A Notice of Penalty for Early Withdrawal Letter is a formal document issued by financial institutions to inform depositors about charges incurred for closing a time deposit or CD before its maturity date. This letter details the specific fees assessed and the final payout amount. Understanding these terms helps you manage your personal finances effectively. Below are some ready to use templates.

Image cover: Mastering the Early Withdrawal Penalty Notice: Professional Templates and Samples

Letter Samples List

- Standard Notice of Penalty for Early Withdrawal Letter

- Certificate of Deposit Early Withdrawal Penalty Notice Letter

- Fixed Deposit Premature Withdrawal Penalty Letter

- Term Deposit Early Encashment Penalty Letter

- Individual Retirement Account Premature Distribution Penalty Letter

- Time Deposit Early Withdrawal Fee Assessment Letter

- Retirement Savings Early Withdrawal Penalty Letter

- Notice of Assessment for Premature Withdrawal Penalty Letter

- Early Withdrawal Penalty Acknowledgment Letter

- Savings Certificate Early Surrender Penalty Letter

- Commercial Term Deposit Penalty for Early Withdrawal Letter

- Notice of Interest Penalty for Early Withdrawal Letter

- Trust Account Early Withdrawal Penalty Letter

- Notice of Substantial Penalty for Early Withdrawal Letter

- Retail Certificate of Deposit Penalty Assessment Letter

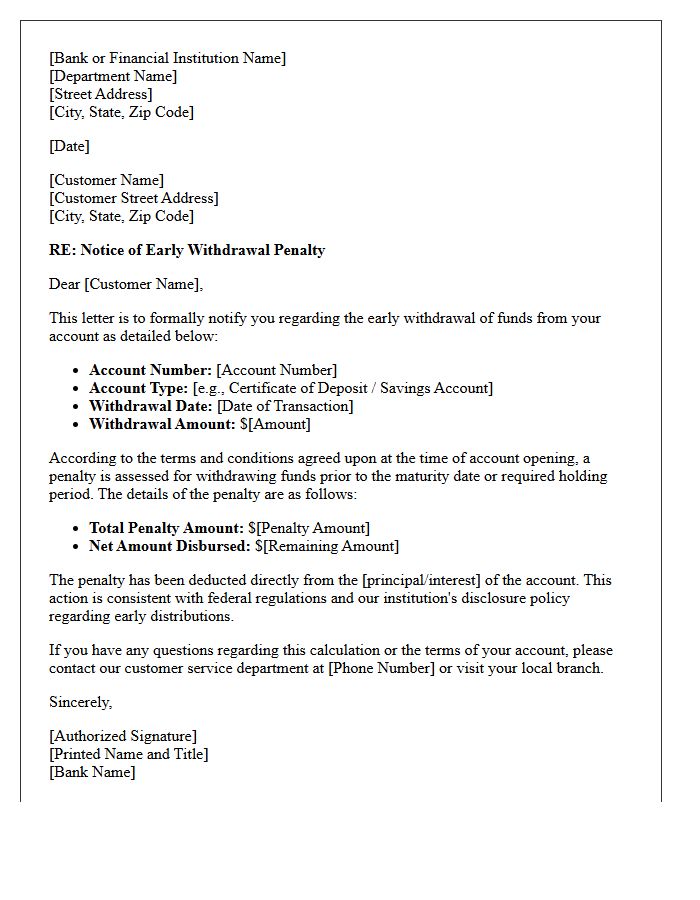

Standard Notice of Penalty for Early Withdrawal Letter

A Standard Notice of Penalty for Early Withdrawal Letter is a formal disclosure issued by financial institutions when a depositor closes a Certificate of Deposit (CD) before its maturity date. This document outlines the financial penalties incurred, typically calculated as a specific amount of interest lost. It ensures transparency regarding the reduction of the total payout. Understanding this notice is essential for assessing the cost of accessing liquid funds prematurely, as early withdrawal fees can significantly impact your investment's net yield and overall principal balance.

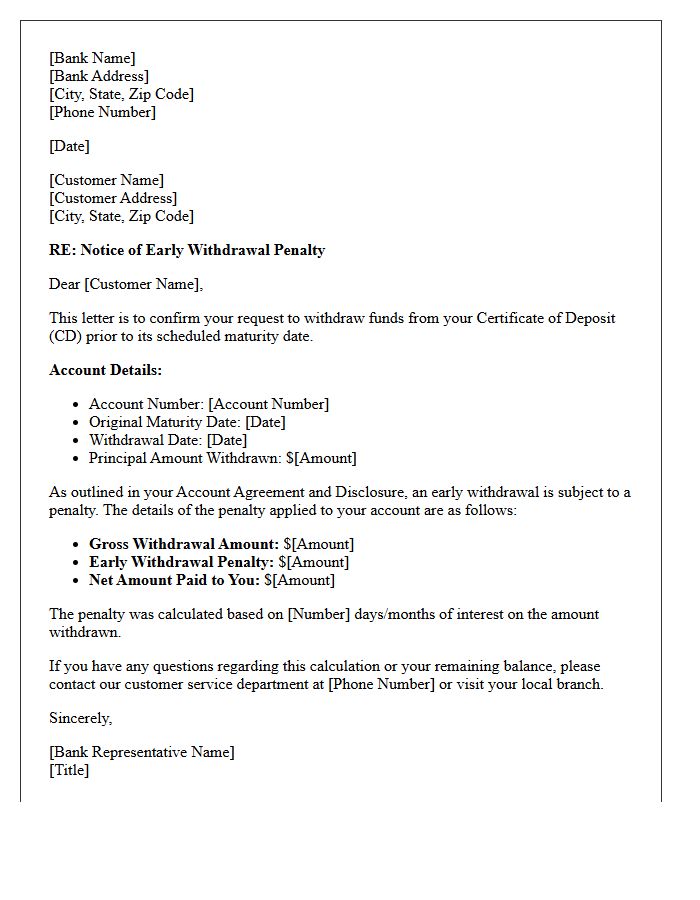

Certificate of Deposit Early Withdrawal Penalty Notice Letter

A Certificate of Deposit Early Withdrawal Penalty Notice Letter is a formal document issued by financial institutions to inform account holders about the financial consequences of closing a CD before its maturity date. This notice outlines the specific penalty fees incurred, which are often calculated as a portion of the earned interest. It is crucial to review these terms because early access to funds can significantly reduce your total return or even impact your initial principal investment depending on the bank's specific policies.

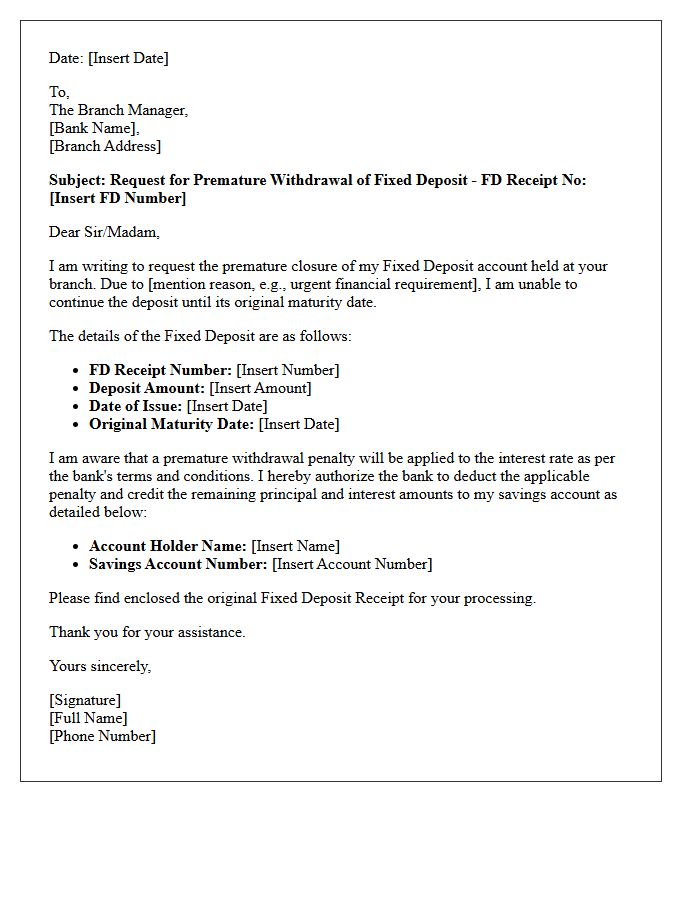

Fixed Deposit Premature Withdrawal Penalty Letter

A Fixed Deposit Premature Withdrawal Penalty Letter is a formal request submitted to a bank to close an investment before its maturity date. This document must clearly state the account details and the reason for early liquidation. It is essential to understand that banks typically levy a penalty fee, which reduces the total interest earned. Some institutions may waive these charges under specific hardship clauses. Always verify the current penalty rates and updated terms and conditions with your financial institution before finalizing the request to minimize potential financial loss.

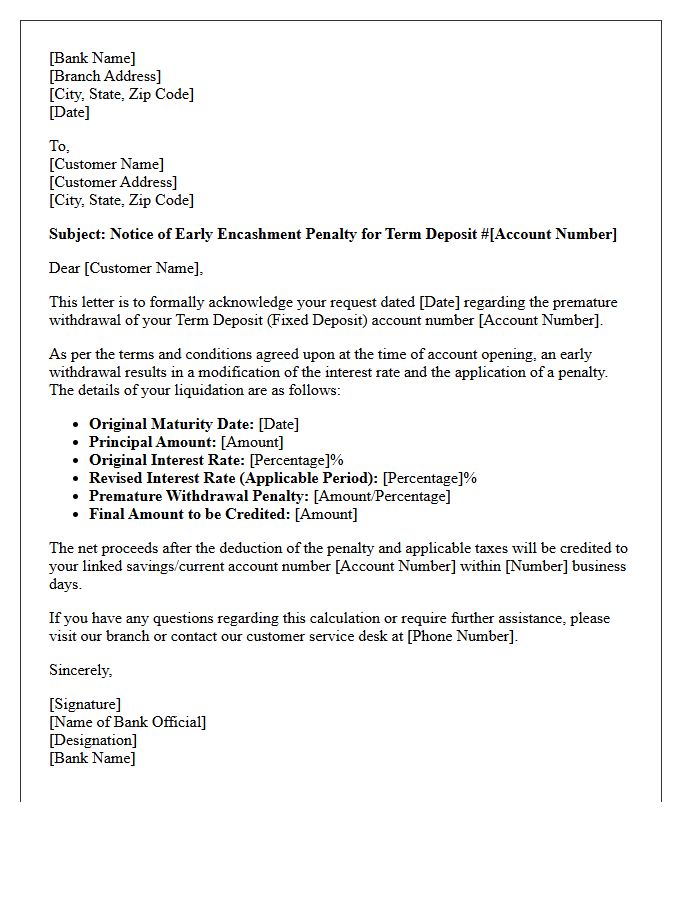

Term Deposit Early Encashment Penalty Letter

A Term Deposit Early Encashment Penalty Letter is a formal notification from a financial institution detailing the costs of withdrawing funds before the maturity date. This document specifies the reduction in interest earned or the flat fees applied for breaking the fixed-term agreement. It serves as essential legal documentation for account holders to understand the financial impact of early liquidation. Reviewing this letter ensures you are aware of the exact break funding costs and the final net amount you will receive upon closing the account prematurely.

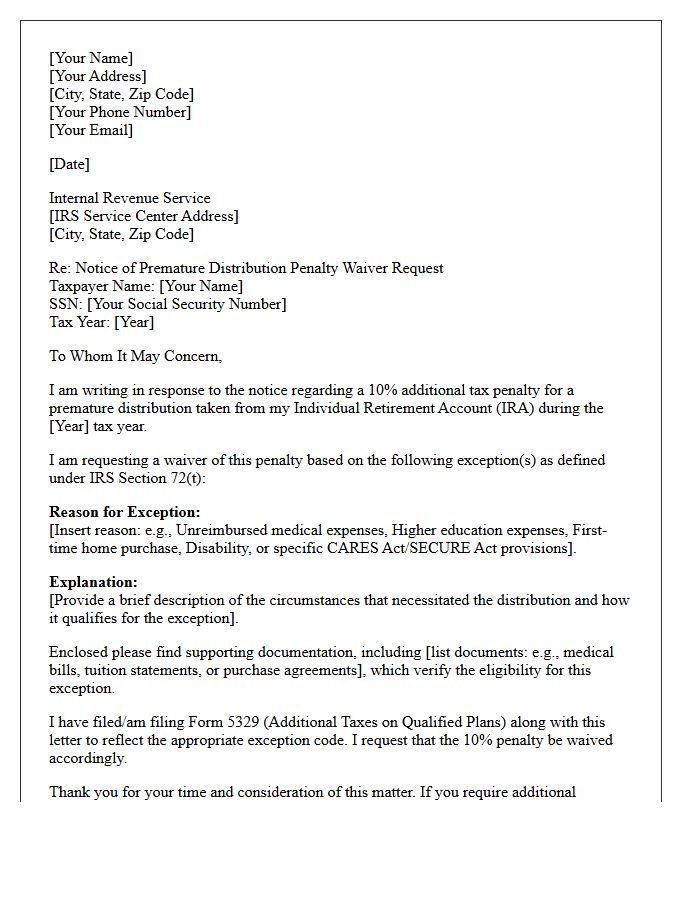

Individual Retirement Account Premature Distribution Penalty Letter

An IRS CP2100 notice or similar correspondence notifies taxpayers of an Individual Retirement Account premature distribution penalty. If you withdraw funds from an IRA before reaching age 59½, you typically owe a 10% additional tax unless an exception applies. This letter arrives when reported distributions do not match your tax return filings. To resolve this, you must verify the distribution amount, check for qualifying exemptions like medical expenses or first-time home purchases, and respond promptly to avoid further interest or penalties on the unpaid balance.

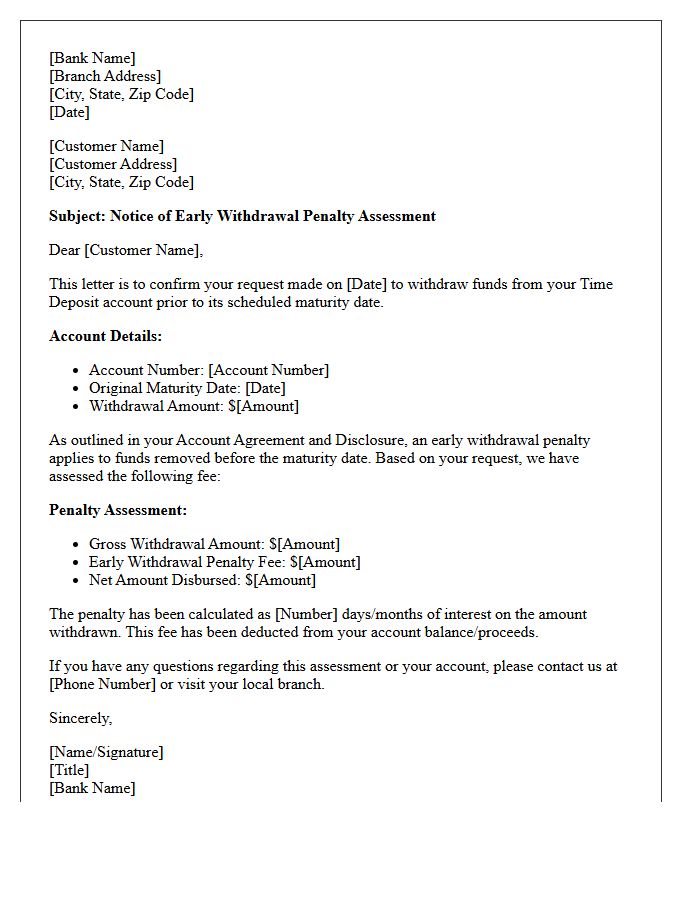

Time Deposit Early Withdrawal Fee Assessment Letter

A Time Deposit Early Withdrawal Fee Assessment Letter is a formal notification sent by a bank detailing the financial penalties incurred for closing a certificate before its maturity date. This document provides a clear breakdown of costs, specifying how the penalty was calculated-often based on a set number of months of interest. It is a critical record for understanding the net payout received and is essential for personal tax reporting, as early withdrawal penalties are often tax-deductible. Always review this letter to verify accuracy against your original account agreement.

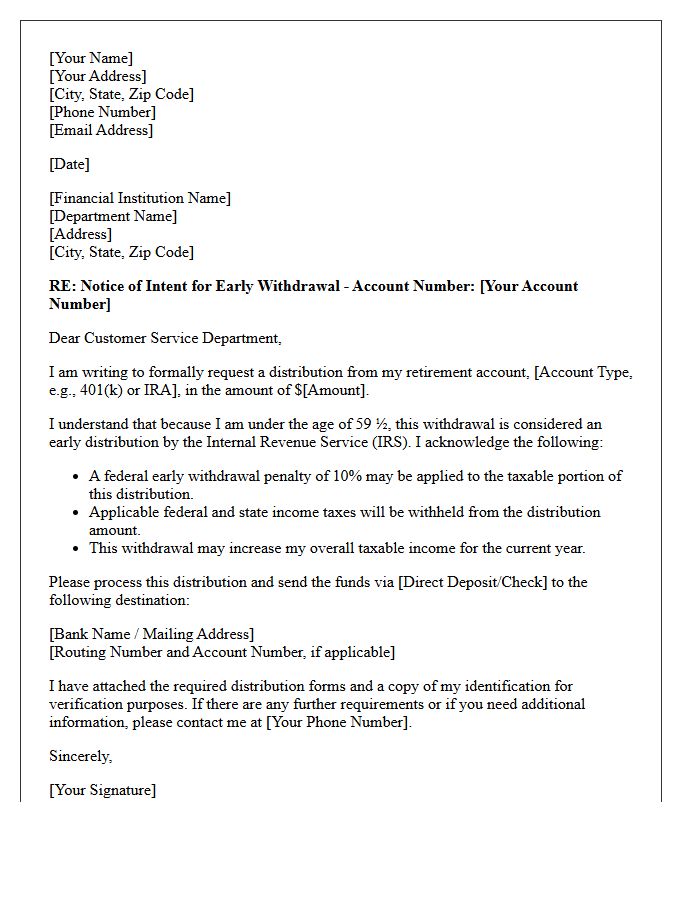

Retirement Savings Early Withdrawal Penalty Letter

Receiving a Retirement Savings Early Withdrawal Penalty Letter (IRS Notice CP15 or CP21) typically means you owe a 10% additional tax for distributing funds before age 59½. The IRS uses Form 1099-R to track these transactions. To resolve this, verify if you qualify for an exception, such as first-time home purchases or specific medical expenses. If the penalty is correct, you must update your tax return and pay the balance. Always keep records of your qualified distributions to avoid unnecessary assessments or future audits regarding your retirement accounts.

Notice of Assessment for Premature Withdrawal Penalty Letter

A Notice of Assessment for Premature Withdrawal Penalty is a legal document issued by the IRS when early distributions are taken from a retirement account, such as a 401(k) or IRA. This letter confirms that you owe a 10% additional tax on the amount withdrawn before age 59½. It outlines the specific tax liability, calculated interest, and required payment deadlines. To avoid further penalties, you must verify the distribution amount and ensure all IRS compliance requirements are met or provide proof of a qualifying exemption to contest the assessment.

Early Withdrawal Penalty Acknowledgment Letter

An Early Withdrawal Penalty Acknowledgment Letter is a formal document confirming that a depositor understands the financial consequences of accessing funds before a fixed-term investment, such as a CD, matures. This letter protects financial institutions by verifying that the client accepts a reduction in earned interest or principal. It serves as essential legal documentation to prevent future disputes regarding lost earnings. Reviewing the specific penalty calculations within this acknowledgment ensures you are fully aware of the costs associated with breaking your liquidity agreement early.

Savings Certificate Early Surrender Penalty Letter

A savings certificate early surrender penalty letter is a formal notice issued by a bank when you close a Certificate of Deposit (CD) before its maturity date. This document outlines the early withdrawal penalty, which typically calculates a specific number of months' interest forfeited. It is essential for tax reporting and personal accounting, as it confirms the final payout amount after fees. Always review this letter to understand the financial loss incurred and ensure the bank applied the terms of your original agreement accurately during the redemption process.

Commercial Term Deposit Penalty for Early Withdrawal Letter

A Commercial Term Deposit Penalty for Early Withdrawal Letter is a formal notification issued by a bank detailing the financial consequences of terminating a fixed-term investment before its maturity date. This document outlines the Interest Reduction or breakage fees applied to the principal balance. Businesses must review this letter to understand the specific Break Costs and liquidations terms. It serves as a legal record of the modified payout, ensuring transparency regarding the penalty calculation and the final distribution of remaining corporate funds after early exit adjustments.

Notice of Interest Penalty for Early Withdrawal Letter

A Notice of Interest Penalty for Early Withdrawal is a formal document issued by financial institutions when a depositor closes a Certificate of Deposit (CD) or time account before its maturity date. This letter details the specific financial penalty assessed for breaking the agreement, typically calculated as a loss of earned interest. It serves as essential documentation for your tax records, as these penalties are often tax-deductible on your annual return, even if you do not itemize deductions. Always verify the penalty amount against your original account disclosure statement.

Trust Account Early Withdrawal Penalty Letter

A Trust Account Early Withdrawal Penalty Letter is a formal notification issued by a financial institution when funds are removed from a restricted account before the agreed maturity date. This document outlines the specific financial penalties incurred, the reduction in earned interest, and the final disbursement amount. It serves as an essential compliance record for trustees to justify asset depletion to beneficiaries or tax authorities. Understanding these terms is crucial to minimize loss of principal and ensure proper fiduciary management of the trust's underlying investments.

Notice of Substantial Penalty for Early Withdrawal Letter

A Notice of Substantial Penalty for Early Withdrawal is a formal document issued by financial institutions when a customer liquidates a fixed-term asset, such as a Certificate of Deposit (CD), before its maturity date. This letter details the specific financial costs incurred, which often consist of forfeited interest or a portion of the principal balance. Receiving this notice is crucial for tax reporting, as the penalty amount is generally deductible on your federal income tax return to offset reported interest income. Always review the terms to understand the total impact on your investment.

Retail Certificate of Deposit Penalty Assessment Letter

A Retail Certificate of Deposit Penalty Assessment Letter is a formal notice sent by a financial institution when a customer initiates an early withdrawal from a CD. This document calculates the monetary penalty incurred for breaking the fixed-term agreement before its maturity date. It provides transparency by detailing the original investment, the specific interest forfeiture, and the final payout amount. Understanding this letter is essential for evaluating the total cost of accessing liquidity prematurely and ensuring your banking records remain accurate for tax and personal accounting purposes.

What is a Notice of Penalty for Early Withdrawal letter?

A Notice of Penalty for Early Withdrawal is a formal notification sent by a financial institution to an account holder explaining the fees and interest forfeitures incurred when funds are removed from a time-deposit account, such as a CD, before its maturity date.

What information is included in an early withdrawal penalty notice?

The letter typically includes the account number, the total amount withdrawn, the specific penalty calculation (often a set number of months of interest), the remaining account balance, and the federal or state regulations governing the penalty.

How is the early withdrawal penalty calculated on a CD?

The penalty is generally calculated based on a predetermined period of simple interest. For example, a bank may charge 90 days of interest for early withdrawal on a 12-month CD, regardless of how much interest the account has actually earned at the time of the request.

Can an early withdrawal penalty exceed the interest earned?

Yes, if the penalty amount exceeds the interest earned to date, the financial institution is often required to deduct the difference from the principal balance of the account, as detailed in the terms and conditions provided at account opening.

Are there exceptions where an early withdrawal penalty may be waived?

Penalties may be waived in specific circumstances such as the death or declared mental incompetence of an account holder, or if the withdrawal is made during a designated "grace period" immediately following an account's maturity and automatic renewal.

Comments