A Substitute Check Policy Disclosure explains your rights regarding electronic check processing under the Check 21 Act. This essential letter outlines how substitute checks differ from originals and the specific procedures for claiming a refund if errors occur. Understanding these legal protections ensures consumer financial safety. To help you draft this notice, below are some ready to use templates.

Image cover: Substitute Check Policy Disclosure: Official Templates and Compliance Guide

Letter Samples List

- Initial Substitute Check Policy Disclosure Letter

- Annual Substitute Check Policy Disclosure Letter

- Updated Substitute Check Policy Disclosure Letter

- Consumer Substitute Check Policy Disclosure Letter

- Commercial Substitute Check Policy Disclosure Letter

- Substitute Check Expedited Recredit Claim Letter

- Substitute Check Claim Acknowledgment Letter

- Substitute Check Claim Resolution Letter

- Substitute Check Claim Denial Letter

- Substitute Check Image Request Acknowledgment Letter

- Substitute Check Error Investigation Notice Letter

- Amended Substitute Check Policy Disclosure Letter

Initial Substitute Check Policy Disclosure Letter

The Substitute Check Policy Disclosure is a mandatory document informing consumers about their rights under the Check 21 Act. It explains that digital copies, known as substitute checks, are the legal equivalent of original paper checks. Importantly, it outlines the expedited recredit procedure, which allows customers to claim a refund if a substitute check was processed incorrectly or caused a financial loss. Consumers should retain this notice to understand the specific timeframes and requirements for disputing unauthorized charges or processing errors involving these digital instruments.

Annual Substitute Check Policy Disclosure Letter

The Annual Substitute Check Policy Disclosure Letter is a mandatory notice sent by financial institutions to inform customers about their rights under the Check 21 Act. It explains how digital images of checks, known as substitute checks, serve as legal equivalents to originals. This document is essential for understanding expedited recredit procedures if a loss occurs due to an error. Reviewing this disclosure ensures you know how to dispute unauthorized charges and protects your consumer rights regarding electronic check processing and bank accountability.

Updated Substitute Check Policy Disclosure Letter

The Updated Substitute Check Policy Disclosure explains your rights regarding "substitute checks," which are legal paper copies of original checks. It is crucial to understand the expedited recredit process, which allows you to claim a refund if a substitute check was processed incorrectly. You must typically file a claim within 40 days to recover lost funds and interest. This disclosure ensures transparency in electronic processing, protecting consumers from financial errors caused by Check 21 Act image replacements during bank transactions.

Consumer Substitute Check Policy Disclosure Letter

A Substitute Check Policy Disclosure explains your rights under the Check 21 Act. When a bank creates a digital image of your original paper check to process payments, it becomes a legal equivalent called a substitute check. This letter is crucial because it outlines specific reclaim procedures if a substitute check causes a processing error or financial loss. You have the right to request an expedited recredit if you identify an unauthorized or incorrect charge, provided you file a claim within the timeframe specified in this mandatory consumer protection notice.

Commercial Substitute Check Policy Disclosure Letter

A Commercial Substitute Check Policy Disclosure Letter explains your rights under the Check 21 Act regarding electronic check processing. It informs businesses that original paper checks may be replaced by substitute checks, which are legally equivalent documents. This disclosure is vital because it outlines specific loss recovery procedures and indemnity protections available if a substitute check causes a financial error. Understanding these terms ensures your business can effectively navigate claims for expedited recredit and maintain accurate records during digital banking transactions.

Substitute Check Expedited Recredit Claim Letter

A Substitute Check Expedited Recredit Claim Letter is a formal request sent to a bank when an consumer loses money due to an improperly processed substitute check. Under the Check 21 Act, this document must be submitted within 40 days of the incident. It must include a written description of the error, the specific financial loss incurred, and proof of why the substitute check was invalid. If the claim is valid, the bank must generally provide a provisional credit of up to $2,500 within ten business days during their investigation.

Substitute Check Claim Acknowledgment Letter

A Substitute Check Claim Acknowledgment Letter is a formal notification sent by a financial institution to confirm receipt of an expedited recredit request. Under the Check 21 Act, banks must acknowledge your claim within ten business days. This document serves as proof that the bank is investigating a potential error involving a substitute check. It outlines your legal rights, the expected investigation timeline, and whether a provisional credit has been applied to your account while the discrepancy is being resolved.

Substitute Check Claim Resolution Letter

A Substitute Check Claim Resolution Letter is a formal notification from a bank regarding a Check 21 Act investigation. It informs the consumer whether their claim for a refund due to an unauthorized or incorrect substitute check has been approved, denied, or requires more time. If approved, the letter details the recredit of funds to the account. If denied, it must explain the reasoning and provide documentation used for the decision. Understanding this letter is essential for protecting your consumer rights and ensuring financial recovery from check processing errors.

Substitute Check Claim Denial Letter

Receiving a Substitute Check Claim Denial Letter means your financial institution has rejected a request for a refund under the Check 21 Act. This document must clearly state the specific reason for denial, such as missing the 40-day filing deadline or failing to provide proof of loss. To contest this decision, you should immediately review the bank's evidence and provide additional documentation to support your claim. Timely action is essential, as consumers have limited legal protections once a formal denial is issued regarding these paper-to-digital reproductions.

Substitute Check Image Request Acknowledgment Letter

A Substitute Check Image Request Acknowledgment Letter confirms that a financial institution has received your formal inquiry regarding a specific transaction. This document serves as legal proof of your request under the Check 21 Act. It outlines the investigation timeline, typically providing a response within ten business days. This acknowledgment is essential for tracking dispute resolution status and ensures your consumer rights are protected if a substitute check was processed incorrectly. Always retain this letter for your personal financial records until the claim is resolved.

Substitute Check Error Investigation Notice Letter

The Substitute Check Error Investigation Notice Letter is a formal document used to dispute inaccuracies under the Check 21 Act. If you identify a processing error involving a substitute check, you must provide expedited recredit claims within forty days. This letter notifies your bank of the discrepancy and initiates a mandatory investigation. Legally, financial institutions must resolve the issue or provide a provisional credit to your account within ten business days. Promptly submitting this notice ensures your consumer rights are protected and helps recover lost funds quickly.

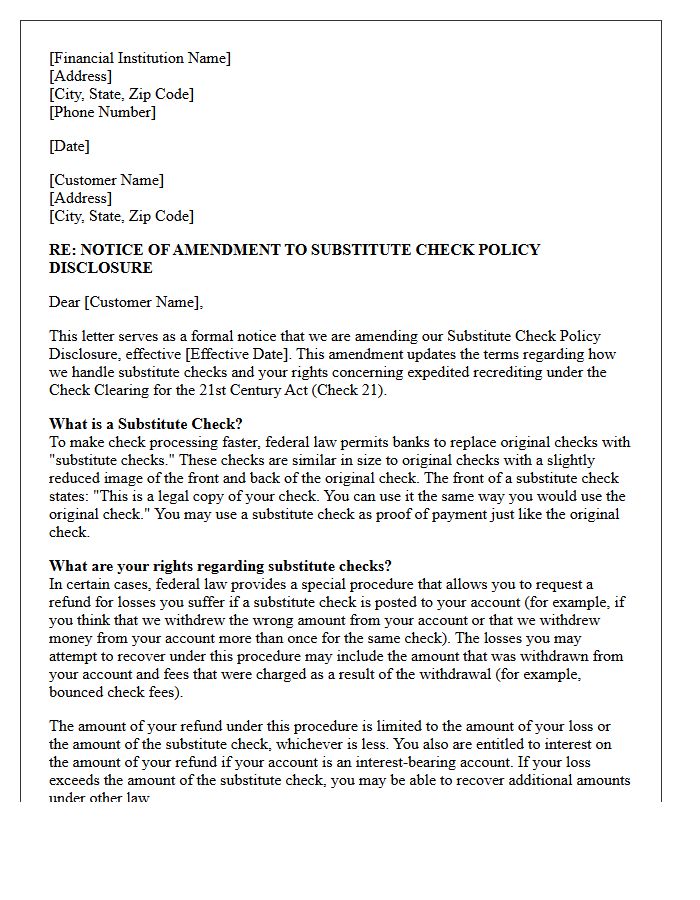

Amended Substitute Check Policy Disclosure Letter

The Amended Substitute Check Policy Disclosure Letter updates consumers on their rights regarding electronic image replacements of original checks. Under the Check 21 Act, these substitute checks are the legal equivalent of paper originals. This document outlines the expedited recredit procedure, allowing customers to claim refunds if a substitute check was processed incorrectly, causing a financial loss. It is essential to review these updates to understand specific timeframes for reporting errors and the necessary documentation required to resolve billing disputes or unauthorized processing issues effectively.

What is a Substitute Check Policy Disclosure?

A Substitute Check Policy Disclosure is a legal notice provided by financial institutions to inform customers of their rights under the Check Clearing for the 21st Century Act (Check 21). It explains how digital images of original paper checks are processed and the specific legal protections available if a consumer encounters an error related to a substitute check.

What is a substitute check and how does it differ from my original check?

A substitute check is a high-quality paper reproduction of an original check that contains an image of the front and back and is legally the same as the original. It must include the statement: "This is a legal copy of your check. You can use it the same way you would use the original check." Unlike the original, a substitute check is created electronically to speed up processing times.

What are my rights if I find an error involving a substitute check?

Under federal law, you have the right to file a claim for an "expedited recredit" if you believe a substitute check was charged to your account in error or resulted in a loss. This protection applies specifically to substitute checks; it does not cover original paper checks or electronic ACH transfers. If your claim is valid, the bank must generally restore the funds while they investigate the discrepancy.

How do I file a claim for a refund under the Check 21 Act?

To file a claim, you must contact your bank within 40 calendar days of the date the account statement showing the error was mailed. You must provide a description of the error, an estimate of your loss, and an explanation of why the substitute check is necessary for your investigation. Many banks require this notice in writing to initiate the formal recredit process.

When will my funds be returned after filing a substitute check claim?

If the bank determines your claim is valid, they must recredit your account by the end of the next business day following their determination. If the investigation takes longer than 10 business days, the bank must provide a provisional credit for the amount of the loss (up to $2,500, plus interest) while they continue to investigate, unless they can prove the substitute check was processed correctly.

Comments