A force-placed insurance notice letter is a formal notification from a lender informing a homeowner that their property insurance has lapsed. If you fail to provide proof of coverage, the bank will purchase a policy on your behalf, often at a significantly higher cost. Understanding your rights is essential to resolving this issue quickly. To assist you, below are some ready to use template.

Image cover: Professional Force-Placed Insurance Notice Templates: Sample Letters and Best Practices

Letter Samples List

- Initial Notice of Expired Hazard Insurance Letter

- Second Warning of Lapsed Coverage Letter

- Notice of Intent to Force-Place Insurance Letter

- Final Demand for Proof of Insurance Letter

- Notice of Force-Placed Insurance Activation Letter

- Force-Placed Insurance Premium Assessment Letter

- Notice of Force-Placed Flood Insurance Letter

- Confirmation of Borrower Insurance Verification Letter

- Notice of Force-Placed Insurance Cancellation Letter

- Force-Placed Insurance Premium Refund Letter

- Annual Renewal of Force-Placed Coverage Letter

- Notice of Insufficient Insurance Coverage Letter

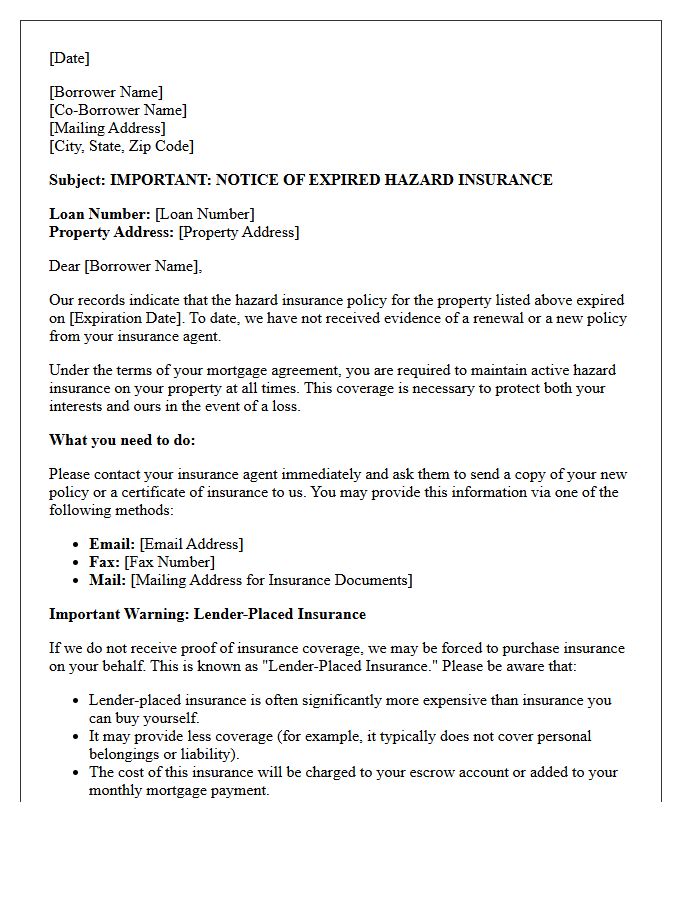

Initial Notice of Expired Hazard Insurance Letter

An Initial Notice of Expired Hazard Insurance Letter is a formal notification from your mortgage lender stating that your property insurance coverage has lapsed. It is crucial to act immediately by providing proof of renewed coverage to avoid lender-placed insurance. This forced-placed policy is typically more expensive and offers less protection than private plans. To resolve this, contact your insurance agent to send the updated declarations page to your lender, ensuring your homeowner's insurance meets the required mortgage standards and protects your financial interest in the property.

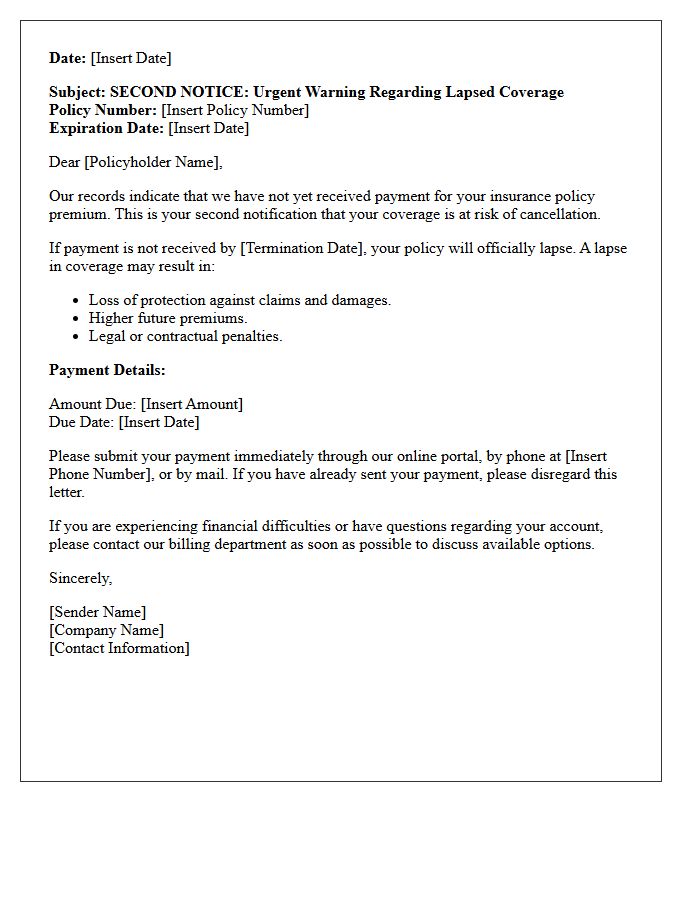

Second Warning of Lapsed Coverage Letter

Receiving a Second Warning of Lapsed Coverage Letter is a critical final notice indicating that your insurance policy is about to terminate. This document signifies that your grace period is ending due to unpaid premiums. To prevent a permanent loss of protection and potential financial liability, you must submit the outstanding balance immediately. Ignoring this warning leads to a coverage gap, which can cause higher future rates or legal penalties. Contact your insurer instantly to verify your status and ensure your policy remains active through prompt payment.

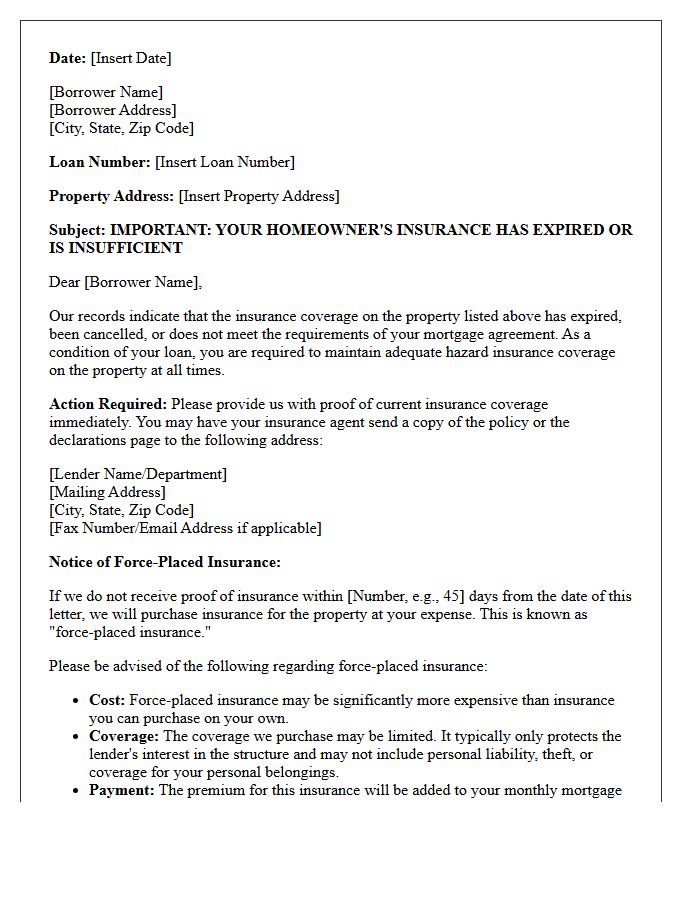

Notice of Intent to Force-Place Insurance Letter

A Notice of Intent to Force-Place Insurance is a formal warning from your mortgage lender stating that your homeowners insurance has lapsed or is insufficient. Federal law requires the lender to send this notice at least 45 days before purchasing a policy on your behalf. This force-placed insurance is typically much more expensive and provides less coverage than private policies. To avoid these high costs, you must immediately provide the lender with proof of active coverage to ensure your property remains protected and your monthly payments stay manageable.

Final Demand for Proof of Insurance Letter

A Final Demand for Proof of Insurance is a critical legal notice from a lender or landlord. It serves as a last warning that your property lacks active coverage, violating your contractual agreement. Failing to provide valid documentation by the specified deadline allows the sender to implement "force-placed insurance," which is often significantly more expensive and provides less protection. To protect your financial interests, immediately contact your insurance agent to verify coverage and send the Certificate of Insurance to the requesting party to prevent costly penalties or potential default.

Notice of Force-Placed Insurance Activation Letter

A Notice of Force-Placed Insurance Activation informs you that your lender has purchased coverage for your property because your private policy lapsed or was insufficient. This force-placed insurance is typically significantly more expensive than standard market rates and only protects the lender's financial interest, not your personal belongings or liability. To cancel this costly requirement, you must immediately provide your mortgage servicer with proof of active hazard insurance. Failure to act will result in higher monthly mortgage payments and potential escrow shortages.

Force-Placed Insurance Premium Assessment Letter

A Force-Placed Insurance Premium Assessment Letter notifies a homeowner that their lender has purchased a hazard insurance policy on their behalf. This occurs if your personal coverage lapses or is deemed insufficient by the lender. These policies are typically much more expensive and provide less protection than private plans. Receiving this letter serves as a final warning to provide proof of insurance immediately to avoid high monthly costs. To resolve the assessment, you must submit your active policy declarations page to your mortgage servicer to cancel the lender-placed coverage.

Notice of Force-Placed Flood Insurance Letter

Receiving a Notice of Force-Placed Flood Insurance Letter indicates your lender has determined your property lacks adequate flood coverage. Federal law requires mandatory flood insurance for properties in high-risk zones with federally backed mortgages. If you do not provide proof of a policy within 45 days, the lender will purchase insurance on your behalf. These force-placed policies are often significantly more expensive and provide less protection than private plans. You should immediately contact your insurance agent to verify coverage and submit the required documentation to avoid unnecessary costs.

Confirmation of Borrower Insurance Verification Letter

A Confirmation of Borrower Insurance Verification Letter is a formal document used by lenders to ensure collateral protection. It confirms that a borrower maintains active, adequate insurance coverage as required by the loan agreement. This verification mitigates risk for financial institutions by verifying the policy status, coverage limits, and loss payee clauses. If a borrower fails to provide this proof, the lender may implement force-placed insurance. Keeping this documentation updated is essential for maintaining loan compliance and avoiding additional premiums or legal complications during the mortgage or auto loan term.

Notice of Force-Placed Insurance Cancellation Letter

A Notice of Force-Placed Insurance Cancellation is a critical document confirming that your lender has terminated the high-cost policy they purchased on your behalf. This usually occurs once you provide proof of voluntary coverage that meets your mortgage requirements. It is vital to verify the effective date of cancellation to ensure no gaps exist. Additionally, your lender must refund any unearned premiums charged during the overlapping period. Always keep this letter as permanent evidence that your homeowners insurance compliance has been restored and your escrow account is updated.

Force-Placed Insurance Premium Refund Letter

If you receive a Force-Placed Insurance Premium Refund Letter, it indicates your mortgage lender charged you for unnecessary or overpriced property coverage. This typically occurs when proof of private insurance was missing but later provided. The letter confirms a reimbursement is owed to your escrow account or via check. Always verify the refund amount against your premium disclosures to ensure you are fully compensated for the overlapping coverage period. Promptly update your lender with current policy details to prevent future lapses and avoid costly, involuntary insurance placements.

Annual Renewal of Force-Placed Coverage Letter

An Annual Renewal of Force-Placed Coverage Letter notifies homeowners that their lender is extending lender-placed insurance because voluntary coverage is missing. This mandatory notification outlines the premium cost, which is typically much higher than private policies while providing less protection. Homeowners should immediately provide proof of insurance to their servicer to cancel this coverage and receive a refund for overlapping periods. Maintaining independent insurance is essential to avoid these costly automatic renewals and ensure comprehensive property protection.

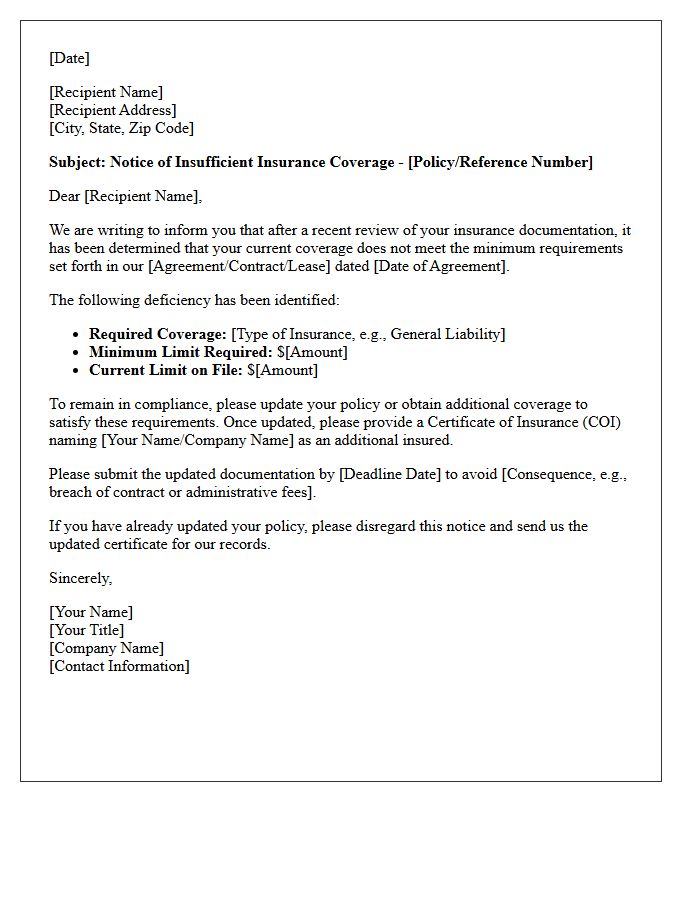

Notice of Insufficient Insurance Coverage Letter

A Notice of Insufficient Insurance Coverage is a critical legal alert sent by lenders or contractors when your current policy fails to meet specific contract requirements. This document signifies a compliance gap that could lead to financial liability or breach of contract. It is essential to address these discrepancies immediately to avoid "force-placed insurance," which is often more expensive and provides less protection. Always review the stated deficiencies against your policy limits and endorsements to ensure continuous protection and maintain your professional or financial standing.

What is a force-placed insurance notice letter?

A force-placed insurance notice letter is a formal notification from your mortgage lender informing you that your homeowners insurance has expired, been canceled, or is insufficient. The letter warns that the lender will purchase a policy on your behalf and charge you for the premiums if you do not provide proof of active coverage.

Why did I receive a notice about lender-placed insurance?

You received this notice because your lender has not received updated proof of insurance from your carrier. This typically happens if your policy lapsed due to non-payment, your insurance company canceled your coverage, or your current policy limits do not meet the minimum requirements outlined in your mortgage agreement.

How much time do I have to respond to a force-placed insurance notice?

Under federal law, lenders must send at least two notices before charging you for force-placed insurance. The first notice is sent at least 45 days before a premium charge is assessed, and a second reminder notice is sent at least 30 days after the first notice and at least 15 days before you are charged.

Is force-placed insurance more expensive than a private policy?

Yes, force-placed insurance is significantly more expensive than a policy you purchase yourself, often costing double or triple the market rate. Additionally, these policies typically only protect the lender's interest in the structure and do not provide coverage for personal belongings, personal liability, or loss of use.

How do I stop force-placed insurance from being added to my mortgage?

To stop force-placed insurance, you must immediately provide your lender with a copy of your current insurance declarations page. This document must show that you have continuous coverage that meets the lender's requirements. Once valid proof is received, the lender must cancel the force-placed policy and refund any overlapping premiums charged.

Comments