A Notice of Negative Information Furnished is a formal notification from a creditor stating they have reported late payments or defaults to credit bureaus. Receiving this letter allows you to dispute inaccuracies before your credit score is severely impacted. Understanding your rights under the Fair Credit Reporting Act is essential for financial health. To assist you, below are some ready to use template.

Image cover: Responding to Negative Information Notices: Templates and Best Practices

Letter Samples List

- Notice of Negative Information Furnished Regarding Late Mortgage Payment Letter

- Notice of Negative Information Furnished Regarding Auto Loan Default Letter

- Notice of Negative Information Furnished Regarding Overdrawn Checking Account Letter

- Notice of Negative Information Furnished Regarding Credit Card Charge-Off Letter

- Notice of Negative Information Furnished Regarding Personal Loan Delinquency Letter

- Notice of Negative Information Furnished Regarding Unpaid Overdraft Fees Letter

- Notice of Negative Information Furnished Regarding Repossessed Vehicle Deficiency Balance Letter

- Notice of Negative Information Furnished Regarding Foreclosed Property Deficit Letter

- Notice of Negative Information Furnished Regarding Student Loan Nonpayment Letter

- Notice of Negative Information Furnished Regarding Small Business Loan Default Letter

- Notice of Negative Information Furnished Regarding Unsecured Credit Account Delinquency Letter

- Notice of Negative Information Furnished Regarding Home Equity Line of Credit Nonpayment Letter

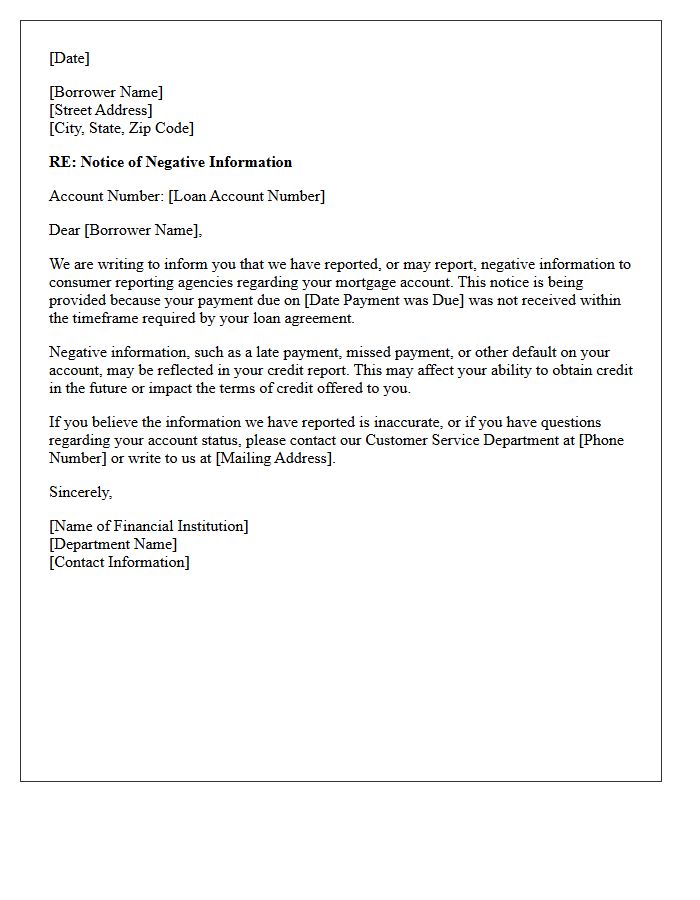

Notice of Negative Information Furnished Regarding Late Mortgage Payment Letter

A Notice of Negative Information is a formal legal warning issued by lenders before reporting a late mortgage payment to national credit bureaus. Under the Fair Credit Reporting Act, creditors must notify you either before or within thirty days of submitting adverse data. This letter is critical because it signals an imminent drop in your credit score, which can impact future loan eligibility and interest rates. Reviewing this notice immediately allows you to verify the debt's accuracy, dispute errors, or arrange a payment plan to mitigate long-term financial damage.

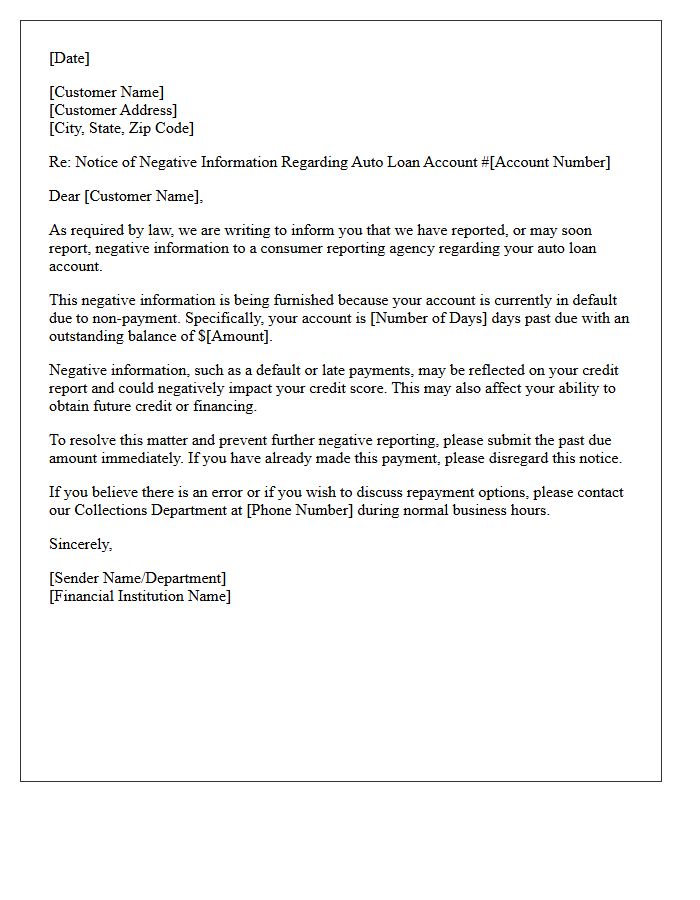

Notice of Negative Information Furnished Regarding Auto Loan Default Letter

A Notice of Negative Information is a formal alert sent by lenders before or shortly after reporting a default or late payment to credit bureaus. Regarding an auto loan, this letter signifies that your delinquency will severely damage your credit score for up to seven years. It serves as a final opportunity to rectify the balance or dispute inaccuracies. Receiving this notice is a critical warning to take immediate action to avoid repossession and long-term financial consequences associated with negative reporting on your consumer credit file.

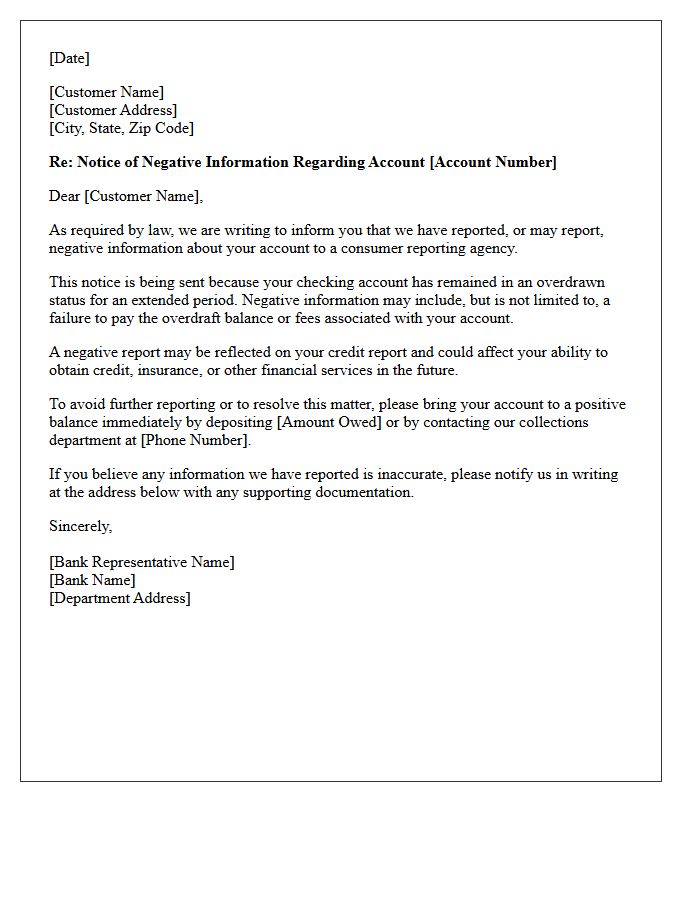

Notice of Negative Information Furnished Regarding Overdrawn Checking Account Letter

A Notice of Negative Information warns consumers that a financial institution intends to report delinquent account activity to major credit bureaus. This letter is a legal requirement under the Fair Credit Reporting Act before a bank can damage your credit score due to an overdrawn checking account. Receiving this notice provides a final opportunity to settle the outstanding balance and avoid long-term negative marks on your credit report. Acting quickly can prevent collection actions and preserve your future ability to open new banking accounts or secure favorable loan terms.

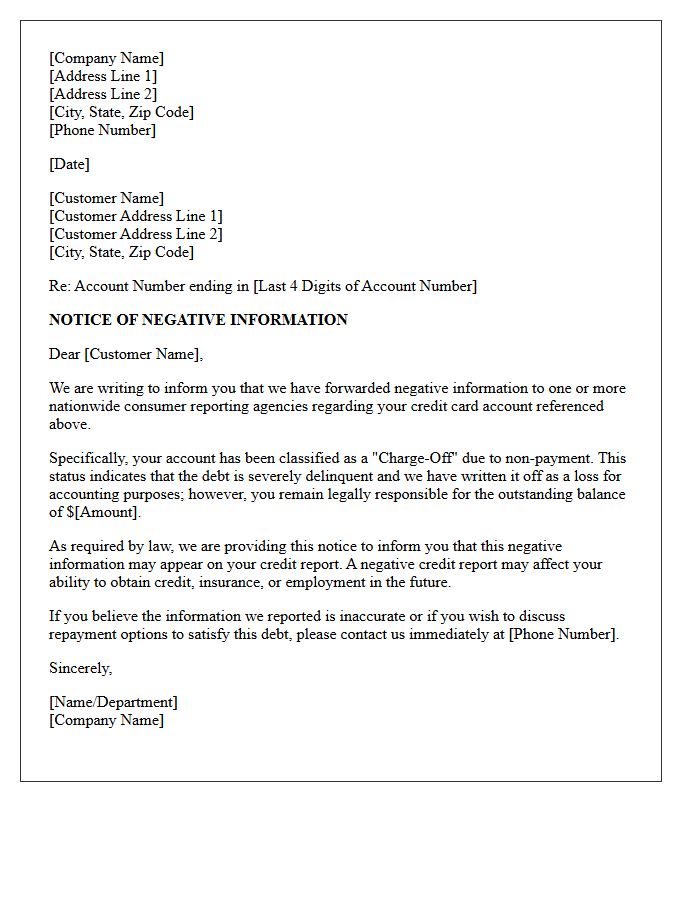

Notice of Negative Information Furnished Regarding Credit Card Charge-Off Letter

A Notice of Negative Information is a formal alert from a lender stating they have reported late payments or a credit card charge-off to credit bureaus. This notification is a legal requirement under the Fair Credit Reporting Act. Receiving this letter means your account is deemed uncollectible, significantly lowering your credit score and affecting future loan eligibility. It is crucial to verify the accuracy of the charge-off status and understand that you still owe the debt unless it is legally settled or discharged.

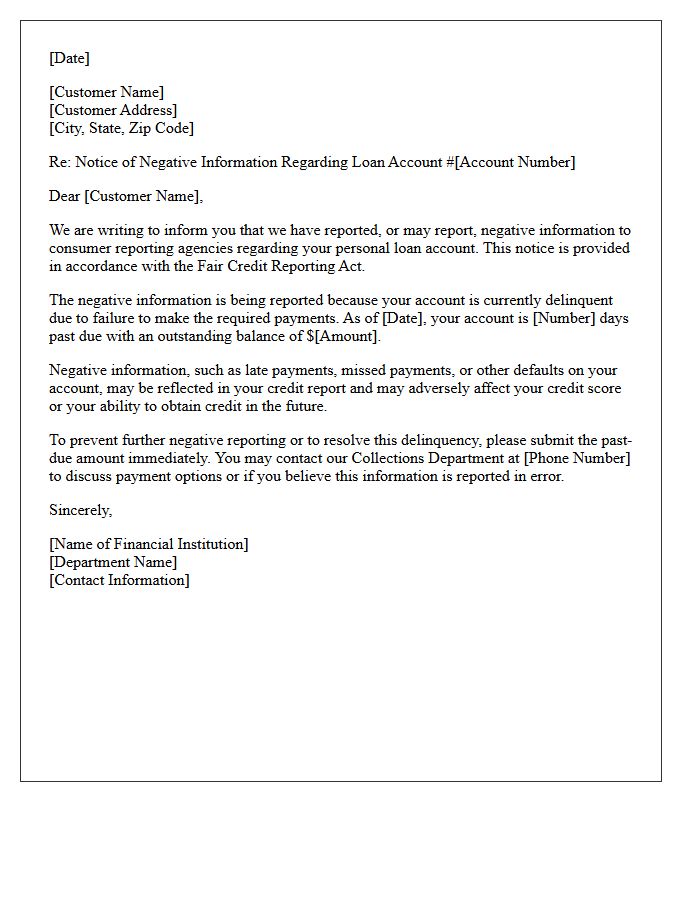

Notice of Negative Information Furnished Regarding Personal Loan Delinquency Letter

A Notice of Negative Information is a critical legal alert sent by lenders when you fall behind on personal loan payments. It signifies that your delinquency will be reported to credit bureaus, severely impacting your credit score. This notification serves as a final warning, offering a brief window to resolve the default before your financial history is damaged. Receiving this letter means the lender is fulfilling their legal obligation under the Fair Credit Reporting Act to inform you of the negative credit reporting consequences of non-payment.

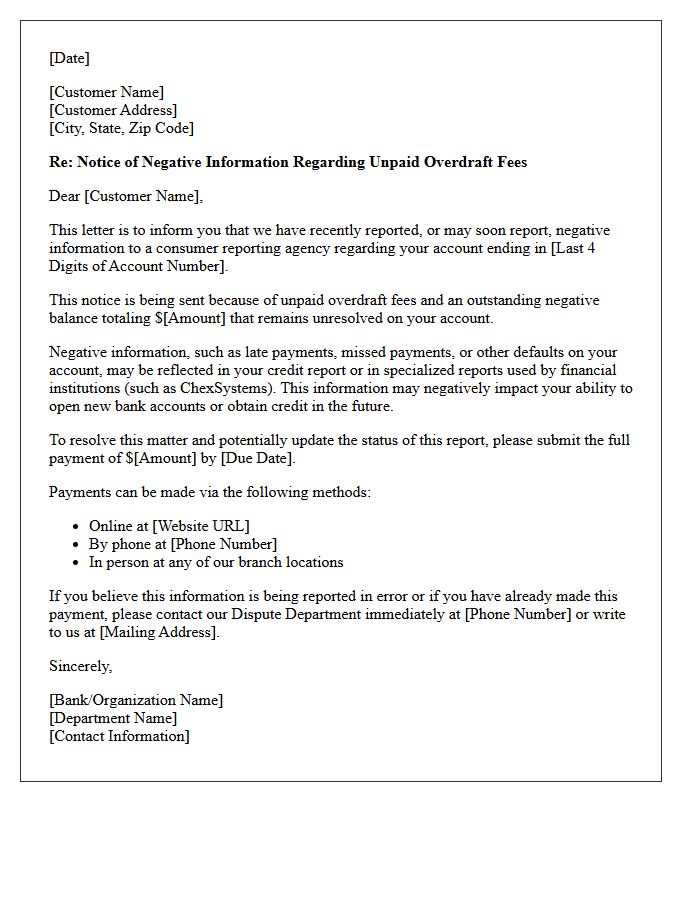

Notice of Negative Information Furnished Regarding Unpaid Overdraft Fees Letter

Receiving a Notice of Negative Information is a critical warning that your financial institution intends to report your unpaid overdraft fees to a credit bureau or specialty agency like ChexSystems. This notice is a legal requirement under the Fair Credit Reporting Act before the delinquency impacts your credit score or ability to open future bank accounts. To protect your financial standing, you must resolve the outstanding balance immediately. Timely payment can prevent long-term negative remarks from appearing on your permanent consumer reports and affecting your future borrowing power.

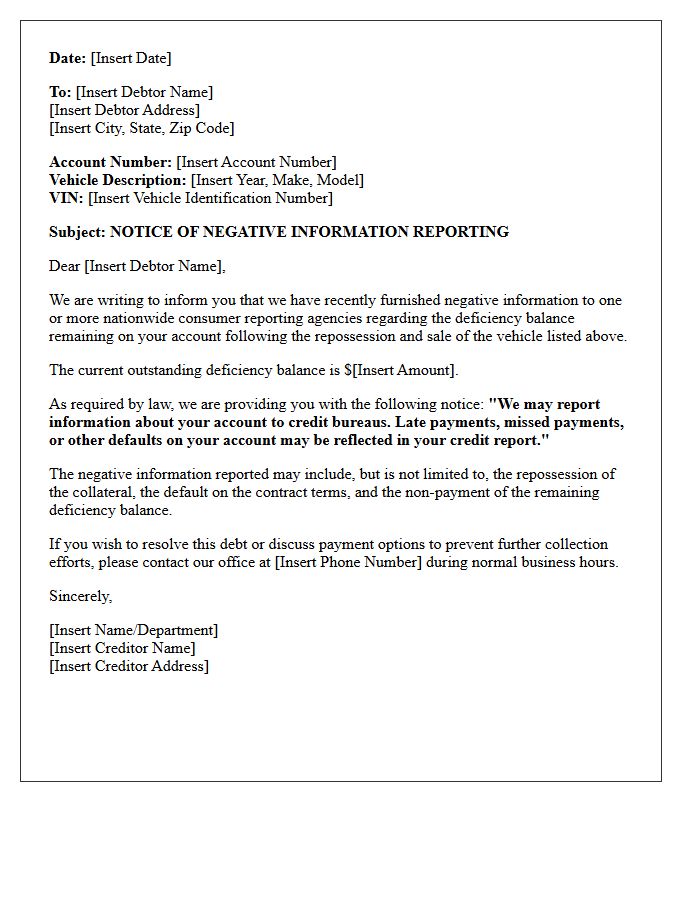

Notice of Negative Information Furnished Regarding Repossessed Vehicle Deficiency Balance Letter

A Notice of Negative Information warns that your lender intends to report a deficiency balance to credit bureaus following a vehicle repossession. This occurs when the car's auction price fails to cover your remaining loan amount. Receiving this letter is a critical alert that your credit score will be negatively impacted by a collection status or charge-off. You have a legal right to receive this disclosure, allowing you a final opportunity to dispute the debt or negotiate a settlement before long-term financial damage occurs on your credit report.

Notice of Negative Information Furnished Regarding Foreclosed Property Deficit Letter

A Notice of Negative Information warns that a deficiency balance remains after a foreclosure sale. When the property sells for less than the total debt, the lender may report this unpaid deficit to major credit bureaus. Receiving this letter indicates a significant drop in your credit score and potential legal action for debt recovery. It is critical to review the foreclosed property deficit amount for accuracy and understand your rights under the Fair Credit Reporting Act to dispute errors or negotiate a settlement to prevent long-term financial damage.

Notice of Negative Information Furnished Regarding Student Loan Nonpayment Letter

A Notice of Negative Information warns that your student loan nonpayment will be reported to consumer reporting agencies. This formal letter is a final opportunity to resolve delinquency before your credit score is adversely affected. Creditors are legally required to notify you before or shortly after sharing negative data with bureaus. To protect your financial future, you must act quickly by exploring repayment options, deferment, or forbearance to prevent a long-term credit rating decline that can impact housing, employment, and future borrowing eligibility.

Notice of Negative Information Furnished Regarding Small Business Loan Default Letter

A Notice of Negative Information warns that a small business loan default will be reported to credit bureaus. Receiving this letter is critical because it signals imminent damage to your commercial credit score, potentially hindering future financing and vendor terms. Federal law often requires lenders to provide this notification before or shortly after reporting delinquencies. To mitigate the impact, business owners should immediately dispute inaccuracies or negotiate a repayment plan to prevent long-term financial repercussions and preserve their professional reputation.

Notice of Negative Information Furnished Regarding Unsecured Credit Account Delinquency Letter

A Notice of Negative Information is a formal warning issued by lenders before reporting a late payment to credit bureaus. This letter informs you that your delinquency on an unsecured credit account, such as a credit card or personal loan, will negatively impact your credit score. Receiving this notice provides a final opportunity to settle the past-due balance and avoid long-term financial damage. It is legally required under the Fair Credit Reporting Act to ensure consumers are aware of impending adverse reporting that affects future borrowing eligibility and interest rates.

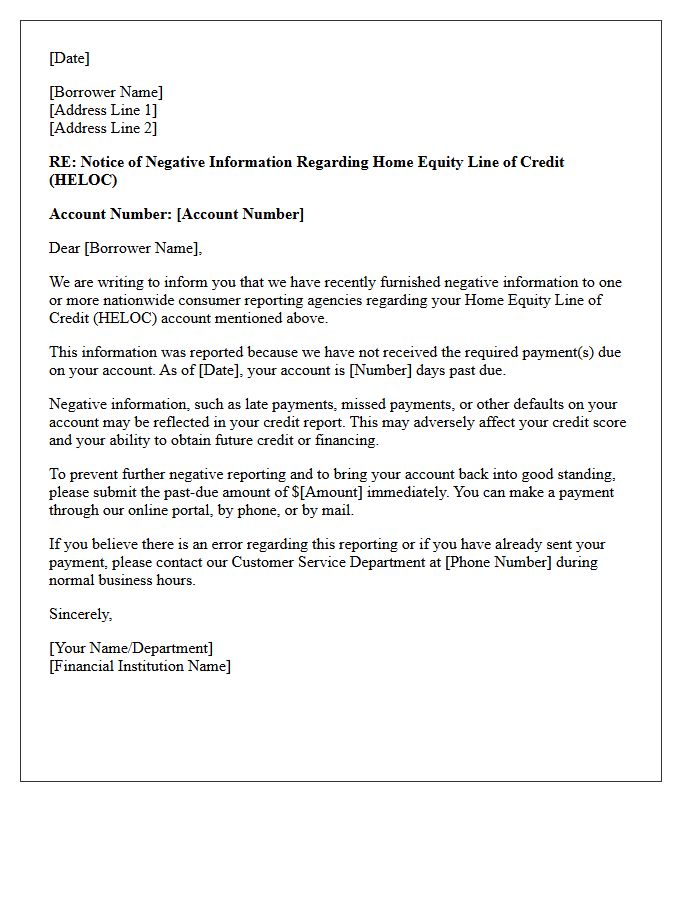

Notice of Negative Information Furnished Regarding Home Equity Line of Credit Nonpayment Letter

A Notice of Negative Information warns that nonpayment of your Home Equity Line of Credit (HELOC) will be reported to national credit bureaus. Receiving this letter indicates that a missed payment is about to damage your credit score significantly. This formal notice is a legal requirement before lenders submit adverse data, providing a final window to resolve the delinquency. Protecting your credit standing is vital, as a recorded default can hinder future loan approvals and increase interest rates. Always contact your lender immediately to discuss repayment options or hardship programs.

What is a Notice of Negative Information Furnished letter?

A Notice of Negative Information Furnished is a formal disclosure sent by a financial institution or creditor informing a consumer that they have reported, or may report, unfavorable information such as late payments or defaults to a credit reporting agency.

Why did I receive a Notice of Negative Information?

You received this notice because a creditor has determined that your account activity-typically a missed or late payment-meets the criteria to be reported to credit bureaus, which may negatively impact your credit score.

When must a creditor send a Notice of Negative Information Furnished letter?

Under the Fair Credit Reporting Act (FCRA), financial institutions must provide this notice either before or within 30 days after reporting the negative data to a credit bureau to ensure the consumer is aware of the reporting action.

Does receiving this notice mean my credit score has already dropped?

Not necessarily. Some creditors send a "pre-reporting" notice to warn you that negative information will be sent if the account is not brought current. However, if the notice states information has already been furnished, your credit score may have already been affected.

How should I respond to a Notice of Negative Information Furnished?

You should immediately verify the accuracy of the claim. if the information is incorrect, file a formal dispute with both the creditor and the credit bureaus. If the information is accurate, contact the creditor to negotiate a payment plan or a "pay for delete" agreement to mitigate further credit damage.

Comments