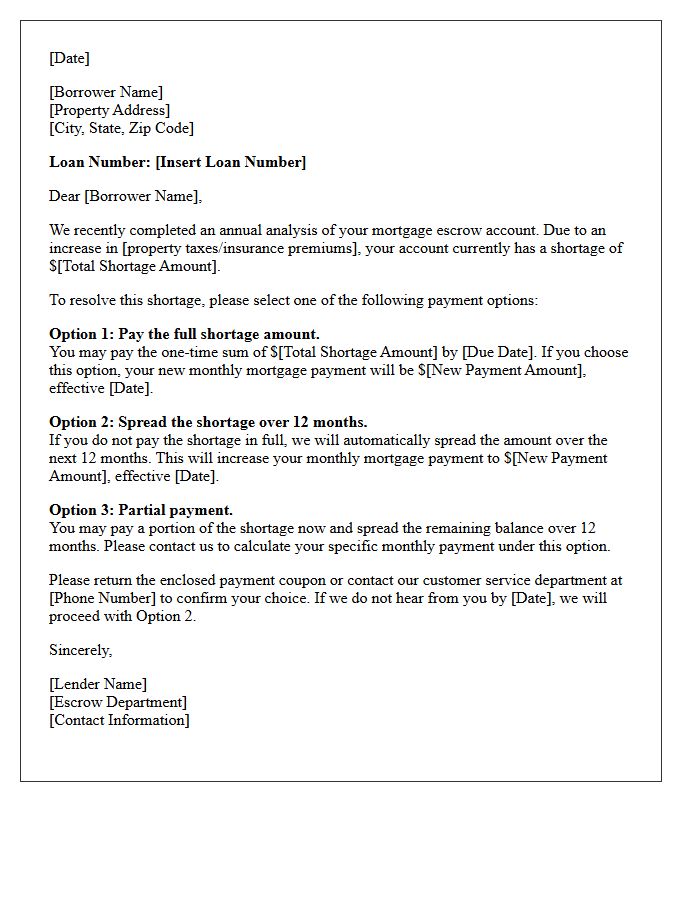

Mortgage Escrow Shortage Payment Option Letter

A mortgage escrow shortage payment option letter informs homeowners of a deficit in their escrow account due to increased taxes or insurance premiums. To resolve this, you typically have two repayment choices: pay the full shortage upfront in a lump sum or spread the balance over the next twelve months through higher monthly mortgage payments. Carefully review the escrow analysis provided to ensure accuracy. Selecting the lump sum option helps maintain a lower monthly payment, while the installment plan preserves your immediate cash flow but increases your recurring debt obligation.

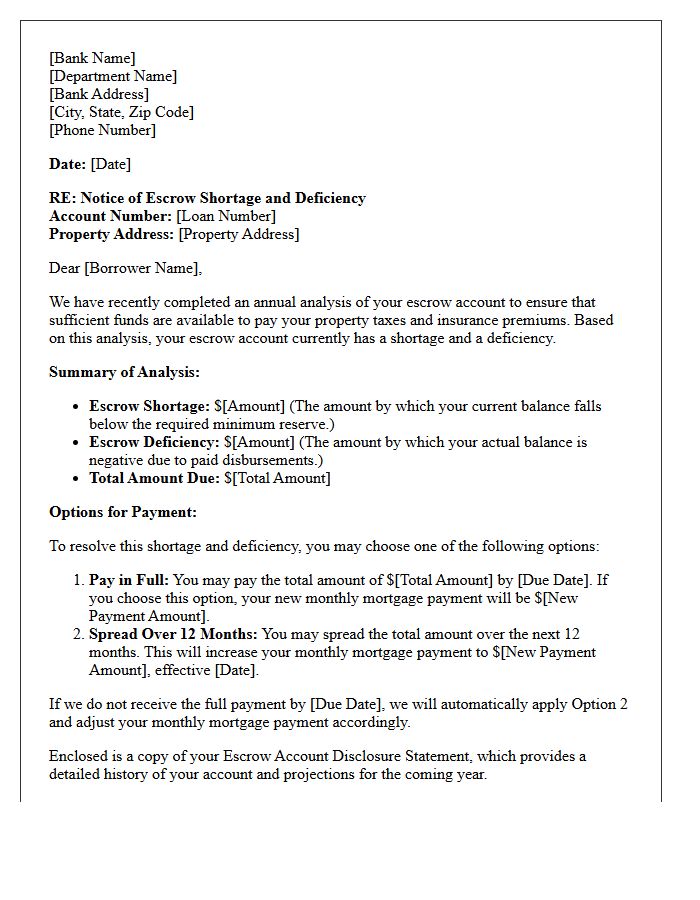

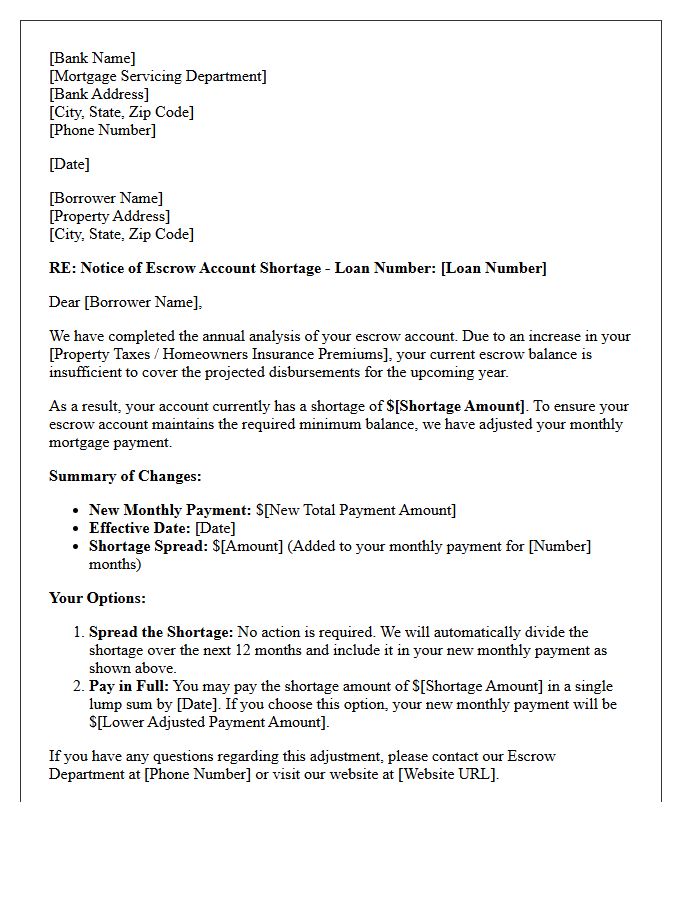

Banking Escrow Deficiency and Shortage Notice Letter

A banking escrow analysis identifies a deficiency when your account balance falls below the required minimum reserve, or a shortage when funds are insufficient to cover upcoming property taxes and insurance premiums. Receiving a notice letter means your monthly mortgage payment will likely increase to recover these costs. To manage this, you can typically pay the entire shortage as a one-time lump sum to keep your principal and interest payment stable, or spread the balance across your next twelve monthly installments. Monitoring your escrow statement helps avoid unexpected financial strain.

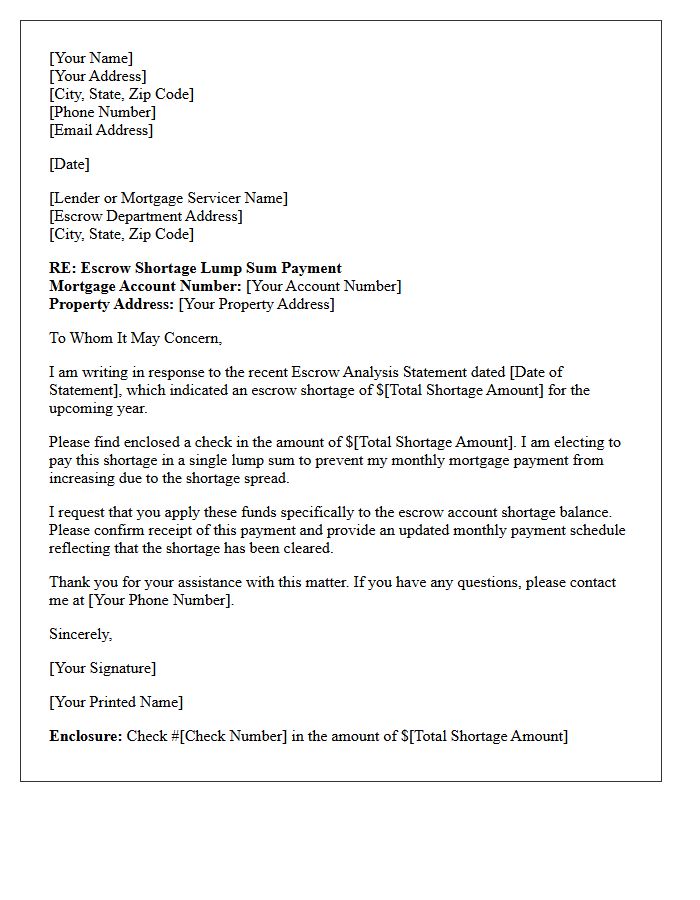

Escrow Shortage Adjustment Lump Sum Payment Letter

An Escrow Shortage Adjustment Lump Sum Payment Letter notifies homeowners that their property taxes or insurance premiums exceeded the funds available in their escrow account. To rectify this deficit, the lender provides an option to pay the shortage balance in a single installment. Choosing this immediate payment prevents a significant increase in future monthly mortgage payments. Failing to address the deficiency will result in the lender automatically spreading the cost over the next year, which raises your recurring costs to replenish the account and cover future escrow requirements.

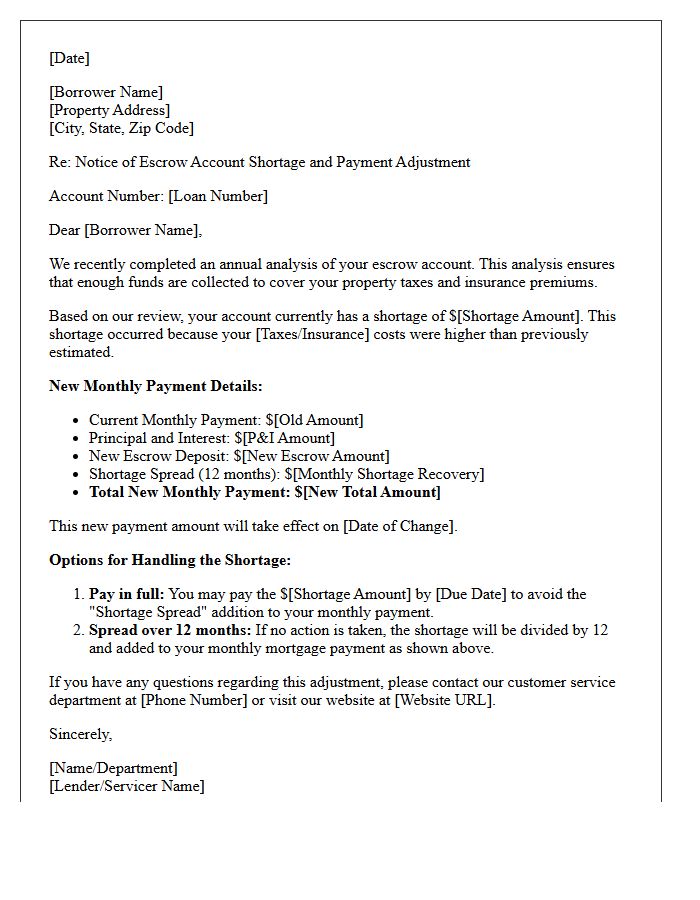

Escrow Account Shortage Monthly Installment Adjustment Letter

An escrow account shortage letter notifies homeowners that their property taxes or insurance premiums exceeded previous estimates. To resolve this deficit and maintain a required cushion, your lender will implement a monthly installment adjustment, increasing your total mortgage payment. You typically have two options: pay the full shortage upfront to keep payments stable or spread the balance over the next year. Reviewing this notice immediately is essential to understand your new payment obligations and ensure your loan remains in good standing through the upcoming fiscal cycle.

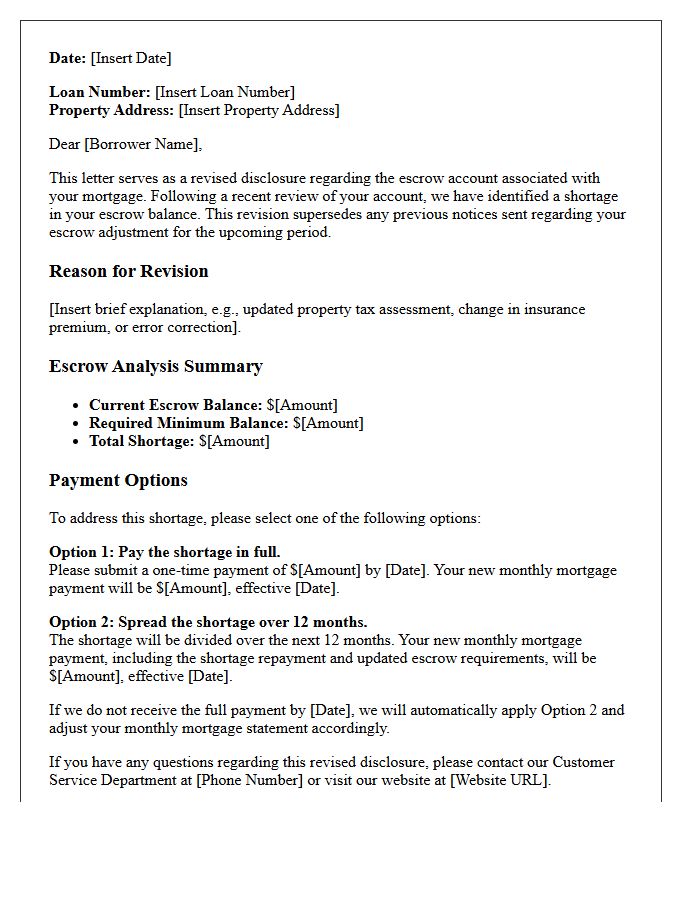

Revised Escrow Shortage Adjustment Disclosure Letter

The Revised Escrow Shortage Adjustment Disclosure Letter is a formal notice sent when your mortgage escrow account lacks sufficient funds to cover taxes and insurance. This critical update recalculates your monthly payment to bridge the deficit and maintain a required safety cushion. Homeowners should review the document to understand whether they prefer a one-time lump sum payment or a gradual monthly increase. Timely review ensures you stay compliant with federal RESPA guidelines and avoid unexpected payment spikes during the upcoming fiscal year.

Escrow Analysis Shortage Adjustment Informational Letter

An Escrow Analysis Shortage Adjustment Informational Letter notifies homeowners when their escrow account balance falls below the required minimum due to increased property taxes or insurance premiums. This document explains the shortage amount and outlines options to resolve it, such as a one-time payment or increased monthly mortgage installments. Reviewing this letter is essential to understand changes in your housing costs and ensure your lender can continue paying third-party obligations on your behalf without risking a negative account balance.

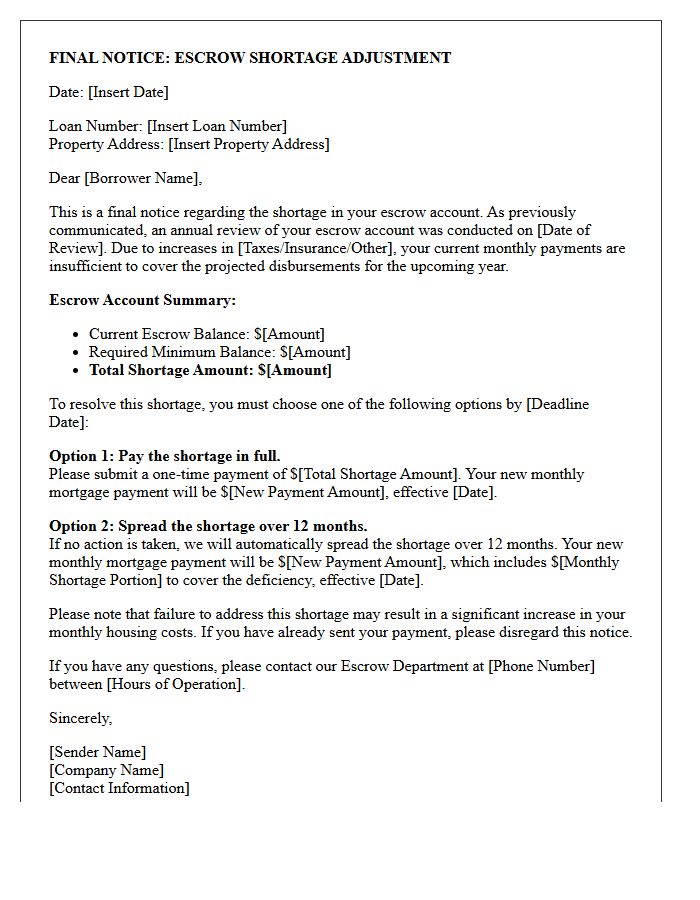

Final Notice Escrow Shortage Adjustment Letter

A Final Notice Escrow Shortage Adjustment Letter is a critical communication from your mortgage servicer indicating that your escrow account balance is insufficient to cover projected property taxes and insurance premiums. This document outlines the escrow deficiency and provides options to rectify the balance, such as a one-time payment or increased monthly installments. It is essential to review the Escrow Analysis statement included to understand how changes in tax assessments or insurance rates affected your mortgage payment and to ensure your account remains in good standing.

Escrow Shortage Adjustment Account Review Letter

An Escrow Shortage Adjustment Account Review Letter notifies you that your mortgage escrow account has insufficient funds to cover rising property taxes or insurance premiums. This mandatory annual analysis calculates the deficit between your current balance and projected expenses. To resolve a shortage, lenders typically offer two options: making a one-time lump sum payment to cover the gap or increasing your monthly mortgage payment over the next year. Reviewing this letter promptly is essential to understand how your housing costs will change and to ensure your escrow account remains balanced.

Automated Escrow Shortage Adjustment Banking Letter

An Automated Escrow Shortage Adjustment banking letter notifies homeowners of a deficiency in their impound account, typically caused by rising property taxes or insurance premiums. This document outlines the required payment increase to maintain a positive balance. Borrowers can usually resolve the gap through a one-time lump sum payment or by spreading the cost across monthly mortgage installments. Reviewing this notice promptly is essential to understand changes in your total monthly mortgage obligation and ensure continuous coverage for critical home-related expenses without unexpected financial strain.

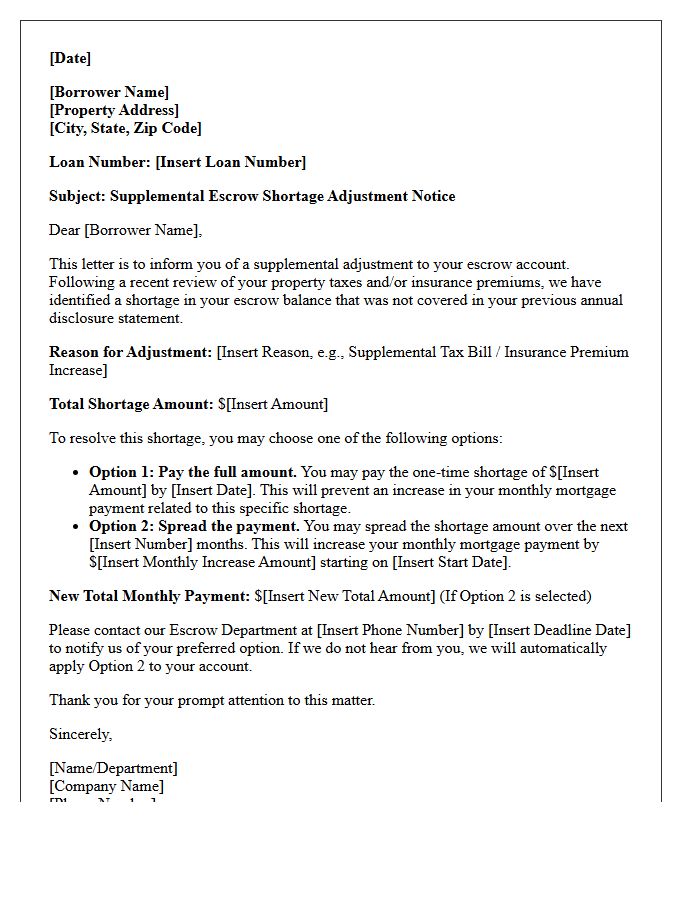

Supplemental Escrow Shortage Adjustment Letter

A Supplemental Escrow Shortage Adjustment Letter notifies homeowners of a funding deficiency in their impound account. This occurs when property taxes or insurance premiums increase beyond initial estimates. To maintain a minimum required balance, your mortgage servicer will adjust your monthly payment or request a one-time payment to cover the gap. Reviewing this document is essential to understand changes in your mortgage obligations and to ensure your escrow account remains compliant with federal guidelines, preventing unexpected financial strain during the next disbursement cycle.

What is an escrow shortage adjustment notification?

An escrow shortage adjustment notification is a formal notice from your mortgage servicer informing you that your escrow account balance is lower than required to cover projected property taxes and insurance premiums. This results in a recalculated monthly payment to cover the deficit and maintain the necessary minimum balance.

Why did my mortgage payment increase due to an escrow shortage?

Your mortgage payment increased because your property taxes or homeowners insurance premiums rose over the past year. To compensate for the shortage and ensure future bills are paid, your servicer adjusts your monthly escrow contribution to cover the higher costs and repay the existing deficit.

Can I pay my escrow shortage in a one-time lump sum?

Yes, most mortgage servicers provide the option to pay the full shortage amount as a one-time lump sum. While this will prevent your monthly payment from rising to cover the previous year's deficit, your payment may still increase slightly to account for the higher projected cost of taxes and insurance moving forward.

What happens if I do not pay the escrow shortage?

If you do not pay the shortage in a lump sum, your mortgage servicer will automatically spread the deficiency over a 12-month period. This amount will be added to your regular monthly mortgage payment, resulting in a higher total monthly obligation for the duration of the adjustment period.

How is a minimum escrow cushion calculated?

Under federal law (RESPA), mortgage lenders are typically allowed to maintain a "cushion" equal to one-sixth of the total annual escrow disbursements, which is equivalent to two months of payments. The adjustment notification ensures your account maintains this minimum threshold to prevent future overdrafts.

Comments