Late payments often trigger financial consequences defined in contractual agreements. This guide explains how to issue a formal Demand for Payment of Accrued Penalty Fees to recover outstanding interest and administrative charges effectively. Learn the legal requirements for enforcement and professional communication strategies to ensure compliance. To simplify your process, below are some ready to use template.

Image cover: Official Notice Templates for Demanding Accrued Penalty Fee Payments

Letter Samples List

- First Demand Letter for Accrued Overdraft Penalty Fees

- Final Demand Letter for Commercial Loan Late Payment Penalties

- Official Letter of Demand for Outstanding Mortgage Penalty Fees

- Formal Demand Letter for Accrued Credit Card Default Penalties

- Legal Demand Letter for Unpaid Banking Facility Penalty Fees

- Urgent Demand Letter for Accrued Trade Finance Penalty Charges

- Pre-Litigation Demand Letter for Corporate Account Penalty Fees

- Second Notice Demand Letter for Accrued Personal Loan Penalties

- Statutory Demand Letter for Unsettled Syndicate Loan Penalty Fees

- Notice of Default and Demand Letter for Accrued Covenant Breach Penalties

- Final Warning Demand Letter for Accrued Auto Financing Penalty Fees

- Official Demand Letter for Delinquent Business Account Penalty Fees

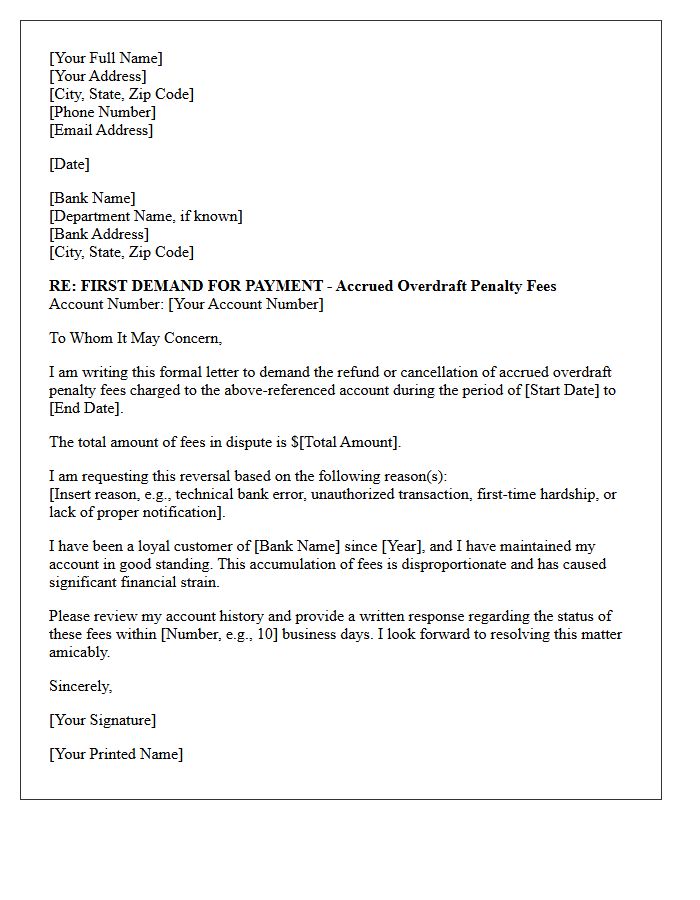

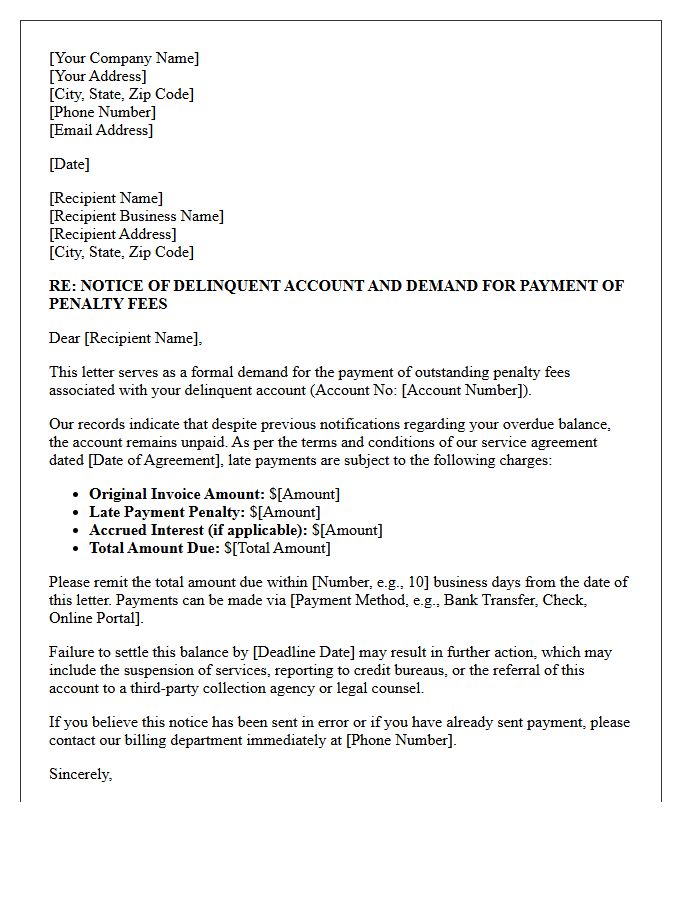

First Demand Letter for Accrued Overdraft Penalty Fees

A first demand letter for accrued overdraft penalty fees is a formal notice sent to a bank or financial institution to dispute or request the reversal of excessive charges. It must clearly outline the specific account details, the total amount in question, and the legal or contractual grounds for the refund. This document serves as critical evidence of your attempt to resolve the issue before escalating to regulatory bodies or legal action. Ensuring a professional tone and providing a clear deadline for a response is essential for an effective resolution.

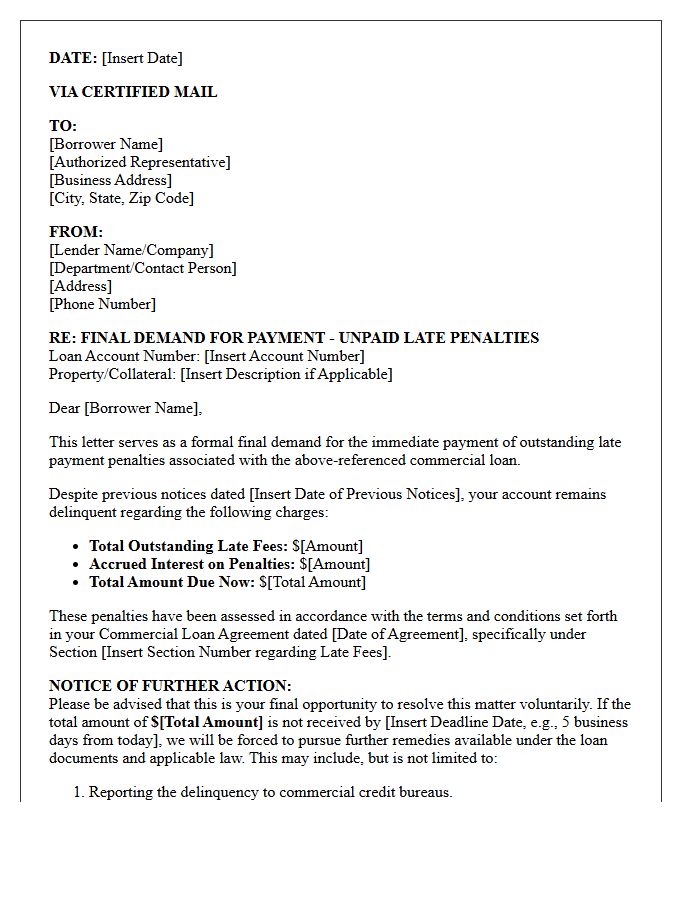

Final Demand Letter for Commercial Loan Late Payment Penalties

A Final Demand Letter serves as the ultimate formal notice before a commercial lender initiates legal action or foreclosure. This document specifies the exact late payment penalties, accrued interest, and principal balance owed. It establishes a strict deadline for remediation, making it a critical piece of evidence in debt recovery litigation. Recipients must act immediately to negotiate a settlement or provide proof of payment to avoid severe credit damage and the acceleration of the entire loan balance, which mandates full repayment of the debt instantly.

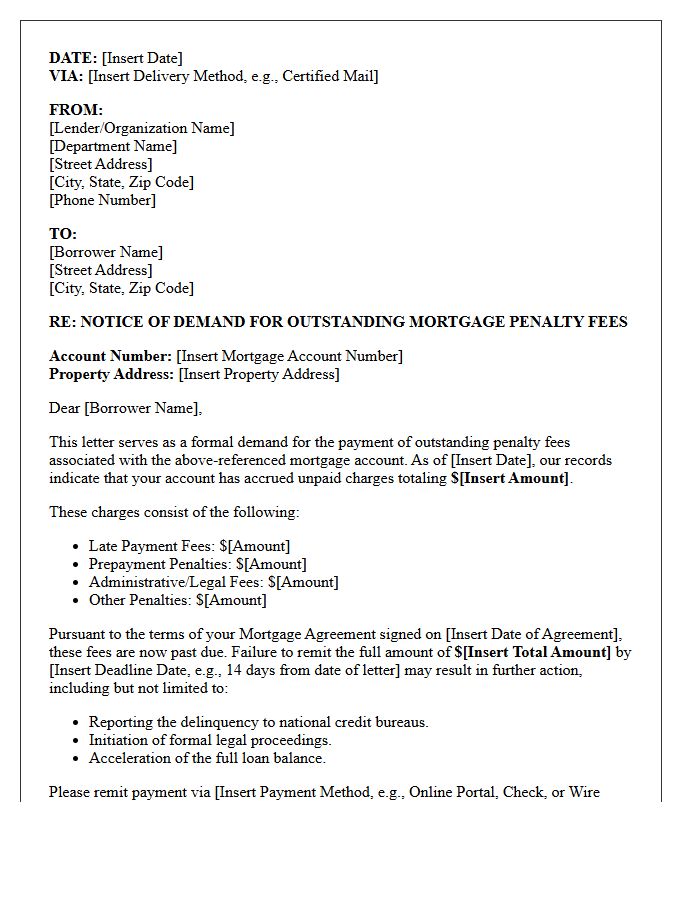

Official Letter of Demand for Outstanding Mortgage Penalty Fees

An official letter of demand for outstanding mortgage penalty fees serves as a formal legal notice requiring immediate payment of overdue charges. This document outlines specific contractual breaches, detailing late payment penalties or administrative fees accrued. It acts as a final warning before a lender initiates foreclosure proceedings or debt recovery litigation. Recipients must act swiftly to verify the accuracy of the stated amounts and negotiate a settlement or provide proof of payment to protect their property rights and maintain credit stability.

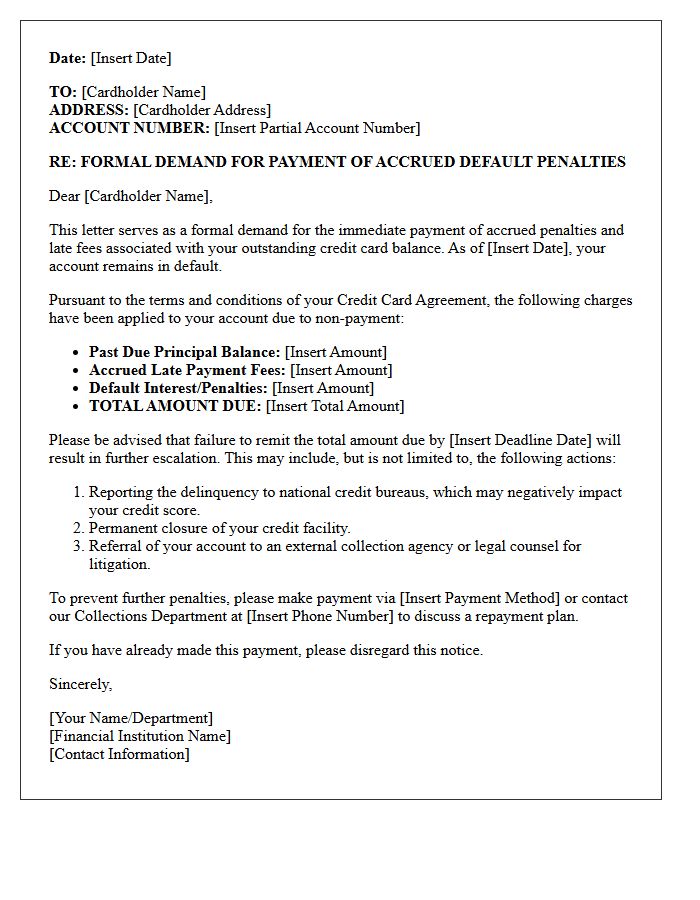

Formal Demand Letter for Accrued Credit Card Default Penalties

A formal demand letter for accrued credit card default penalties serves as a final legal notice before litigation or debt collection. It explicitly outlines the total outstanding balance, including contractual late fees and penalty interest rates triggered by a breach of terms. This document establishes a formal timeline for repayment to avoid further legal escalation. Recipients must verify the accuracy of the penalty calculations against their original cardholder agreement to ensure compliance with consumer protection laws and to prevent unfair debt collection practices.

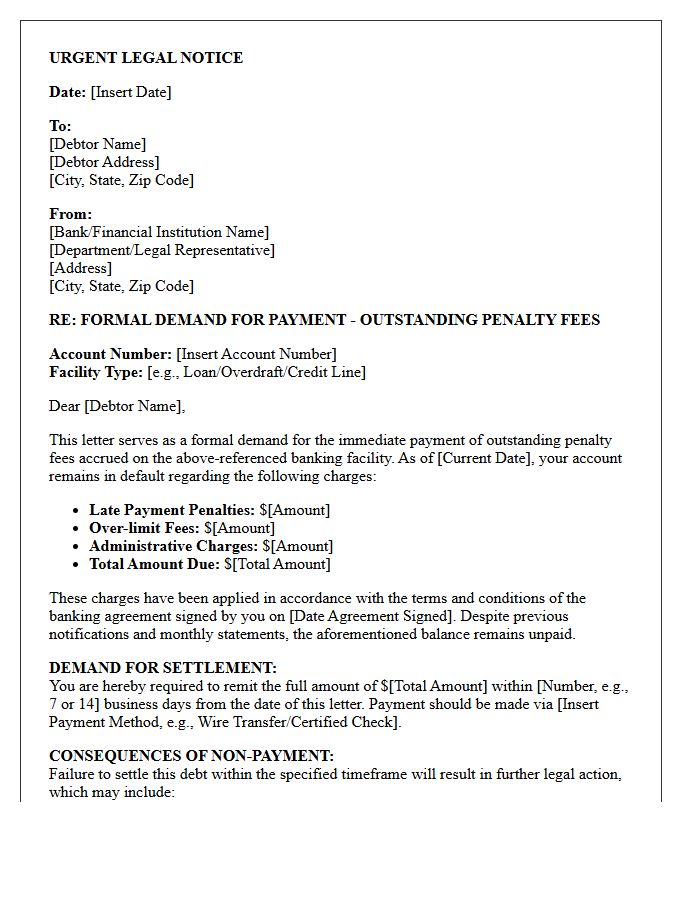

Legal Demand Letter for Unpaid Banking Facility Penalty Fees

A legal demand letter serves as a formal notice to resolve unpaid banking facility penalty fees before litigation. It outlines the specific outstanding balance, including accrued interest and administrative charges, as per the credit agreement. This document establishes a clear deadline for payment and acts as critical evidence of a creditor's attempt to settle the debt amicably. Receiving this letter indicates that the financial institution may initiate legal proceedings or asset recovery if the default persists. Prompt response or negotiation is essential to avoid further legal costs and negative impacts on your credit rating.

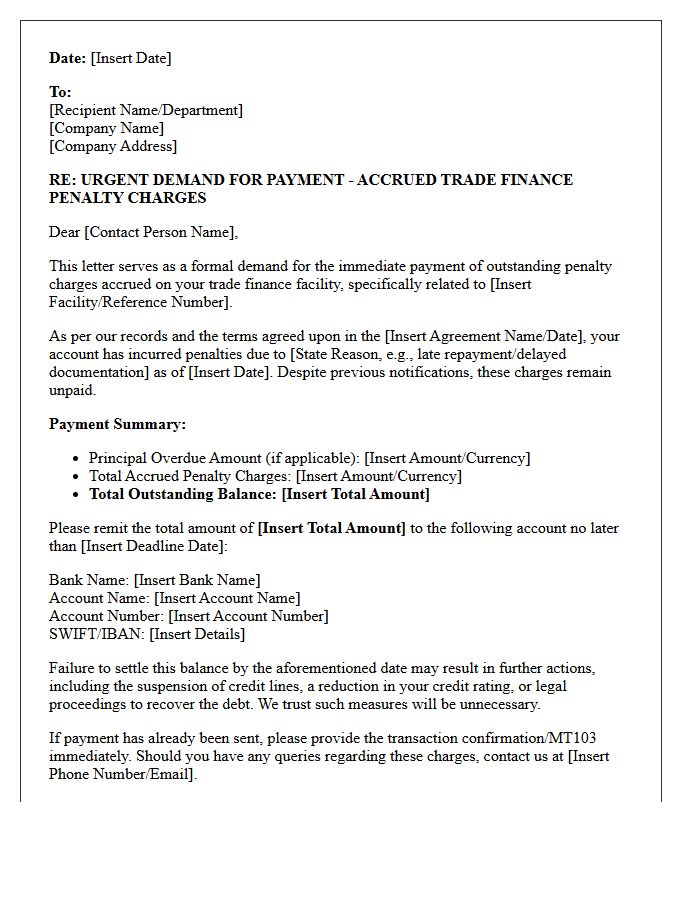

Urgent Demand Letter for Accrued Trade Finance Penalty Charges

An Urgent Demand Letter serves as a formal notification requiring immediate payment of accrued trade finance penalty charges. These fees typically arise from late payments, document discrepancies, or breaches in credit facility terms. Ignoring this notice can lead to legal action, a default status, and severe damage to your corporate credit rating. It is essential to review the underlying loan agreement, verify the penalty calculations, and respond promptly with either a payment confirmation or a formal dispute to mitigate further financial liabilities and maintain banking relationships.

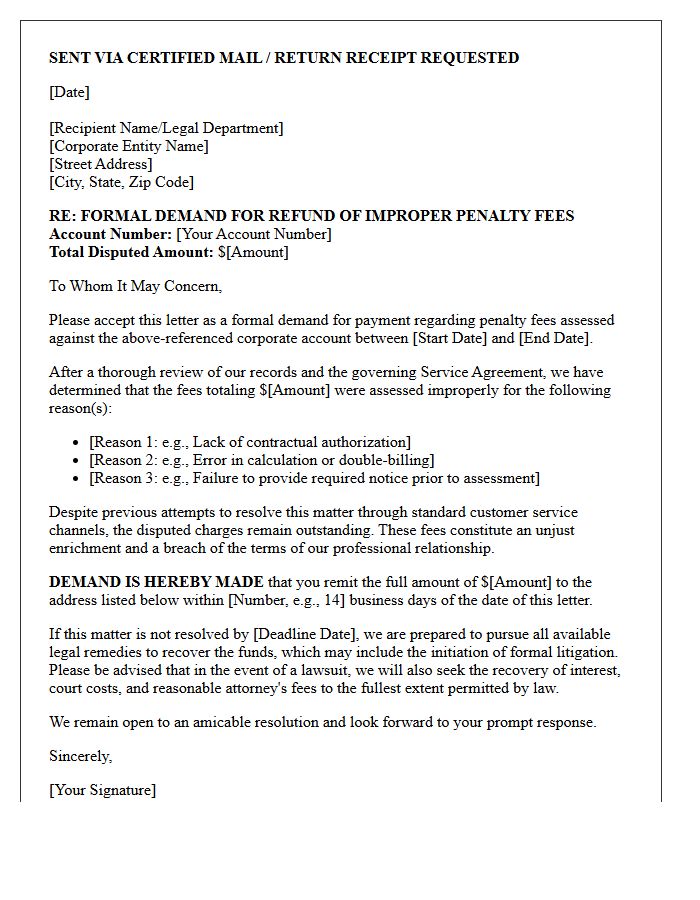

Pre-Litigation Demand Letter for Corporate Account Penalty Fees

A Pre-Litigation Demand Letter serves as a formal legal notice to a company disputing excessive corporate account penalty fees. It outlines the specific charges contested, identifies potential breaches of contract or consumer law, and sets a strict deadline for resolution. This document is essential because it demonstrates a good-faith effort to settle the conflict outside of court, often required by judges. By clearly stating legal grounds and intent to sue, it pressures corporations to waive unfair assessments and provides a critical evidentiary paper trail for future litigation or arbitration proceedings.

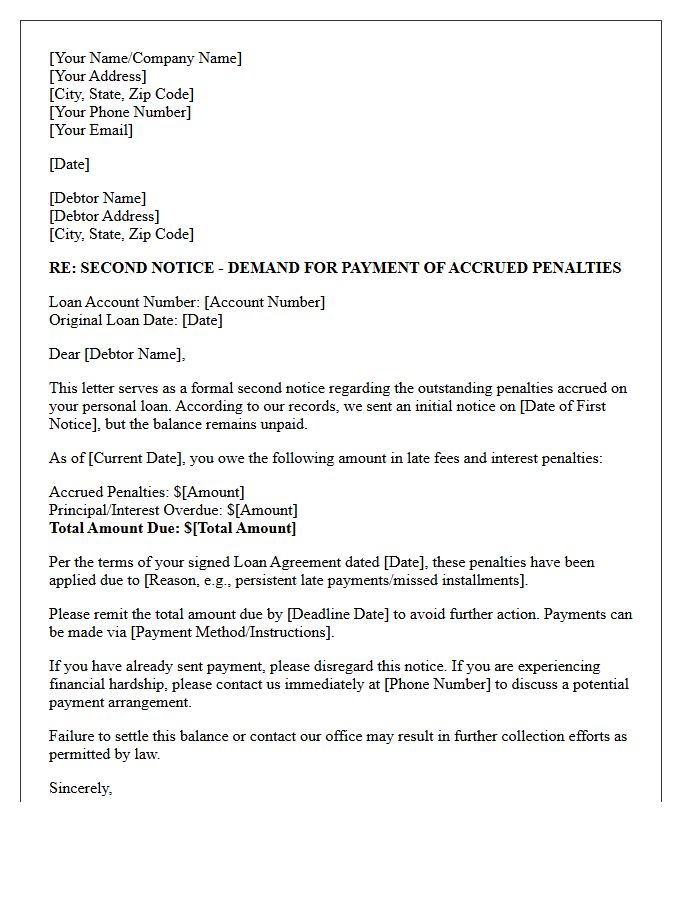

Second Notice Demand Letter for Accrued Personal Loan Penalties

A Second Notice Demand Letter serves as a formal final warning regarding unpaid accrued personal loan penalties. This document outlines the specific late fees, interest surcharges, and the total outstanding balance requiring immediate settlement. It is critical to address this notice promptly to avoid severe consequences, such as negative reports to credit bureaus, professional debt collection actions, or potential litigation. Reviewing the original loan agreement ensures all assessed penalties align with the contract terms. Timely communication with the lender may still allow for a repayment plan or fee waiver before further escalation.

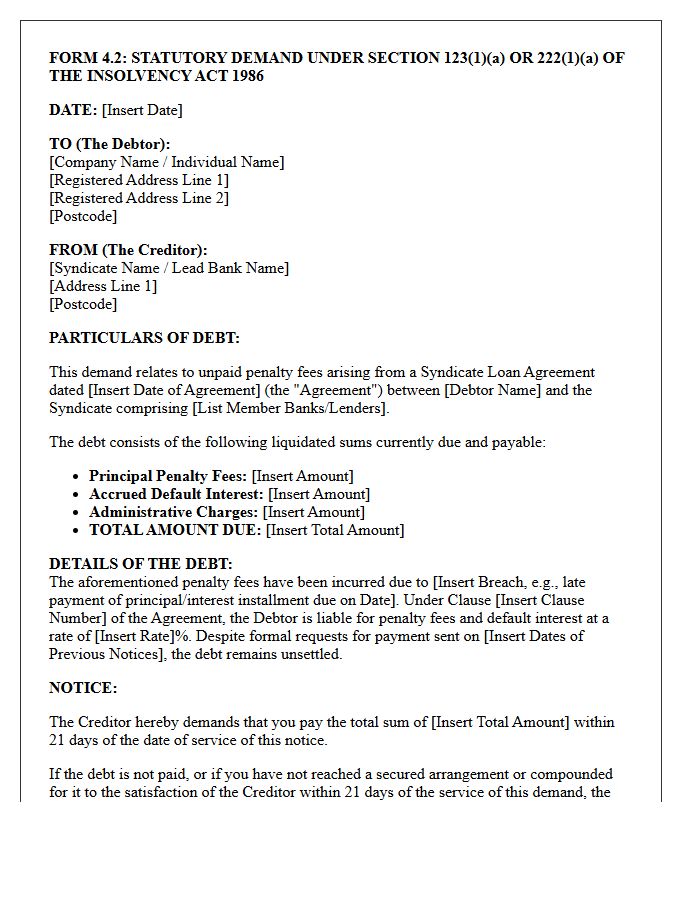

Statutory Demand Letter for Unsettled Syndicate Loan Penalty Fees

A statutory demand is a formal legal notice used to enforce payment of unsettled syndicate loan penalty fees. Under the Insolvency Act, this document serves as a final warning, giving the debtor 21 days to settle the outstanding debt or reach a formal arrangement. Failure to respond can lead to a winding-up petition or bankruptcy proceedings. It is crucial to verify the accuracy of the penalty calculations and the syndicate agreement terms immediately upon receipt to determine if there are grounds to set the demand aside.

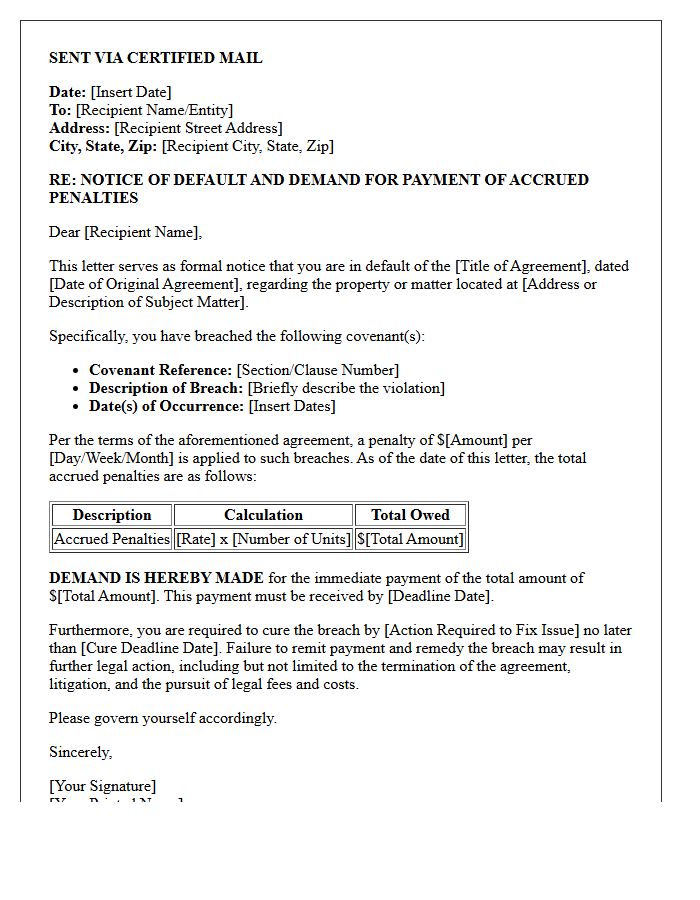

Notice of Default and Demand Letter for Accrued Covenant Breach Penalties

A Notice of Default and Demand Letter is a formal legal document used to notify a party that they have violated specific contractual obligations or property covenants. It serves as an official warning, detailing the exact nature of the breach and the total accrued penalties owed. This letter establishes a strict deadline for the recipient to cure the default and pay outstanding fines before the sender pursues further legal action or foreclosure. It is a critical step in enforcing agreements and protecting the claimant's financial and legal interests.

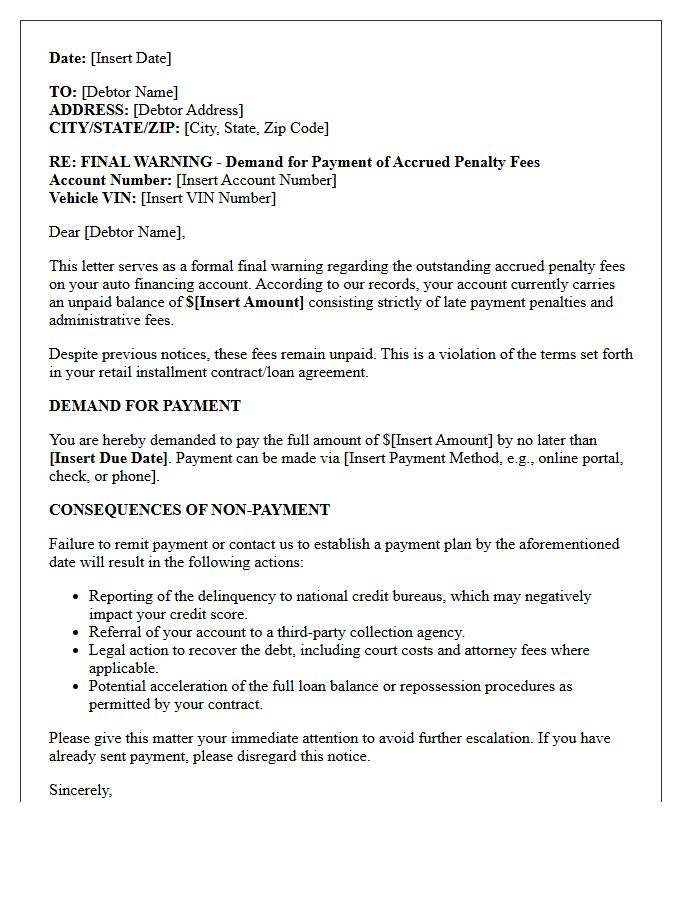

Final Warning Demand Letter for Accrued Auto Financing Penalty Fees

A final warning demand letter is a critical legal notice issued when accrued auto financing penalty fees remain unpaid after prior reminders. It serves as a formal notification that failure to settle the balance immediately will result in repossession or legal action. To protect your credit score, you must respond by the specified deadline. Review the itemized charges for accuracy and consider negotiating a settlement or payment plan to avoid losing your vehicle and facing significant long-term financial damage to your borrower profile.

Official Demand Letter for Delinquent Business Account Penalty Fees

An official demand letter for delinquent business account penalty fees serves as a formal notice to a debtor regarding unpaid balances and accrued charges. It is crucial to clearly state the outstanding amount, the specific nature of the penalties, and the original invoice dates. This document establishes a legal paper trail, demonstrating a good-faith effort to resolve the debt before escalating to litigation or collections. Providing a strict deadline for payment and professional consequences for non-compliance ensures the communication is legally sound and prioritizes immediate debt recovery for your business.

What is a Demand for Payment of Accrued Penalty Fees?

A Demand for Payment of Accrued Penalty Fees is a formal legal notice sent to a debtor requesting the immediate settlement of accumulated late charges, interest, or fines resulting from a breach of contract or overdue balance.

When should a company issue a demand for accrued penalty fees?

A company should issue this demand as soon as a payment exceeds the agreed-upon grace period defined in the service agreement, or when specific contractual milestones are missed, triggering pre-determined financial penalties.

Can penalty fees be legally enforced without a prior agreement?

Generally, penalty fees must be explicitly outlined in a signed contract or terms of service to be legally enforceable. However, statutory interest rates may apply under certain jurisdictions even if a specific penalty amount was not pre-negotiated.

What details must be included in a formal demand letter for penalties?

A formal demand letter should include the original debt amount, the specific clause in the contract authorizing penalties, a detailed breakdown of the accrued fees, the deadline for payment, and the potential legal consequences of non-compliance.

How are accrued penalty fees calculated on overdue accounts?

Accrued penalties are typically calculated as either a fixed one-time late fee or a daily/monthly percentage (compounded or simple interest) applied to the principal balance from the date the payment first became delinquent.

Comments