Falling victim to a fraudulent transaction requires immediate action to recover your funds. This guide explains how to initiate a dispute of unauthorized wire transfer with your financial institution and protect your legal rights under banking regulations. Learn the essential steps to report errors and reclaim your missing capital effectively. To help you start the process, below are some ready to use template.

Image cover: Dispute Toolkit: Unauthorized Wire Transfer Sample Letters and Templates

Letter Samples List

- Initial Notice of Unauthorized Wire Transfer Letter

- Formal Wire Transfer Dispute Letter

- Fraudulent Wire Transaction Affidavit Letter

- Request for Wire Transfer Reversal Letter

- Unauthorized Commercial Wire Dispute Letter

- Follow-Up Wire Transfer Investigation Letter

- Escalation of Unresolved Wire Fraud Letter

- Bank Mandate and Wire Authorization Breach Letter

- Appeal of Denied Wire Transfer Claim Letter

- Pre-Litigation Wire Transfer Demand Letter

- Regulatory Agency Wire Fraud Complaint Letter

- Final Demand for Wire Funds Reimbursement Letter

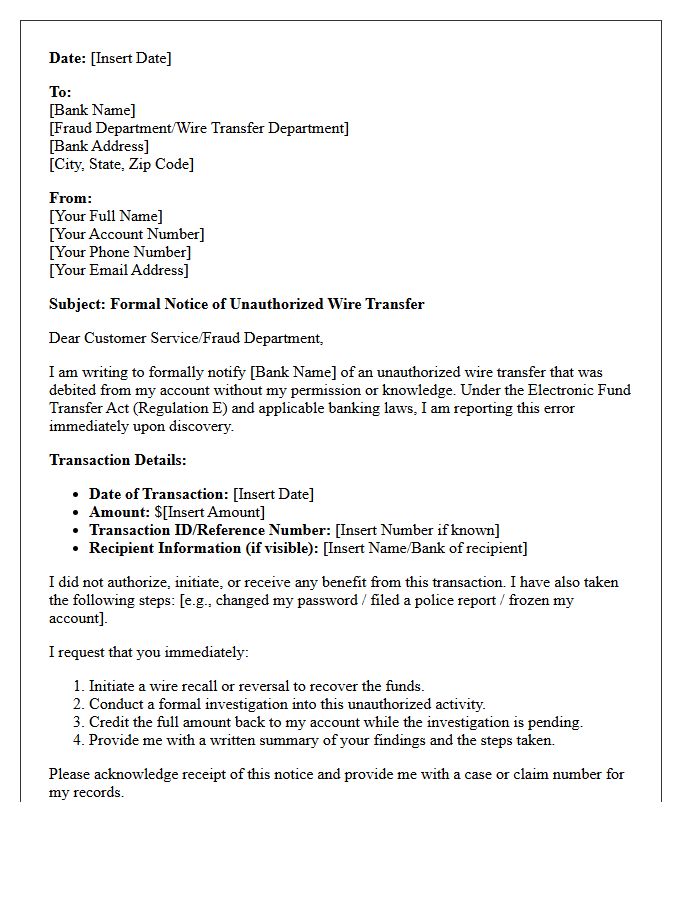

Initial Notice of Unauthorized Wire Transfer Letter

An Initial Notice of Unauthorized Wire Transfer Letter is a critical legal document used to alert your financial institution of fraudulent activity. Under Federal Regulation E or the Uniform Commercial Code, you must act quickly to limit your liability. This formal notification should include your account details, the specific transaction date, and the unauthorized amount. Sending this letter via certified mail provides a paper trail essential for recovering lost funds. Promptly reporting the error is the most effective way to protect your consumer rights and initiate a formal bank investigation.

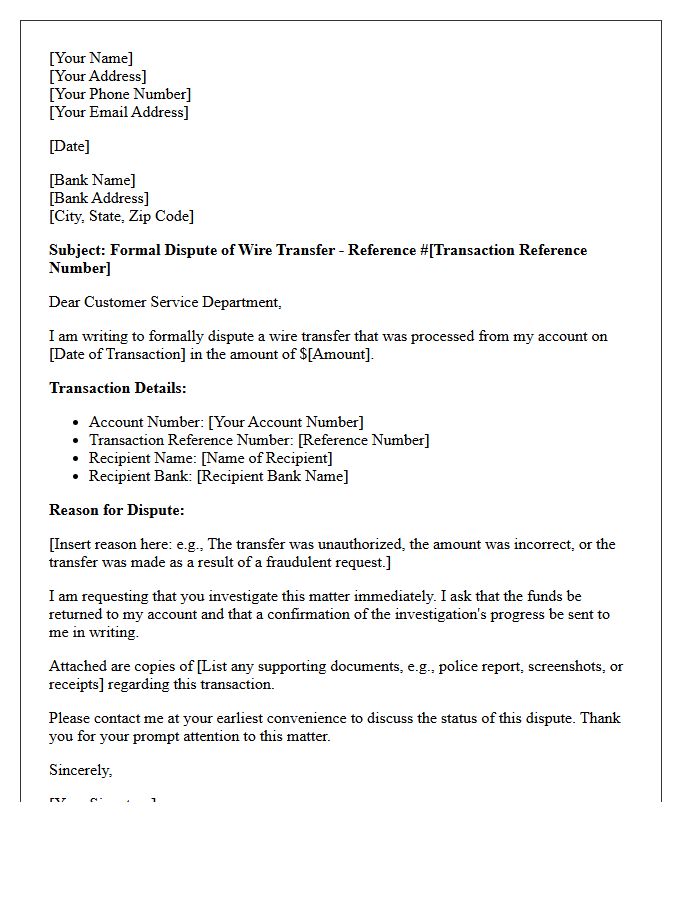

Formal Wire Transfer Dispute Letter

A Formal Wire Transfer Dispute Letter is a critical legal document used to contest unauthorized or erroneous electronic fund transfers. To protect your rights under the Electronic Fund Transfer Act, you must submit this written notice to your bank, typically within 60 days of the statement date. Ensure the letter includes your account details, the specific transaction amount, and a clear explanation of the billing error. Sending this via certified mail provides essential proof of delivery, ensuring the financial institution is legally obligated to investigate and resolve your dispute promptly.

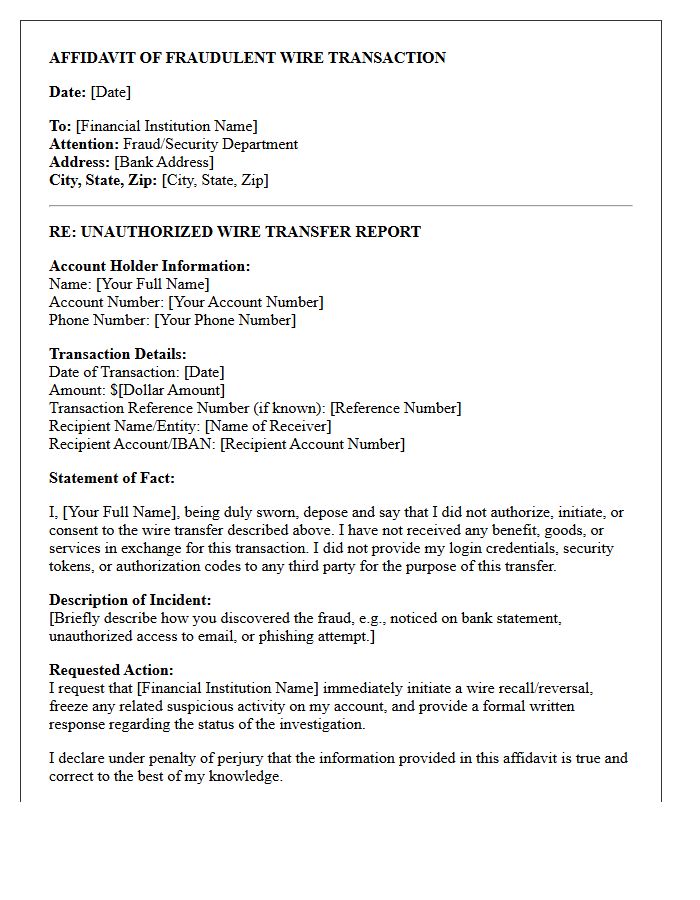

Fraudulent Wire Transaction Affidavit Letter

A Fraudulent Wire Transaction Affidavit Letter is a formal sworn statement used to dispute unauthorized fund transfers. It serves as essential legal evidence for banks to initiate a fraud investigation and potential recovery process. This document must clearly detail the transaction specifics, confirm the account holder did not authorize the payment, and be notarized to ensure its validity. Timely submission is critical to meeting financial institutions' reporting deadlines and maximizing the chances of recovering lost assets from cybercrime or identity theft.

Request for Wire Transfer Reversal Letter

A wire transfer reversal letter is a formal document used to request the recall of funds sent in error or due to fraud. It must include critical details like the transaction date, exact amount, and the recipient's banking information. Because wire transfers are generally irreversible, you must contact your bank immediately to initiate a recall request. Clearly state the reason for the reversal, such as a clerical mistake or unauthorized activity, to improve the chances of a successful recovery through the bank's interbank communication system.

Unauthorized Commercial Wire Dispute Letter

An Unauthorized Commercial Wire Dispute Letter is a formal legal notification sent to a financial institution to contest fraudulent electronic fund transfers. Under Uniform Commercial Code (UCC) Article 4A, businesses must report discrepancies immediately to maintain liability protections. The letter should specify the transaction date, amount, and reference number while asserting that the transfer was not authorized. Timely submission is critical, as commercial accounts lack the same consumer protections found in Regulation E, making rapid notification the primary way to recover lost corporate funds and mitigate potential losses.

Follow-Up Wire Transfer Investigation Letter

A Follow-Up Wire Transfer Investigation Letter is a formal request sent to a financial institution to trace missing funds or resolve discrepancies. This document provides critical details, such as the IMAD/OMAD sequence numbers, transaction dates, and amount. It ensures a written record exists for compliance and recovery efforts. Promptly sending this letter is essential if a recipient reports non-receipt despite a successful debit. Precise documentation helps banks initiate a tracer to locate assets within the global banking network efficiently.

Escalation of Unresolved Wire Fraud Letter

An Escalation of Unresolved Wire Fraud Letter is a formal demand sent when initial recovery efforts fail. This critical document targets senior bank executives and compliance officers to trigger internal investigations and legal review. It must detail the specific transaction timestamps, reporting history, and a clear request for a hold harmless agreement or fund reversal. Timely submission is vital to mitigate financial loss, ensure regulatory accountability, and provide necessary evidence for potential litigation or insurance claims regarding the stolen assets.

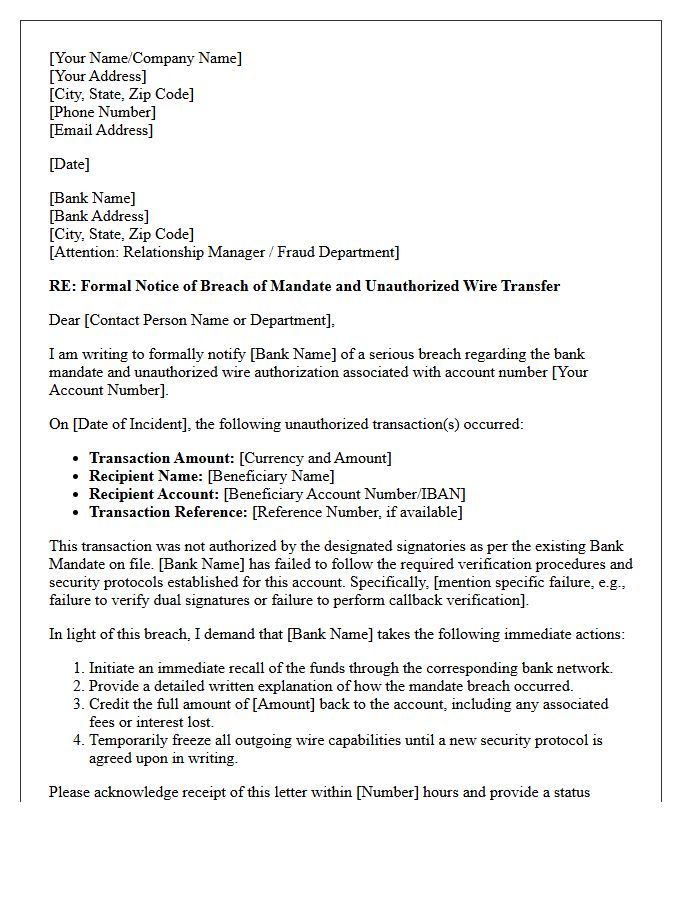

Bank Mandate and Wire Authorization Breach Letter

A Bank Mandate and Wire Authorization Breach Letter is a formal notification sent when unauthorized changes are made to corporate payment instructions. It serves as a legal alert to financial institutions that fraudulent activity has compromised sensitive banking data. Immediate issuance is critical to freezing accounts and initiating funds recovery protocols. This document documents the security failure, helps mitigate liability, and triggers internal cybersecurity investigations into potential business email compromise. Promptly reporting the breach ensures compliance and maximizes the chances of reversing fraudulent wire transfers before funds are permanently lost.

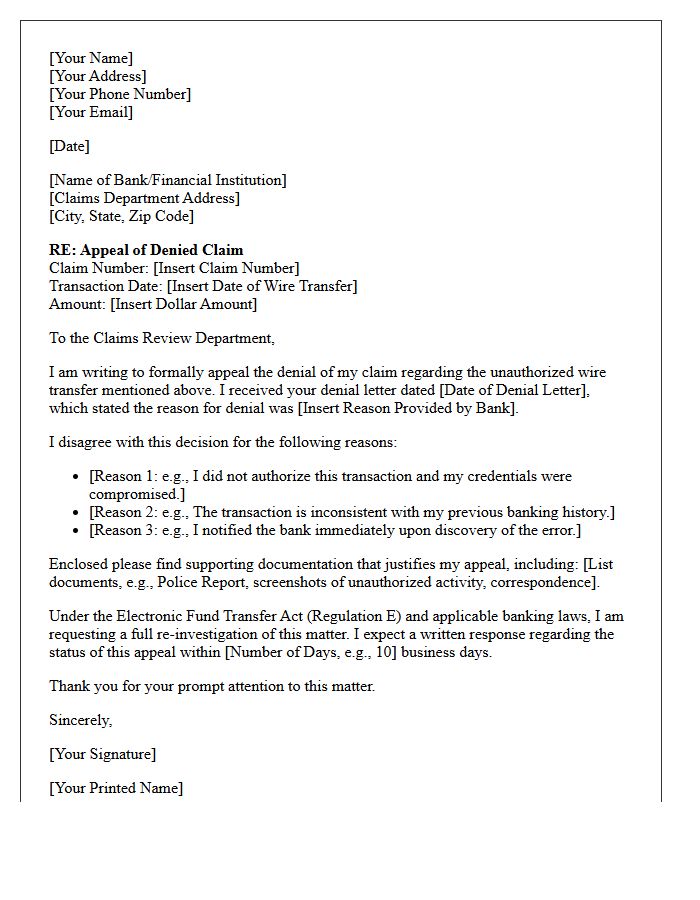

Appeal of Denied Wire Transfer Claim Letter

When drafting an Appeal of Denied Wire Transfer Claim Letter, you must provide new evidence to challenge the bank's initial decision. Clearly state why the transaction was unauthorized or fraudulent, referencing specific consumer protection regulations like Regulation E if applicable. Include copies of police reports, communication logs, and transaction receipts to strengthen your case. Be concise, adhere to the bank's strict appeal deadlines, and explicitly demand a formal re-investigation. A well-structured appeal increases your chances of recovering lost funds and correcting billing errors effectively.

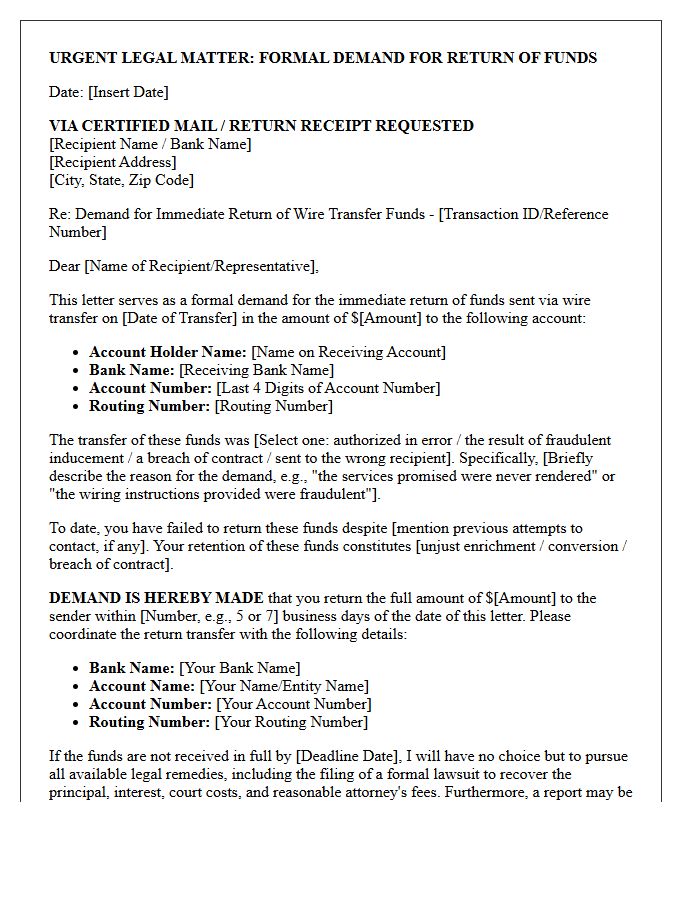

Pre-Litigation Wire Transfer Demand Letter

A Pre-Litigation Wire Transfer Demand Letter serves as a formal legal notice sent to financial institutions or recipients following fraudulent activity. Its primary purpose is to freeze disputed funds immediately and demand the reversal of unauthorized transactions. This document establishes a clear timeline of the incident, provides essential transaction details, and warns of impending legal action if the assets are not recovered. Sending this letter promptly is critical for demonstrating due diligence and maximizing the chances of successful asset recovery before funds are moved through multiple accounts.

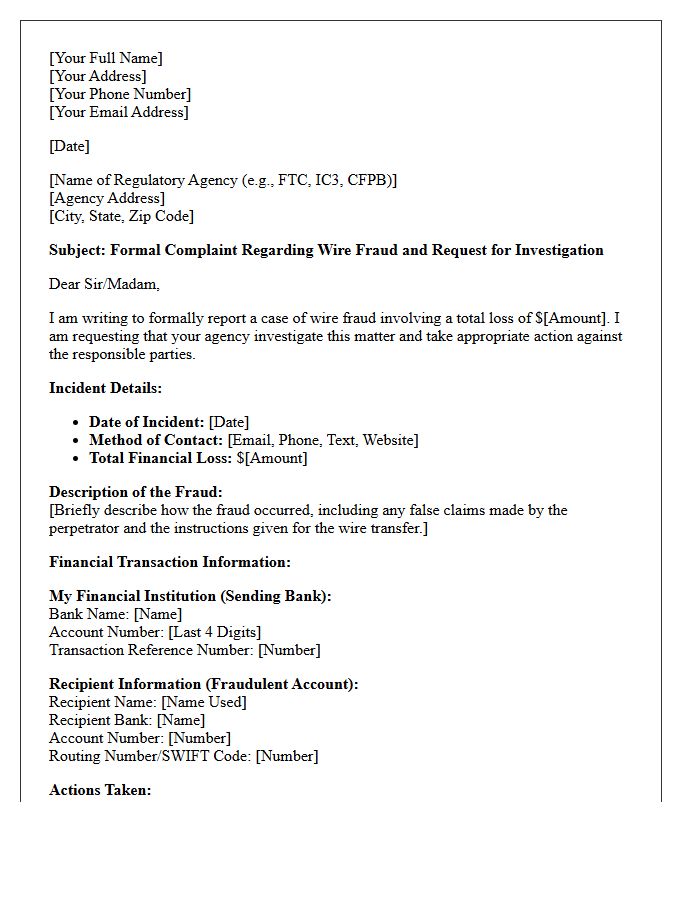

Regulatory Agency Wire Fraud Complaint Letter

A regulatory agency wire fraud complaint letter is a formal document used to report unauthorized electronic fund transfers to government bodies like the FBI or FTC. This letter must include precise details, such as transaction timestamps, recipient bank information, and the specific communication methods used by scammers. Filing this report promptly is crucial for the recovery of lost assets and helps authorities track criminal patterns. Providing a clear, chronological narrative of the incident strengthens the case for legal investigation and potential financial restitution from the involved banking institutions.

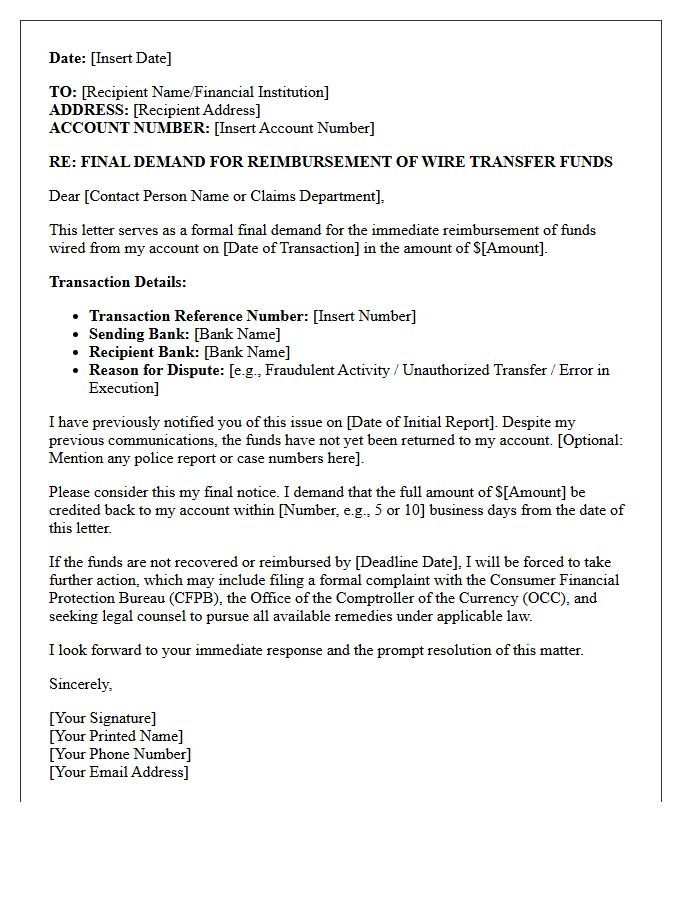

Final Demand for Wire Funds Reimbursement Letter

A final demand for wire funds reimbursement is a formal legal notice issued to recover money sent via electronic transfer. This document serves as the last opportunity for the recipient to return funds before litigation or formal legal action commences. It must clearly outline the specific transaction details, the reason for the claim, and a strict deadline for payment. Sending this letter is a critical step in demonstrating a good-faith effort to resolve the dispute, often required by courts to prove the debtor was properly notified of their obligation.

What steps should I take immediately if I discover an unauthorized wire transfer?

Contact your financial institution immediately to report the unauthorized transaction and request a "Wire Recall." Follow up with a written formal dispute, change your account credentials, and file a report with the Internet Crime Complaint Center (IC3) or your local law enforcement.

How long do I have to dispute an unauthorized wire transfer under federal law?

Under the Electronic Fund Transfer Act (Regulation E), consumers generally have up to 60 days from the date the bank statement reflecting the error was sent to report unauthorized electronic transfers. However, wire transfers are often governed by UCC Article 4A, which may have different notification requirements depending on your account agreement.

Am I liable for the funds lost in an unauthorized wire transfer?

Liability often depends on how quickly you report the activity and the security protocols in place. If the bank failed to follow commercially reasonable security procedures or if you reported the breach promptly, you may be entitled to a full refund. Conversely, negligence in safeguarding credentials may impact your recovery options.

Can a wire transfer be reversed once it has been completed?

Wire transfers are designed to be instantaneous and irreversible; however, a "Recall Request" can be initiated by the sending bank. Success depends on the receiving bank's cooperation and whether the recipient has already withdrawn the funds. If the funds are still in the recipient's account, the bank may freeze them pending investigation.

What is the difference between a wire transfer scam and an unauthorized wire transfer?

An unauthorized wire transfer occurs when a third party accesses your account without permission to move money. A wire transfer scam (or "authorized push payment fraud") occurs when you are deceived into voluntarily initiating the transfer yourself. Legal protections and reimbursement chances are typically higher for unauthorized transfers than for scams you authorized under false pretenses.

Comments