A demand letter for unsecured personal loan default serves as a formal notice to borrowers who have failed to make payments. This legal document outlines the outstanding balance, specifies a final repayment deadline, and details potential legal consequences for non-compliance. It is a critical step in debt collection before initiating litigation. To help you draft a professional notice, below are some ready to use template.

Image cover: Official Demand for Payment: Unsecured Personal Loan Default Notice and Templates

Letter Samples List

- Initial Demand Letter for Unsecured Personal Loan Default

- Final Demand Letter for Unsecured Personal Loan Default

- Pre-Legal Action Demand Letter for Loan Default

- Notice of Default and Payment Demand Letter

- Account Acceleration and Debt Demand Letter

- Breach of Contract Demand Letter for Unsecured Loan

- Delinquent Account Payment Demand Letter

- Final Warning Demand Letter Before Litigation

- Unsecured Credit Default Demand Letter

- Bank Notice and Demand Letter for Outstanding Balance

- Settlement Offer and Repayment Demand Letter

- Outstanding Debt Collection Demand Letter

- Formal Demand Letter for Unsecured Loan Repayment

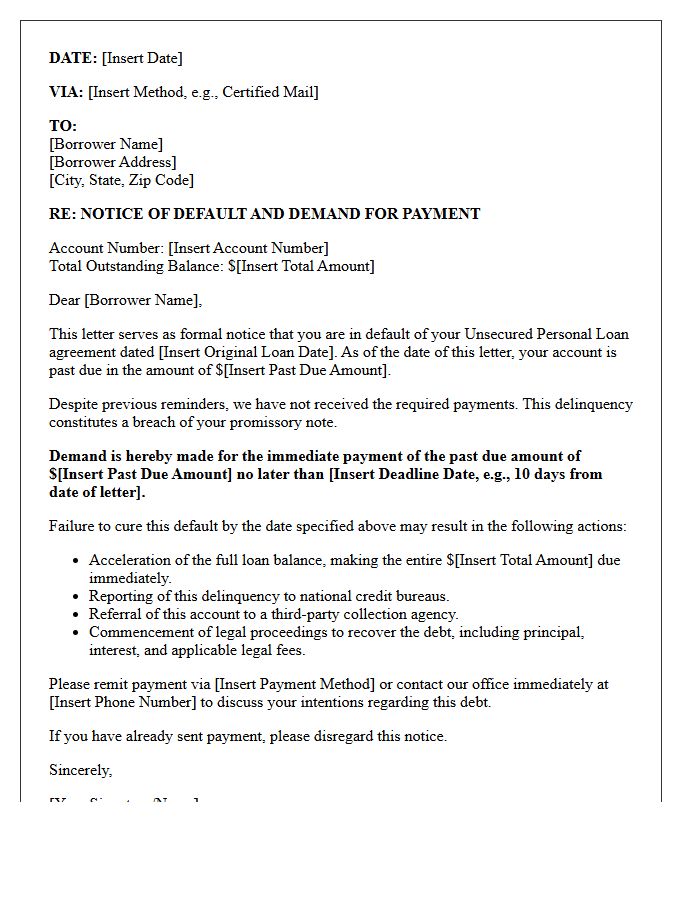

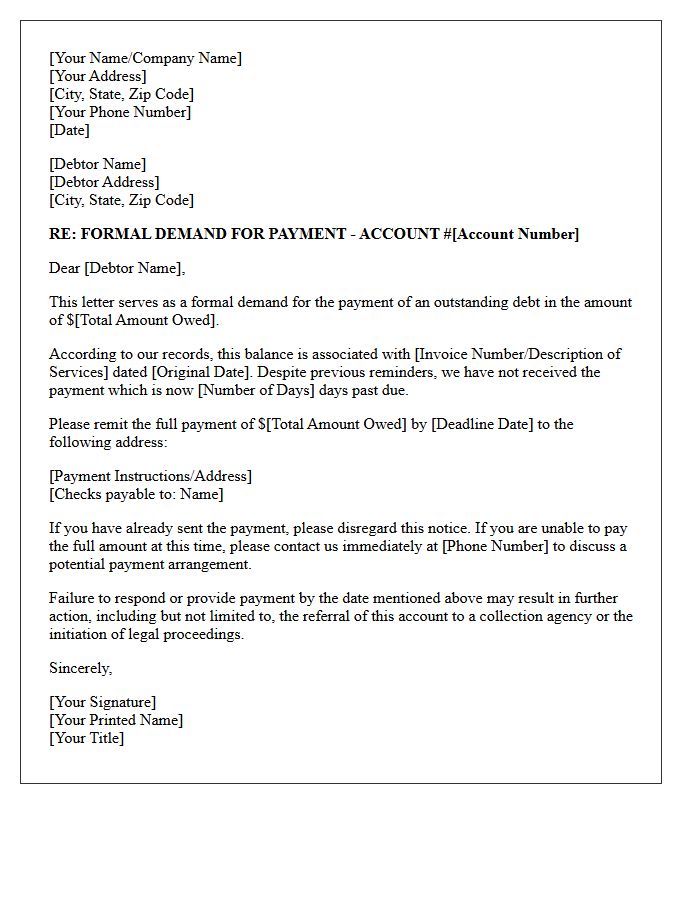

Initial Demand Letter for Unsecured Personal Loan Default

An Initial Demand Letter serves as a formal notification when a borrower defaults on an unsecured personal loan. This document officially notifies the debtor of their breach of contract and specifies the outstanding balance, including interest and late fees. It establishes a strict deadline for payment to avoid further legal action or credit damage. Receiving this letter is a critical warning; responding promptly can prevent the debt from being sold to a collection agency or resulting in a lawsuit. It acts as essential evidence of the lender's attempt to resolve the debt amicably.

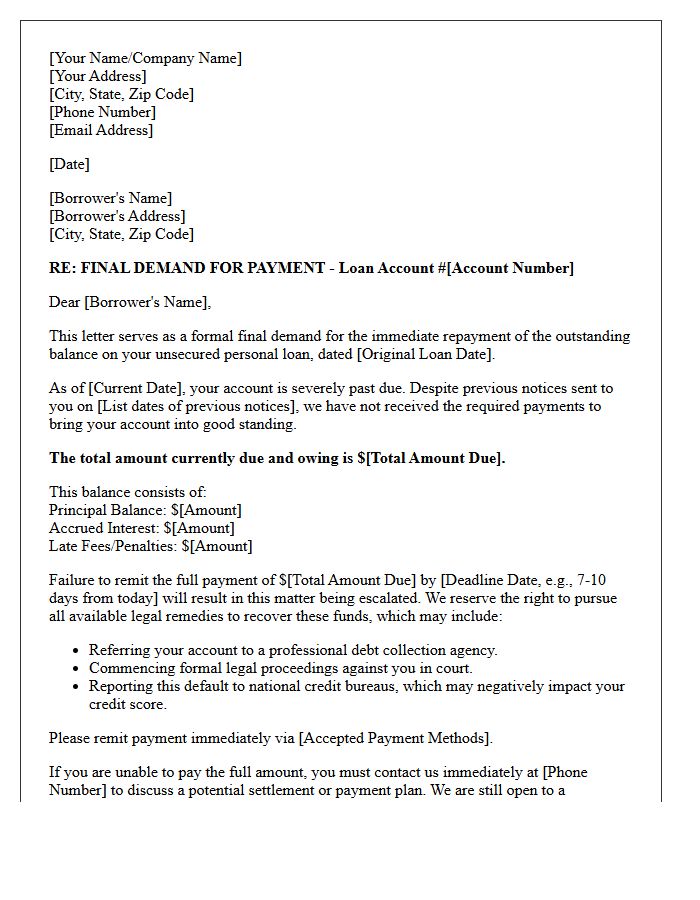

Final Demand Letter for Unsecured Personal Loan Default

A Final Demand Letter is the formal legal notice issued before a lender initiates litigation or debt collection actions for an unsecured personal loan default. It outlines the total outstanding balance, including accrued interest and penalties, while providing a strict deadline for payment. Receiving this letter indicates that internal collections have ended and legal proceedings or credit reporting damage are imminent. Borrowers should prioritize immediate communication or settlement negotiations to avoid court summons, wage garnishment, or a severe negative impact on their long-term credit score.

Pre-Legal Action Demand Letter for Loan Default

A Pre-Legal Action Demand Letter serves as a final formal notice to a borrower in default. It outlines the total outstanding debt, including interest and penalties, while establishing a strict deadline for repayment. This document is a critical procedural requirement that demonstrates a creditor's good-faith effort to resolve the dispute before initiating litigation. Receiving or sending this letter signifies that failure to comply will result in immediate court proceedings, potentially leading to asset seizure or wage garnishment. It acts as vital evidence of notification in future legal hearings.

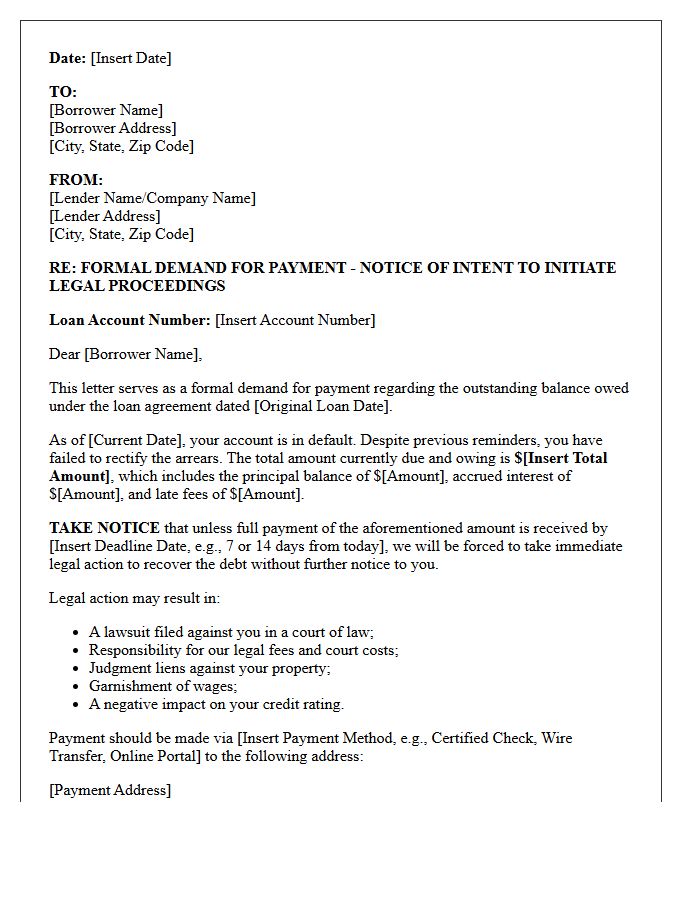

Notice of Default and Payment Demand Letter

A Notice of Default and Payment Demand Letter is a critical legal document sent by a creditor to notify a borrower of a breach of contract. It formally identifies the specific delinquency and outlines the total amount owed to rectify the debt. Receiving this notice serves as a final warning before the lender initiates foreclosure or legal action. To protect your rights, you must respond within the specified timeframe to avoid further penalties or the loss of collateral. Prompt reinstatement or negotiation is essential to resolve the default status effectively.

Account Acceleration and Debt Demand Letter

An Account Acceleration occurs when a creditor demands immediate full repayment of an outstanding balance after a borrower defaults. This action is officially initiated through a Debt Demand Letter, which serves as a formal legal notice. Receiving this document means you have lost the privilege of installment payments. It is crucial to act quickly to avoid litigation or foreclosure. Understanding your rights under the Fair Debt Collection Practices Act is essential for negotiating potential settlements or reinstatement plans to resolve the delinquency before further legal escalation occurs.

Breach of Contract Demand Letter for Unsecured Loan

A Breach of Contract Demand Letter serves as a formal legal notice requesting the immediate repayment of an unsecured loan. Since no collateral backs the debt, this document is a critical first step in establishing a paper trail for potential litigation. It must clearly outline the specific terms violated, the total balance due, and a strict deadline for payment. Sending this letter demonstrates a good-faith effort to resolve the dispute out of court, often motivating the borrower to settle before facing costly legal action or credit damage.

Delinquent Account Payment Demand Letter

A Delinquent Account Payment Demand Letter serves as a formal final notice before initiating legal action or credit reporting. It clearly outlines the outstanding balance, original due date, and a specific deadline for settlement. This document provides crucial evidence of your attempt to resolve the debt amicably if the case proceeds to court. To ensure effectiveness, include payment instructions and potential consequences of continued non-payment. Using a structured demand letter professionalizes the collection process, often prompting immediate response from debtors to avoid litigation or further financial penalties.

Final Warning Demand Letter Before Litigation

A Final Warning Demand Letter is the last formal notification sent to a debtor or breaching party before initiating legal action. It serves as a pre-action protocol, clearly outlining the legal basis for the claim and specifying the required remedy or payment amount. This document must include a firm deadline for compliance to demonstrate seriousness. Providing this final opportunity for settlement can save time and costs by avoiding court, while simultaneously establishing a critical evidence trail that proves your reasonable attempts to resolve the dispute through formal litigation procedures.

Unsecured Credit Default Demand Letter

An Unsecured Credit Default Demand Letter is a formal legal notice issued by a creditor when a borrower fails to repay a loan lacking collateral. This document serves as a final warning, demanding immediate payment of the outstanding balance plus accrued interest. It outlines the specific breach of contract and sets a strict deadline for resolution. Receiving this letter indicates that the creditor may soon initiate legal action or transfer the debt to a collection agency, which can severely impact your credit score and financial standing.

Bank Notice and Demand Letter for Outstanding Balance

A bank notice serves as a formal alert regarding a delinquent account. If ignored, the institution issues a demand letter, which is a final legal notification requiring immediate payment of the outstanding balance. This document specifies the total debt, applicable interest, and a strict deadline. Receiving this means the bank may initiate legal action or debt collection processes. It is crucial to respond promptly to negotiate a repayment plan or settlement to avoid severe damage to your credit score and potential litigation.

Settlement Offer and Repayment Demand Letter

A Settlement Offer is a formal proposal to resolve a debt for less than the total balance owed. In contrast, a Repayment Demand Letter is a legal notification requiring the debtor to pay the outstanding amount by a specific deadline to avoid further action. Both documents are crucial for debt resolution and legal protection. It is essential to ensure all terms are documented in writing to create a binding settlement agreement, preventing future disputes while clearly defining payment schedules, total amounts, and release of liability.

Outstanding Debt Collection Demand Letter

An Outstanding Debt Collection Demand Letter serves as a formal legal notice requesting immediate payment of an overdue balance. It is a critical step in the recovery process, establishing a paper trail for potential litigation. The document must clearly state the total amount owed, the original due date, and a specific deadline for settlement. Including dispute resolution rights is essential to comply with fair practices. By providing a final opportunity to pay before escalating to a collection agency or court, this letter helps protect your professional interests and ensures clear communication with the debtor.

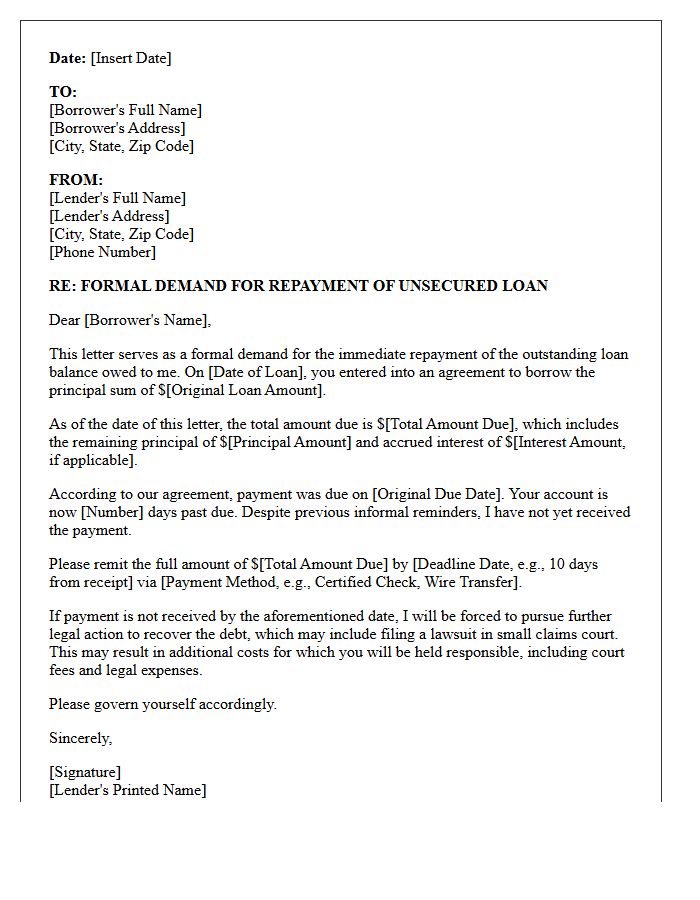

Formal Demand Letter for Unsecured Loan Repayment

A formal demand letter is a critical legal step to recover an unsecured loan. Since no collateral backs the debt, this document serves as official notice, clearly stating the outstanding balance, interest, and a specific repayment deadline. It establishes a formal paper trail, demonstrating to a court that you attempted to resolve the dispute before initiating litigation. Clearly outlining the original agreement terms and the consequences of non-payment can often prompt a settlement without costly legal action, protecting your financial interests and providing necessary evidence for future proceedings.

What is a demand letter for an unsecured personal loan default?

A demand letter is a formal written notice sent by a lender to a borrower who has failed to make payments on an unsecured personal loan. it serves as a final warning, officially documenting the default and requesting immediate payment of the outstanding balance before legal action or debt collection processes are initiated.

What key information should be included in a personal loan demand letter?

The letter should include the original loan agreement date, the current total balance (including accrued interest and late fees), the specific default date, a deadline for payment (typically 10 to 30 days), and the acceptable methods of payment to rectify the delinquency.

Can a lender sue for an unsecured loan default after sending a demand letter?

Yes. Since unsecured loans are not backed by collateral like a house or car, a lender's primary recourse is to sue the borrower for a money judgment. The demand letter is a prerequisite step that demonstrates to the court that the lender attempted to resolve the debt amicably before filing a lawsuit.

How does a demand letter affect a borrower's credit score?

While the letter itself is a private communication, the underlying default reported to credit bureaus significantly lowers a credit score. If the demand letter is ignored and the debt is sold to a collection agency or results in a court judgment, the negative impact on the borrower's credit report becomes even more severe and long-lasting.

What are the borrower's options after receiving a demand letter for a loan default?

Upon receiving a demand letter, a borrower can pay the full amount to stop further action, propose a lump-sum settlement for a lesser amount, or request a revised repayment plan. Communication at this stage is critical to prevent the lender from escalating the matter to a debt collection attorney.

Comments