A Notice of Right to Rescind is a critical consumer protection document that allows borrowers to cancel certain home equity loans or refinances within three business days. Understanding this legal safeguard ensures you can withdraw from a credit transaction without financial penalty. To help you draft this document accurately, below are some ready to use templates.

Image cover: Mastering the Notice of Right to Rescind: Essential Letter Samples and Templates

Letter Samples List

- Notice of Right to Rescind Mortgage Refinancing Letter

- Home Equity Line of Credit Right to Rescind Letter

- Notice of Right to Cancel Loan Transaction Letter

- Truth in Lending Act Right to Rescind Letter

- Confirmation of Voluntary Waiver of Right to Rescind Letter

- Notice of Right to Rescind Bridge Loan Letter

- Second Mortgage Notice of Right to Rescind Letter

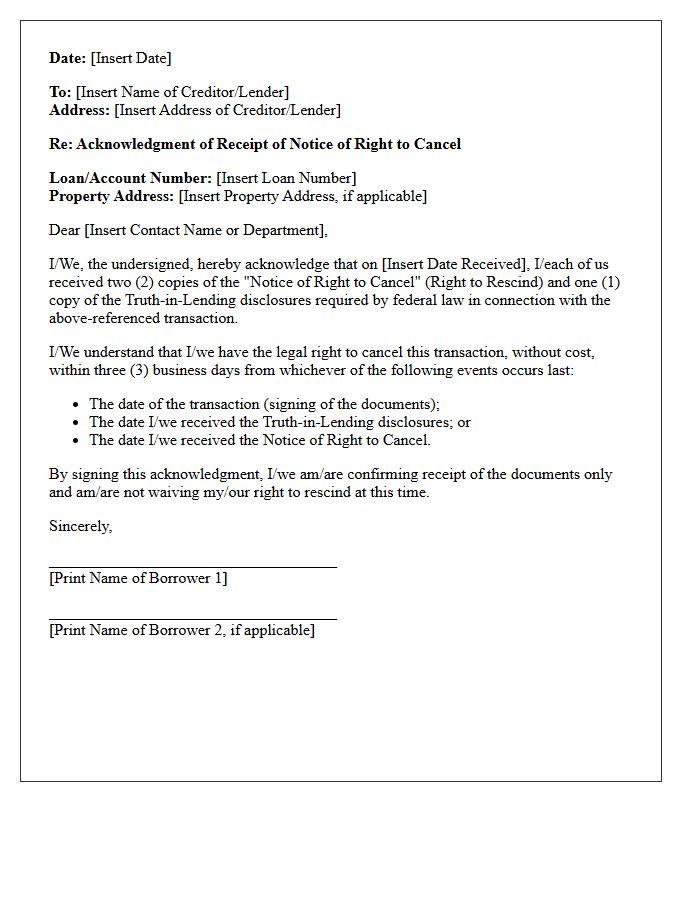

- Acknowledgment of Receipt of Right to Rescind Letter

- Rescission of Closed End Credit Transaction Letter

- Notice of Right to Rescind Reverse Mortgage Letter

- Regulation Z Right to Rescind Disclosure Letter

- Notice of Right to Rescind Primary Residence Refinance Letter

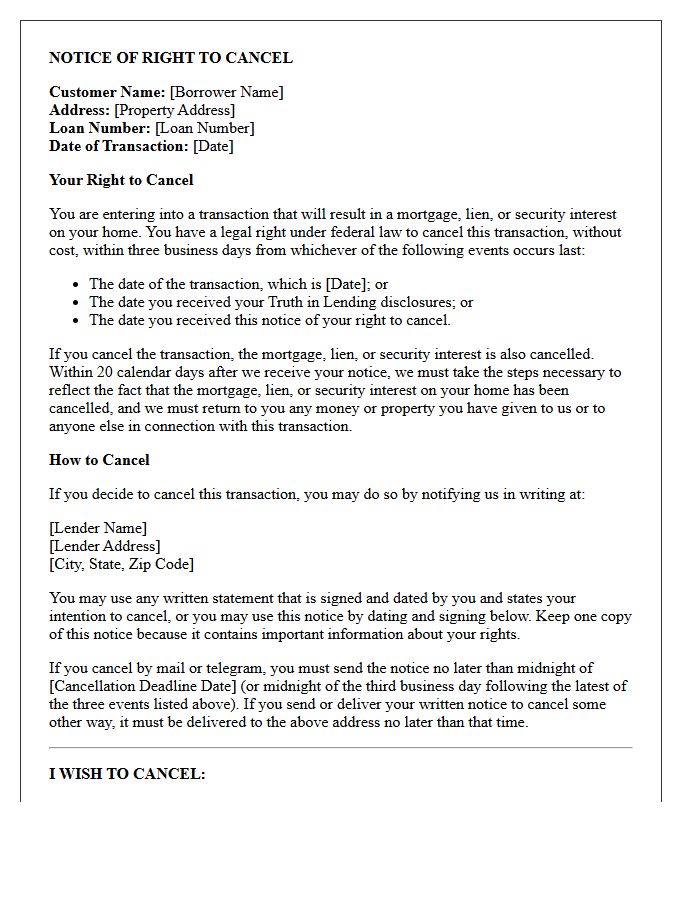

Notice of Right to Rescind Mortgage Refinancing Letter

The Notice of Right to Rescind is a critical consumer protection under the Truth in Lending Act. It provides homeowners a three-day cooling-off period to cancel a mortgage refinancing contract without penalty. This right applies only to primary residences and begins after signing the closing documents, receiving the notice, and reviewing the Truth in Lending disclosure. If the lender fails to provide accurate disclosures or the required notice, the rescission period may extend up to three years. Exercising this right voids the security interest and entitles you to a refund of all fees.

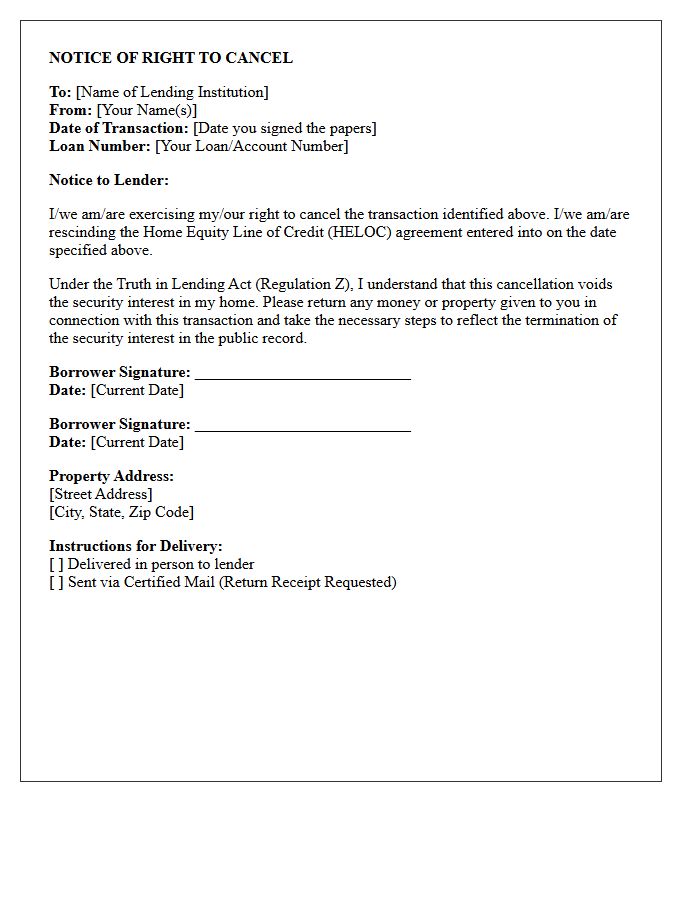

Home Equity Line of Credit Right to Rescind Letter

The Right to Rescind is a federal protection under the Truth in Lending Act. It allows homeowners to cancel a Home Equity Line of Credit (HELOC) within three business days of signing the contract. To exercise this right, you must provide a written Rescind Letter to the lender before the midnight deadline. This "cooling-off" period ensures you are not pressured into debt secured by your primary residence. Once validly rescinded, the lender must release any claim on your home and refund all closing fees collected during the application process.

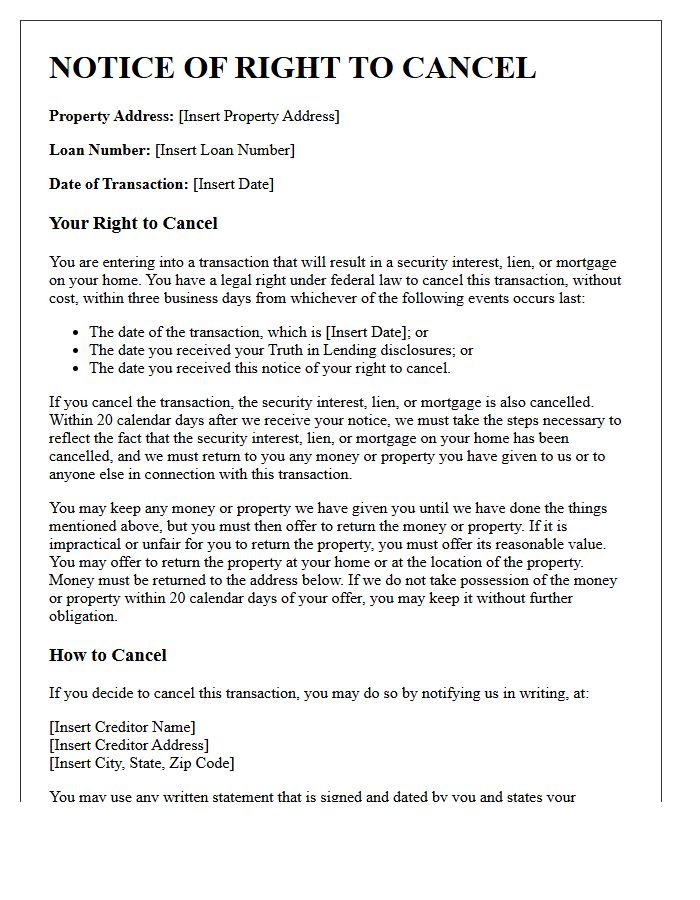

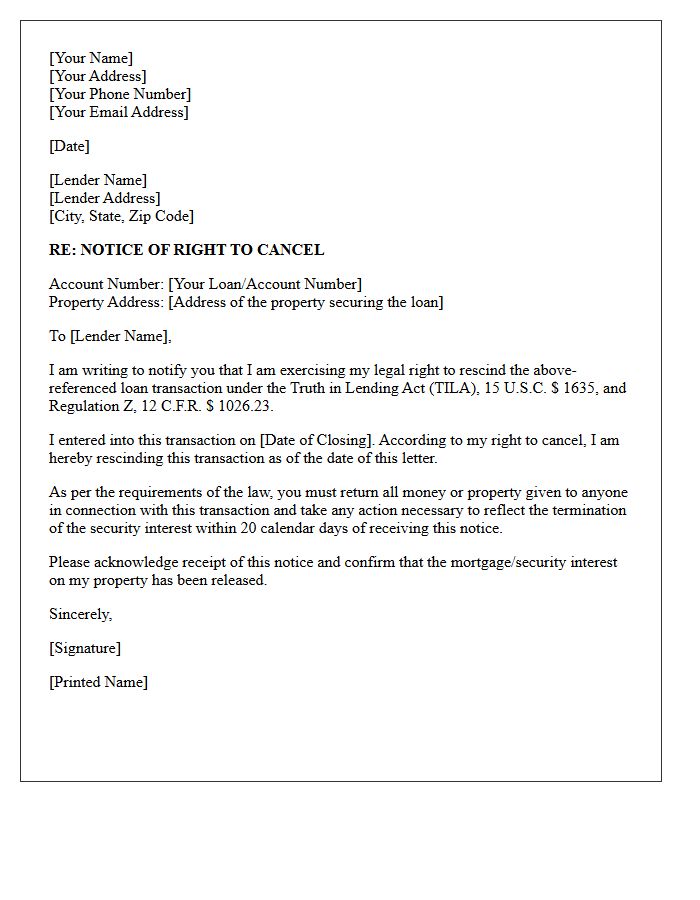

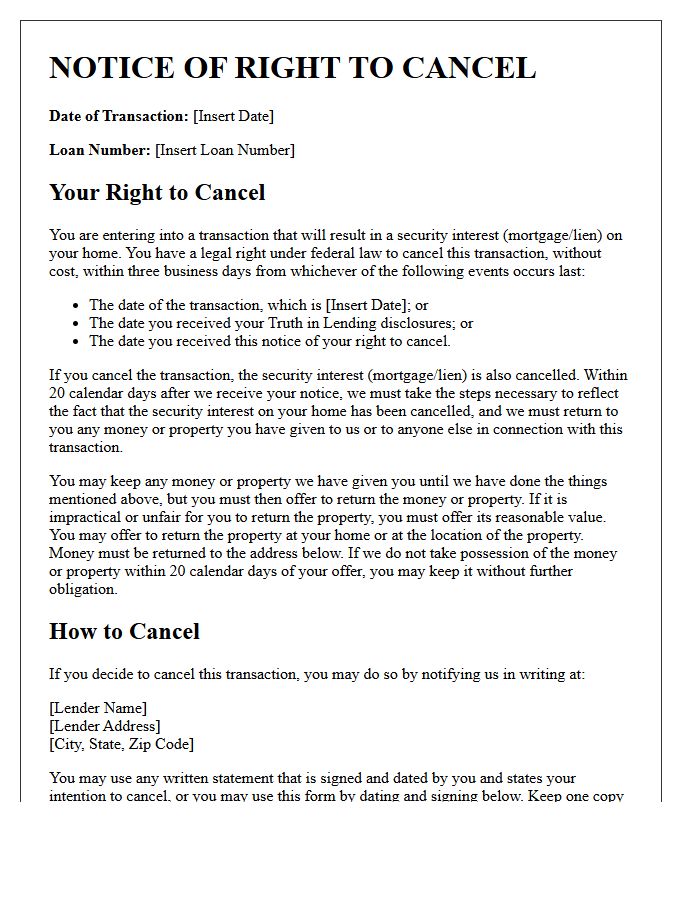

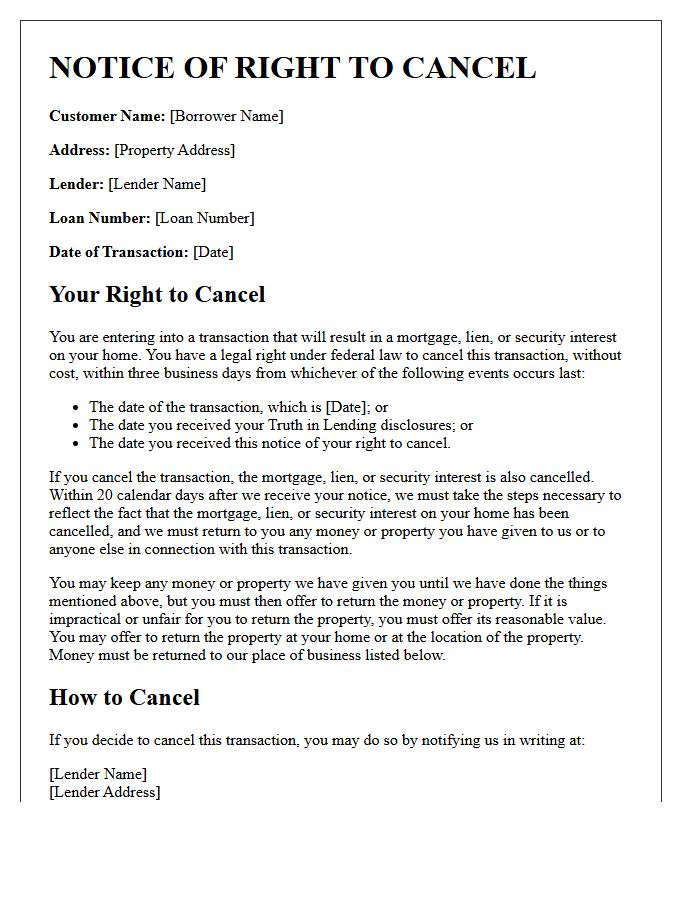

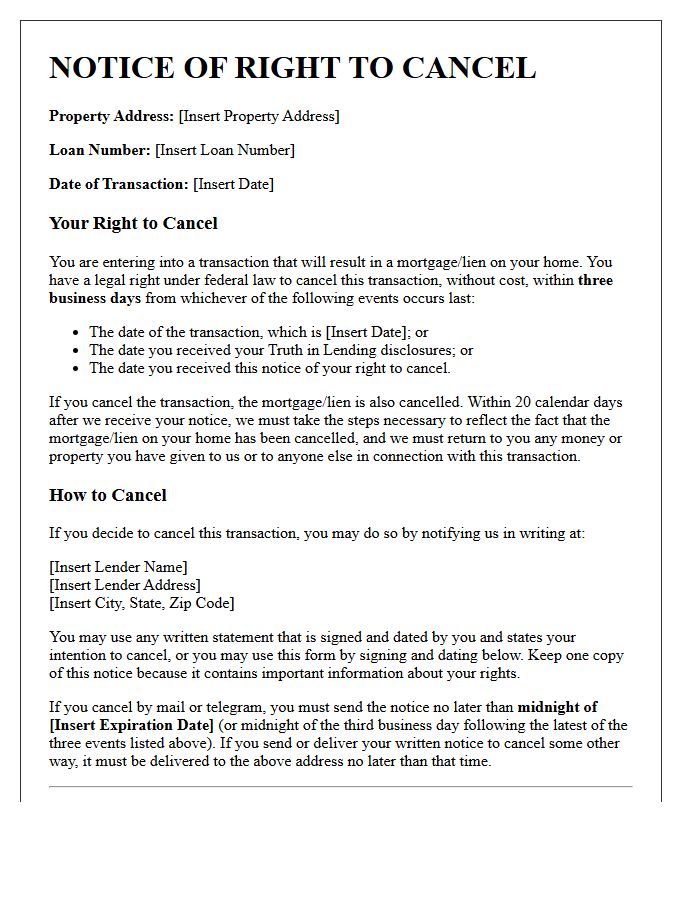

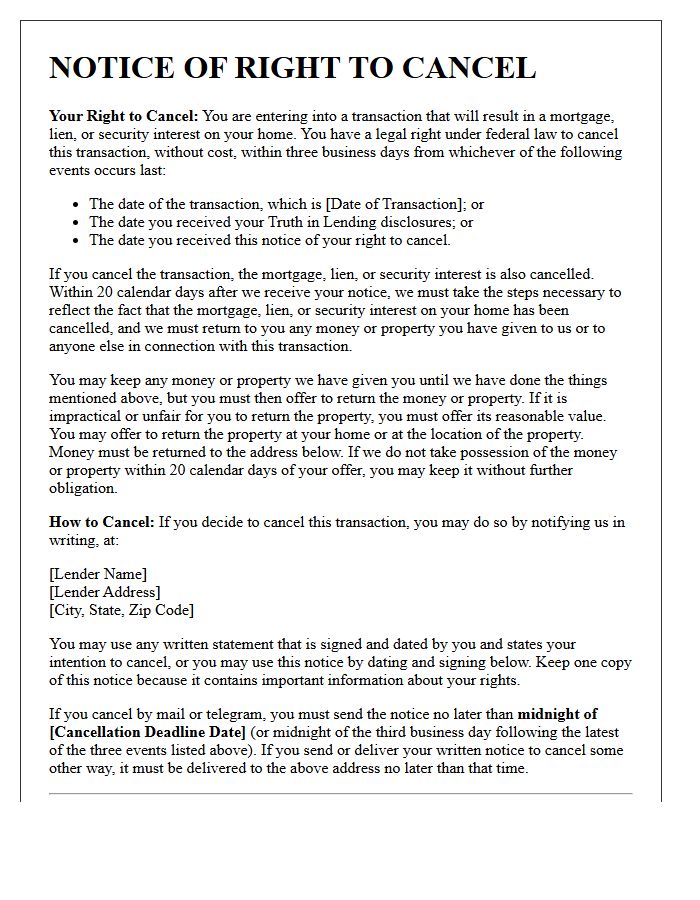

Notice of Right to Cancel Loan Transaction Letter

A Notice of Right to Cancel is a critical consumer protection document in mortgage refinancing or home equity lines of credit. It grants borrowers a three-day rescission period to void the loan agreement without financial penalty. This cooling-off period begins only after you receive the notice, the Truth in Lending disclosures, and sign the contract. To exercise this right, you must provide written notification by midnight of the third business day. Understanding this legal right ensures homeowners can withdraw from unfavorable terms before the loan funds are disbursed.

Truth in Lending Act Right to Rescind Letter

The Right to Rescind is a powerful consumer protection under the Truth in Lending Act. It allows homeowners to cancel certain mortgage-related loans within three business days of signing without penalty. This cooling-off period applies to home equity lines of credit and refinances on a primary residence, but not original purchase mortgages. To exercise this right, you must submit a formal rescission letter to the lender before the deadline. This ensures the loan agreement is voided and any fees paid are fully refunded, protecting your home equity from predatory lending practices.

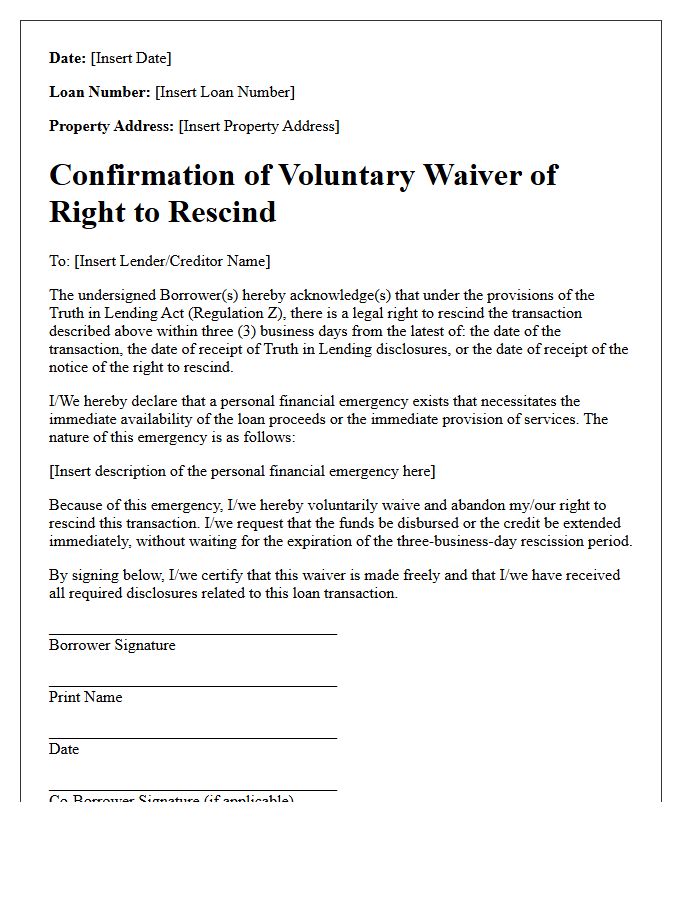

Confirmation of Voluntary Waiver of Right to Rescind Letter

A Confirmation of Voluntary Waiver of Right to Rescind is a legal document used in refinancing or home equity lending. By signing this letter, the borrower intentionally forfeits their federal Truth in Lending Act (TILA) right to cancel the loan agreement within the standard three-day cooling-off period. This action is typically permitted only during a bona fide personal financial emergency to expedite the immediate disbursement of funds. It serves as formal evidence that the consumer voluntarily waived their consumer protection rights to meet urgent financial obligations without delay.

Notice of Right to Rescind Bridge Loan Letter

A Notice of Right to Rescind is a critical document for homeowners securing a bridge loan against their primary residence. Under the Truth in Lending Act, borrowers typically have a three-day cooling-off period to cancel the agreement without penalty. This right ensures you can back out if the terms are unfavorable. It is essential to sign and return the rescission form within the specified timeframe if you choose to void the loan. Failure to receive this notice can legally extend your cancellation rights for up to three years.

Second Mortgage Notice of Right to Rescind Letter

A Second Mortgage Notice of Right to Rescind is a critical consumer protection under the Truth in Lending Act. It grants homeowners a three-day cooling-off period to cancel a home equity loan or refinance without penalty. This right applies only to primary residences, not investment properties. If the lender fails to provide this notice or accurate disclosures, the rescission period may legally extend up to three years. Homeowners must submit a written cancellation letter before the deadline to void the security interest and recover all paid fees.

Acknowledgment of Receipt of Right to Rescind Letter

The Acknowledgment of Receipt of Right to Rescind Letter serves as formal proof that a borrower was legally notified of their three-day cancellation period. Under the Truth in Lending Act, homeowners have the right to cancel certain loan contracts without penalty. Signing this document confirms you received notice of this protection and understands the rescission deadline. It is critical for lenders to maintain compliance and ensure the legal validity of the mortgage or refinancing agreement before funds are disbursed to the borrower.

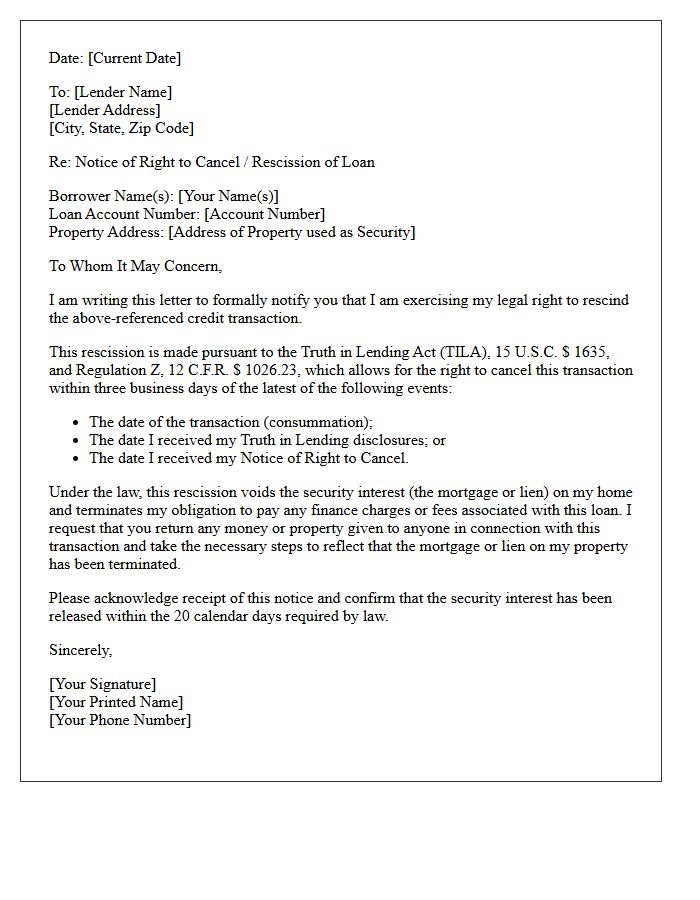

Rescission of Closed End Credit Transaction Letter

A Rescission of Closed End Credit Transaction Letter is a formal notice used to exercise the Right of Rescission under the Truth in Lending Act. Borrowers have a three-day cooling-off period to cancel certain home-secured loans without penalty. To be legally effective, this written notice must be delivered to the lender within the specified timeframe. Once rescinded, the security interest becomes void, and the creditor must return all fees and finance charges paid by the consumer, restoring both parties to their original financial positions.

Notice of Right to Rescind Reverse Mortgage Letter

The Notice of Right to Rescind is a critical consumer protection document in a reverse mortgage. It grants borrowers a legal three-day cooling-off period to cancel the loan agreement without financial penalty. This window begins once the contract is signed, the disclosure is received, and two copies of the notice are provided. To exercise this right, you must deliver written notification to the lender before the midnight deadline. This ensures borrowers have a final opportunity to reconsider the financial commitment before the loan funds are disbursed.

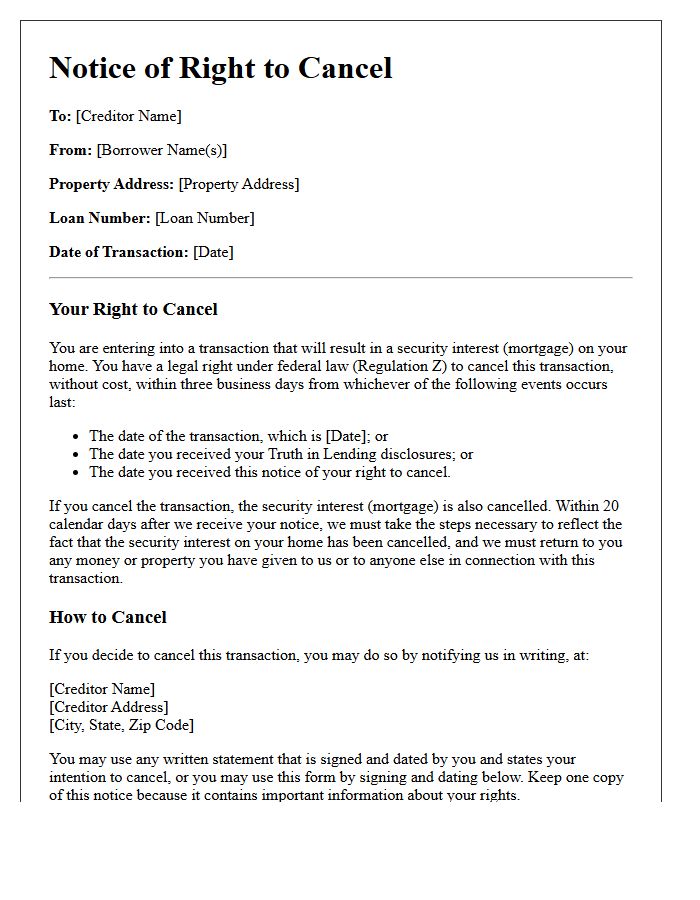

Regulation Z Right to Rescind Disclosure Letter

The Regulation Z Right to Rescind Disclosure Letter is a critical consumer protection under the Truth in Lending Act. It grants homeowners a three-day cooling-off period to cancel certain home equity loans or refinances without penalty. Lenders must provide two copies of this notice to each borrower; failure to do so can legally extend the rescission period for up to three years. This right applies only to principal residences and ensures borrowers have time to reconsider high-stakes financial commitments before their home is used as collateral.

Notice of Right to Rescind Primary Residence Refinance Letter

A Notice of Right to Rescind is a critical consumer protection under the Truth in Lending Act. When you refinance your primary residence, federal law grants you a three-day cooling-off period to cancel the loan agreement without penalty. This right ensures homeowners can back out if they reconsider the terms. To exercise this, you must provide written notice by midnight of the third business day. Note that this right typically applies only to refinancing with a different lender, not to new home purchases or investment properties.

What is a Notice of Right to Rescind?

A Notice of Right to Rescind is a legal document required by the Truth in Lending Act (TILA) that allows borrowers to cancel certain types of home loans within three business days without financial penalty.

How long do I have to exercise my right to rescind?

Borrowers generally have until midnight of the third business day after signing the loan documents, receiving the Truth in Lending disclosure, or receiving the Notice of Right to Rescind, whichever occurs last.

What types of loans are covered by the Right to Rescind?

The right to rescind typically applies to refinancing, home equity lines of credit (HELOCs), and home equity loans on a principal residence. It does not apply to mortgages used to purchase a new home or investment properties.

How do I officially cancel my loan using the Right to Rescind letter?

To cancel the loan, you must sign and deliver the Notice of Right to Rescind letter to the lender by the specified deadline. It is recommended to send the notice via certified mail with a return receipt to provide proof of timely delivery.

What happens after I submit a Notice of Right to Rescind?

Once the lender receives your rescission notice, the mortgage or lien becomes void. The lender has 20 calendar days to return any money or property given in connection with the transaction and must take steps to terminate their security interest in your home.

Comments