Victims of digital scams must act quickly to recover lost funds. Submitting a formal Request for Resolution of Peer-to-Peer Payment Fraud to your financial institution is a critical step in disputing unauthorized transactions and seeking reimbursement. This guide explains how to document the incident effectively to strengthen your claim. To help you get started, below are some ready to use template.

Image cover: Securing Your Funds: P2P Payment Fraud Dispute Templates and Resolution Guide

Letter Samples List

- Formal Dispute Letter for Fraudulent Peer-to-Peer Payment

- Request Letter for Investigation of Unauthorized Peer-to-Peer Transfer

- Peer-to-Peer Payment Fraud Resolution Request Letter

- Letter Requesting Provisional Credit for Peer-to-Peer Fraud

- Escalation Letter for Unresolved Peer-to-Peer Payment Scam

- Appeal Letter for Denied Peer-to-Peer Fraud Dispute

- Letter of Demand for Reversal of Fraudulent Peer-to-Peer Transaction

- Affidavit Letter for Peer-to-Peer Account Takeover Fraud

- Victim Statement Letter for Peer-to-Peer Financial Fraud Resolution

- Letter of Complaint to Bank Compliance Regarding Peer-to-Peer Fraud

- Request Letter for Final Decision on Peer-to-Peer Fraud Claim

- Demand Letter for Restitution of Stolen Peer-to-Peer Funds

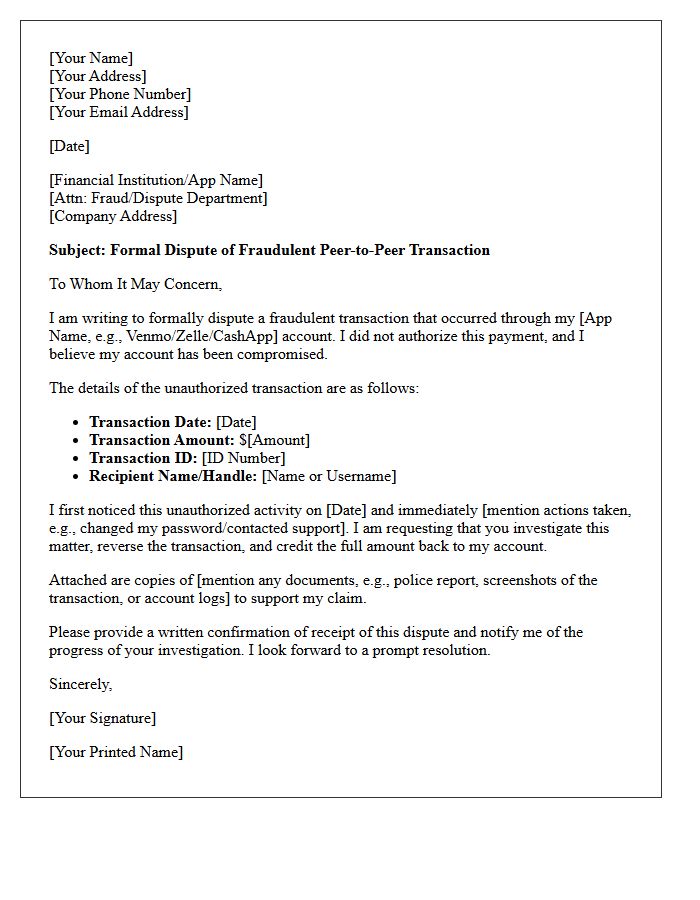

Formal Dispute Letter for Fraudulent Peer-to-Peer Payment

When drafting a formal dispute letter for a fraudulent peer-to-peer payment, you must clearly state that the transaction was unauthorized. Under Regulation E, consumers have specific protections against electronic fund transfer errors. Include your account details, the exact transaction date, and the specific amount stolen. Explicitly request a permanent credit and an investigation into the security breach. Sending this document via certified mail provides a legal paper trail, ensuring the financial institution acknowledges your claim within the required statutory timeframe to recover your lost funds effectively.

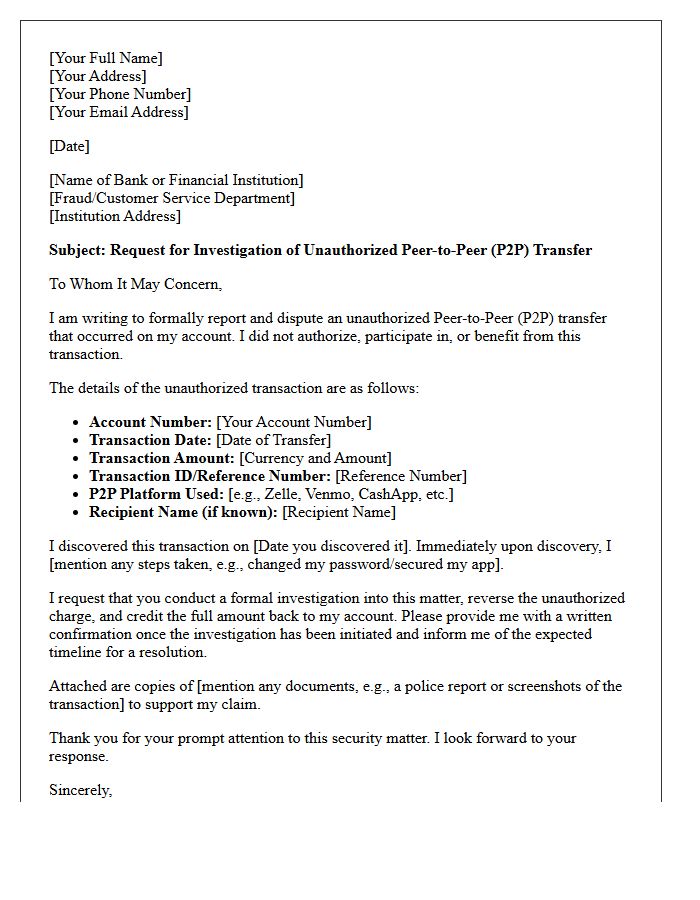

Request Letter for Investigation of Unauthorized Peer-to-Peer Transfer

A request letter for investigation of unauthorized peer-to-peer transfer is a formal legal notice sent to a financial institution to dispute a transaction. It is crucial to clearly document the specific date, amount, and recipient of the unauthorized transfer. To protect your rights under consumer protection laws, you must highlight the lack of authorization and demand a formal fraud investigation. Submitting this request promptly is essential to recover lost funds and ensure your account security is restored following a potential breach or digital scam.

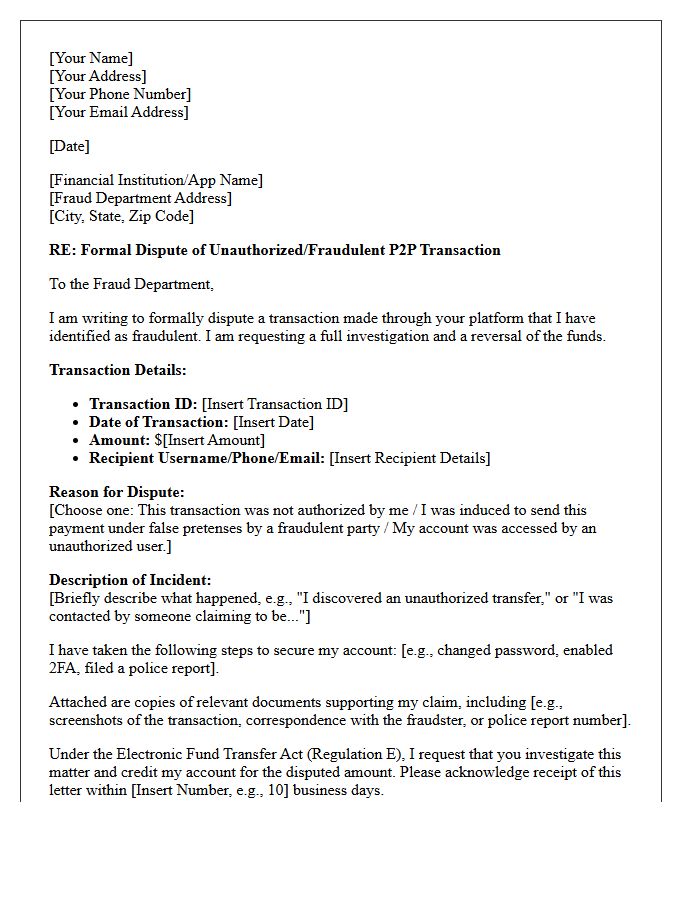

Peer-to-Peer Payment Fraud Resolution Request Letter

When drafting a Peer-to-Peer Payment Fraud Resolution Request Letter, it is crucial to clearly state the unauthorized transaction details, including the date, amount, and recipient. To strengthen your claim, emphasize the Regulation E protections that safeguard consumers against electronic fund transfer errors. Formally request an immediate investigation and a full refund of the stolen funds. Send this document via certified mail to maintain a paper trail. Providing documented evidence of the scam or unauthorized access ensures the financial institution handles your dispute with the necessary urgency and legal compliance.

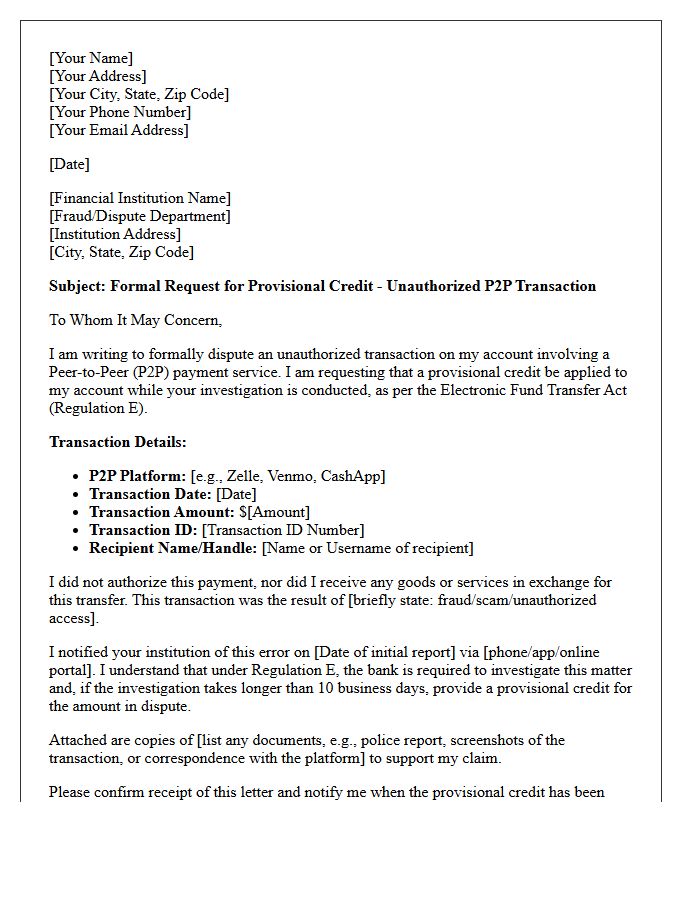

Letter Requesting Provisional Credit for Peer-to-Peer Fraud

When drafting a Letter Requesting Provisional Credit for peer-to-peer fraud, clearly cite the Electronic Fund Transfer Act (Regulation E). Explicitly state that the transaction was unauthorized and request an immediate investigation. Banks are often required to provide a temporary credit within ten business days if the inquiry takes longer. Ensure you include the specific date, amount, and recipient details to expedite the process. Sending this formal notice via certified mail creates a vital legal paper trail to protect your consumer rights during financial disputes.

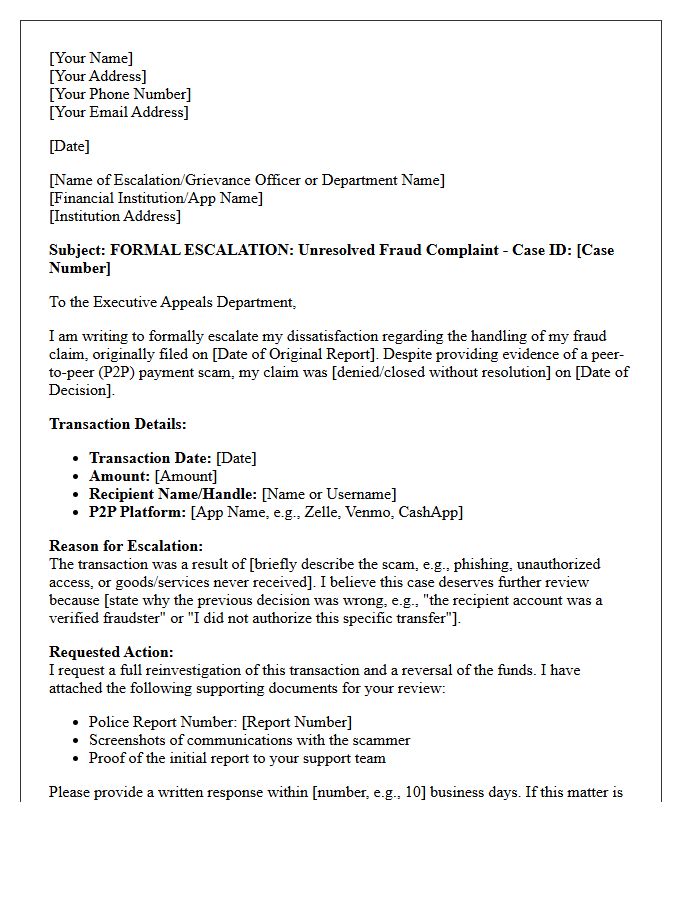

Escalation Letter for Unresolved Peer-to-Peer Payment Scam

When formal disputes fail, an Escalation Letter is your final demand for restitution regarding an unresolved peer-to-peer payment scam. This document should clearly outline the fraudulent transaction details, previous communication logs, and the platform's failure to provide consumer protection under Electronic Fund Transfer regulations. Address the letter to the financial institution's legal or executive office, signaling your intent to involve the Consumer Financial Protection Bureau (CFPB) or legal counsel. Professional persistence often forces a manual review, increasing the likelihood of recovering lost funds from recalcitrant payment services or banks.

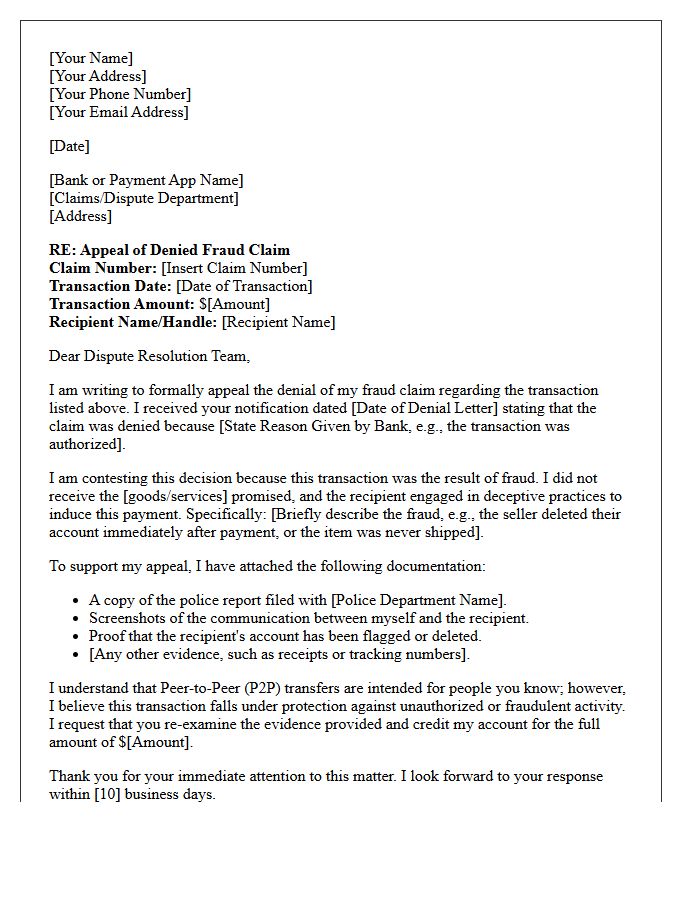

Appeal Letter for Denied Peer-to-Peer Fraud Dispute

When drafting an appeal letter for a denied peer-to-peer fraud dispute, focus on providing new evidence that proves the transaction was unauthorized. Clearly outline the timeline, include police reports, and highlight any security breaches or identity theft documentation. Emphasize that you did not authorize the payment and did not receive any goods or services in exchange. Formally request a reinvestigation under the Electronic Fund Transfer Act (Regulation E) to protect your consumer rights and recover lost funds from the financial institution or payment platform.

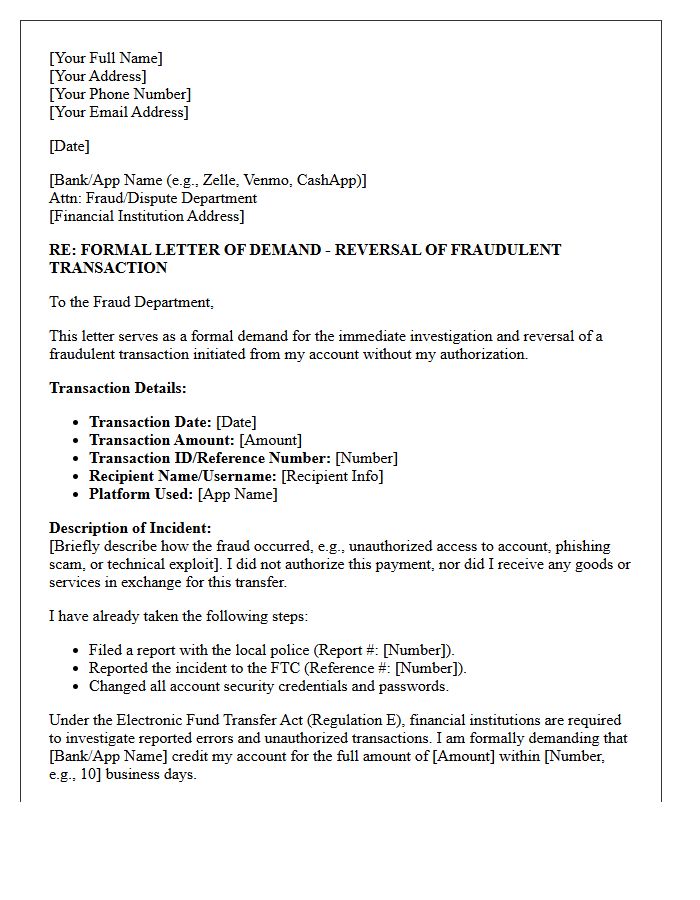

Letter of Demand for Reversal of Fraudulent Peer-to-Peer Transaction

A Letter of Demand is a formal legal notice used to dispute unauthorized activity. When addressing a fraudulent peer-to-peer transaction, this document officially requests a reversal of funds from the recipient or financial institution. It must clearly outline the specific transaction details, evidence of the scam, and a strict deadline for the restitution of assets. Sending this letter serves as a critical prerequisite for potential litigation or police reports, demonstrating that you have made a formal attempt to resolve the financial loss before escalating to legal action.

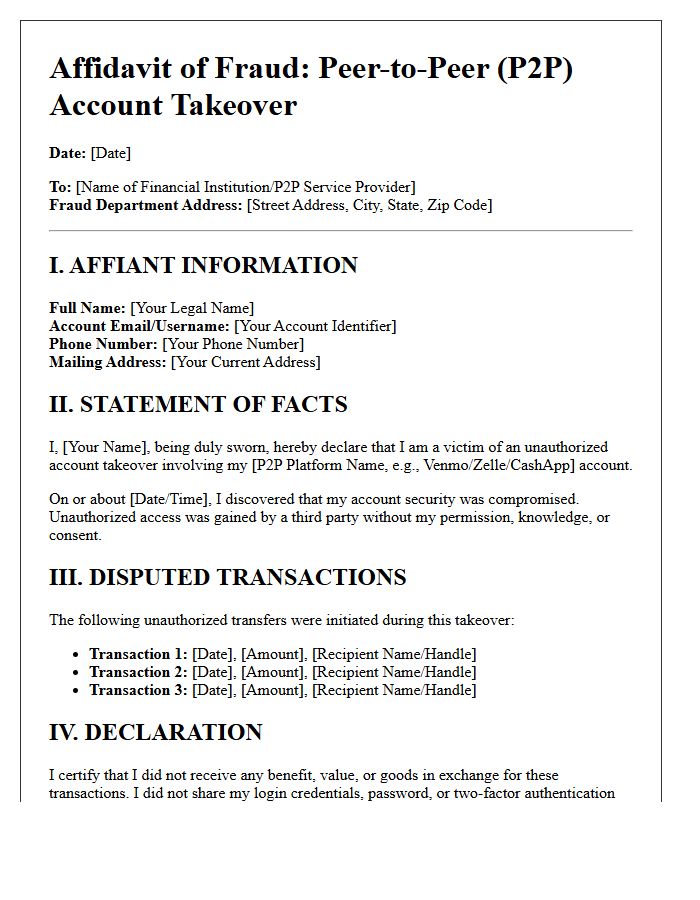

Affidavit Letter for Peer-to-Peer Account Takeover Fraud

An affidavit letter serves as a formal sworn statement used to dispute unauthorized transactions during a peer-to-peer account takeover. This legal document verifies that you did not authorize the fraudulent activity and provides essential evidence for financial institutions or law enforcement. It should clearly detail the timeline of the breach, specific unauthorized transfers, and any security compromises. Submitting an accurate affidavit is the most critical step in initiating a formal fraud investigation to recover lost funds and restore your digital identity after a malicious hijacking occurs.

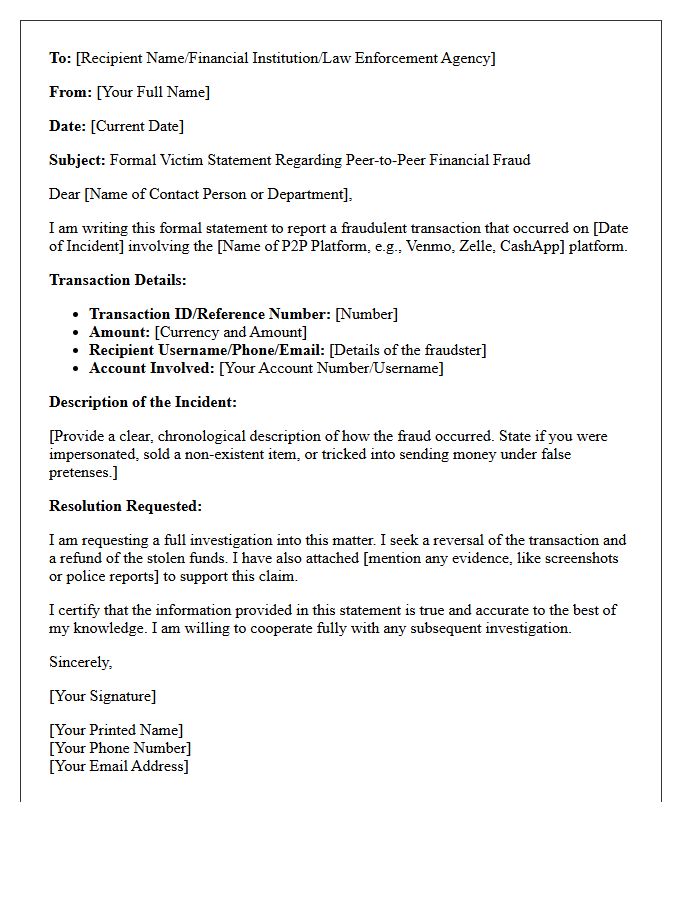

Victim Statement Letter for Peer-to-Peer Financial Fraud Resolution

A victim statement letter is a critical document used to explain the personal and financial impact of Peer-to-Peer (P2P) fraud to authorities or financial institutions. To improve your chances of restitution, you must provide a clear, chronological account of the transaction details and the deceptive tactics used by the scammer. Clearly stating the emotional distress and monetary loss helps investigators prioritize your case. Ensure you attach supporting evidence, such as chat logs and transaction receipts, to create a formal record for a successful resolution and potential fund recovery.

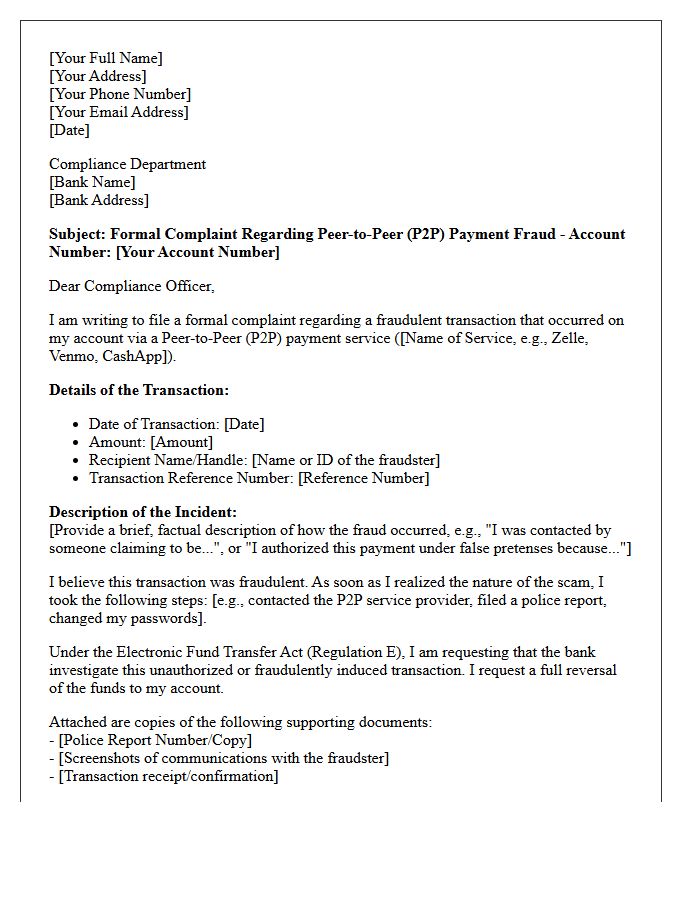

Letter of Complaint to Bank Compliance Regarding Peer-to-Peer Fraud

When drafting a formal complaint regarding peer-to-peer (P2P) fraud, clearly state you are disputing an unauthorized transaction or a victim of deception. Explicitly request a formal reclamation of funds under the bank's internal compliance protocols. Detail the specific platform used, the timeline of events, and any evidence of the scam. Emphasize the bank's duty of care and regulatory obligations to investigate fraudulent activity. Sending this letter creates a critical paper trail for potential escalations to financial ombudsmen or regulatory bodies if the initial recovery attempt is denied by the financial institution.

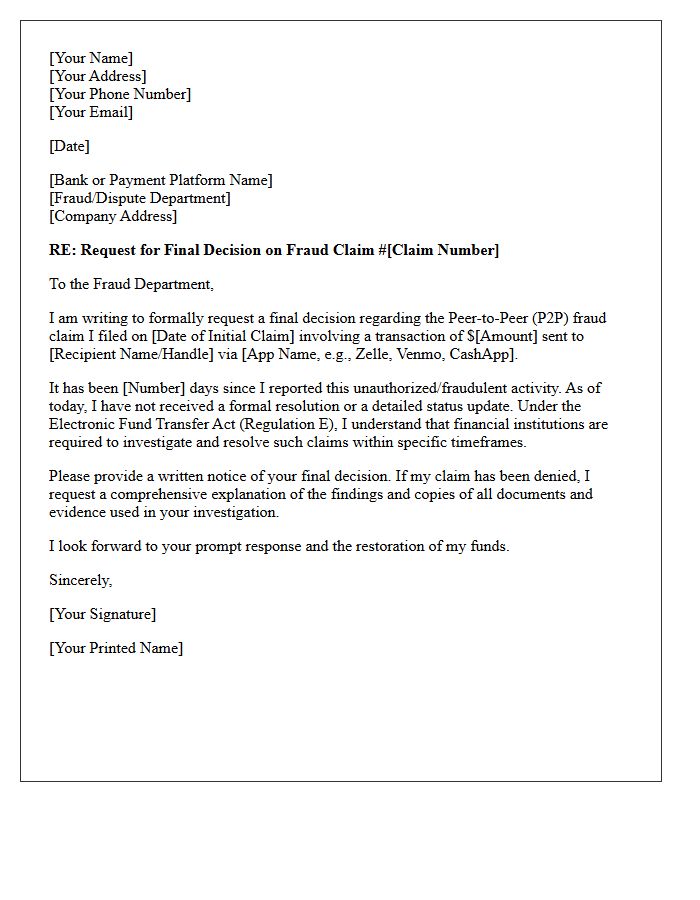

Request Letter for Final Decision on Peer-to-Peer Fraud Claim

When drafting a Request Letter for Final Decision on a peer-to-peer fraud claim, clarity is essential. Formally state your case by referencing the specific transaction ID, date, and disputed amount. Explicitly mention that you are seeking a formal resolution under Electronic Fund Transfer Act protections or platform policies. Include any new evidence, such as police reports or communication logs, to support your fraud claim. Demand a written explanation for the final determination to ensure your rights are protected during the appeals process if the reimbursement is denied.

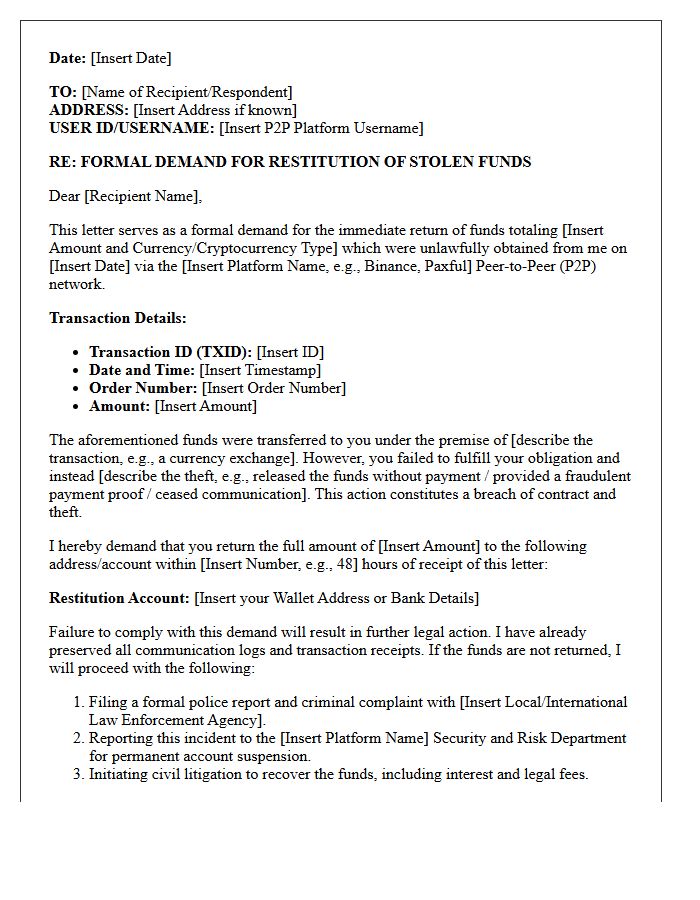

Demand Letter for Restitution of Stolen Peer-to-Peer Funds

A Demand Letter for Restitution is a formal legal notice used to recover money lost through P2P payment fraud or unauthorized transfers. It serves as a pre-litigation strategy, explicitly documenting the theft and demanding the return of funds by a specific deadline. Sending this letter is essential because it establishes a formal record of dispute required by many financial institutions and courts. By citing consumer protection regulations, such as Electronic Fund Transfer Act provisions, victims can pressure recipients or platforms to resolve the unlawful conversion of assets before escalating to a lawsuit.

What steps should I take immediately after discovering peer-to-peer (P2P) payment fraud?

Immediately notify your bank or the payment app provider to report the unauthorized transaction and request a payment reversal. You should also change your account passwords, enable two-factor authentication, and file a formal police report to document the incident for your claim.

Can I get a refund for a fraudulent peer-to-peer payment?

Refund eligibility depends on the platform's terms and the nature of the fraud; while unauthorized transfers are often protected under the Electronic Fund Transfer Act (Regulation E), voluntary payments made to scammers are harder to recover. Submitting a formal request for resolution with supporting evidence is essential to start the recovery process.

How do I write a formal request for resolution of payment fraud?

Your request should include your full contact information, the transaction ID, the date and amount of the transfer, the recipient's details, and a clear explanation of why the charge is fraudulent. Attach supporting documents such as screenshots of conversations or a copy of your police report to strengthen your case.

How long does a bank have to investigate a reported P2P fraud claim?

Under federal regulations, financial institutions generally have 10 business days to investigate a reported unauthorized electronic transfer. If the investigation takes longer, they may be required to provide a provisional credit to your account while they conclude their findings.

What should I do if my request for resolution is denied by the payment platform?

If your claim is denied, ask the provider for the specific documents used in their investigation and file an appeal. You can also escalate the dispute by filing a complaint with the Consumer Financial Protection Bureau (CFPB) or your state's Attorney General's office.

Comments