Experiencing a delay with an unprocessed account deposit can be frustrating and disrupt your financial planning. This guide explains how to effectively dispute missing funds, communicate with your bank, and provide the necessary transaction evidence to resolve the issue quickly. To help you take immediate action, below are some ready to use template.

Image cover: Resolving Unprocessed Deposits: Professional Dispute Letter Templates and Guide

Letter Samples List

- Initial Dispute Letter for Unprocessed ATM Cash Deposit

- Formal Dispute Letter for Uncredited Mobile Check Deposit

- Escalation Letter Regarding Missing Wire Transfer Deposit

- Follow-Up Dispute Letter for Delayed Branch Teller Deposit

- Letter of Dispute for Unprocessed Employer Direct Deposit

- Notice Letter for Unrecorded Night Depository Submission

- Second Request Dispute Letter for Unprocessed Account Deposit

- Final Demand Letter for Missing Bank Deposit Investigation

- Dispute Letter for Unprocessed International Fund Transfer

- Claim Letter for Missing Business Merchant Account Deposit

- Inquiry Letter for Unprocessed Automated Clearing House Deposit

- Official Dispute Letter for Uncredited Cashier Check Deposit

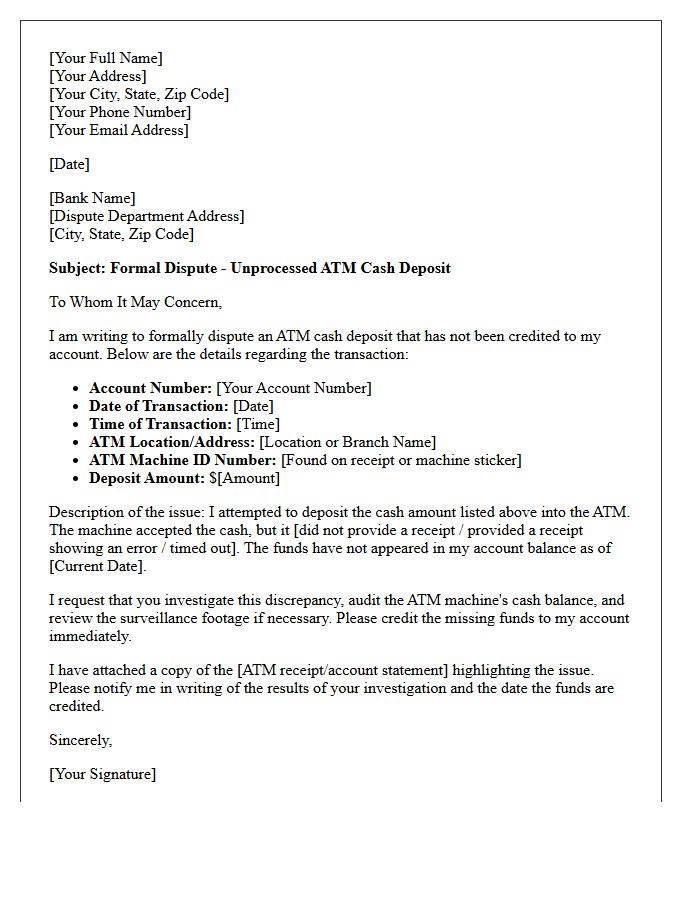

Initial Dispute Letter for Unprocessed ATM Cash Deposit

An Initial Dispute Letter is your primary legal protection when an ATM fails to credit a cash deposit. You must notify your bank immediately in writing to trigger rights under the Electronic Fund Transfer Act (Regulation E). Clearly state the transaction date, exact amount, machine location, and the specific error. Request a formal investigation and a provisional credit to your account while the bank audits the machine's physical cash logs and internal journals. Send this letter via certified mail to establish a formal paper trail for your claim.

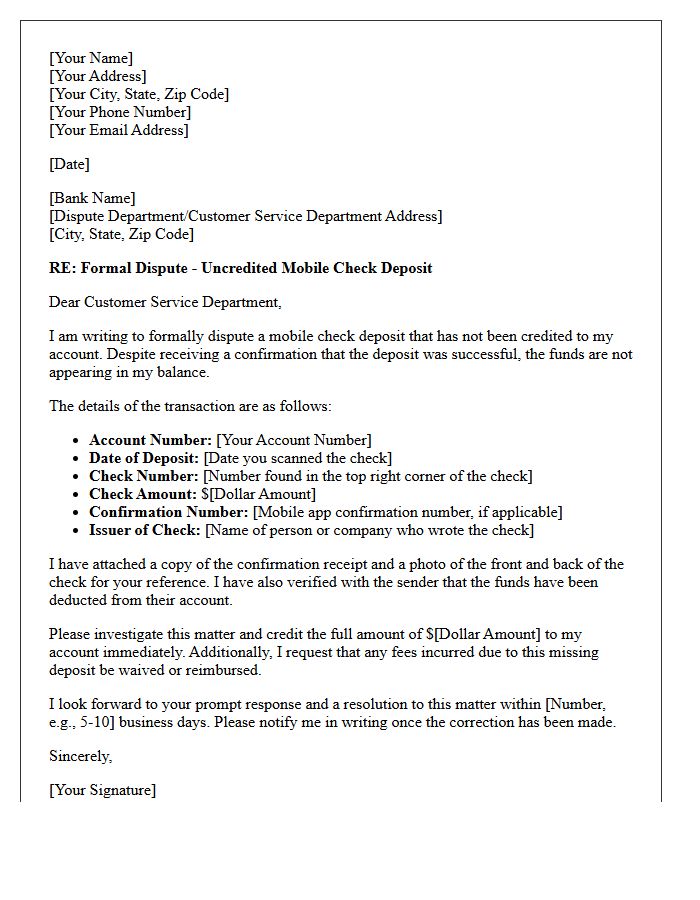

Formal Dispute Letter for Uncredited Mobile Check Deposit

When drafting a formal dispute letter for an uncredited mobile check deposit, clarity is essential. Clearly state your account details, the exact deposit amount, and the date of the transaction. Attach a copy of the check and the confirmation receipt provided by the mobile app as evidence. Demand a prompt investigation under Regulation E or applicable banking laws to resolve the missing funds. Send the letter via certified mail with a return receipt to ensure you have legal proof of delivery for your records.

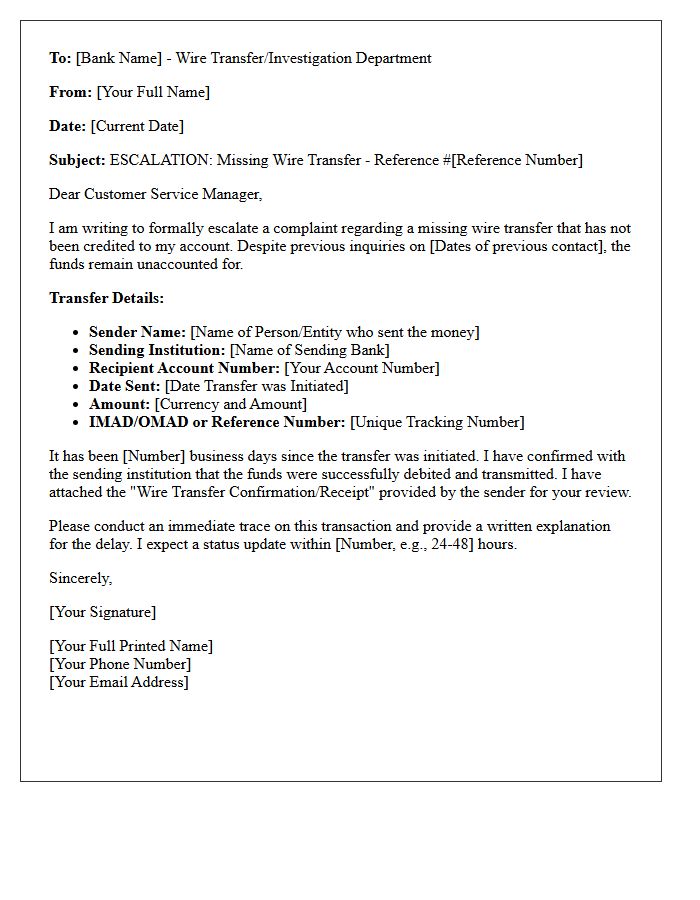

Escalation Letter Regarding Missing Wire Transfer Deposit

An escalation letter is a formal request sent to a bank's management or compliance department when a missing wire transfer remains unresolved through standard support. It must include the Federal Reference Number, exact amount, and date of the transaction to facilitate an immediate trace. Clearly document previous failed attempts to locate the funds and specify a deadline for a resolution. This document serves as critical evidence of your due diligence should you need to file a formal complaint with financial regulatory authorities or legal counsel.

Follow-Up Dispute Letter for Delayed Branch Teller Deposit

When a bank fails to credit a branch teller deposit within the promised timeframe, a follow-up dispute letter is essential for consumer protection. Clearly state the transaction date, location, and deposit amount while attaching a copy of your validated receipt. Explicitly reference the Electronic Fund Transfer Act to enforce your right to a timely investigation. Formally demand an immediate account adjustment or a written explanation for the delay. Maintaining a paper trail ensures regulatory compliance and provides critical evidence should you need to escalate the claim to the Consumer Financial Protection Bureau.

Letter of Dispute for Unprocessed Employer Direct Deposit

If your direct deposit remains unprocessed, you must submit a formal Letter of Dispute to your employer's payroll department immediately. This document serves as a legal record of the missing wages. Clearly state the expected payment date, the exact amount due, and your banking details to rule out administrative errors. Under federal laws like the FLSA, employers are required to pay employees promptly. Retaining a signed copy protects your rights if you need to escalate the claim to the Department of Labor for wage theft recovery.

Notice Letter for Unrecorded Night Depository Submission

A Notice Letter for an unrecorded night depository submission is a critical formal communication sent by a financial institution. It informs a customer that a reported deposit was not found or recorded within the vault. Upon receipt, you must immediately provide deposit slips, merchant logs, or surveillance proof to resolve the discrepancy. This notice is an essential security protocol designed to initiate a formal investigation into missing funds, ensuring account accountability and protecting against potential internal errors or external theft during the after-hours banking process.

Second Request Dispute Letter for Unprocessed Account Deposit

If your initial inquiry regarding a missing credit remains ignored, a Second Request Dispute Letter is essential for formal escalation. This follow-up correspondence serves as a written record of the financial institution's failure to resolve the unprocessed account deposit. You must re-attach your original deposit receipt and clearly state the previous reference number. Demanding an immediate investigation under banking regulations ensures your legal rights are protected. Sending this document via certified mail provides critical proof of delivery, strengthening your case for potential regulatory intervention if the funds are not credited promptly.

Final Demand Letter for Missing Bank Deposit Investigation

A final demand letter is a critical legal document issued when a financial institution fails to resolve a missing bank deposit investigation within the promised timeframe. It serves as a formal ultimatum, highlighting the bank's liability and your intent to escalate the matter to regulatory bodies or legal counsel. This letter must clearly state the disputed amount, transaction dates, and a strict deadline for resolution. Providing conclusive evidence, such as deposit receipts or digital logs, is essential to prove the loss and compel the bank to rectify the accounting error immediately.

Dispute Letter for Unprocessed International Fund Transfer

When sending a dispute letter for an unprocessed international fund transfer, time is critical. Clearly state your transaction reference number, the exact amount, and the date of the request. Explicitly mention the recipient's details and the SWIFT/BIC code used. Demand a formal investigation under Regulation E or local banking laws to trace the funds. Attach proof of the original transfer request and any communication from the receiving bank confirming non-receipt. This formal documentation protects your consumer rights and forces the financial institution to resolve the missing wire transfer promptly.

Claim Letter for Missing Business Merchant Account Deposit

A claim letter for a missing merchant account deposit is a formal request to your payment processor to investigate undeposited funds. It must include your merchant ID, exact transaction dates, and the total missing amount to facilitate a quick trace. Attaching point-of-sale reports and bank statements serves as vital evidence of the discrepancy. Timely submission is critical, as many processors have strict dispute windows. Clear documentation ensures the processor can reconcile their records and restore your business cash flow efficiently.

Inquiry Letter for Unprocessed Automated Clearing House Deposit

An Inquiry Letter for an unprocessed ACH deposit is a formal request sent to a financial institution to track a missing electronic transfer. To resolve the issue, clearly state the transaction date, exact amount, and routing details. Providing the Trace Number is essential, as it allows banks to locate the funds within the banking network. Use this letter to formally document the delay and request an immediate status update or manual reconciliation to ensure the deposit is correctly credited to your account.

Official Dispute Letter for Uncredited Cashier Check Deposit

An Official Dispute Letter is a formal legal notice used to resolve an uncredited cashier check deposit. It must include the check number, exact amount, and the date of transaction. Under Federal Regulation CC, banks have specific timelines for fund availability. Explicitly request a formal investigation and provide a copy of your deposit receipt as evidence. Send the document via certified mail to establish a verifiable paper trail. This written record protects your consumer rights if the financial institution fails to rectify the accounting error or missing credit promptly.

What should I do if my account deposit has not been processed?

If your deposit is not reflecting in your account after the standard processing time, you should first verify the transaction status with your bank and then contact our billing support team with your transaction reference number and proof of payment to initiate a formal trace.

How long does it typically take to resolve a disputed deposit?

Most unprocessed deposit disputes are resolved within 3 to 5 business days. This timeframe allows our financial department to coordinate with payment processors to locate the funds and manually credit them to your account balance.

What documentation is required to file a dispute for a missing deposit?

To expedite your claim, you must provide a digital copy of the transaction receipt or a bank statement screenshot that clearly displays the date, the exact amount, the merchant name, and the unique transaction ID or reference number.

Can I cancel a pending deposit that is taking too long to process?

Once a deposit transaction has been initiated through a banking gateway, it cannot be canceled manually. If the funds have left your bank but are not visible in your account, you must wait for the verification period to end before filing a dispute for a manual adjustment.

Why is my deposit showing as "Pending" or "Unprocessed" for several days?

Deposits may be delayed due to bank verification procedures, international wire transfer clearing times, or incorrect account details provided during the transaction. If the status does not update within 48 hours, a formal dispute should be lodged to investigate the bottleneck.

Comments