When a borrower fails to maintain the required financial margins, lenders must issue a Demand Letter for Breach of Debt Service Coverage Ratio Covenant. This formal notice alerts the debtor to the default, outlines potential acceleration of the loan, and protects the lender's legal position. Understanding how to structure this notice is essential for debt recovery. Below are some ready to use templates.

Image cover: Official Notice: Debt Service Coverage Ratio (DSCR) Covenant Breach and Demand for Remedy

Letter Samples List

- Notice of Default and Demand Letter for Debt Service Coverage Ratio Covenant Breach

- Demand Letter for Immediate Cure of Debt Service Coverage Ratio Violation

- Reservation of Rights and Demand Letter Regarding DSCR Non-Compliance

- First Warning Letter for Debt Service Coverage Ratio Covenant Breach

- Final Demand Letter for Breach of Debt Service Coverage Ratio Financial Covenant

- Letter of Demand for Debt Service Coverage Ratio Covenant Rectification

- Formal Demand Letter for Default on Debt Service Coverage Ratio

- Waiver Denial and Demand Letter for Debt Service Coverage Ratio Breach

- Notice of Acceleration and Demand Letter for DSCR Covenant Violation

- Pre-Foreclosure Demand Letter for Debt Service Coverage Ratio Default

- Letter of Notification and Demand for DSCR Covenant Cure

- Strict Compliance Demand Letter for Debt Service Coverage Ratio Covenant

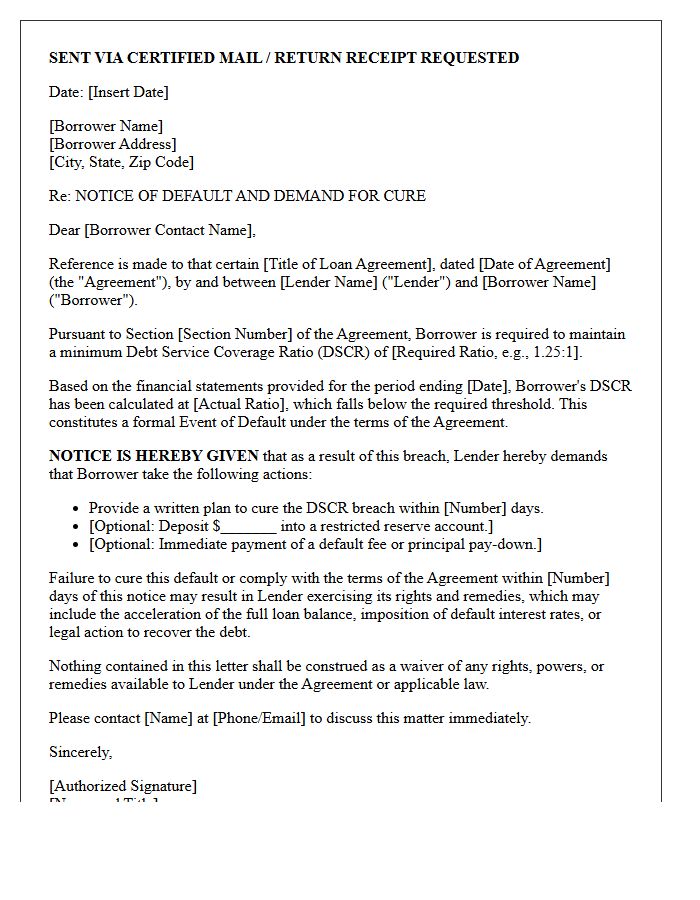

Notice of Default and Demand Letter for Debt Service Coverage Ratio Covenant Breach

A Notice of Default and Demand Letter for a Debt Service Coverage Ratio (DSCR) covenant breach is a formal legal notification from a lender to a borrower. This document signifies that the borrower's net operating income has fallen below the required threshold to cover debt obligations. It serves as a formal declaration of default, potentially triggering loan acceleration or foreclosure. Borrowers must respond urgently to negotiate a forbearance agreement or waiver to prevent the lender from exercising collateral seizure or other legal remedies outlined in the original loan contract.

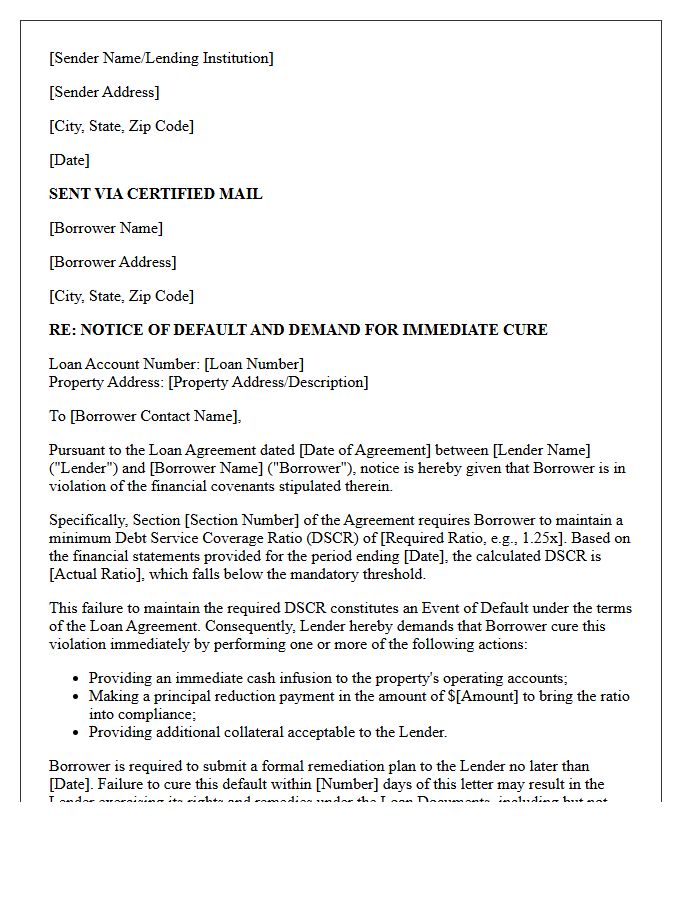

Demand Letter for Immediate Cure of Debt Service Coverage Ratio Violation

A demand letter for a DSCR violation serves as a formal notice that a borrower's net operating income has fallen below the lender's required threshold. This document mandates an immediate cure to restore the agreed-upon financial ratio. Failure to rectify this breach can trigger a technical default, allowing the lender to accelerate the loan or seize collateral. Common remedies include making a principal curtailment or boosting revenue to ensure the property generates sufficient cash flow to cover its annual debt obligations securely.

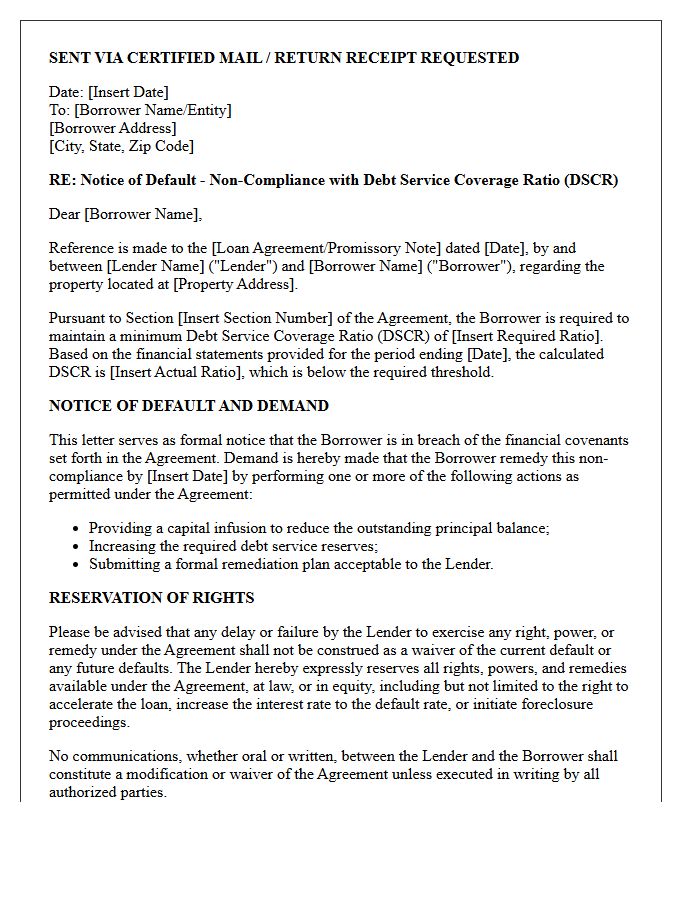

Reservation of Rights and Demand Letter Regarding DSCR Non-Compliance

A Reservation of Rights letter is a critical legal tool used by lenders when a borrower fails to meet the Debt Service Coverage Ratio (DSCR) requirement. This document informs the borrower of the default while formally preserving the lender's right to pursue future remedies, such as foreclosure or acceleration, without immediate waiver. Simultaneously, a demand letter may require immediate corrective action or additional collateral to restore compliance. Understanding these notices is vital, as they signal potential legal escalation and provide a formal record of the non-compliance event under the loan agreement.

First Warning Letter for Debt Service Coverage Ratio Covenant Breach

A first warning letter for a DSCR covenant breach notifies a borrower that their net operating income is insufficient to cover debt obligations. This formal notice signals a technical default, though lenders often prioritize resolution over immediate foreclosure. It is crucial to provide a compliance certificate and a detailed remediation plan to restore the ratio. Open communication and financial transparency are essential to negotiate a waiver or amendment, preventing further escalation like accelerated repayment or increased interest rates. Addressing this early protects your creditworthiness and long-term financing stability.

Final Demand Letter for Breach of Debt Service Coverage Ratio Financial Covenant

A final demand letter for breaching a Debt Service Coverage Ratio (DSCR) covenant serves as a formal notice that a borrower has failed to maintain sufficient cash flow to cover loan obligations. This document typically accelerates the debt, meaning the entire outstanding balance becomes immediately due. It marks the final step before a lender initiates legal action or foreclosure. Receiving this letter indicates that previous cure periods have expired, and the lender is now exercising its contractual rights to protect its capital against heightened financial risk and potential default.

Letter of Demand for Debt Service Coverage Ratio Covenant Rectification

A Letter of Demand for DSCR Covenant Rectification is a formal notice issued by a lender when a borrower's cash flow fails to meet the required debt service obligations. This document identifies a specific financial covenant breach, requiring the borrower to implement immediate corrective actions. Failure to restore the ratio within the remedy period may trigger a technical default, leading to accelerated repayment or collateral seizure. It serves as a critical legal step to protect the lender's interests while demanding a credible turnaround plan to ensure future loan sustainability.

Formal Demand Letter for Default on Debt Service Coverage Ratio

A formal demand letter for a DSCR default serves as an official notice that a borrower's net operating income has fallen below the required threshold to cover debt obligations. This legal document alerts the debtor to a covenant breach, potentially triggering loan acceleration or technical default penalties. It is a critical step for lenders to protect their interests, often requiring the borrower to provide a remedy plan or additional collateral to restore financial stability and maintain the credit agreement's standing.

Waiver Denial and Demand Letter for Debt Service Coverage Ratio Breach

A DSCR breach occurs when a property's net operating income fails to meet the lender's required coverage ratio. If the lender issues a waiver denial, they have officially refused to overlook the default. This typically triggers a demand letter, a formal legal notice requiring the borrower to rectify the violation immediately. Possible consequences include accelerated loan repayment, increased interest rates, or the commencement of foreclosure proceedings. To protect your investment, you must promptly address the financial shortfall or negotiate alternative restructuring terms to avoid total loss of the asset.

Notice of Acceleration and Demand Letter for DSCR Covenant Violation

A Notice of Acceleration and Demand Letter is a formal legal notification issued by a lender when a borrower breaches a DSCR covenant. This document signals that the entire loan balance is now due immediately. Since the Debt Service Coverage Ratio measures the property's ability to cover debt payments with its net operating income, a violation indicates financial distress. Receiving this letter means the lender has revoked the installment plan, often serving as the final step before foreclosure or legal action to recover the outstanding capital and interest.

Pre-Foreclosure Demand Letter for Debt Service Coverage Ratio Default

A pre-foreclosure demand letter for a DSCR default serves as a formal notice that a commercial property's net operating income has fallen below the required debt service coverage ratio. This document warns the borrower that they are in technical default of their loan covenants, even if monthly payments are current. It outlines the specific remediation period and required actions to avoid acceleration. Understanding this letter is crucial for investors to initiate workout negotiations, cure the financial imbalance, and prevent the lender from initiating formal foreclosure proceedings against the collateralized asset.

Letter of Notification and Demand for DSCR Covenant Cure

A Letter of Notification and Demand for DSCR Covenant Cure is a formal legal notice issued by a lender when a property's Debt Service Coverage Ratio falls below the agreed threshold. This document serves as an official warning that the borrower is in technical default. To maintain compliance, the borrower must cure the breach, typically by making a principal reduction payment or increasing net operating income. Timely action is essential to avoid loan acceleration, penalties, or potential foreclosure proceedings initiated by the financial institution.

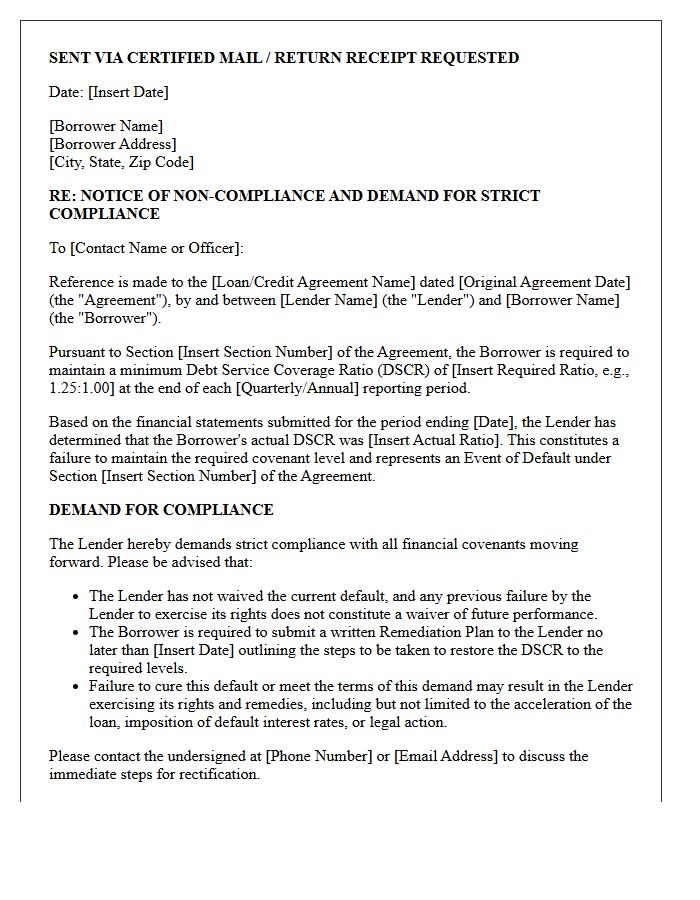

Strict Compliance Demand Letter for Debt Service Coverage Ratio Covenant

A strict compliance demand letter serves as a formal notification that a borrower has failed to maintain the required Debt Service Coverage Ratio (DSCR), triggering a technical default. This document emphasizes that the lender is enforcing covenant compliance without granting further leniency or waivers. It typically outlines the specific financial breach, demands immediate corrective action, and preserves the lender's right to accelerate the loan or seize collateral. Understanding this letter is critical, as it signals that the financial institution is prioritizing risk mitigation over informal negotiations to protect its capital investment.

What is a Demand Letter for Breach of Debt Service Coverage Ratio (DSCR)?

A Demand Letter for Breach of DSCR is a formal legal notice sent by a lender to a borrower when the borrower's cash flow fails to meet the minimum Debt Service Coverage Ratio specified in the loan agreement. It serves as a notice of default, demanding that the borrower rectify the covenant violation to avoid further legal action or loan acceleration.

What are the common consequences of receiving a DSCR covenant breach notice?

Common consequences include the implementation of a "cash trap" or sweep, increased interest rates (default rates), a suspension of further draws on credit lines, and the requirement of a principal pay-down to restore the ratio. If the breach is not cured, the lender may reserve the right to accelerate the entire loan balance or initiate foreclosure proceedings.

How can a borrower cure a breach of the Debt Service Coverage Ratio covenant?

Borrowers typically cure a DSCR breach by making a "curative payment" to reduce the outstanding principal debt, providing additional collateral, or negotiating a formal waiver or amendment with the lender. In some cases, an equity injection from ownership can improve the cash flow position to meet the required financial threshold.

Is a DSCR covenant breach considered a technical default or a payment default?

A DSCR breach is classified as a technical default because it involves a violation of the loan's financial reporting and performance requirements rather than a failure to make scheduled principal and interest payments. However, most loan documents stipulate that a technical default carries the same legal weight and remedies as a payment default if left unaddressed.

Does a lender have to provide a grace period after issuing a DSCR demand letter?

The requirement for a grace or "cure" period depends entirely on the specific terms of the Credit Agreement or Deed of Trust. While many agreements offer 15 to 30 days to remedy a financial covenant breach, some contracts allow the lender to declare an immediate default upon the submission of a non-compliant Compliance Certificate.

Comments