An erroneous clearing house transfer can disrupt business operations and cause significant financial discrepancies. If your organization has mistakenly sent funds or received an unauthorized credit, issuing a formal Demand Letter for Return of Erroneous Clearing House Funds is the essential first step for legal recovery and financial reconciliation. Learn how to assert your rights effectively; below are some ready to use template.

Image cover: Formal Demand for Reversal of Erroneous Clearing House Transfers: Templates and Legal Notice Guide

Letter Samples List

- Demand Letter for Return of Erroneous Clearing House Funds

- First Notice Letter for Recovery of Misdirected ACH Settlement

- Final Demand Letter for Reversal of Duplicate Wire Transfer

- Urgent Letter of Demand for Recall of Incorrect Interbank Funds

- Formal Demand Letter for Restitution of Misrouted Clearing Funds

- Official Notice and Demand Letter for Erroneously Credited Account

- Second Request Letter for Return of Unjustified Clearing Settlement

- Legal Demand Letter for Immediate Remittance of Mistaken Fedwire Transfer

- Pre-Litigation Demand Letter for Unreturned Clearing House Transaction

- Bank to Bank Demand Letter for Mistaken Institutional Credit Reversal

- Compliance Demand Letter for Recovery of Invalid Clearing House Payment

- Executive Demand Letter for Reimbursement of Erroneous Settlement Funds

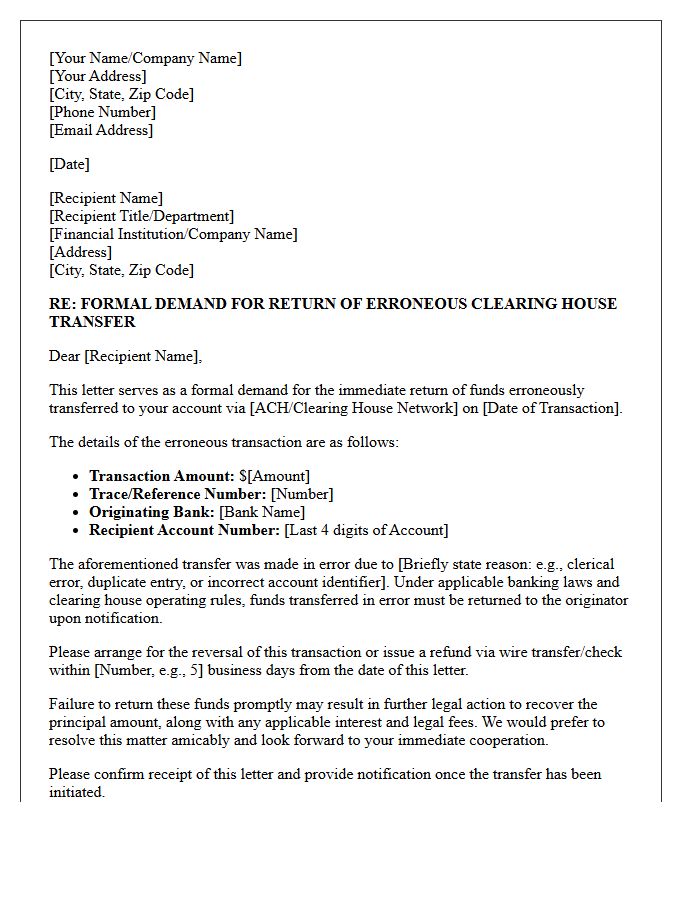

Demand Letter for Return of Erroneous Clearing House Funds

A demand letter for the return of erroneous clearing house funds is a formal legal request used to recover misdirected electronic transfers. It serves as official notice to the recipient that funds were credited in error, often due to technical glitches or incorrect account details. Clearly state the transaction date, exact amount, and reference numbers to facilitate tracking. Highlighting the legal obligation for restitution is essential to avoid claims of unjust enrichment. Providing a specific deadline for repayment encourages a swift resolution and establishes a necessary paper trail for potential litigation or regulatory escalation.

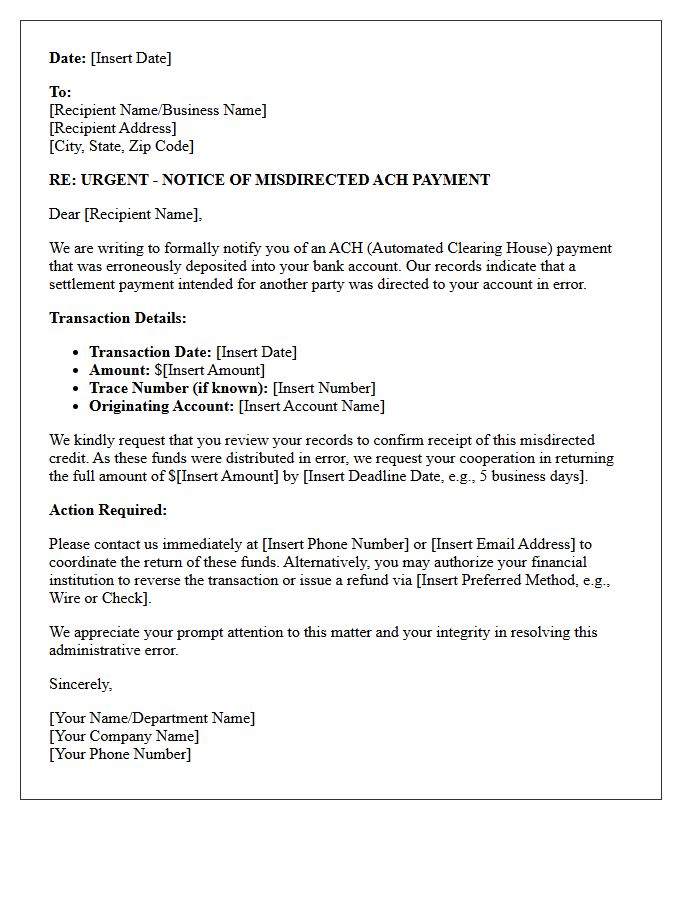

First Notice Letter for Recovery of Misdirected ACH Settlement

A First Notice Letter is a formal legal request sent to a recipient who unintentionally received funds due to a banking error. It serves as an official demand for the recovery of misdirected ACH settlements by notifying the party of the mistake and their obligation to return the money. Promptly responding to this notice is critical to avoid potential litigation or bank-enforced reversals. This document establishes a clear paper trail, ensuring that both the sender and the financial institution can resolve the erroneous transfer efficiently and according to federal banking regulations.

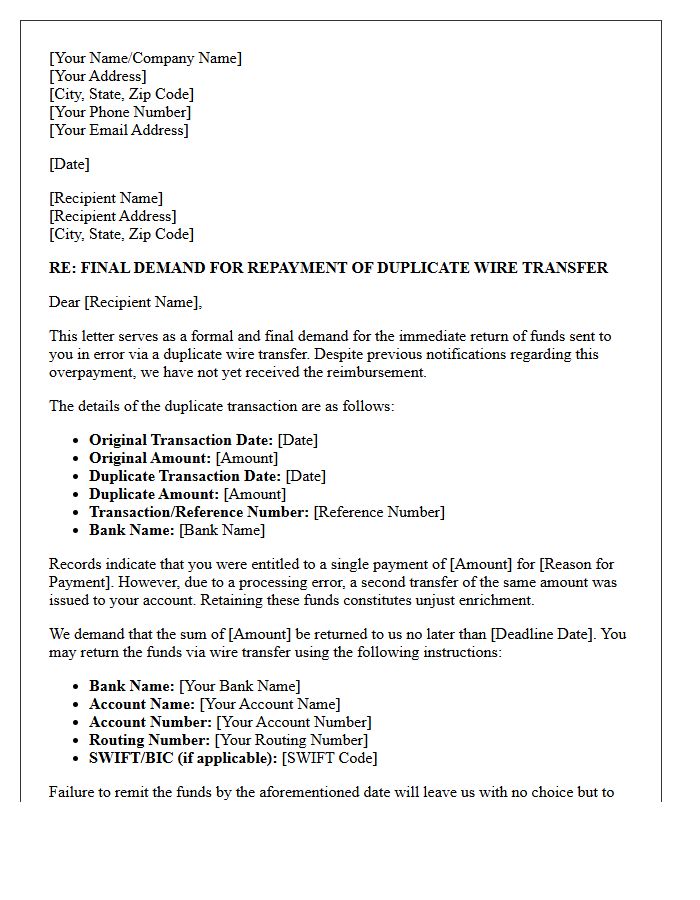

Final Demand Letter for Reversal of Duplicate Wire Transfer

A final demand letter for a wire transfer reversal serves as a formal legal notice to recover funds credited twice. This document must clearly state the transaction dates, reference numbers, and the exact duplicate amount. It notifies the recipient of their legal obligation to return the unintended enrichment immediately. Explicitly mentioning a deadline for repayment and potential legal action for non-compliance is essential to ensure a swift resolution. Providing clear instructions for the return transfer helps facilitate the process and provides critical evidence if a court claim becomes necessary.

Urgent Letter of Demand for Recall of Incorrect Interbank Funds

An Urgent Letter of Demand is a formal legal notice used to recall funds sent to the wrong bank account. It serves as critical evidence that you identified the error and requested a reversal immediately. To be effective, the document must include the specific transaction reference, date, and exact amount. Acting swiftly is vital because banks require formal authorization to freeze or recover misdirected payments. Sending this letter creates a clear paper trail, which is essential if legal action or a bank indemnity process becomes necessary to reclaim your capital.

Formal Demand Letter for Restitution of Misrouted Clearing Funds

A formal demand letter for the restitution of misrouted clearing funds serves as a critical legal notice to recover capital sent to the wrong account. It must clearly outline the transaction details, including the date, amount, and routing numbers involved. To ensure effectiveness, the document should specify a strict deadline for repayment and state the intent to pursue litigation if the debt remains unpaid. This formal communication establishes a verifiable paper trail, proving the sender's attempt to resolve the financial discrepancy before escalating to regulatory authorities or court action.

Official Notice and Demand Letter for Erroneously Credited Account

An Official Notice and Demand Letter serves as a formal legal instrument to recover funds mistakenly deposited into a bank account. This document notifies the recipient of the error, asserts the rightful owner's legal claim, and establishes a specific deadline for restitution. It is a critical step in demonstrating good faith before pursuing litigation or reporting the incident to financial regulators. Providing clear evidence of the erroneous transaction ensures the recipient understands their obligation to return the capital promptly to avoid potential charges of unjust enrichment or theft.

Second Request Letter for Return of Unjustified Clearing Settlement

A Second Request Letter serves as a final formal demand for the return of unjustified clearing settlement funds. This document is essential if a financial institution fails to rectify an erroneous debit or overpayment after the initial notice. Clearly state the original transaction details, the specific amount owed, and the previous communication history. Emphasizing a deadline for reimbursement demonstrates legal intent and urgency. This follow-up ensures a documented paper trail, which is critical for regulatory compliance or potential litigation if the dispute remains unresolved.

Legal Demand Letter for Immediate Remittance of Mistaken Fedwire Transfer

A legal demand letter for the immediate remittance of a mistaken Fedwire transfer is a formal notice used to recover funds sent in error. It serves as a pre-litigation requirement, notifying the recipient of their legal obligation to return the money under principles of unjust enrichment. The document must include precise transaction details, a strict deadline for repayment, and a clear warning of impending legal action. Promptly issuing this letter is critical to freeze assets and prevent the unauthorized permanent loss of capital through subsequent transfers or withdrawals.

Pre-Litigation Demand Letter for Unreturned Clearing House Transaction

A Pre-Litigation Demand Letter serves as a formal legal notice to recover funds from an unreturned Clearing House transaction. It establishes a clear timeline for repayment, typically ten business days, before escalating to a lawsuit. This document is essential for proving a good-faith attempt to resolve the dispute out of court. Key elements include the precise transaction date, the exact dollar amount, and clear evidence of the failed reversal. Sending this via certified mail creates a vital evidentiary trail that strengthens your position during potential breach of contract or unjust enrichment litigation.

Bank to Bank Demand Letter for Mistaken Institutional Credit Reversal

A bank-to-bank demand letter is a formal legal request used to resolve a Mistaken Institutional Credit Reversal. This document is essential when a financial institution erroneously claws back funds from a recipient's account without valid justification. It serves as formal notice to the initiating bank, demanding the immediate restoration of capital while citing specific transaction details and regulatory compliance. Sending this letter is a critical first step in dispute resolution, establishing a paper trail for potential litigation or regulatory escalation if the institution fails to rectify the accounting error promptly.

Compliance Demand Letter for Recovery of Invalid Clearing House Payment

A Compliance Demand Letter is a formal legal notice issued to recover funds from an invalid clearing house payment. This document serves as a critical first step in the restitution process, notifying the recipient of a processing error, unauthorized debit, or breach of protocol. It outlines the specific transaction details, legal basis for the claim, and a deadline for repayment. Properly structured letters help avoid protracted litigation by documenting the recovery effort and providing the recipient an opportunity to rectify the financial discrepancy voluntarily under banking regulations.

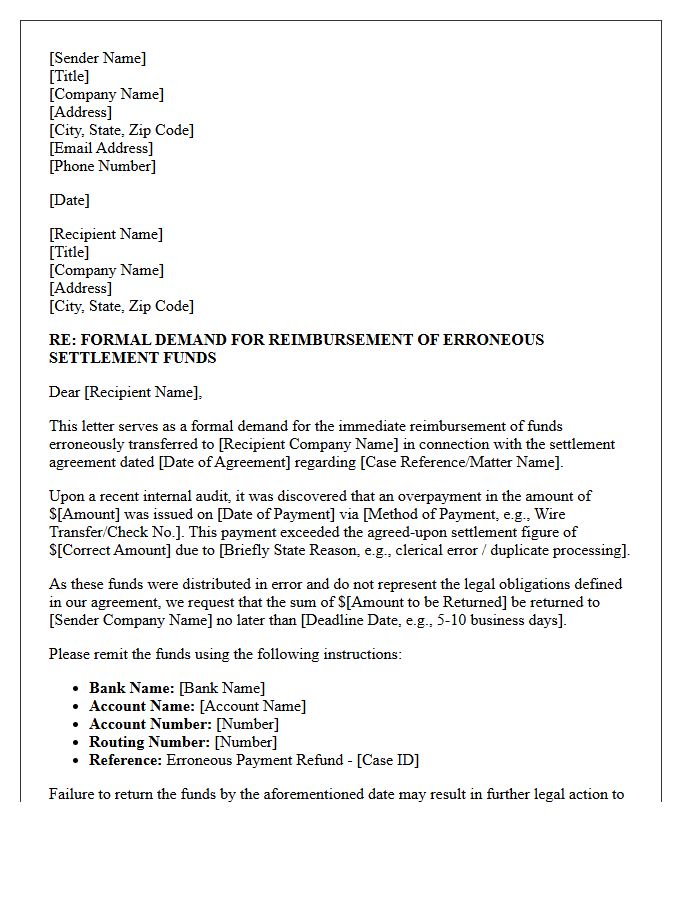

Executive Demand Letter for Reimbursement of Erroneous Settlement Funds

An executive demand letter for reimbursement of erroneous settlement funds is a formal legal notice used to recover overpayments or funds distributed by mistake. It serves as a pre-litigation strategy to resolve financial discrepancies without immediate court intervention. The document must clearly outline the specific accounting error, provide a strict repayment deadline, and detail the legal basis for the claim. By formally documenting the demand, organizations protect their rights and establish a clear evidence trail necessary for potential future litigation regarding unjust enrichment or breach of settlement terms.

What is a Demand Letter for Return of Erroneous Clearing House Funds?

This is a formal legal notice sent by a financial institution or business to a recipient who has received money through an Automated Clearing House (ACH) or wire transfer by mistake. The letter demands the immediate reversal or repayment of the specific funds identified as erroneously processed.

What information should be included in an erroneous fund recovery demand?

The letter must include the exact transaction date, the trace or reference number, the specific dollar amount, the originating bank details, and the reason for the error (such as a duplicate entry or incorrect account number). It should also provide clear instructions and a deadline for returning the funds.

How long does a recipient have to return funds after receiving a demand letter?

Standard demand letters typically provide a window of 3 to 10 business days for the recipient to initiate a reversal. While NACHA rules govern technical reversals, a formal demand letter serves as a legal prerequisite for further litigation if the recipient refuses to cooperate.

Can a recipient legally keep money sent via an ACH error?

No. Under the principle of "unjust enrichment," a recipient has no legal right to retain funds sent in error. Failing to return the money after receiving a formal demand can lead to civil lawsuits, bank account freezes, and in some jurisdictions, criminal charges for theft of property lost by mistake.

What are the next steps if the demand letter for clearing house funds is ignored?

If the recipient fails to respond or return the funds by the specified deadline, the sender may file a claim in small claims court or superior court depending on the amount. Additionally, the sender can contact the recipient's financial institution to report a "Notification of Change" or a "Reclamation" request under banking regulations.

Comments