Protect your company's capital by issuing a formal demand letter for small business line of credit revocation. If a lender unexpectedly cancels your access to funds without legal justification, a professional notice can help restore your financing or document a breach of contract. Understanding your rights is essential for financial stability. To assist your efforts, below are some ready to use template.

Image cover: Protecting Your Business: Responding to a Line of Credit Revocation (With Templates)

Letter Samples List

- Initial Demand Letter for Small Business Line of Credit Revocation

- Final Notice Demand Letter for Small Business Line of Credit Revocation

- Breach of Covenant Demand Letter for Small Business Line of Credit Revocation

- Non-Payment Default Demand Letter for Small Business Line of Credit Revocation

- Material Adverse Change Demand Letter for Small Business Line of Credit Revocation

- Collateral Shortfall Demand Letter for Small Business Line of Credit Revocation

- Immediate Repayment Demand Letter for Small Business Line of Credit Revocation

- Pre-Litigation Demand Letter for Small Business Line of Credit Revocation

- Account Delinquency Demand Letter for Small Business Line of Credit Revocation

- Insolvency Risk Demand Letter for Small Business Line of Credit Revocation

- Facility Closure Demand Letter for Small Business Line of Credit Revocation

- Asset Seizure Demand Letter for Small Business Line of Credit Revocation

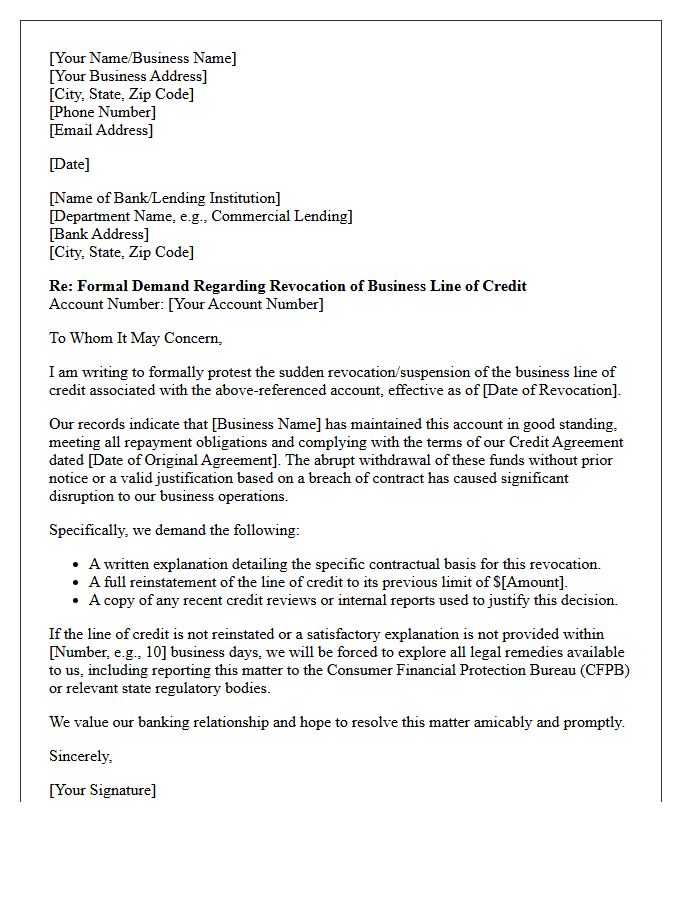

Initial Demand Letter for Small Business Line of Credit Revocation

Receiving an initial demand letter regarding a Small Business Line of Credit Revocation signifies that the lender has terminated your access to funds and requires immediate repayment. This legal notice often triggers due to a default, such as missed payments or a breach of financial covenants. It is critical to review the specific default reason and the deadline for full acceleration of the debt. To protect your business assets, you should immediately document all communications and seek legal counsel to negotiate a workout agreement or repayment plan before litigation begins.

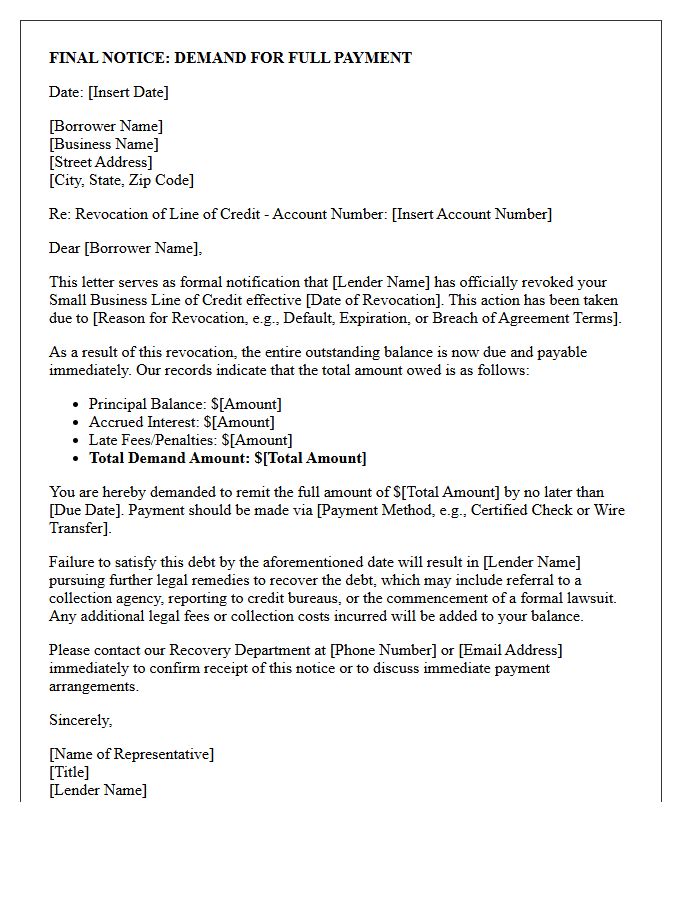

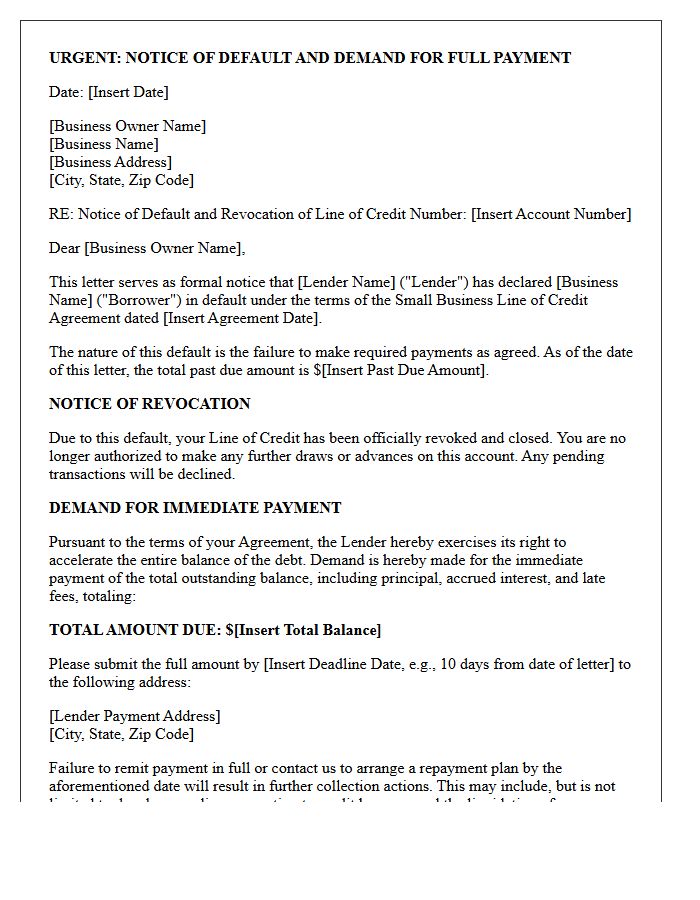

Final Notice Demand Letter for Small Business Line of Credit Revocation

A final notice demand letter signifies the immediate revocation of your small business line of credit. This formal document requires the full repayment of the outstanding balance, including interest and fees, by a strict deadline. Failure to comply typically results in legal action, asset seizure, or a negative impact on your business credit score. It is the last opportunity to resolve the debt before the lender initiates liquidation or collections. Reviewing the original loan agreement and seeking legal counsel is essential to understand your repayment obligations and potential settlement options.

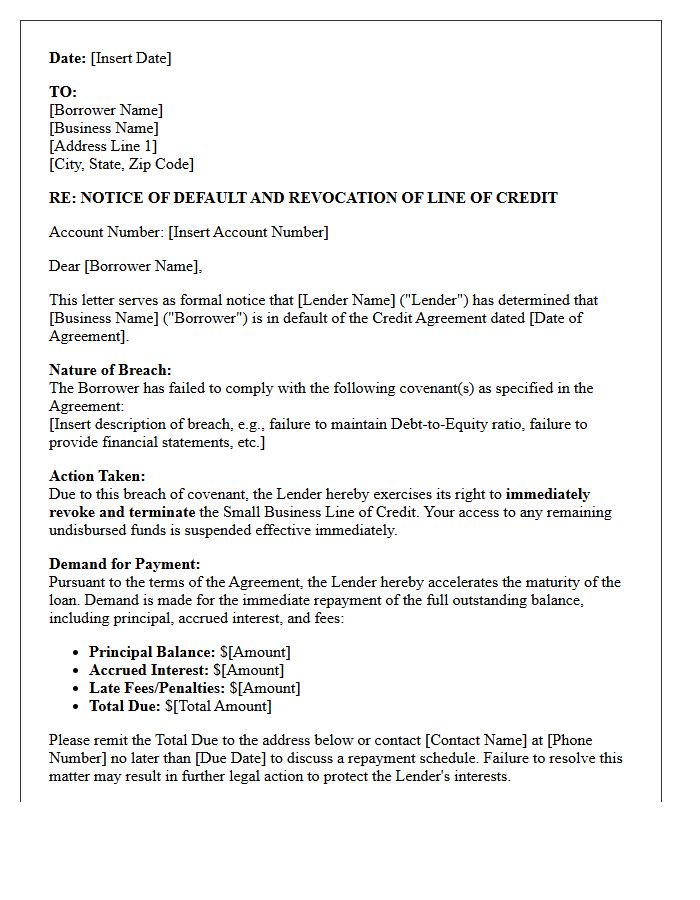

Breach of Covenant Demand Letter for Small Business Line of Credit Revocation

A breach of covenant demand letter is a formal legal notice issued when a small business fails to meet specific loan requirements. This document signifies that the lender may trigger a line of credit revocation, immediately ending access to funds. It typically outlines the specific violation, such as a missed financial ratio or late payment. To prevent total closure, businesses must provide a formal response or a cure plan. Understanding these terms is vital, as a default can lead to accelerated repayment demands and severe damage to your business credit profile.

Non-Payment Default Demand Letter for Small Business Line of Credit Revocation

A non-payment default demand letter is a critical formal notice indicating your Small Business Line of Credit has been revoked due to missed payments. This legal document signifies that the lender has terminated your borrowing privileges and is now accelerating the debt, making the entire outstanding balance due immediately. Small business owners must act quickly to negotiate a repayment plan or cure the default to avoid aggressive collection actions, lawsuits, or permanent damage to their corporate credit rating and personal assets used as collateral.

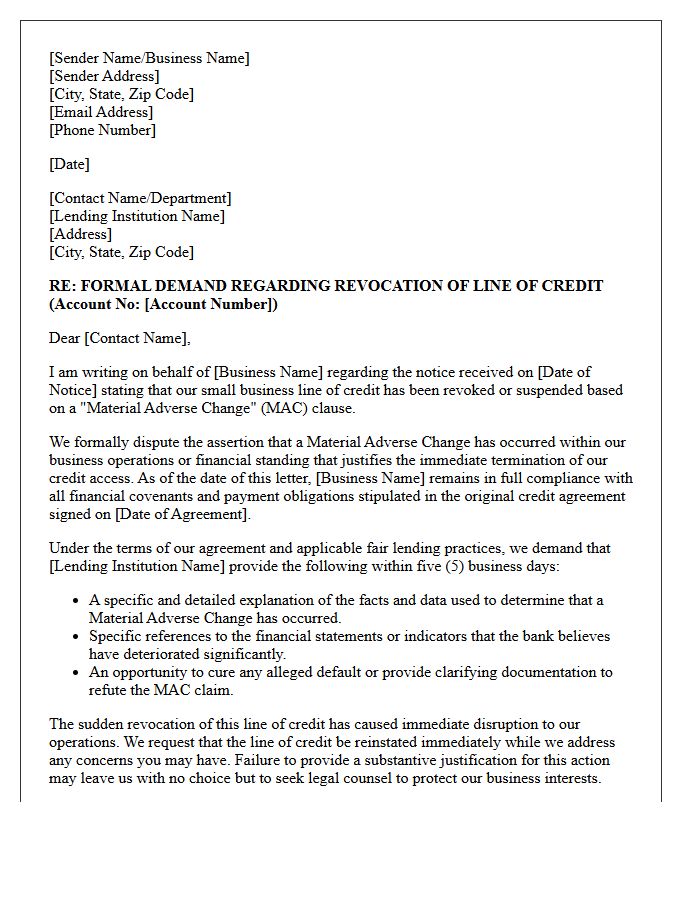

Material Adverse Change Demand Letter for Small Business Line of Credit Revocation

A Material Adverse Change (MAC) demand letter is a formal notice from a lender terminating a small business line of credit. It asserts that a significant decline in the borrower's financial stability or operational health has occurred, triggering a default clause. Small businesses must respond immediately with documented proof of solvency to contest the revocation. Understanding these clauses is vital, as they allow banks to freeze funding based on subjective assessments of risk. Consulting legal counsel is essential to challenge the lender's adverse determination and protect your company's liquidity.

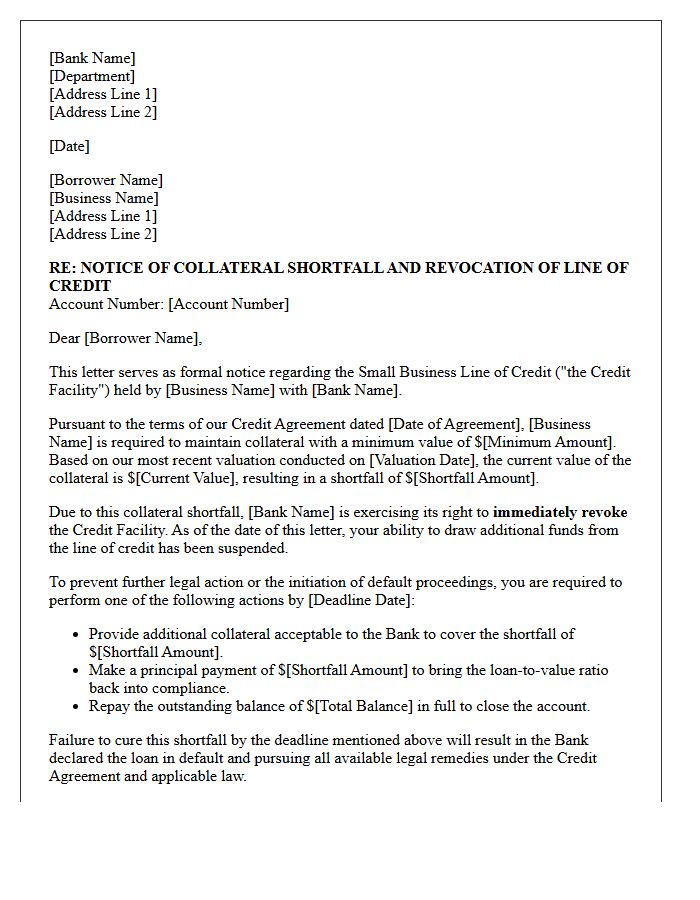

Collateral Shortfall Demand Letter for Small Business Line of Credit Revocation

A Collateral Shortfall Demand Letter is a formal notice from a lender stating that the assets securing your Small Business Line of Credit have decreased in value. This imbalance triggers a violation of the loan-to-value ratio, allowing the bank to initiate revocation of your credit access. Borrowers must immediately provide additional security or pay down the principal to restore the required margin. Ignoring this demand often leads to a default, immediate repayment acceleration, and potential seizure of existing business assets to satisfy the outstanding debt obligations.

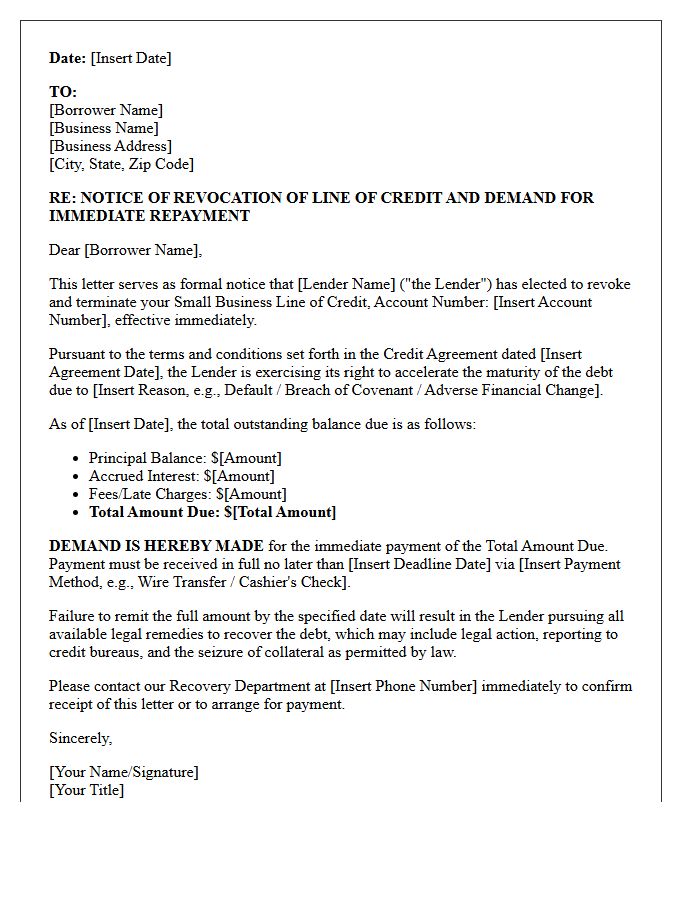

Immediate Repayment Demand Letter for Small Business Line of Credit Revocation

An Immediate Repayment Demand Letter signals that a lender has officially revoked your small business line of credit. This formal notice typically triggers a full balance acceleration, requiring total repayment within a specified deadline. Business owners must immediately review their loan agreement for default triggers and seek legal counsel to negotiate a forbearance or repayment plan. Ignoring this document can lead to asset seizure or personal liability if a guarantee was signed. Prioritizing open communication with the bank is essential to prevent aggressive collection actions or business insolvency during a credit withdrawal.

Pre-Litigation Demand Letter for Small Business Line of Credit Revocation

A pre-litigation demand letter is a legal formal notice sent to a lender after a small business line of credit is abruptly revoked. It serves to highlight breach of contract or lack of "good faith" in the bank's decision. This document outlines your intent to pursue legal action unless the credit facility is restored or damages are paid. Formally documenting the dispute encourages settlement negotiations before incurring high court costs, often prompting lenders to justify their actions or offer a workout agreement to avoid litigation.

Account Delinquency Demand Letter for Small Business Line of Credit Revocation

An Account Delinquency Demand Letter serves as a final formal notice before a lender initiates the revocation of a small business line of credit. This legal document notifies the borrower that their payment default has triggered a breach of contract. It demands immediate repayment of the outstanding balance to avoid permanent closure of the credit facility and potential legal action. Receiving this letter indicates that the acceleration clause has been activated, making the entire debt due immediately, which can severely impact business credit scores and future financing eligibility.

Insolvency Risk Demand Letter for Small Business Line of Credit Revocation

An insolvency risk demand letter is a formal notice from a lender stating they believe your business can no longer meet its financial obligations. This trigger allows the bank to perform a line of credit revocation, immediately freezing your access to funds. To protect your business, you must demonstrate liquidity and provide updated financial statements to prove solvency. Receiving this letter is a critical warning; failure to respond with proof of fiscal health often leads to a total recall of the outstanding balance, potentially forcing a liquidation process or bankruptcy.

Facility Closure Demand Letter for Small Business Line of Credit Revocation

A facility closure demand letter notifies a borrower that their small business line of credit has been permanently revoked. This legal document mandates the immediate repayment of the total outstanding balance, including interest and fees. Lenders typically issue these notices due to default, financial instability, or expired terms. Failure to comply can lead to asset seizure, litigation, or damage to your credit profile. It is essential to review your loan agreement immediately and consider professional legal counsel to negotiate a settlement or structured exit plan to protect your enterprise.

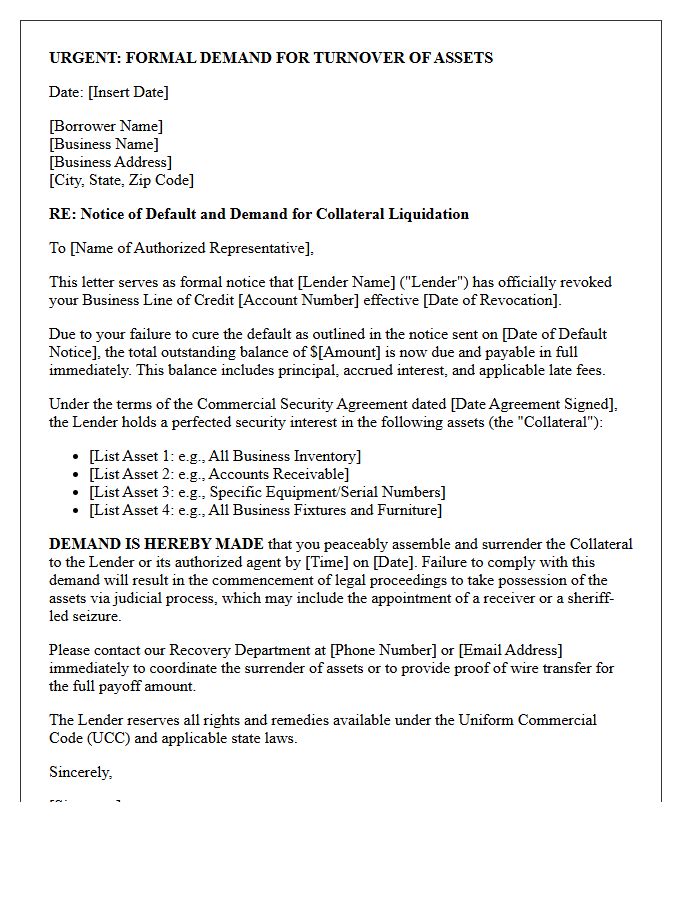

Asset Seizure Demand Letter for Small Business Line of Credit Revocation

Receiving an asset seizure demand letter signifies that your lender has initiated legal acceleration of your small business line of credit. This formal notice typically follows a default or revocation of your borrowing privileges. It warns that the creditor intends to repossess collateral, such as equipment, inventory, or accounts receivable, to satisfy the outstanding debt. To protect your enterprise, you must immediately review the cure period and security agreement terms. Seeking professional legal counsel is vital to negotiate a settlement or restructuring plan before the forced liquidation of essential business assets begins.

What is a demand letter for a small business line of credit revocation?

A demand letter is a formal legal notice sent by a lender to a borrower officially notifying them that their business line of credit has been revoked and demanding the immediate repayment of the outstanding balance, interest, and applicable fees.

Under what conditions can a bank revoke a business line of credit?

Lenders typically revoke lines of credit due to "events of default," which include failure to make timely payments, a significant drop in the business's credit score, a breach of loan covenants, or a material adverse change in the borrower's financial condition.

How long do I have to pay the balance after receiving a revocation demand letter?

The repayment timeframe is governed by the original credit agreement; however, because lines of credit are often "payable on demand," the letter may require full payment within 7 to 30 days to avoid further legal action or collateral liquidation.

Can a demand letter for credit revocation be contested or negotiated?

Yes, business owners can respond by disputing inaccuracies in the default claim or by proposing a structured repayment plan or "workout agreement" to prevent the lender from pursuing aggressive collection tactics or seizing assets.

What happens if a business ignores a demand letter for a revoked line of credit?

Ignoring the letter usually results in the lender accelerating the debt, reporting the default to credit bureaus, and initiating legal proceedings to obtain a judgment or seize business and personal assets used as collateral for the loan.

Comments