If you discover a discrepancy between the written and numerical value on a check, or suspect unauthorized modifications, you must act quickly. This guide explains the legal protections available when dealing with a dispute of altered check amount and how to notify your bank to recover lost funds. To help you resolve this banking issue efficiently, below are some ready to use template.

Image cover: Disputed Altered Check Amount: Formal Claim Letter Samples and Templates

Letter Samples List

- Initial Notification Letter Regarding Altered Check Amount Dispute

- Formal Dispute Letter for Fraudulent Check Amount Alteration

- Customer Letter Demanding Reversal of Altered Check Funds

- Affidavit and Dispute Letter for Forged Check Amount

- Bank Acknowledgment Letter of Altered Check Dispute

- Investigation Update Letter Concerning Altered Check Claim

- Provisional Credit Letter for Disputed Altered Check Amount

- Final Resolution Letter Regarding Altered Check Dispute

- Request Letter for Original Check Image in Alteration Dispute

- Letter of Appeal for Denied Altered Check Amount Claim

- Demand Letter for Restitution of Altered Check Overpayment

- Account Holder Letter Reporting Unauthorized Check Amount Change

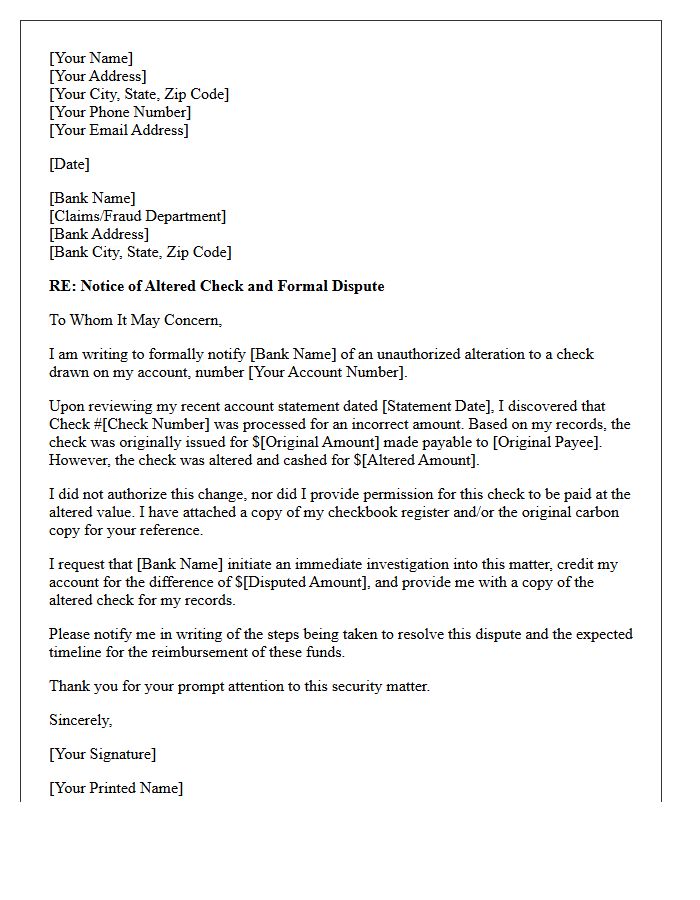

Initial Notification Letter Regarding Altered Check Amount Dispute

An Initial Notification Letter is a formal document sent by a financial institution to inform a customer about an altered check amount dispute. This notice confirms that an investigation has begun regarding discrepancies between the original check value and the processed amount. It is crucial to review the transaction details immediately to ensure accuracy. This letter serves as legal evidence of the claim, protecting your rights under banking regulations while the bank works to recover misappropriated funds and resolve the fraudulent activity on your account.

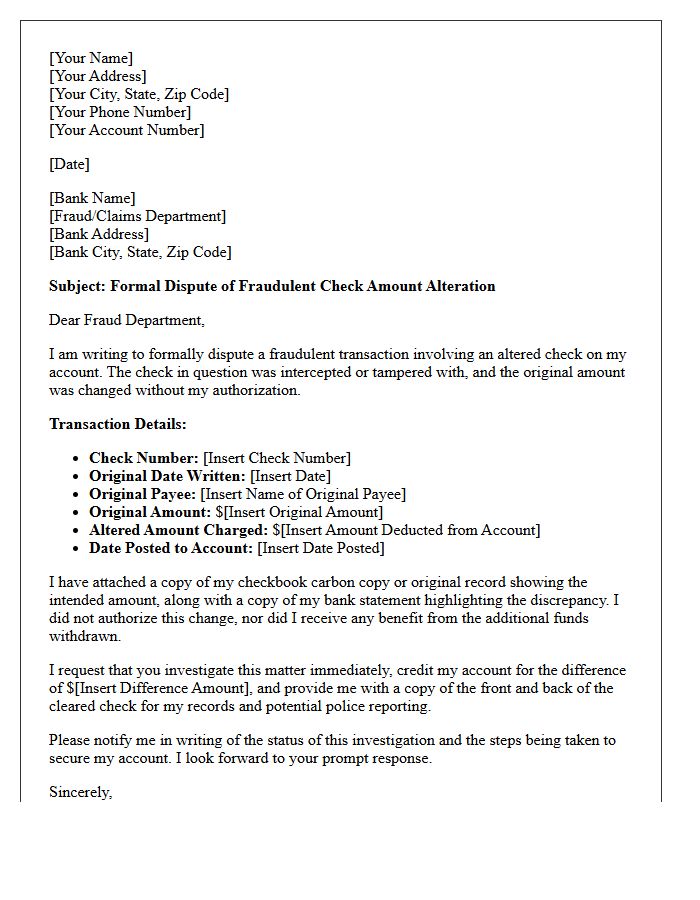

Formal Dispute Letter for Fraudulent Check Amount Alteration

A formal dispute letter for a fraudulent check amount alteration is a critical legal document used to notify your bank of unauthorized changes. To protect your rights under the Uniform Commercial Code, you must clearly state that the original check was intercepted and modified. Include essential details like the check number, the original intended value, and the unauthorized amount debited. Request an immediate reimbursement and a formal investigation. Sending this via certified mail creates a vital paper trail to prove you reported the check fraud within the required statutory timeframe.

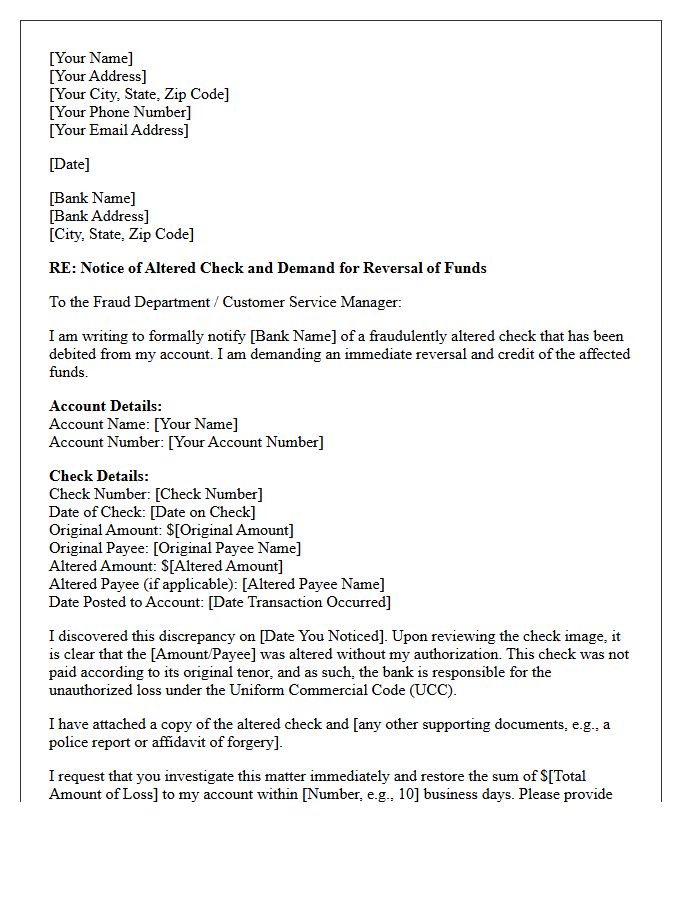

Customer Letter Demanding Reversal of Altered Check Funds

A demand letter for altered check funds is a formal legal notice sent to your bank to recover money stolen through unauthorized document changes. You must notify the financial institution immediately upon discovering the discrepancy to preserve your rights under the Uniform Commercial Code. Clearly state the account details, the specific check number, and the exact amount of the unauthorized alteration. Demand a full reversal of the debited funds within a specific timeframe, as banks are generally strictly liable for honoring checks that are not properly payable due to material alterations.

Affidavit and Dispute Letter for Forged Check Amount

When dealing with a forged check amount, you must immediately file a fraudulent alteration claim with your bank. Use a formal affidavit to provide a sworn statement confirming the original intended value and the unauthorized changes made. Accompany this with a dispute letter that specifies the check number, date, and discrepancy details. Acting quickly is essential to protect your legal rights under the Uniform Commercial Code, which mandates that banks must generally reimburse customers for unauthorized transactions reported within a specific statutory timeframe.

Bank Acknowledgment Letter of Altered Check Dispute

A Bank Acknowledgment Letter is a formal document confirming that your financial institution has received your claim regarding an altered check dispute. This letter serves as critical proof that the investigation process has officially begun. It typically includes a unique case number and outlines the expected resolution timeframe. It is essential to keep this record to protect your legal rights under banking regulations while the bank verifies the unauthorized modifications made to the original payment instrument to recover your funds.

Investigation Update Letter Concerning Altered Check Claim

An Investigation Update Letter keeps claimants informed regarding the status of an altered check claim. This essential document confirms that the financial institution is actively verifying discrepancies, such as changed payees or modified amounts. It outlines the current progress, requests any missing documentation, and provides a tentative timeline for resolution. Receiving this notice ensures transparency and helps protect your rights under banking regulations while the bank coordinates with the payor institution to recover lost funds or issue a reimbursement.

Provisional Credit Letter for Disputed Altered Check Amount

A provisional credit letter confirms that your bank has temporarily restored funds to your account while they investigate a disputed altered check amount. This notice validates that your claim was received and provides immediate liquidity. However, it is crucial to understand that these funds are not permanent. If the bank's investigation determines the transaction was legitimate or your claim is denied, they reserve the right to reverse the credit. Always retain this documentation until the bank issues a final written resolution confirming the permanent adjustment of your account balance.

Final Resolution Letter Regarding Altered Check Dispute

A Final Resolution Letter regarding an altered check dispute confirms the bank's definitive decision after investigating unauthorized changes to a check's payee or amount. This document outlines whether your reimbursement claim was approved or denied based on evidence like check images and account history. It serves as official documentation of the case closure, detailing any permanent credits issued or the reasons for liability. If you disagree with the outcome, this letter provides the necessary legal record for initiating further appeals or regulatory complaints to recover lost funds.

Request Letter for Original Check Image in Alteration Dispute

When disputing an unauthorized alteration, you must submit a formal request letter to your bank to obtain the original check image. This document serves as critical evidence to prove that payment details, such as the payee name or amount, were modified after signing. Ensure your letter includes the check number, transaction date, and a specific demand for high-resolution copies of both the front and back. Securing this forensic proof is the most important step in demonstrating fraud and recovering lost funds during a banking investigation or legal challenge.

Letter of Appeal for Denied Altered Check Amount Claim

A Letter of Appeal for a denied altered check claim is your formal challenge against a bank's refusal to refund fraudulent losses. It must clearly state the claim reference number and provide specific evidence of the unauthorized changes. Highlight that you met the duty of ordinary care in handling your finances. Attach supporting documents, such as copies of the original check and police reports, to prove the discrepancy. Timeliness is critical; ensure your appeal is submitted within the bank's mandated statutory deadline to preserve your legal rights under the Uniform Commercial Code.

Demand Letter for Restitution of Altered Check Overpayment

A demand letter for the restitution of an altered check overpayment is a formal legal notification sent to a recipient who unjustly received excess funds. This document explicitly outlines the discrepancy between the original intended amount and the fraudulent or accidental alteration. It serves as a mandatory request for repayment before pursuing further litigation. To be effective, it must include copies of the altered instrument, a specific deadline for restitution, and a clear warning of potential legal action. Sending this letter is a critical step in establishing a paper trail for financial recovery.

Account Holder Letter Reporting Unauthorized Check Amount Change

When you receive an account holder letter reporting an unauthorized check amount change, you must act immediately. This document signifies potential check alteration fraud, where a criminal modifies the original value of your payment. To protect your finances, contact your bank to initiate a formal dispute and request a claim form. Timely reporting is essential to recover stolen funds under banking regulations. Always verify your monthly statements and use secure payment methods to minimize risks associated with physical check tampering and identity theft.

What should I do if I discover a check I wrote has been altered for a different amount?

You should immediately notify your bank's fraud department to report the discrepancy. Request to file a formal "Affidavit of Forged or Altered Instrument" to initiate the dispute process and protect your account from further unauthorized activity.

How long do I have to dispute an altered check amount with my bank?

Under the Uniform Commercial Code (UCC), you typically have up to 30 days from the date your bank statement was made available to report an alteration. However, specific bank agreements may require notification within 14 days to maintain full reimbursement rights.

What evidence is needed to prove a check amount was fraudulently altered?

To support your dispute, provide a copy of the original check (if available), the carbon copy from your checkbook, or images of the check showing visible signs of tampering, such as different ink colors, erased handwriting, or chemical washing marks.

Can I get my money back if a bank cashes a check with an altered amount?

Yes, banks are generally responsible for paying checks as originally authorized. If you report the alteration timely and provide proof that the amount was changed without your consent, the bank is usually required to credit the difference back to your account.

Who is liable for a dispute involving an altered check amount?

Liability usually falls on the "bank of first deposit" (the bank that accepted the altered check) for breaching the transfer warranty. However, the payor bank may deny the claim if they can prove the account holder was negligent, such as leaving large blank spaces when writing the check.

Comments