A Change in Terms Notice Letter is an essential legal communication used by businesses to inform clients about modifications to existing agreements or service conditions. Providing clear, transparent updates helps maintain professional transparency and ensures regulatory compliance. Understanding how to draft these notices effectively protects your business relationships. To assist your drafting process, below are some ready to use template.

Image cover: Updating Your Terms: Professional Notice Templates and Letter Samples

Letter Samples List

- Credit Card Annual Percentage Rate Increase Notice Letter

- Overdraft Fee Policy Change Notice Letter

- Checking Account Minimum Balance Requirement Change Letter

- Online Banking Terms and Conditions Update Letter

- Installment Loan Repayment Schedule Modification Letter

- Monthly Account Maintenance Fee Introduction Letter

- Wire Transfer Limit and Fee Adjustment Letter

- Credit Card Rewards Program Benefit Modification Letter

- Dormant Account Handling Policy Change Letter

- Savings Account Withdrawal Limit Adjustment Letter

- Mortgage Escrow Account Terms Modification Letter

- Out-Of-Network ATM Fee Reimbursement Change Letter

- Business Line of Credit Covenant Update Letter

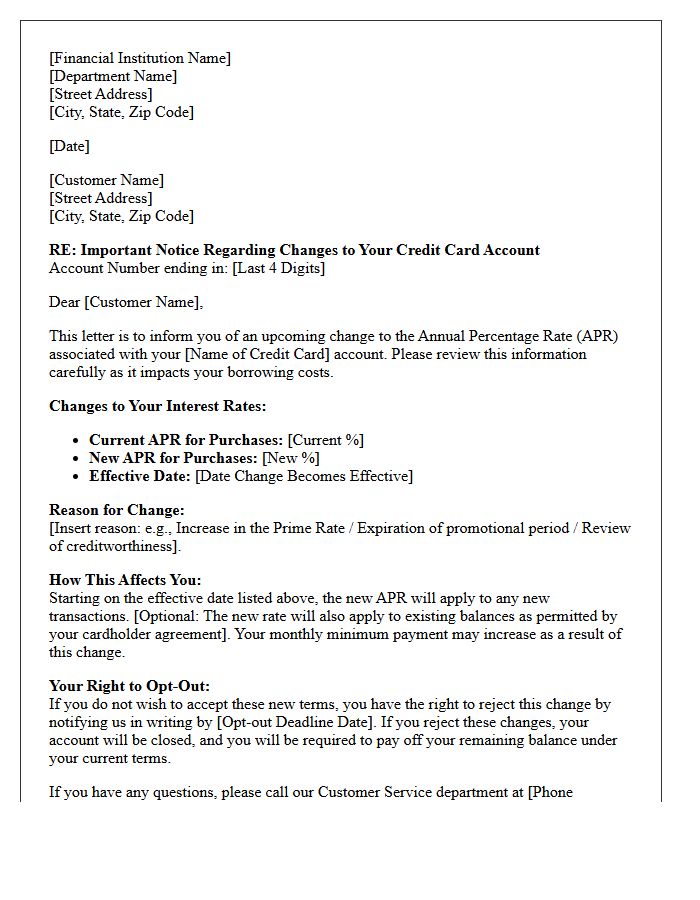

Credit Card Annual Percentage Rate Increase Notice Letter

A credit card APR Increase Notice is a legal document informing you that your interest rate is rising. Under the CARD Act, issuers must provide a 45-day advance notice before applying a higher rate to new purchases. This letter details the effective date, the new percentage, and your right to opt-out by closing the account. Always review these notices to understand how your cost of credit changes, as a higher APR significantly increases your monthly interest charges if you carry a balance.

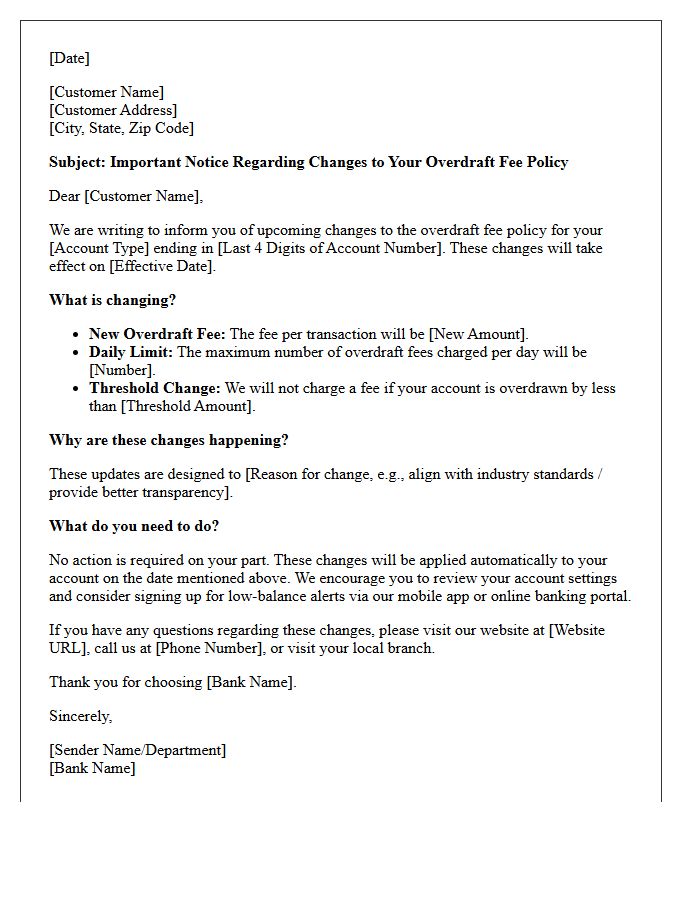

Overdraft Fee Policy Change Notice Letter

An Overdraft Fee Policy Change Notice Letter informs customers about modified terms regarding account deficits. This mandatory disclosure typically outlines updated fee structures, transaction coverage rules, and effective dates for the new policy. It is crucial to review these updates to understand how the bank handles insufficient funds and to determine if you should opt-in or opt-out of overdraft services. Staying informed helps you avoid unexpected charges and manage your personal finances more effectively in accordance with revised banking regulations.

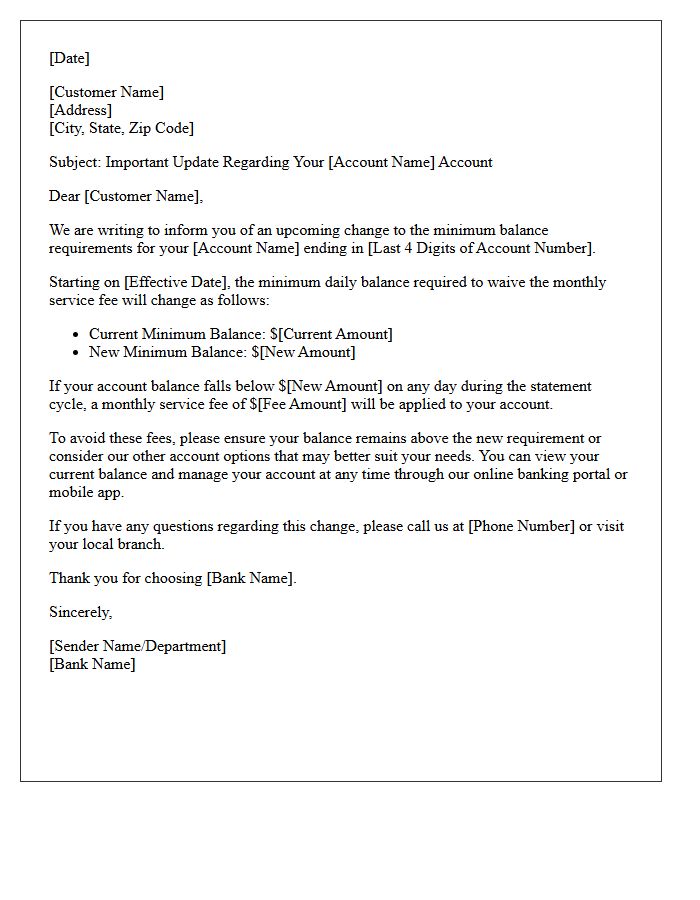

Checking Account Minimum Balance Requirement Change Letter

A Checking Account Minimum Balance Requirement Change Letter is a formal notification from your bank announcing new financial thresholds. It is crucial to review the effective date to avoid unexpected monthly maintenance fees. These updates often occur due to policy shifts or account restructuring. To maintain fee-free banking, you may need to increase your daily balance or set up qualifying direct deposits. Always compare the new terms against your current spending habits to determine if your existing account remains the most cost-effective option for your personal finances.

Online Banking Terms and Conditions Update Letter

An Online Banking Terms and Conditions Update Letter is a formal notification informing customers about legal modifications to their financial service agreement. These updates often cover critical changes to interest rates, liability for unauthorized transactions, and data privacy protocols. It is essential to review these documents promptly, as continued use of the platform typically implies automatic consent to the new terms. Pay close attention to sections regarding security obligations and fee structures to ensure your financial activities remain protected and compliant with the bank's latest regulatory standards.

Installment Loan Repayment Schedule Modification Letter

An Installment Loan Repayment Schedule Modification Letter is a formal request to adjust your current billing structure due to financial hardship. This document proposes new terms, such as extended durations or lower monthly payments, to avoid default. It must include your account details, the specific reason for the adjustment, and a clear repayment plan. If the lender approves, this modification helps protect your credit score by establishing a manageable legal agreement that supersedes your original contract, ensuring long-term financial stability for both the borrower and the financial institution.

Monthly Account Maintenance Fee Introduction Letter

A Monthly Account Maintenance Fee Introduction Letter serves as a formal notification to customers regarding upcoming service charges. It is essential to clearly explain the fee structure, the specific effective date, and the reasons behind the price adjustment, such as enhanced security or better features. To maintain transparency, the letter should outline waiver requirements, allowing clients to avoid costs by meeting minimum balance criteria. This clear communication helps manage customer expectations, ensures regulatory compliance, and minimizes potential disputes while reinforcing the value of the ongoing professional relationship.

Wire Transfer Limit and Fee Adjustment Letter

A Wire Transfer Limit and Fee Adjustment Letter is a formal notification from a financial institution regarding changes to your transaction capabilities. This document outlines updated daily or monthly caps on electronic fund transfers and any increases in service charges. It is essential to review these adjustments to ensure your liquidity management remains uninterrupted. Pay close attention to the effective date to avoid unexpected processing delays or higher operational costs. Understanding these modifications helps you maintain accurate financial records and evaluate if your current banking plan still meets your specific transfer requirements.

Credit Card Rewards Program Benefit Modification Letter

A Credit Card Rewards Program Benefit Modification Letter is a formal notification informing cardholders of upcoming changes to their terms of service. Banks use these letters to announce adjustments in point values, earning rates, or redemption options. It is crucial to review these updates immediately, as they often involve a reduction in benefits or the expiration of specific perks. Understanding these policy shifts allows you to optimize your spending strategy or redeem existing rewards before they lose value due to new program limitations.

Dormant Account Handling Policy Change Letter

A Dormant Account Handling Policy Change Letter notifies customers about updated procedures for inactive accounts. It is crucial to review the specific timeline for dormancy to prevent your funds from being classified as unclaimed property. This document outlines how to reactivate your account through simple actions like logging in or making a transaction. Ignoring this notice may result in your balance being transferred to the state treasury via escheatment laws. Always verify the sender to ensure the communication is legitimate and protect your financial assets from permanent closure.

Savings Account Withdrawal Limit Adjustment Letter

A Savings Account Withdrawal Limit Adjustment Letter is a formal notification from a financial institution regarding changes to your monthly transaction limits. Following federal regulatory shifts, banks may now increase or remove the previous six-per-month cap on convenience transfers. This document details updated fees, specific account restrictions, and the effective date of these policy adjustments. Reviewing this letter is essential to understand how liquidity access and potential penalties impact your personal financial management and long-term savings goals.

Mortgage Escrow Account Terms Modification Letter

A Mortgage Escrow Account Terms Modification Letter is a formal notice sent by a lender to adjust your monthly payments. This document typically reflects changes in property taxes or homeowners insurance premiums identified during an annual escrow analysis. It is crucial to review these updates immediately to understand your new total monthly mortgage obligation and any potential escrow shortages or surpluses. Promptly acknowledging this modification ensures your loan remains in good standing and prevents unexpected financial deficits or gaps in essential insurance coverage.

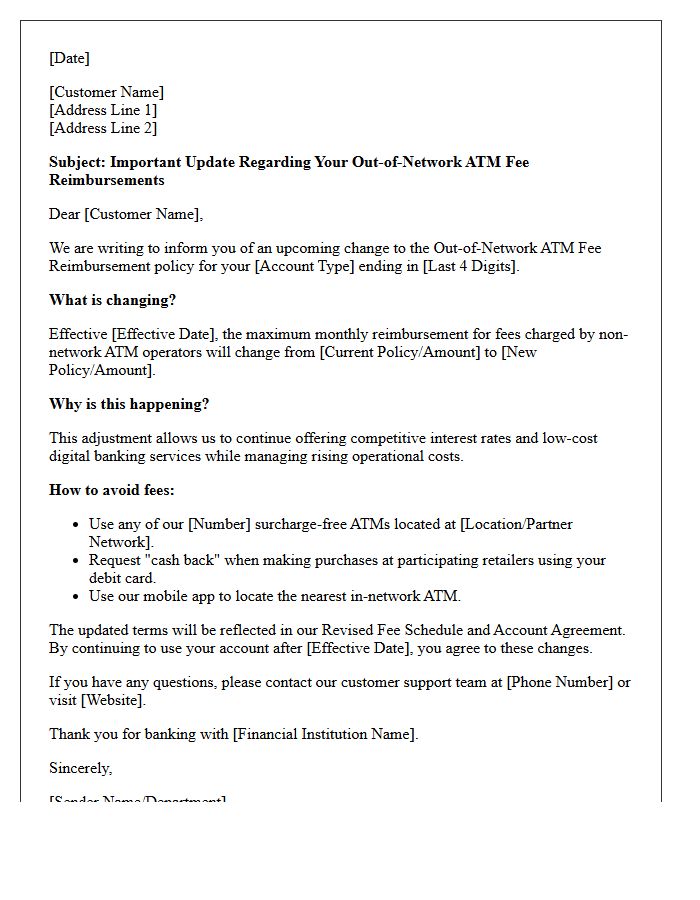

Out-Of-Network ATM Fee Reimbursement Change Letter

An Out-Of-Network ATM Fee Reimbursement Change Letter is a formal notice from your bank regarding updates to their refund policy. It typically outlines new monthly caps on reimbursements or changes to eligibility requirements for domestic and international withdrawals. Reviewing this document is essential to avoid unexpected surcharges when using third-party machines. If your financial institution is reducing these benefits, you may need to adjust your cash access habits or maintain a higher account balance to qualify for continued fee waivers.

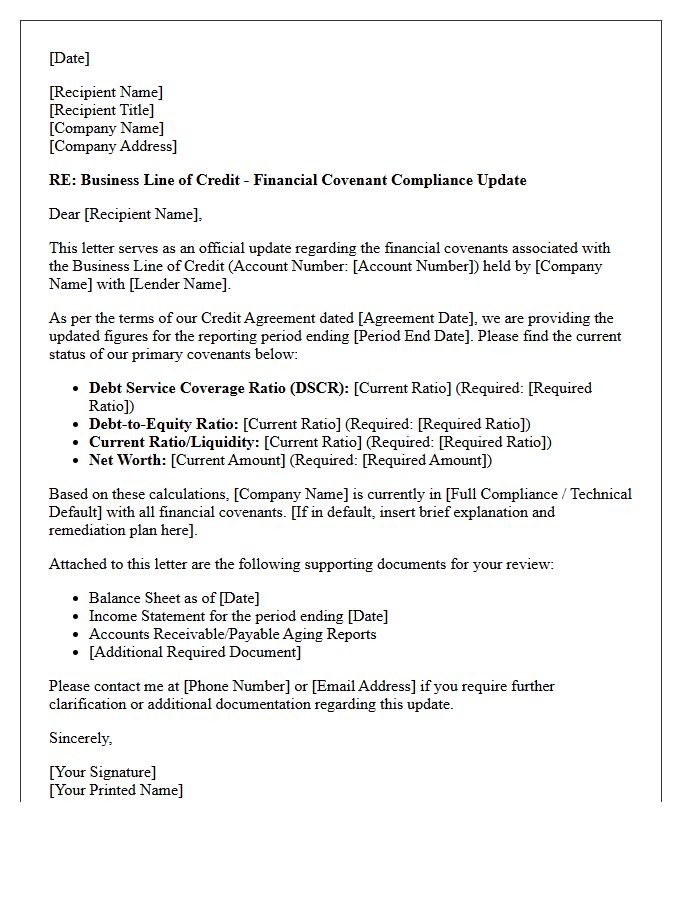

Business Line of Credit Covenant Update Letter

A Business Line of Credit Covenant Update Letter is a formal notification issued by a lender to modify or clarify specific financial compliance requirements. This document ensures the borrower remains in good standing by adjusting benchmarks like debt-to-equity ratios or liquidity thresholds. Understanding these updates is critical, as failing to meet revised financial covenants can trigger a technical default, leading to reduced credit access or accelerated repayment demands. Always review these amendments carefully to maintain operational flexibility and ensure continuous access to your business funding.

What is a Change in Terms Notice letter?

A Change in Terms Notice is a formal document sent by a service provider or financial institution to inform customers of modifications to their existing contract, such as adjusted interest rates, updated fees, or revised privacy policies.

How much advance notice is required for a change in terms?

Under federal regulations like the Truth in Lending Act (Regulation Z), most financial institutions are required to provide a written notice at least 45 days before significant changes to account terms take effect.

Does a Change in Terms Notice require a signature to be valid?

Generally, no. Most agreements include a clause stating that continued use of the service or account after the effective date constitutes acceptance of the new terms outlined in the notice.

What should be included in a legally compliant Change in Terms Notice?

A compliant notice must clearly state the specific terms being modified, the effective date of the changes, any actions the customer needs to take, and information regarding the right to opt-out or close the account.

Can I reject the changes outlined in a Change in Terms Notice?

Yes, consumers typically have the right to reject changes; however, doing so usually results in the termination of the service or the closing of the account, often requiring the balance to be paid under the original terms.

Comments